High-performance Plastic Compounds Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Engineering Plastics, High-performance Thermoplastics), by Resin Type (Polyamide, Fluoropolymers, Polyether Ether Ketone (PEEK), Polycarbonate), by Reinforcement Type (Glass Fiber Reinforced, Carbon Fiber Reinforced), by Processing Method (Injection Molding, Extrusion, Blow Molding), by End Use (Automotive and Transportation, Electrical and Electronics, Aerospace, Healthcare, Industrial, Packaging)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9674 | Industry : Automotive & Transportation | Available Format :

|

Page : 165 |

High-performance Plastic Compounds Market Overview

The global high-performance plastic compounds market which was valued at approximately USD 9.20 billion in 2025 and is estimated to reach around USD 9.85 billion in 2026, is projected to reach approximately USD 20.60 billion by 2035, expanding at a CAGR of about 8.6% during the forecast period from 2026 to 2035.

Market expansion is primarily supported by increasing demand for lightweight and high strength materials in automotive and aerospace applications, rising adoption of advanced polymers in electrical and electronics manufacturing, and growing need for temperature resistant and chemically stable materials in industrial processing. Continuous material innovation which creates more durable products with better performance advantages establishes a market expansion path in this industry. Government programs which back sustainable material development and advanced manufacturing technologies are driving material adoption in essential regions.

The World Health Organization and other regulatory bodies establish material safety requirements which indirectly affect the development process of non-toxic recyclable polymer compounds that medical and packaging industries use. The industrial policies which back electric mobility and energy efficient infrastructure development lead to increased adoption of high-performance materials in battery systems and electronic components. Public investment in manufacturing modernization together with increasing focus on circular economy practices and emission reduction targets creates market demand throughout Asia Pacific, Europe and North America which present ongoing regulatory alignment and industrial growth as drivers of enduring market evolution.

High-performance Plastic Compounds Market Dynamics

Market Trends

The industry is undergoing a fundamental change toward advanced lightweight sustainable materials which meet current manufacturing needs and environmental regulations. The market shows a significant trend toward bio-based recyclable high-performance polymers because people now prefer products which match their sustainability goals and environmental regulations and which produce fewer environmental damages. Organizations which include the United Nations Environment Program together with global environmental standards all over the world work to create frameworks which help manufacturers implement advanced materials that produce fewer emissions while maintaining better performance throughout their entire lifespan.

Advanced compounding technologies now combine with digital manufacturing systems through automation and industrial modernization efforts. The developments show how they affect product innovation by pushing companies to create products with better thermal resistance and durability and specialized features which help them compete in the market. The automotive electronics and healthcare industries now increasingly adopt precision compounding and material engineering because these technologies match national manufacturing guidelines and industrial development plans of key global markets.

Growth Drivers

The market sees its growth through increasing demand for lightweight high strength materials which the automotive and aerospace industries require as their primary market. The market expansion receives additional support from increased investment in electric mobility development and renewable energy infrastructure establishment and advanced electronics manufacturing facilities. Government programs which promote energy efficiency through emission reduction initiatives receive backing from International Energy Agency regulatory bodies to drive advanced polymer solution adoption in battery systems and energy efficient components.

The growth of electrical and electronics industries creates essential support for increased adoption in the market. The demand for high performance compounds will remain strong during the entire forecast period because manufacturers now focus on creating efficient products with thermal stability and miniaturized design. Advanced materials will find their way into future electronic systems through national industrial policies and semiconductor development programs which China, Japan and South Korea have established to promote semiconductor technology.

Market Restraints / Challenges

Market expansion faces two major hurdles which need to be addressed before further progress can happen. The markets which depend on petrochemical derivatives face challenges because raw material price fluctuations impact both cost structures and profit margins in those markets. International energy and resource monitoring agencies establish crude oil supply fluctuations and geopolitical uncertainties as the key factors which determine polymer production costs, thus causing price instability throughout the entire production process.

