Automotive AI Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Technology (Machine Learning, Deep Learning, Computer Vision, Natural Language Processing (NLP), Context Awareness), by Application (Advanced Driver Assistance Systems (ADAS), Autonomous Driving, Human–Machine Interface (HMI), Predictive Maintenance, Infotainment Systems, Fleet Management), by Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Autonomous Vehicles), by Level of Automation (Level 1 (Driver Assistance), Level 2 (Partial Automation), Level 3 (Conditional Automation), Level 4 (High Automation), Level 5 (Full Automation)), by End Use (OEMs (Original Equipment Manufacturers), Aftermarket)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9659 | Industry : Automotive & Transportation | Available Format :

|

Page : 195 |

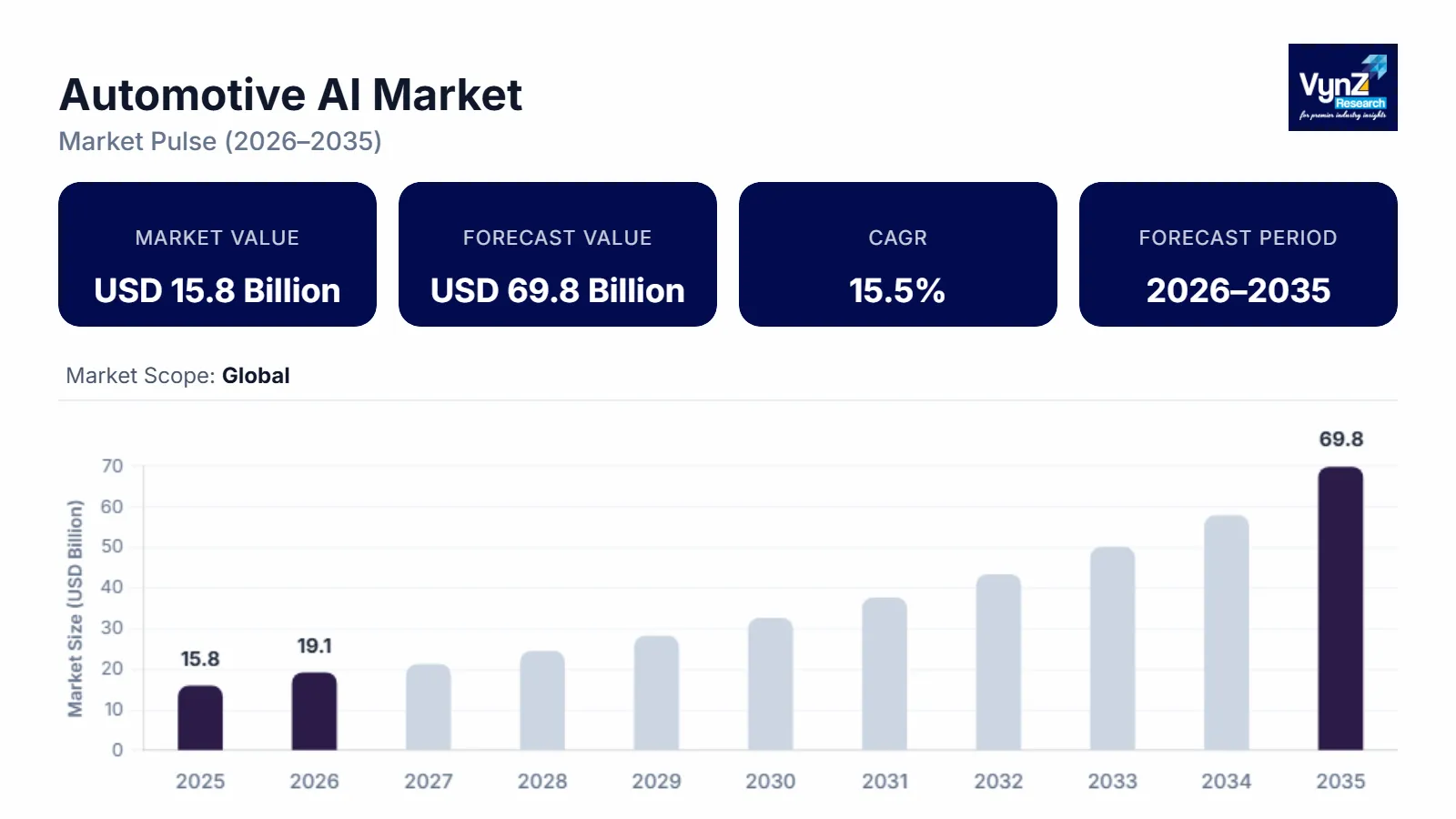

Automotive AI Market Overview

The automotive AI market which was valued at approximately USD 15.8 billion in 2025 and is estimated to reach around USD 19.1 billion in 2026, is projected to reach close to USD 69.8 billion by 2035, expanding at a CAGR of about 15.5% during the forecast period from 2026 to 2035.

