Automotive Aftermarket Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Replacement Part (Tire, Battery, Brake Parts, Filters, Body Parts, Lighting & Electronic Components, Wheels, Exhaust Components, Engine Components), by Service Channel (DIY (Do-It-Yourself), DIFM (Do-It-For-Me), OE (Original Equipment)), by Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV)), by Distribution Channel (Retailers, Wholesalers & Distributors, Online Platforms / E-commerce), by End User (Individual Vehicle Owners, Fleet Operators, Repair Workshops / Service Centers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9665 | Industry : Automotive & Transportation | Available Format :

|

Page : 187 |

Automotive Aftermarket Overview

The automotive aftermarket which was valued at approximately USD 466.2 billion in 2025 and is estimated to reach around USD 507.5 billion in 2026, is projected to reach close to USD 892.2 billion by 2035, expanding at a CAGR of about 6.5% during the forecast period from 2026 to 2035.

The automotive aftermarket market is driven by the growing number of vehicles in operation worldwide and the increasing average age of vehicles, which raises the demand for replacement parts, maintenance, and repair services. Brakes, filters, batteries, tires, and engine parts must be changed on a regular basis as consumers hold their vehicles longer thus selling aftermarket parts. The growth of the independent repair shops and service centers is also part of the growth of the market as these centers depend on the aftermarket product extensively to offer low-cost repair solutions.

Moreover, there has been increased accessibility to products and transparency in prices to consumers and workshops as the e-commerce platform and online automotive parts retailers have continued to grow rapidly. The increasing number of vehicles owned by people in emerging markets also translates into increased demand of regular servicing and spares. The vehicles, electronic systems, and other connected components are also generating a demand of specialized tools and advanced replacement parts due to the technological advancements of the vehicles. Besides, the governmental regulations concerning the vehicle safety checks and emission limitations stimulate the regular maintenance and parts changing, which further promotes the growth of the automotive aftermarket market.

Automotive Aftermarket Market Dynamics

Market Trends

The expansion of e-commerce platforms for automotive parts has become a significant trend in the automotive aftermarket market, as digital marketplaces are transforming how consumers and repair shops purchase vehicle components. It improves the level of transparency and trust in the buying decisions made by customers as they can simply compare the prices, product features, and the reviews left by others through online platforms. Large aftermarket suppliers and distributors are turning to online sales and distribution to access more customers and simplify the inventory process. Another benefit of e-commerce is that it allows delivery to be faster due to the better logistics networks and regional warehouses, less time on the vehicle is spent on repair. The Production Linked Incentive (PLI) Scheme for the Automobile and Auto Component Industry, approved by the Government of India, has a budgetary outlay of approximately ₹25,938 crore (about USD 3.5 billion) to strengthen domestic automotive manufacturing and supply chains. Moreover, online shops assist home vehicle masters, as well as professional mechanics, with finding a great number of authentic and compatible parts. Increase in mobile application and digital payment systems also makes the purchase processes easier.

Growth Drivers

The increasing global vehicle parc and aging vehicles is a major growth driver for the automotive aftermarket market. With the overall growth in the number of cars on the road all over the whole world, the necessity of routine repair and maintenance as well as the need of replacement parts is also heightened. Consumers in most regions are retaining their vehicles longer because of the expensive nature of new vehicles and the enhanced durability of vehicles that also result in an increased average age of their vehicles. The policy promotes the retirement of old and unfit vehicles through a nationwide ecosystem of Automated Testing Stations (ATS) and Registered Vehicle Scrapping Facilities (RVSF). More than 60 scrapping facilities across 17 states and over 75 automated testing stations have been established to support vehicle inspection and recycling infrastructure. The automobiles of older models usually need more service and change of components like braking systems, batteries, filters, tires, and suspension components. This pattern contributes greatly to the increase in demand for aftermarket products and services. Also aged cars usually demand specialized maintenance and upgrades to keep the performance and safety standards.

Market Restraints / Challenges

The increasing availability of counterfeit and low-quality automotive parts is a significant challenge for the automotive aftermarket market. Counterfeit components, including brake pads, filters, spark plugs, and engine parts, are often sold at lower prices through informal distribution channels and online marketplaces. The products are usually below the safety and performance standards, and it can result in malfunctions of the vehicle, lower durability, and possible safety hazards to the consumer. The availability of fake components also tarnishes the image of legitimate aftermarket producers besides cutting their income. Moreover, it makes it hard to differentiate between original and counterfeit products not only to customers and repair shops, but also in case such counterfeit items resemble branded packaging to the greatest extent. Governments and industry associations are putting more efforts to fight this problem by tightening regulations, authentication technologies, and awareness campaigns.