Manufacturers face operational challenges because they must adhere to strict environmental safety regulations and material usage restrictions which constitute their regulatory compliance responsibilities. Companies that need special additives must import these products which brings about two adverse issues for their operations because it raises their costs and interrupts their supply system. The chemical safety regulations which worldwide environmental and health organizations have established require companies to continuously check their product safety and certification status which increases their operational challenges and delays their product entry into the market.

Market Opportunities

The market presents significant opportunities in the development of sustainable and bio based high performance compounds, particularly driven by increasing environmental awareness and regulatory mandates. Companies that produce lightweight recyclable products which have high durability will gain market share from automotive, packaging and healthcare industries. Government-backed sustainability programs together with circular economy frameworks drive businesses to use eco-friendly materials which leads to new product development opportunities and market growth possibilities.

The market offers an important chance to create advanced electric vehicle applications and high-performance electronic applications because the market now needs specialized materials which create high-efficiency products. Advanced manufacturing processes and automation and material science development should lead to better production rates and improved performance of applications. Research and development receive public funding from major economies which supports industrial innovation programs and technology funding initiatives while enabling companies to develop their product lines and create permanent growth pathways.

Global High-performance Plastic Compounds Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 9.20 Billion |

|

Revenue Forecast in 2035 |

USD 20.60 Billion |

|

Growth Rate |

8.6% |

|

Segments Covered in the Report |

Product Type, Resin Type, Reinforcement Type, Processing Method, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Asia Pacific, North America, Europe, Rest of the World |

|

Key Companies |

Arkema, Asahi Kasei Corporation, BASF SE, Celanese Corporation, Covestro AG, DuPont, Evonik Industries AG, LANXESS AG, LG Chem, SABIC |

|

Customization |

Available upon request |

High-performance Plastic Compounds Market Segmentation

By Product Type

The market in 2025 experienced its largest market share through engineering plastics which generated approximately 57% of overall revenue. The material holds significant importance because engineers require it for various industrial applications where its mechanical strength and thermal resistance and dimensional stability qualities are essential. The material usage in industrial settings increases through its compliance with worldwide safety and performance regulations which enhances its acceptance. The demand for lightweight materials in electric vehicles and energy efficient systems keeps increasing which will result in the segment growing at a projected CAGR of 8.2% during the entire forecasting period. The research predicts that high performance thermoplastics will experience the highest growth rate which will reach a CAGR of 9.1% between 2026 and 2035. The segment expands through its growing use in battery components and semiconductor devices and medical equipment.

By Resin Type

Polyamide based compounds accounted for the largest market share in 2025 which generated approximately 29% of total segment revenue. The two elements form a chemical bond which makes the material suitable for different automotive and electrical component applications because it has both high strength and chemical resistance. Regulatory standards about safety and emissions reduction which receive backing from global industrial policies drive the increase of polyamide material usage in lightweight vehicle structures and electronic assemblies. The market is expected to grow at a stable rate which will achieve a CAGR of 8.0% during the forecasting period. Fluoropolymers and polyether ether ketone-based compounds are expected to achieve the highest growth rate which will result in a CAGR of 9.3% between 2026 and 2035. The demand for materials with excellent thermal stability and chemical resistance together with long lasting performance in critical applications drives growth in aerospace systems and medical devices.

By Reinforcement Type

Glass fiber reinforced compounds held the largest share in 2025 which accounted for nearly 48% of segment revenue. The material achieves market domination because it provides cost savings and improves mechanical strength together with making its use possible in automotive and construction and industrial sectors. Government initiatives which promote energy efficiency together with lightweight materials in transportation systems drive the growth of reinforced compounds usage in structural and semi structural components. The market will experience a growth rate of 8.1% from 2025 to 2030. Carbon fiber reinforced compounds will experience the highest growth rate which will reach a CAGR of 9.4% between 2026 and 2035. The market expands because industrial sectors adopt high-performance applications which need materials that provide both exceptional strength and reduced weight for aerospace applications and electric vehicles. The market expansion of carbon fiber solutions occurs through industrial innovation programs and research funding which drive advanced composites development.

