U.S. TIC Market for Automotive Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In house, Outsourced), by Application (Passenger vehicles, Commercial vehicles), by End Use (Automotive OEMs, Component manufacturers, Aftermarket service providers)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9672 | Industry : Automotive & Transportation | Available Format :

|

Page : 130 |

U.S. TIC Market for Automotive Industry Overview

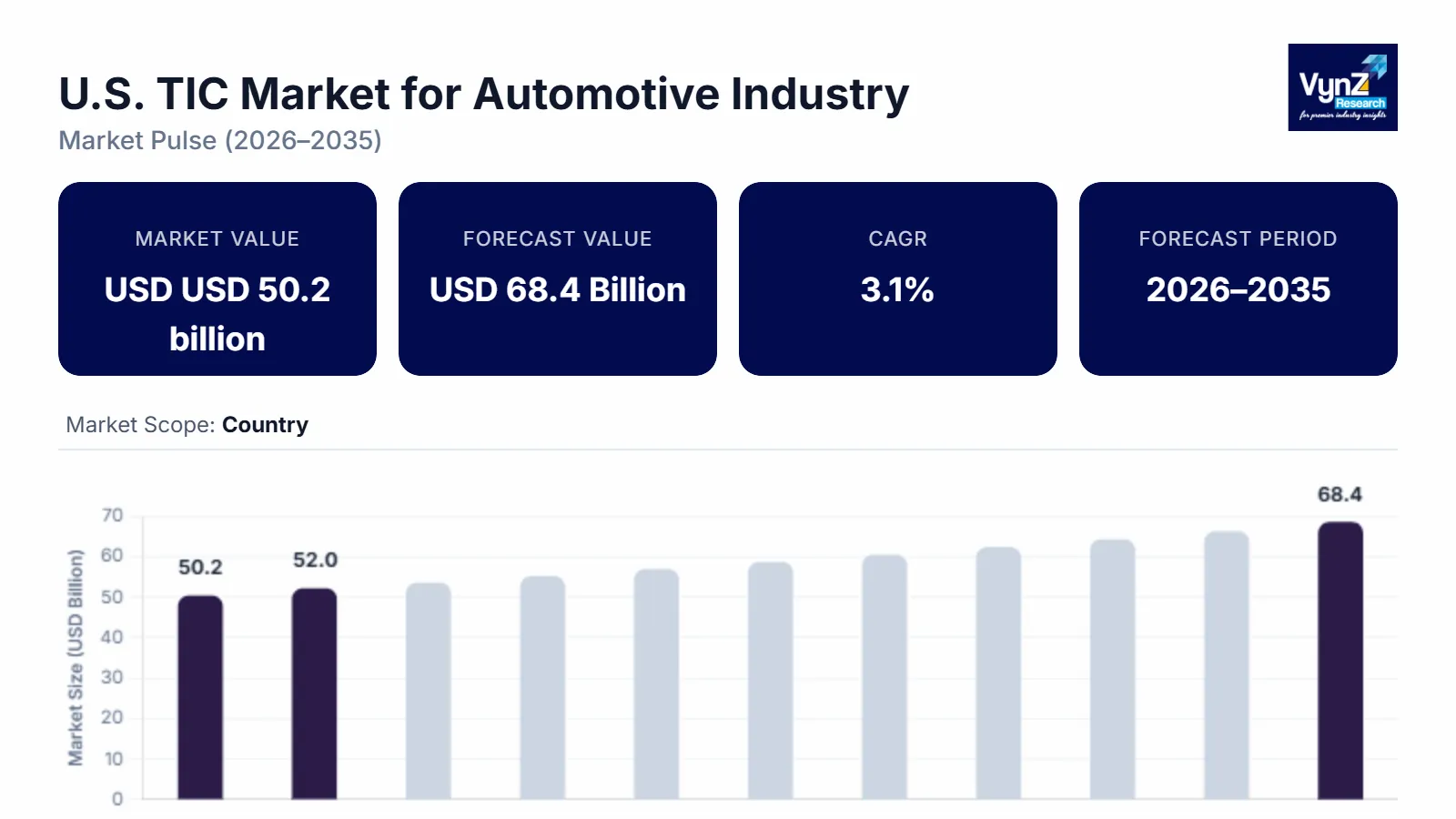

The US TIC market for automotive industry market, which was valued at approximately USD 50.2 billion in 2025 and is estimated to rise further up to almost USD 52.0 billion by 2026, is projected to reach around USD 68.4 billion by 2035, expanding at a CAGR of about 3.1% during the forecast period from 2026 to 2035.