Market Opportunities

The growing aftermarket demand for electric vehicle (EV) components is creating significant opportunities in the automotive aftermarket market as global EV adoption continues to accelerate. Due to the growing number of electric cars in operation, the demand in specialized parts of replacement and services like battery, power electronics, thermal management, charging connections, and electric components of the drive is growing. Even though EVs do not actually need as many routine services as a vehicle with an internal combustion engine, some of their parts such as battery, electronic modules, etc. need to be serviced and replaced after some period. This opens new possibilities to aftermarket suppliers, repair shops, and parts sellers to diversify their EV-based product offerings. The Government of India introduced the PM Electric Drive Revolution in Innovative Vehicle Enhancement (PM E-DRIVE) scheme with an allocation of around ₹10,900 crore to promote electric mobility and charging infrastructure development. Moreover, the independent service provider market is moving towards investment in EV diagnostic tools and training of technicians that can assist with the EV repair and maintenance. Another way that EV charging infrastructure and battery refurbishment services contribute to the growth of the aftermarket is the development of the infrastructure.

Global Automotive Aftermarket Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 466.2 Billion |

|

Revenue Forecast in 2035 |

USD 892.2 Billion |

|

Growth Rate |

6.5% |

|

Segments Covered in the Report |

Replacement Part, Service Channel, Vehicle Type, Distribution Channel, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Robert Bosch GmbH, Denso Corporation, ZF Friedrichshafen AG, Continental AG, Magna International Inc., Aisin Corporation, Valeo SE, Bridgestone Corporation, Michelin Group, The Goodyear Tire & Rubber Company, 3M Company, Federal-Mogul LLC (Tenneco Inc.) |

|

Customization |

Available upon request |

Automotive Aftermarket Market Segmentation

By Replacement Part

Tire is the largest category with a market share of about 25% in 2025, since they have high replacement rate as compared to other automotive parts. The tires go through continuous wear and tear due to the condition of the roads, driving trends, and environmental exposures, and this necessitates them to be replaced after some time to ensure the safety and performance of the vehicle. The passenger cars, commercial fleet, and logistics operators all need tire change regularly to meet the safety standards. Demand is further escalated by seasonal changing the tires in the colder geographies and the increasing car pools. Moreover, the use of ridesharing, delivery services and fleet operations has increased tire consumption.

Lighting & Electronic Components is the fastest-growing category with a CAGR of 6.7% during the forecast period, because of the growing development of the use of electronic systems in the vehicles. New and existing vehicles are also getting advanced driver assistance systems (ADAS), sensors, and infotainment systems as well as LED lighting technologies. These are parts that need special replacement and upgrade with time, thus forming robust aftermarket demand. Moreover, the swift transition to connected cars and electric cars is escalating the consumption of advanced electronic units. The demand is also dictated by the increasing consumer behavior towards vehicle customization like the use of a better LED lighting system.