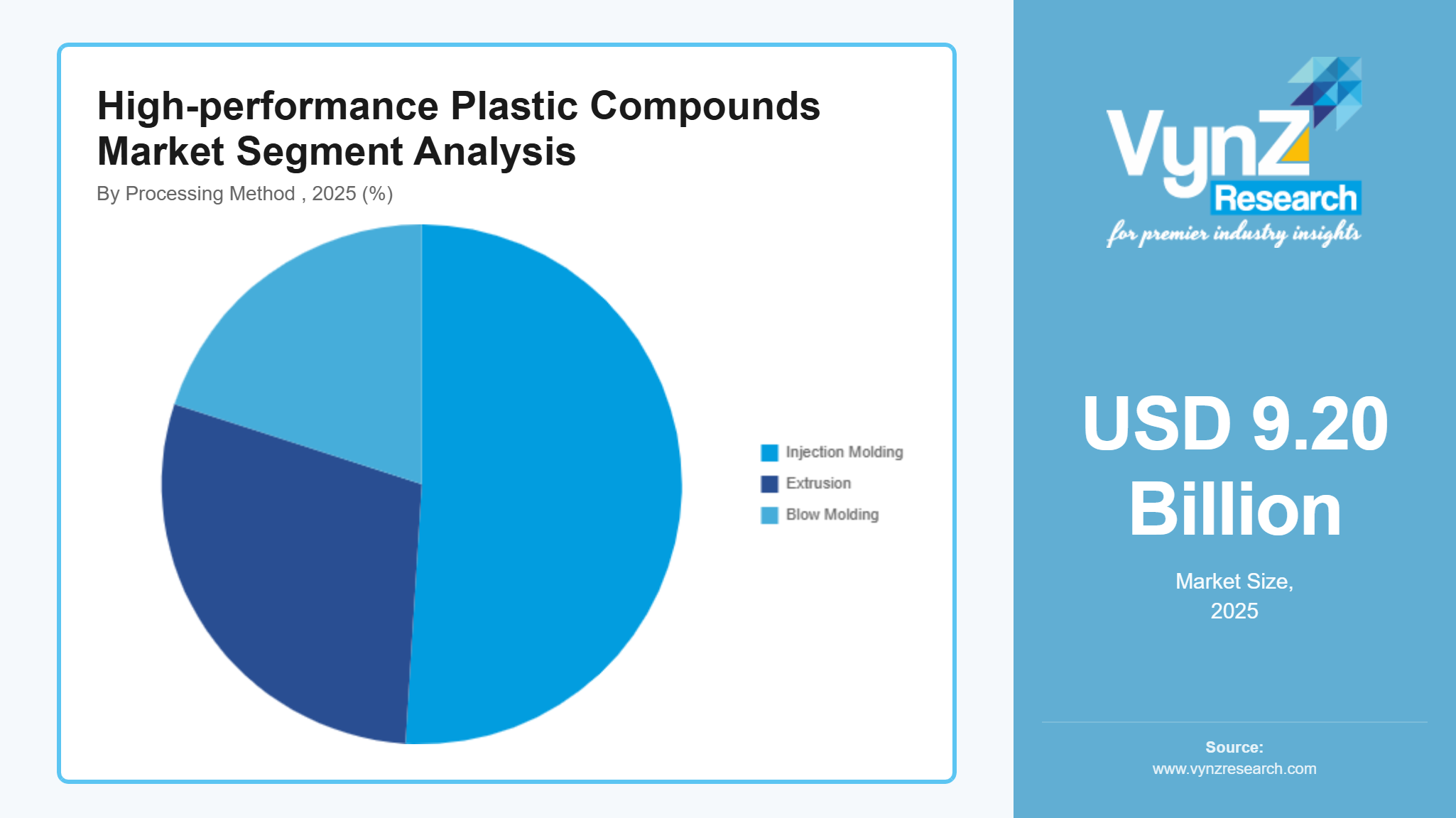

By Processing Method

Injection molding held the largest market share in 2025 which accounted for approximately 51% of total market revenue. The system maintains its dominant position because it achieves high production efficiency while allowing design flexibility and it can produce complex components through mass manufacturing. Industrial automation initiatives and government backed manufacturing policies together with their support for scalable and cost-effective production methods drive adoption. The market will experience a growth rate of 8.0% which will remain constant throughout the entire forecasting period. Extrusion and blow molding processes will achieve the highest growth rate which will result in a CAGR of 8.8% between 2026 and 2035. The demand for continuous production of high-performance materials which companies use in packaging piping and insulation applications drives market growth. The segment continues to grow through the development of new processing technologies together with the rising investment in manufacturing facilities.