The market expansion occurs because businesses must follow strict regulatory standards while automotive systems become increasingly complex and vehicle safety standards receive more attention so companies adopt advanced testing and certification solutions. The market shows growth through three factors which include the higher demand for compliant automotive components, the continuous development of regulatory systems and safety initiatives that receive backing from the National Highway Traffic Safety Administration and World Health Organization in California, Michigan and Texas.

U.S. TIC Market for Automotive Industry Dynamics

Market Trends

The industry is currently undergoing significant technological changes because businesses are now buying products that help them meet compliance standards and implement digital quality control systems. The market landscape today is shaped by automated testing and digital inspection systems, which modern automotive validation programs use to achieve their goals of efficiency and traceability and cost efficiency. The National Highway Traffic Safety Administration and the International Organization for Standardization support frameworks that establish safety standards and certification standards, which drive organizations to implement emerging inspection technologies. The pattern of increasing regulatory digital transition and technological developments and regulatory changes drives the development of connected vehicle ecosystems. The market development process is currently undergoing changes because these developments create new service delivery methods, which lead companies to establish integrated compliance systems and superior validation capabilities to gain market advantage.

Growth Drivers

The market is experiencing growth because increasing safety compliance requirements and regulatory scrutiny create ongoing demand for testing services across vehicle manufacturing and component validation processes. The automotive industry expansion is accelerating market growth because electric vehicle infrastructure and advanced mobility solutions receive more funding for their production and development. The National Highway Traffic Safety Administration and World Health Organization road safety guidelines require testing and certification processes to protect public safety through testing and certification. The increasing complexity of automotive electronics and software systems has become a crucial factor that drives their adoption throughout the industry. The testing and inspection certification service market will maintain strong demand throughout the forecast period because manufacturers focus on compliance and performance reliability and safety validation.

Market Restraints / Challenges

The market experiences growth potential, but it encounters specific obstacles that restrict its business development. The market entry and operational productivity of smaller service providers and cost-sensitive businesses face challenges from regulatory complexity and changing compliance standards. The government reports and regulatory frameworks create certification timelines and documentation requirements that result in increased operational delays for service providers. Service providers face operational difficulties because they need both advanced testing facilities and trained technical staff to deliver services. The requirement to use high-cost testing equipment and specialized personnel and dynamic testing methods generates both cost pressures and limitations on scalability, which reduce market performance in times of economic instability and variable automotive demand.

Market Opportunities

The market provides substantial business potential through validation services for advanced mobility and electric vehicles, which have emerged because of technological progress and the rapid move toward electrification and vehicle connectivity. The automotive industry customers will enhance their demand for testing services, which will benefit companies that deliver high-performance testing solutions that combine automated functions into a complete testing system. Digital compliance platforms and remote inspection capabilities present key market potential. Smart validation systems and data-driven certification processes create new business opportunities. The National Highway Traffic Safety Administration and World Health Organization road safety framework support initiatives that will boost demand through their service enhancements and artificial intelligence testing solutions.

U.S. TIC Market for Automotive Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 50.2 Billion |

|

Revenue Forecast in 2035 |

USD 68.4 Billion |

|

Growth Rate |

3.1% |

|

Segments Covered in the Report |

Service Type, Sourcing Type, Application, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

West, Midwest, South, Northeast, Others |

|

Key Companies |

Applus+, Bureau Veritas SA, DEKRA SE, Eurofins Scientific, Intertek Group Plc, SGS SA, TUV Rheinland AG, TUV SUD AG, UL Solutions Inc, DNV Group |

|

Customization |

Available upon request |

U.S. TIC Market for Automotive Industry Segmentation

By Service Type

At 48%, testing services achieved the largest market share for 2025 because automotive electronics and emission systems and safety validation requirements across vehicle types showed increasing complexity which drove testing service demand. The National Highway Traffic Safety Administration and other agencies strengthened their regulatory enforcement which created greater demand for standardized testing protocols used in electric and autonomous vehicle systems testing. Manufacturers and suppliers have strengthened their segment dominance through increased usage of software validation together with performance benchmarking as a result of this development.