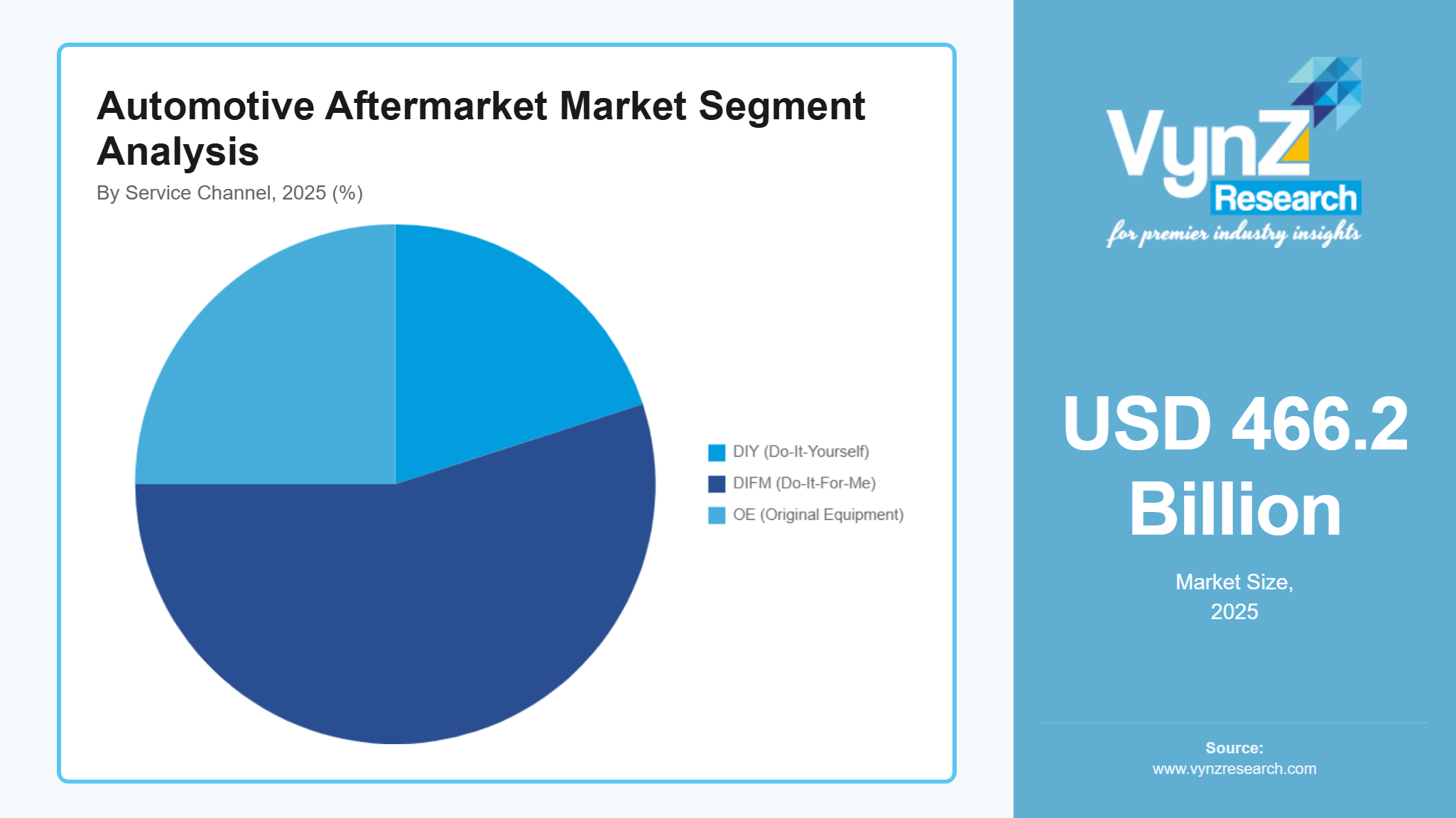

By Service Channel

DIFM (Do-It-For-Me) is the largest category with a market share of about 55% in 2025, due to the increasing complexity of modern vehicles and the need for professional repair services. Many vehicle owners prefer authorized service centers or independent workshops to handle maintenance tasks such as brake repairs, engine diagnostics, and electronic system troubleshooting. The growing use of computerized vehicle systems requires specialized tools and trained technicians, which further supports the DIFM model. Fleet operators and commercial vehicle owners also rely heavily on professional service providers for timely maintenance. Additionally, time constraints and lack of technical expertise among vehicle owners reduce the adoption of DIY repairs.

DIY (Do-It-Yourself) is the fastest-growing category with a CAGR of 6.9% during the forecast period, supported by the increasing availability of online automotive parts and repair tutorials. E-commerce platforms provide consumers with easy access to a wide range of automotive components, tools, and instructional content. Vehicle owners are increasingly performing basic maintenance tasks such as replacing filters, batteries, and lighting components themselves to reduce service costs. The rise of digital platforms and mobile applications that provide step-by-step repair guidance further encourages DIY adoption. In addition, younger vehicle owners and automotive enthusiasts are showing greater interest in personal vehicle maintenance.

By Vehicle Type

Passenger cars is the largest category with a market share of about 65% in 2025, due to the large global passenger vehicle fleet and the high demand for routine maintenance and replacement parts. Most vehicles on the road are passenger cars especially within urban regions and emerging economies where people are owning personal vehicles. The frequent servicing needs like tire change, brake, parts of the engine, and replacement of the battery promote high aftermarket demand. Also, due to the rising rate of aging passenger cars, the demand of parts of replacement also rises.