The automotive AI market is driven by the rapid adoption of advanced driver assistance systems (ADAS) and autonomous driving technologies across passenger and commercial vehicles. Lane-keeping assistance, adaptive cruise control, automatic emergency braking and driver monitoring systems are examples of AI-based features that automakers are increasingly incorporating into their vehicles to enhance vehicle safety and lower accident rates.

Regulatory bodies and governments in key automotive economies such as North America, Europe, and Asia-Pacific are also requiring vehicles to be equipped with safety technologies which is increasing the rate of the adoption of AI-driven systems. Due to the need to have safer and smarter vehicles, manufacturers are putting a lot of money in artificial intelligence to develop real-time decision making, object detection, and predictive driving functions. Sensors, cameras, radar, LiDAR, and onboard computing systems are installed on modern vehicles and provide the generation of large amounts of data, which requires effective processing by AI algorithms. Machine learning and deep learning models are assisting automobile companies to process this data to support navigation, predicting traffic, voice recognition, predictive maintenance, and personalised in-car experiences.

Automotive AI Market Dynamics

Market Trends

The integration of autonomous driving technologies is one of the most significant trends in the Automotive AI Market, as automakers increasingly focus on developing vehicles capable of performing driving tasks with minimal or no human intervention. Artificial intelligence is an important element of autonomous systems because it helps to create real-time perception, decision-making, and vehicle control by applying machine learning, computer vision, and deep learning algorithms. Current autonomous vehicles are based on a set of sensors, including cameras, radar, LiDAR, ultrasonic sensors, and high-performance processors that receive and analyse large amounts of data at any given time to interpret the conditions of the road and identify obstacles in its path, recognise traffic lights and signs, and anticipate the actions of other vehicles and pedestrians. The European Union has allocated about €1.5 billion under the Horizon Europe program to support research in artificial intelligence, advanced sensors, LiDAR, radar, and intelligent vehicle technologies used in autonomous driving systems. Automobile companies and technology players are spending heavily on Level 2, Level 3, and beyond automation where AI is used to enhance the accuracy of driving, minimize human error, and improve road safety. Moreover, AI chips, edge computing, and high-speed connectivity are improving, and it is becoming possible to process complex data within milliseconds, which is vital to safe autonomous operation. The adoption of self-driving technology is also being accelerated by governments in a few countries who are supporting the technology by pilot programs and regulative frameworks.

Growth Drivers

The automotive AI market will experience significant growth through the increased use of AI chips and edge computing in cars as the latest cars need fast data processing and decision-making units to provide high impression of safety, automation, and connectivity features. Different automotive systems like advanced driver assistance systems (ADAS), autonomous driving, driver monitoring, and intelligent infotainment produce enormous amounts of data in form of camera, radar, LiDAR, and other onboard sensors, and they are supposed to be processed in real-time to achieve safe and efficient vehicle control. Artificial intelligence chips such as GPUs, NPUs and automotive-specific processors can allow vehicles to do more intricate calculations on-board without always having to be connected to the cloud. The Chinese government created the third phase of the National Integrated Circuit Industry Investment Fund with about 344 billion yuan (approximately $47.5 billion), making it the largest semiconductor investment program in the country. Edge computing enables data to be processed directly within the vehicle to minimize latency, decrease response time, and increase reliability, that is, which is very important in applications involving safety. The automakers are also collaborating more closely with semiconductor and technology firms to create high-performance AI hardware platforms to be used in automotive. Moreover, the move toward software-defined cars and autonomous transportation is also causing the demand to expand to higher-powered systems on board.