Inspection services will grow steadily at 2.8% during the forecast period from 2026 to 2035 because real time quality assurance and compliance monitoring throughout production processes have become essential. Certification services will experience the most rapid growth because businesses need to create standardized compliance documentation to meet regulatory requirements and cross border trade rules and comply with international standards. The market growth for testing and certification solutions leads service providers to build their testing capabilities which helps to grow their business.

By Sourcing Type

In house services held a majority share of 57% in 2025 because automotive manufacturers wanted to control their quality validation processes and protect their intellectual property and complete projects faster. OEMs operate testing facilities which help them meet safety standards and performance requirements while maintaining their production equipment efficiency.

Outsourced services are seeing rapid growth which will continue into the future with a CAGR of 3.5% because businesses need to cut costs while they require specialized knowledge. Manufacturers can decrease their capital costs through independent service providers who provide advanced testing infrastructure and certification capabilities and regulatory compliance solutions. Internal quality systems gain operational flexibility through third party validation while customer acquisition expands to all parts of the automotive value chain.

By Application

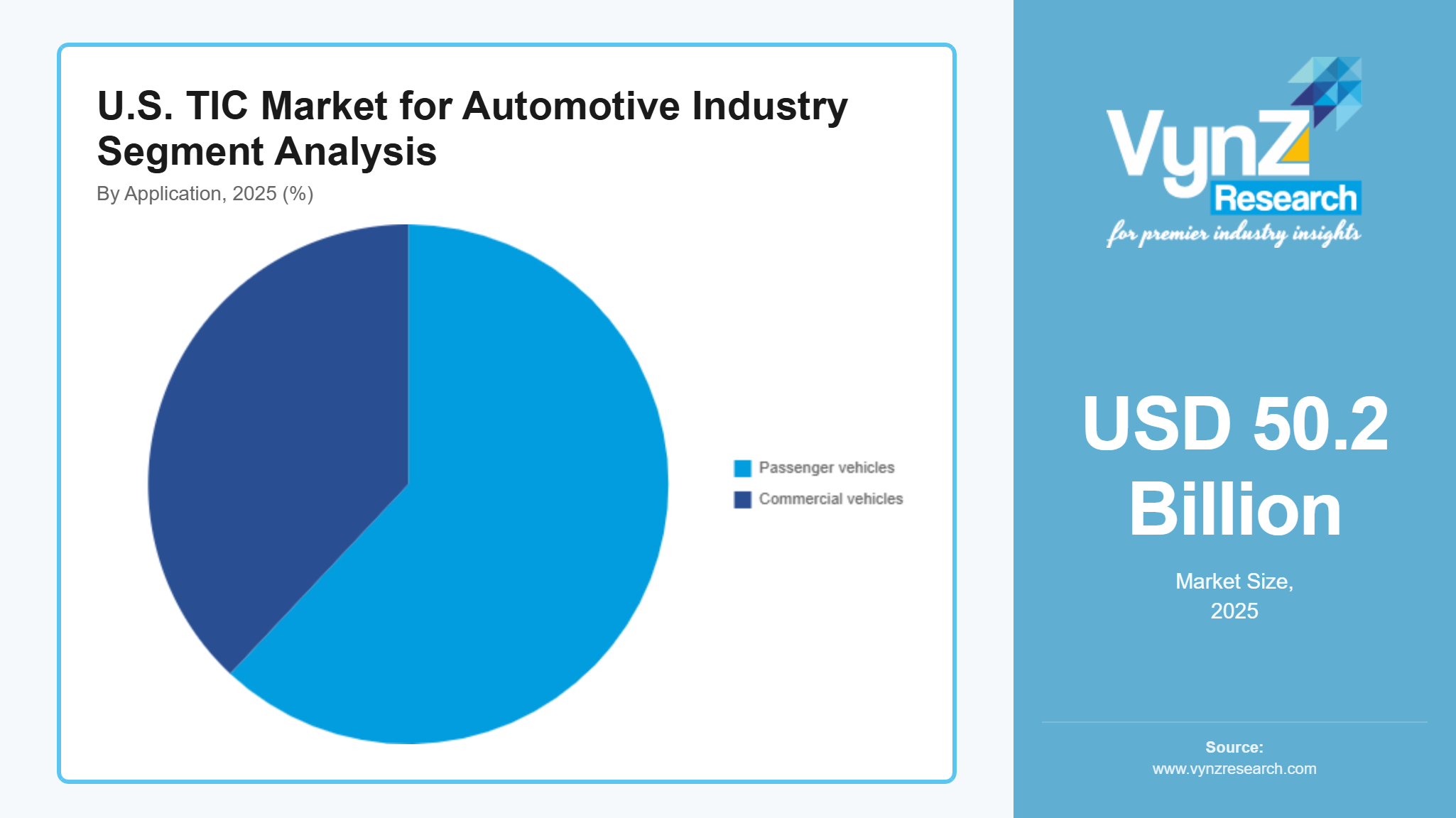

Passenger vehicles accounted for the largest share in 2025 because they produced 62% of total revenue through high production rates and rising consumer demand for safety compliant vehicles and ongoing development of advanced driver assistance systems. Passenger vehicle manufacturing requires testing and certification based on national and international safety mandates which regulatory frameworks enforce.

The commercial vehicle market will experience quick growth because it will achieve a 3.3% CAGR between 2026 and 2035 due to logistics investment and fleet modernization and emission compliance needs. The auto industry will see rising demand for inspection and certification services because electric commercial vehicle adoption increases and heavy-duty vehicle regulations become stricter. Industrial and transportation sector growth continues because these factors drive expansion in both sectors.

By End Use

Automotive OEMs generated the highest revenue share in 2025 with 54% because their production needs and regulatory compliance and advanced safety technology integration requirements drove their operations. The need for complete testing and validation procedures across manufacturing sites receives strengthening support from government safety programs and regulatory mandates.