Light Commercial Vehicles (LCV) is the fastest-growing category with a CAGR of 7.1% during the forecast period, because of the accelerated growth of e-commerce, point-to-point delivery services, and city logistics systems. Companies are facing the need to use light commercial vehicles in transporting goods and this intensifies the demands of vehicle use and maintenance. The constant use will increase the wear and tear of tires, brakes, and suspension systems. There is also increased LCV sales in the world because of the development of small enterprises, as well as logistics startups.

By Distribution Channel

Wholesalers & Distributors is the largest category with a market share of about 45% in 2025, due to their central role in the automotive aftermarket market supply chain. These intermediaries connect manufacturers with retailers, repair workshops, and service centers, ensuring the efficient distribution of automotive parts. Large distribution networks allow wholesalers to manage inventory, logistics, and bulk procurement efficiently. Repair shops and independent service centers often rely on distributors to access a wide variety of parts from multiple brands.

Online Platforms / E-commerce is the fastest-growing category during the forecast period, driven by increasing digitalization and consumer preference for online purchasing. E-commerce platforms enable customers to compare prices, access a wider product selection, and receive parts quickly through improved logistics networks. Many aftermarket manufacturers and distributors are expanding their digital presence to reach a broader customer base. Online platforms also support both DIY consumers and professional repair shops seeking quick and cost-effective procurement.

By End User

Individual vehicle owners is the largest category in 2025, because of the high number of privately owned passenger cars in the world, which need regular maintenance, repair, as well as replacement parts. The aftermarket products that personal vehicle owners purchase regularly include tires, batteries, brake parts, filters, and lighting systems to ensure that the vehicles remain safe and perform well. The growing age of the vehicles is another factor which poses greater demand among the owners of the personal cars in terms of maintenance and spare parts. Secondly, the increase in vehicle ownership in the emerging economies is greatly broadening the segment of individual customers in the aftermarket ecosystem.

Fleet operators is the fastest-growing category during the forecast period, since logistics, ride-hailing, and commercial transportation services have been growing rapidly. Fleet operators must deal with high-traffic numbers of vehicles that must be serviced and maintained regularly, with the components frequently changed to guarantee efficient operations and minimize losses. The rise of e-commerce and the last-mile delivery services have greatly expanded the total commercial fleets, including light commercial vehicles that are utilized in urban deliveries. Fleet managers emphasize on routine servicing and preventive maintenance to maintain the life of the vehicle at a low cost of operation. Moreover, the telematics and fleet management systems are assisting firms to track the performance of their vehicles and arrange maintenance on time.

Regional Insights

North America

North America is the largest regional market for the automotive aftermarket market, supported by a large vehicle parc and a high average vehicle age across the region. The American market controls the regional market because it has many passenger vehicles and a high culture of routine vehicle service and repair. The consumers in the area have the habit of retaining their vehicles longer hence boosting the need to replace car parts like tires, batteries, brakes, and filters. The United States government introduced large-scale incentives under the Inflation Reduction Act (IRA) to strengthen domestic EV battery supply chains and manufacturing capacity. The program provides production tax credits of up to USD 35 per kWh for battery cells and USD 10 per kWh for battery module assembly, encouraging companies to build EV battery factories and component manufacturing facilities in North America. The market activity is further enhanced by an established system of independent repair shops, dealerships, and aftermarket distributors. Additionally, the large availability of aftermarket manufacturers and existing supply chains provide efficient distribution channels of components. The use of modern diagnostic tools and vehicle technologies is also high and creates demand of special parts of replacement.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the automotive aftermarket market, driven by rapid vehicle ownership growth and expanding automotive production. The rise of the numbers of vehicles on the road is very high in such countries like China, India, Japan, and South Korea, which of course automatically increases the demand of maintenance services and spare parts. The growth of the urban transport system and increased disposable income is pushing the consumers to buy and keep their personal vehicles. Moreover, the increased rate of development of online platforms in the market is enhancing the availability of automotive aftermarket market parts in the region. The Chinese government provided approximately USD 230 billion in financial support through purchase incentives, research funding, and infrastructure programs. These policies have helped China become the world’s largest EV market and a global leader in EV battery manufacturing. There is also a move by governments to tighten vehicle safety and emission laws and regulations whereby vehicles are allotted regular checks and replacement of all parts. The intensity of vehicle uses caused by the increasing logistics and ride-hailing industry also contribute to an increased maintenance demand. With the growing fleets of vehicles in the developing economies, Asia-Pacific is witnessing a great demand of aftermarket services and parts.