Market Restraints / Challenges

Data privacy and cybersecurity risks represent a major challenge for the Automotive AI Market, as modern AI-enabled vehicles rely heavily on connected technologies, cloud platforms, and real-time data exchange to support advanced functions such as autonomous driving, navigation, remote diagnostics, and infotainment services. Such vehicles actively gather and process huge amounts of sensitive information, such as driver actions, position data, vehicle status, and interaction with external systems, posing a higher risk of information security violations and unauthorized access. In case of an insufficient cybersecurity, it is possible that hackers obtain the control of essential car systems, and it can influence braking, steering, or acceleration, which is a serious safety issue. Moreover, network-based attacks can be directed to the connected cars communicating via vehicle-to-everything (V2X), which also demands safe communication protocols. Strict data protection and car cybersecurity standards are being implemented in various governments and regulatory bodies in different countries, which add to the compliance requirements of the manufacturers. Companies in the automotive industry need to spend a lot of money on encryption, secure software structure, protection of over-the-air updates, and the use of ongoing monitoring systems to avoid cyber threats.

Market Opportunities

The rising adoption of AI in Advanced Driver Assistance Systems (ADAS) is creating a significant opportunity for the Automotive AI Market, as vehicle manufacturers are increasingly integrating intelligent safety and automation features to improve driving performance and reduce road accidents. Machine learning, computer vision, and deep learning are artificial intelligence technologies that allow the ADAS functions to process real-time data samples gathered by cameras, radar, LiDAR, and other devices to identify obstacles, identify traffic signs, track the behavior of a driver, and manage the dynamics of the road condition. The adaptive cruise control, lane-keeping assistance, automatic emergency braking, parking assistance, and driver monitoring systems are among the features that are very dependent on AI algorithms to make decisions quickly and correctly. The U.S. government approved the Infrastructure Investment and Jobs Act, which includes $110 billion for roads and transportation projects, $11 billion for transportation safety programs, and $39 billion for transit modernization, along with additional funding for smart infrastructure and advanced mobility technologies. Some of the ADAS capabilities are also becoming mandatory in new vehicles by governments and safety organizations in most countries, which is further increasing the rate at which AI-based systems are being implemented on passenger and commercial vehicles. Moreover, people are getting more insistent on safer and smarter cars so that the automakers are compelled to invest in the development of AI-driven safety systems to stay abreast of the competition.

Global Automotive AI Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 15.8 Billion |

|

Revenue Forecast in 2035 |

USD 69.8 Billion |

|

Growth Rate |

15.5% |

|

Segments Covered in the Report |

Component, Technology, Application, Vehicle Type, Level of Automation, End Use, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

NVIDIA Corporation, Intel Corporation, Qualcomm Incorporated, Tesla, Inc., Robert Bosch GmbH, Continental AG, Denso Corporation, Aptiv PLC, ZF Friedrichshafen AG, Alphabet Inc., Microsoft Corporation, Amazon Web Services, Inc. |

|

Customization |

Available upon request |

Automotive AI Market Segmentation

By Component

Hardware is the largest category with a market share of about 40% in 2025, because automotive AI systems need high-performance processors, sensors, radar, LiDAR and camera modules to process real-time data. These hardware elements are the core of AI-powered cars, and this component is fundamental to ADAS, self-driving, and connected car capabilities. To make cars safe and precise, automakers spend a lot of money on chips and sensor hardware. Hardware demand is also enhanced by the growing nature of sophisticated electronics integration in current vehicles. Its large revenue share is also contributed by high cost of automotive grade semiconductors. The reason is that continuous development of AI chips and sensors in the field keeps it on a first-mover position.

Software is the fastest-growing category with a CAGR of 15.8% during the forecast period, because of the transition to software-defined vehicles and AI-based control systems. Automakers are also using AI algorithms more to do perception, decision making, predictive maintenance, and infotainment. The use of software in the performance of the vehicle is growing due to over-the-air updates and cloud connectivity. The need to autonomous driving platforms and smart user interfaces is increasing at a high pace. With software, upgrades of features can be made continuous without hardware modification.

By Technology

Machine Learning is the largest category with a market share of about 30% in 2025, as it is popular in driver assistance, predictive analytics, object detection, and vehicle behavior analysis. Most of the automotive AI uses machine learning models to analyze sensor data and enhance the accuracy of the decision. It is simpler to apply than other advanced AI technologies and is already in place in most ADAS functions. Machine learning is applied by automakers to predict traffic, monitor the driver, and optimize safety. Its dominance in terms of market share is supported by the wide range of application to various vehicle systems.