The component manufacturing sector will keep expanding at 3.2% because component production outsourcing growth accompanies rising demand for quality assurance standards across all supply chains. Aftermarket service providers will experience slow business expansion because vehicle maintenance needs and periodic inspection requirements and regulatory compliance checks will drive their operations. All end use segments continue to see demand because safety compliance requirements and lifecycle validation processes have become increasingly important.

Regional Insights

West

The West region owned 28% of the market in 2025 because advanced automotive technology hubs exist there and electric and autonomous vehicles become more common in the area. California and Washington establish themselves as innovation centers which create demand for advanced testing and certification services. The National Highway Traffic Safety Administration implements safety standards and regulatory frameworks which manufacturers must follow to achieve uniform compliance across their production processes. Government initiatives that support clean mobility and emission reduction together with US Environmental Protection Agency environmental programs create stronger regional market performance because they both increase testing requirements and validation processes.

Midwest

The Midwest region supported 26% of the market in 2025 because it has an established automotive manufacturing base and multiple OEMs and component suppliers. Michigan and Ohio require inspection and certification services because they have large vehicle production operations. The region develops through its manufacturing facilities modernization and its development of advanced quality assurance systems. The automotive production networks maintain steady demand because government industrial programs and workforce development initiatives drive testing infrastructure investments while safety and emission standards continue to evolve.

South

The South region maintained 24% of the market in 2025 because automotive assembly plants expand and electric vehicle manufacturing investments increase. Texas and Tennessee have become production hubs which create demand for testing and certification services. The region develops through infrastructure development and industrial policies and increasing global automotive manufacturer participation. Inspection and validation services remain necessary because organizations must comply with federal safety standards and environmental compliance programs which then create long-term market expansion for the region.

Northeast

The Northeast region has a market share of 20% in 2025 because it features technological innovations and research-based automotive development and advanced testing facilities. New York and Massachusetts are developing next-generation mobility solutions which include connected and autonomous vehicles that require advanced validation and certification systems. Government research programs and regulatory compliance requirements will create a higher demand for testing services that use high precision measuring equipment. The remaining market demand is met by the smaller regions.