Europe

Europe maintains a strong presence in the automotive aftermarket market due to its large vehicle base and strict vehicle safety and emission regulations. Germany, the United Kingdom, France, and Italy are all countries with established automotive and developed networks of aftermarket services. The regulatory structures demand consistent checks and routine repairs to the vehicles, and this factor helps to ensure the constant demand of the replacement parts. The European Commission estimates that the policy could generate about €4.8 billion in additional growth and investment in the EU repair market. The directive aims to strengthen the repair economy by encouraging investment in repair services, spare-parts supply chains, and refurbishment businesses across Europe. Moreover, the area boasts of many old automobiles, which take more repairs and replacement of parts. The increased use of electric cars is also introducing fresh aftermarket business options to specialty parts and diagnostic instruments. Distribution networks are also strong besides the availability of major automotive parts manufacturers, which contribute to market growth in Europe.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing gradual expansion in the automotive aftermarket market as vehicle ownership increases. In Latin America, countries such as Brazil and Mexico are witnessing growing demand for vehicle maintenance services due to expanding passenger vehicle fleets. The Middle East is seeing increased aftermarket demand driven by high vehicle usage and challenging environmental conditions that accelerate component wear. In Africa, rising urbanization and economic development are supporting gradual growth in vehicle ownership and aftermarket service demand. The expansion of independent repair shops and automotive parts distributors is improving market accessibility in these regions. Although market maturity varies across countries, increasing vehicle fleets and infrastructure development are expected to support steady aftermarket market growth.

Competitive Landscape / Company Insights

The automotive aftermarket market is highly competitive and moderately fragmented, characterized by the presence of large global component manufacturers, specialized aftermarket suppliers, and extensive distributor networks. The leading multinational corporations like Robert Bosch GmbH, Denso Corporation, ZF Friedrichshafen AG and Continental AG hold their strong positions due to their wide scope of products which also include braking systems, electronic components, filters, ignition systems as well as advanced vehicle diagnostics equipment. These firms enjoy good research and development facilities and global supply chains to supply replacement parts of high quality that can fit in the latest technologies of vehicles. The Goodyear tire and rubber company, Michelin group and tire manufacturers like Bridgestone corporation have a lot of influence in the aftermarket because of the level at which tires are replaced, as also because they have a wide distribution network. There are also large automotive parts manufacturers such as Magna International Inc., Aisin Corporation, and Valeo SE that are competing with a variety of drivetrain, lighting and electronic parts both in traditional and electric vehicles. Also, large aftermarket and retail chains like AutoZone, Inc., O’Reilly Automotive, Inc., and Genuine Parts Company are also very important as they provide links between manufacturers and repair shops and consumers via large logistics and retail networks. Another competitive force that worsens the situation is the presence of independent service providers and regional distributors that provide cost-effective parts and maintenance services.

Mini Profiles

Robert Bosch GmbH is one of the largest global suppliers of automotive components and aftermarket solutions, offering a wide range of replacement parts including braking systems, spark plugs, filters, batteries, sensors, and diagnostic equipment while operating an extensive network of service centers and distribution channels across Europe, Asia-Pacific, and North America.

Denso Corporation is a major automotive technology and component manufacturer providing advanced aftermarket products such as engine management systems, ignition components, thermal systems, and electronic modules, supporting both conventional internal combustion vehicles and emerging electric vehicle platforms through its global supply and service network.

ZF Friedrichshafen AG is a leading automotive parts supplier specializing in driveline and chassis technologies, offering aftermarket solutions including transmission components, suspension systems, steering systems, and braking technologies while supporting vehicle maintenance and repair through its global ZF Aftermarket service division.

Continental AG is a global automotive technology company that provides a wide range of aftermarket products such as braking components, electronic systems, sensors, and tires, leveraging its expertise in vehicle safety, connectivity, and automation technologies to support maintenance and performance upgrades for modern vehicles.

Bridgestone Corporation is one of the world’s largest tire manufacturers supplying replacement tires and mobility solutions for passenger cars, commercial vehicles, and industrial fleets while operating extensive global distribution networks and service centers that support tire maintenance, monitoring, and replacement services in the automotive aftermarket market.