Computer Vision is the fastest-growing category with a CAGR of 15.9% during the forecast period, as it is used in model driving and real-time detection of roads. It helps the vehicles to identify pedestrians, road signs, lanes, and other roadblocks through cameras and sensors. The use of self-driving and advanced-level ADAS systems is being boosted by the growing demand of such systems. Accuracy is being improved by improvements in image processing and deep learning models. There are also governments that promote safety technologies based on the visual recognition. The high rate of increase in camera-based monitoring systems favors its vibrant development.

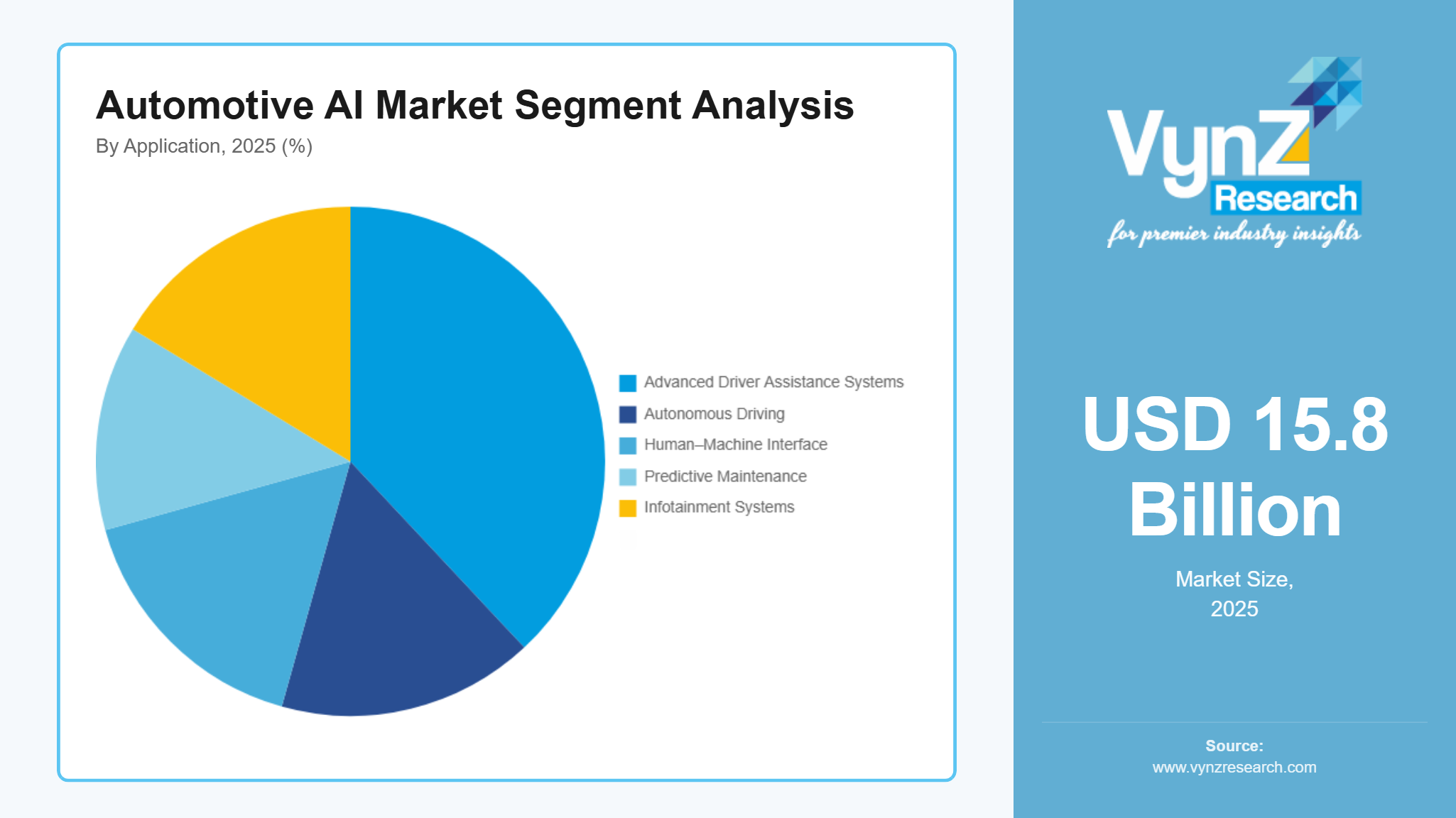

By Application

Advanced Driver Assistance Systems (ADAS) is the largest category with a market share of around 35% in 2025, as majority of the AI features will be initially introduced in passenger cars because of high volume production and the consumer demand to have safety and comfortability. The automakers are concentrating on the implementation of AI in high-end and middle-end vehicles to improve the driving. ADAS, infotainment AI, and driver monitoring are among the most common features used in passenger cars. An increase in the electric and connected cars sales further helps this segment. Its dominant share is enhanced by a high adoption in advanced economies. The sustained upgrade on the consumer cars sustains superiority.

Autonomous Driving is the fastest-growing category with a CAGR of 16.1% during the forecast period, as the electrification and smart mobility are rapidly shifting. AI is vital to EVs, as it is used to control the battery, optimize energy consumption, and predictive maintenance. Electric vehicles are being encouraged in the world as governments use incentives and emission regulations to encourage their use. The EV platforms are additionally more software-based, meaning that it is easier to integrate AI systems. The growth increases with the rise of investment in smart EV technology. This segment is forced to move the quickest by the change toward sustainable transportation.

By Vehicle Type

Passenger Vehicles is the largest category with a market share of about 50% in 2025, since most AI features are first introduced in passenger cars due to high production volume and strong consumer demand for safety and comfort. Automakers focus on integrating AI in premium and mid-range cars to enhance driving experience. Features such as ADAS, infotainment AI, and driver monitoring are widely used in passenger vehicles. Growing sales of electric and connected cars also support this segment. High adoption in developed countries strengthens its leading share. Continuous upgrades in consumer vehicles maintain dominance.