Competitive Landscape / Company Insights

The market operates as a moderately competitive market because established global and regional service providers compete with established companies through their technological advancements and their development of new services and their expansion into new markets. Companies are increasingly investing in digital testing platforms, automation technology and advanced validation systems to enhance their competitive position in the market. The National Highway Traffic Safety Administration enforces regulatory frameworks and compliance standards which force organizations to develop new innovative products and improve existing product quality according to International Organization for Standardization global standards.

Mini Profiles

Applus+ focuses on testing, inspection, and certification services, supported by strong global presence, sector expertise, and diversified service portfolio across automotive, industrial, and energy sectors, ensuring compliance and operational efficiency.

Bureau Veritas SA operates in premium and compliance-driven segments, emphasizing quality assurance, regulatory certification, and risk management services, supported by strong brand credibility and extensive global network across automotive and industrial sectors.

DEKRA SE leverages advanced testing infrastructure, strategic partnerships, and strong presence in automotive safety and inspection services to expand market reach and enhance compliance capabilities across vehicle and component validation segments.

Eurofins Scientific focuses on specialized testing and analytical services, supported by strong laboratory network, technical expertise, and expanding capabilities in automotive material testing and environmental compliance solutions across global markets.

Intertek Group Plc operates in mass and industrial segments, emphasizing performance testing, certification, and assurance services, supported by global reach, digital capabilities, and strong client relationships across automotive manufacturing and supply chains.

Key Players

- Applus+

- Bureau Veritas SA

- DEKRA SE

- Eurofins Scientific

- Intertek Group Plc

- SGS SA

- TUV Rheinland

- AG

- TUV SUD AG

- UL Solutions Inc

- DNV Group

Recent Developments

In May 2025, Applus+ expanded its automotive testing infrastructure in North America to support electric vehicle validation and advanced safety compliance requirements. In November 2025, the company strengthened its digital inspection capabilities to improve certification efficiency and real time compliance monitoring.

In July 2025, Eurofins Scientific enhanced its automotive materials testing services by expanding laboratory capabilities focused on emission and environmental compliance. In October 2025, the company upgraded its analytical testing solutions to align with evolving regulatory standards in vehicle manufacturing.

In June 2025, TUV Rheinland AG expanded its automotive certification services for connected and autonomous vehicle systems, aligning with emerging regulatory frameworks. In December 2025, the company invested in advanced testing technologies to improve safety validation and compliance processes.

In August 2025, UL Solutions Inc introduced new testing protocols for electric vehicle battery safety and performance evaluation across North America. In November 2025, the company expanded its certification services to address increasing demand for advanced mobility compliance solutions.

In September 2025, DNV Group enhanced its assurance services by integrating digital risk assessment tools for automotive supply chains. In December 2025, the company expanded its testing and certification capabilities to support sustainability and safety requirements in next generation automotive technologies.

U.S. TIC Market for Automotive Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In house

- Outsourced

Application Insight and Forecast 2026 - 2035

- Passenger vehicles

- Commercial vehicles

End Use Insight and Forecast 2026 - 2035

- Automotive OEMs

- Component manufacturers

- Aftermarket service providers

U.S. TIC Market for Automotive Industry by Region

- West

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Midwest

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- South

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Northeast

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Others

- By Service Type

- By Sourcing Type

- By Application

- By End Use

Table of Contents for U.S. TIC Market for Automotive Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Application

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. U.S. Market Estimate and Forecast

4.1. U.S. Market Overview

4.2. U.S. Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Passenger vehicles

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial vehicles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Automotive OEMs

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Component manufacturers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Aftermarket service providers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. West Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Application

6.4. By

End Use

7. Midwest Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Application

7.4. By

End Use

8. South Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Application

8.4. By

End Use

9. Northeast Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Application

9.4. By

End Use

10. Others Market Estimate and Forecast

10.1. By

Service Type

10.2. By

Sourcing Type

10.3. By

Application

10.4. By

End Use

11. Company Profiles

11.1.

By Consumer Group

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

Athletes

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

Bodybuilders

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Recreational users

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Lifestyle users

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

By Distribution Channel

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

Supermarkets and hypermarkets

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

Convenience stores

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

Specialty stores

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

Online retail stores

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

U.S. TIC Market for Automotive Industry