Key Players

- Robert Bosch GmbH

- Denso Corporation

- ZF Friedrichshafen AG

- Continental AG

- Magna International Inc.

- Aisin Corporation

- Valeo SE

- Bridgestone Corporation

- Michelin Group

- The Goodyear Tire & Rubber Company

- 3M Company

- Federal-Mogul LLC (a subsidiary of Tenneco Inc.)

Recent Developments

January 2026 – Robert Bosch GmbH announced expansion of its automotive aftermarket market digital diagnostics platform, introducing advanced cloud-based vehicle diagnostic tools and predictive maintenance solutions for independent repair workshops worldwide.

November 2025 – Continental AG expanded its global automotive aftermarket market distribution network by opening new logistics centers in Europe and North America to improve spare parts availability and delivery efficiency for repair shops and retailers.

September 2025 – ZF Friedrichshafen AG introduced a new range of electric vehicle aftermarket components, including electric driveline parts and advanced braking systems designed to support the growing global EV fleet.

July 2025 – Bridgestone Corporation launched a next-generation smart tire monitoring solution for fleet operators, integrating sensor technology and digital platforms to improve predictive maintenance and tire lifecycle management.

May 2025 – Denso Corporation expanded its aftermarket product portfolio by introducing new advanced ignition coils, fuel system components, and thermal management parts designed for modern hybrid and electric vehicles.

Global Automotive Aftermarket Coverage

Replacement Part Insight and Forecast 2026 - 2035

- Tire

- Battery

- Brake Parts

- Filters

- Body Parts

- Lighting & Electronic Components

- Wheels

- Exhaust Components

- Engine Components

Service Channel Insight and Forecast 2026 - 2035

- DIY (Do-It-Yourself)

- DIFM (Do-It-For-Me)

- OE (Original Equipment)

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

Distribution Channel Insight and Forecast 2026 - 2035

- Retailers

- Wholesalers & Distributors

- Online Platforms / E-commerce

End User Insight and Forecast 2026 - 2035

- Individual Vehicle Owners

- Fleet Operators

- Repair Workshops / Service Centers

Global Automotive Aftermarket by Region

- North America

- By Replacement Part

- By Service Channel

- By Vehicle Type

- By Distribution Channel

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Replacement Part

- By Service Channel

- By Vehicle Type

- By Distribution Channel

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Replacement Part

- By Service Channel

- By Vehicle Type

- By Distribution Channel

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Replacement Part

- By Service Channel

- By Vehicle Type

- By Distribution Channel

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Automotive Aftermarket Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Replacement Part

1.2.2. By

Service Channel

1.2.3. By

Vehicle Type

1.2.4. By

Distribution Channel

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Replacement Part

5.1.1. Tire

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Battery

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Brake Parts

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Filters

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Body Parts

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Lighting & Electronic Components

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Wheels

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Exhaust Components

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.1.9. Engine Components

5.1.9.1. Market Definition

5.1.9.2. Market Estimation and Forecast to 2035

5.2. By Service Channel

5.2.1. DIY (Do-It-Yourself)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. DIFM (Do-It-For-Me)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. OE (Original Equipment)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Vehicle Type

5.3.1. Passenger Cars

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Light Commercial Vehicles (LCV)

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Heavy Commercial Vehicles (HCV)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Distribution Channel

5.4.1. Retailers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Wholesalers & Distributors

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Online Platforms / E-commerce

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Individual Vehicle Owners

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Fleet Operators

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Repair Workshops / Service Centers

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Replacement Part

6.2. By

Service Channel

6.3. By

Vehicle Type

6.4. By

Distribution Channel

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Replacement Part

7.2. By

Service Channel

7.3. By

Vehicle Type

7.4. By

Distribution Channel

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Replacement Part

8.2. By

Service Channel

8.3. By

Vehicle Type

8.4. By

Distribution Channel

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Replacement Part

9.2. By

Service Channel

9.3. By

Vehicle Type

9.4. By

Distribution Channel

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Robert Bosch GmbH

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Denso Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

ZF Friedrichshafen AG

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Continental AG

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Magna International Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Aisin Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Valeo SE

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Bridgestone Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Michelin Group

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

The Goodyear Tire & Rubber Company

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

3M Company

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Federal-Mogul LLC (a subsidiary of Tenneco Inc.)

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Automotive Aftermarket