Electric Vehicles is the fastest-growing category during the forecast period, due to the rapid shift toward electrification and smart mobility. EVs rely heavily on AI for battery management, energy optimization, and predictive maintenance. Governments worldwide are promoting electric vehicle adoption through incentives and emission regulations. EV platforms are more software-driven, allowing easier integration of AI systems. Increasing investment in intelligent EV technology accelerates growth. The transition toward sustainable transportation drives this segment fastest.

By Level of Automation

Level 2 (Partial Automation) is the largest category with a market share of about 35% in 2025, as it is the most common level of automation in the commercial vehicles. Several cars already come with features like adaptive cruise control, lane keeping and automated braking. It is safer and is still controllable by the driver hence acceptable by regulators as well as consumers. Level 2 is an offering that is being considered by most automakers. The cost/functionality ratio favors its supremacy. This segment is largest due to widespread use in mid-range cars.

Level 4 (High Automation) is the fastest-growing category during the forecast period, as more highly autonomous vehicles continue to be developed to provide mobility in the future. Level 4 systems enable vehicles to be driven with no human control under most circumstances, which entails sophisticated AI processing. This level is receiving huge investments by technology firms and car manufacturers. There is rising adoption of smart city projects and robotaxi trials. The advancement of AI chips and sensors facilitate commercialization. The long-term trend is that of driverless transportation, which leads to the rapid growth.

By End Use

OEMs is the largest category with a market share of around 70% in 2025, as most AI technologies are implemented in the process of vehicle production, not in sales. To make vehicles safe and performant, automakers develop AI systems as part of the vehicle architecture. Integration of OEM enables enhanced compatibility with sensors and control units. This segment is supported by the growth of its production of connected and autonomous vehicles. Manufacturers like the use of AI that is installed in factories because it is reliable. OEMs remain powerful due to large investment by automakers.

Aftermarket is the fastest-growing category during the forecast period, because more people are demanding to upgrade their old vehicles to compete with the new AI-based safety and infotainment systems. Drivers are equipping cars with driver monitoring, smart cameras, and navigation AI post purchase. This is encouraged by expansion of related car accessories. Vehicles are also upgraded by the fleet operators to enhance efficiency. Retrofit solutions are being offered at lower cost. The quick development of the aftermarket is promoted by awareness about vehicle safety.