By End Use

The automotive and transportation sector held the largest market share in 2025 which accounted for approximately 34% of total market revenue. The two elements create market dominance through their ability to produce lightweight materials which enhance fuel efficiency and cut down emissions. The International Energy Agency and other agencies support regulatory frameworks which promote electric mobility and energy efficient vehicles to drive advanced polymer compound adoption in vehicle manufacturing. The market will achieve a growth rate of 8.3% which will continue throughout the entire forecasting period. The electrical and electronics sector shows the highest growth potential which will achieve a CAGR of 9.2% between 2026 and 2035. The market expands because increasing demand for miniaturized components which offer superior thermal and electrical properties drives the need for high performance components. The adoption of semiconductor and electronics manufacturing initiatives from government agencies in the Asia Pacific region accelerates industry transformation. The healthcare and aerospace and industrial sectors drive continued growth because they need durable materials which can deliver high precision solutions.

Regional Insights

Asia Pacific

The Asia Pacific region will hold about 34% market share of high-performance plastic compounds in 2025 because industrialization progresses and automotive production increases and electronics manufacturing grows in China, India, Japan and South Korea. Shanghai, Shenzhen, Mumbai and Tokyo as main industrial centers lead to rising requirements for advanced polymer compounds which find usage in automotive and electrical and industrial sectors. The region sees greater use of lightweight and high-performance materials because government policies for manufacturing expansion and energy efficient technology development match International Energy Agency guidelines.

North America

The advanced manufacturing capabilities and aerospace and automotive industries and innovative material usage drive North America to maintain 27% of the market in 2025. The United States and Canada continue to experience steady demand for high performance compounds which find applications in aerospace engineering and medical devices and energy systems. Agencies like the Environmental Protection Agency and the Department of Energy conduct regulatory oversight functions to safeguard environmental and performance standards compliance, which helps to create materials that meet sustainability and efficiency criteria.

Europe

The market reached 23% in 2025 because European countries including Germany, France, Italy and the United Kingdom enforce strict environmental protection rules and prioritize sustainability and maintain established industrial systems. The key cities of Berlin, Paris and Milan function as main centers for automotive engineering and advanced manufacturing and industrial innovation. The European Commission and environmental agencies establish regulatory frameworks which drive organizations to embrace recyclable materials and materials that emit low levels of pollutants, leading to increased usage of high-performance plastic compounds in different fields.

Rest of the World

The market shares distribution for 2025 shows approximately 16% of the market belongs to the rest of the world which contains Latin America, the Middle East and Africa. Rising industrialization and infrastructure development and advanced materials adoption in construction and energy sectors drive growth in these regions. The industrial activities and manufacturing sector in Brazil, the United Arab Emirates and South Africa show gradual development, which leads to increasing demand for high performance compounds.

Competitive Landscape / Company Insights

The market is a moderately competitive field because both global and regional companies use material innovation, strategic pricing and capacity expansion to establish stronger market positions. Companies are increasing their research and development investments while they develop advanced compounding technologies to support growing industrial needs. Product development processes now depend on safety standards and regulatory frameworks which agencies like the Environmental Protection Agency and European Chemicals Agency have established. The competitive landscape in major regions of the world continues to evolve because companies maintain ongoing investment in both sustainable materials and high-performance applications.

Mini Profiles

Arkema focuses on advanced polymer materials and specialty compounds, supported by strong innovation capability and sustainability driven product development, strengthening its position across automotive, electronics, and industrial applications globally.

BASF SE operates in premium chemical and materials segments, emphasizing high performance engineering plastics and customized solutions, supported by large scale production networks and strong global supply chain integration.

Covestro AG leverages advanced material science expertise and strategic partnerships to expand market presence, focusing on high quality polycarbonates and polyurethane based solutions across automotive and electronics industries.

DuPont focuses on diversified high-performance materials and specialty compounds, supported by strong research and development capabilities, enabling innovation driven solutions for electronics, healthcare, and industrial applications worldwide.

SABIC operates in large scale petrochemical and advanced materials segments, emphasizing cost efficient production and global distribution strength, supported by integrated manufacturing facilities and strong international market reach.

Key Players

- Arkema

- Asahi Kasei Corporation

- BASF SE

- Celanese Corporation

- Covestro AG

- DuPont

- Evonik Industries AG

- LANXESS AG

- LG Chem

- SABIC

Recent Developments

In March 2026, BASF SE announced expansion of its engineering plastics production capacity in Asia to support rising demand from automotive and electronics sectors. The initiative focuses on strengthening high performance material supply chains and enhancing sustainable manufacturing efficiency across key industrial markets.

In September 2025, Covestro AG expanded its polycarbonate and polyurethane materials portfolio with increased investment in circular economy solutions. The development supports lightweight automotive applications and energy efficient electronics components across global markets.

In December 2025, Evonik Industries AG introduced new high performance polymer solutions aimed at advanced medical and industrial applications. The company emphasized innovation in specialty materials designed for durability, thermal resistance, and precision engineering.

In May 2025, LG Chem expanded its advanced materials division with increased focus on high performance plastic compounds for electric vehicles and electronics industries. The initiative strengthens its position in lightweight and high durability polymer solutions across global supply chains.

In May 2025, Celanese Corporation enhanced its engineered materials segment through capacity expansion in high performance thermoplastics. The development supports growing demand from automotive safety components and industrial applications.

Global High-performance Plastic Compounds Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Engineering Plastics

- High-performance Thermoplastics

Resin Type Insight and Forecast 2026 - 2035

- Polyamide

- Fluoropolymers

- Polyether Ether Ketone (PEEK)

- Polycarbonate

Reinforcement Type Insight and Forecast 2026 - 2035

- Glass Fiber Reinforced

- Carbon Fiber Reinforced

Processing Method Insight and Forecast 2026 - 2035

- Injection Molding

- Extrusion

- Blow Molding

End Use Insight and Forecast 2026 - 2035

- Automotive and Transportation

- Electrical and Electronics

- Aerospace

- Healthcare

- Industrial

- Packaging

Global High-performance Plastic Compounds Market by Region

- North America

- By Product Type

- By Resin Type

- By Reinforcement Type

- By Processing Method

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Resin Type

- By Reinforcement Type

- By Processing Method

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Resin Type

- By Reinforcement Type

- By Processing Method

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Resin Type

- By Reinforcement Type

- By Processing Method

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for High-performance Plastic Compounds Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Resin Type

1.2.3. By

Reinforcement Type

1.2.4. By

Processing Method

1.2.5. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Engineering Plastics

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. High-performance Thermoplastics

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Resin Type

5.2.1. Polyamide

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Fluoropolymers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Polyether Ether Ketone (PEEK)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Polycarbonate

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Reinforcement Type

5.3.1. Glass Fiber Reinforced

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Carbon Fiber Reinforced

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Processing Method

5.4.1. Injection Molding

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Extrusion

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Blow Molding

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By End Use

5.5.1. Automotive and Transportation

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Electrical and Electronics

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Aerospace

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Healthcare

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Industrial

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Packaging

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Resin Type

6.3. By

Reinforcement Type

6.4. By

Processing Method

6.5. By

End Use

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Resin Type

7.3. By

Reinforcement Type

7.4. By

Processing Method

7.5. By

End Use

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Resin Type

8.3. By

Reinforcement Type

8.4. By

Processing Method

8.5. By

End Use

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Resin Type

9.3. By

Reinforcement Type

9.4. By

Processing Method

9.5. By

End Use

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Arkema

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Asahi Kasei Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

BASF SE

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Celanese Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Covestro AG

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

DuPont

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Evonik Industries AG

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

LANXESS AG

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

LG Chem

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

SABIC

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

High-performance Plastic Compounds Market