Regional Insights

North America

North America holds a significant share in the Automotive AI Market, supported by the strong presence of leading automotive manufacturers, semiconductor companies, and artificial intelligence technology providers in the United States and Canada. The level of adoption of advanced driver assistance systems, autonomous driving systems and connected vehicle platforms in the region is high and so the use of AI is in demand. Significant innovations in car intelligence are being boosted by the major investments made in self-driving technology by Tesla, NVIDIA and General Motors, among others. The U.S. government passed the CHIPS and Science Act to strengthen domestic semiconductor manufacturing and advanced computing technologies, allocating about $280 billion for semiconductor production, research, and high-performance computing development. The law includes $39 billion in subsidies and $11 billion for semiconductor R&D, supporting chips used in artificial intelligence, autonomous vehicles, and automotive electronics. The government of the U.S. is also engaged in the creation of smart transportation and autonomous mobility, both with the help of funding programs and regulatory frameworks. The billions of dollars under the Infrastructure Investment and Jobs Act to cover intelligent transportation systems, smart roads and vehicle safety technologies indirectly contribute to the adoption of AI in the automotive industry. The good research and development potential and early electric vehicle adoption is also a strong force in the market. North America is enjoying consistent growth due to high consumer demand of high-end vehicles with technology facilitation.

Asia Pacific

Asia-Pacific is the largest and fastest-growing region in the Automotive AI Market, driven by large-scale automobile production and rapid adoption of electric and connected vehicles in countries such as China, Japan, South Korea, and India. China is the biggest automotive market in the world, and it is highly investing in autonomous driving, AI chips, and smart mobility solutions, which is developing high demand on automotive AI technologies. The Japanese government announced a plan to provide about $65 billion (around 10 trillion yen) in public support through 2030 to strengthen domestic semiconductor and artificial intelligence industries, with a strong focus on next-generation chips used in AI, autonomous vehicles, and high-performance computing. Major automotive and electronics manufacturers are found in Japan and South Korea and are actively working on the development of the advanced safety systems and the intelligent vehicle platforms. The area has a productive sector of semiconductor production, affordable production, and governmental programs of electric and autonomous vehicles. The government of China has launched several national initiatives that aid the AI development and intelligent transportation, and India is increasing investment in smart mobility and electric vehicle infrastructure. The growth in disposable income, urbanization, and the demand in safer vehicles is also promoting the use of AI.

Europe

Europe represents a technologically advanced and regulation-driven market, supported by strong automotive manufacturing in Germany, France, Italy, and the United Kingdom. There are very stringent vehicle safety and emission policies in the region, which promote the use of AI-based driver assistant, electric vehicle control, and autonomous driving solutions. Software-defined vehicles and intelligent mobility solutions are the main areas that European automakers are putting their money in to satisfy the future transportation needs. The European Commission’s Vehicle of the Future initiative includes an initial investment of about €250 million for 2023–2024, funded jointly by the European Commission, EU Member States, and industry partners to support research and innovation in next-generation vehicles, including autonomous driving, AI, and software-defined vehicle technologies. The European Union passed several safety requirements compelling new cars to have advanced driver assistance systems, which directly boosts the demand of AI components and software. Moreover, the area is pursuing green mobility, which is causing increased use of electric vehicles based on AI to manage the battery and optimize performance aspects. Innovation is supported by strong funding of research and partnership of automotive firms with technology firms.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, is witnessing gradual growth in the Automotive AI Market due to increasing vehicle production, urbanization, and expansion of smart transportation infrastructure. Brazil and Mexico are among the countries that are empowering their manufacturing automotive companies, and this is boosting the use of AI-based safety and diagnostic systems. Automatic AI technologies have new prospects in the Middle East because of smart cities, self-driving vehicles, and smart traffic control. Gulf governments are encouraging innovation in the mobility and connected vehicle platforms to enhance efficiency in transportation. The African market is in its early stages but evolves slowly as more digital infrastructure is built, and the need to have modern cars increases. Despite the issues in the region that are associated with price and technological skills, it is anticipated that the growth will be aided by enhanced influx of foreign investments and automotive technology upgrading in the long run.

Competitive Landscape / Company Insights

The automotive AI market is moderately consolidated, characterized by the presence of global automotive manufacturers, semiconductor companies, and artificial intelligence technology providers along with emerging software and mobility solution firms. The leading players, including NVIDIA Corporation, Intel Corporation, Qualcomm Incorporated, Tesla, Inc., and Robert Bosch GmbH, are also powerful because of their developed AI chipsets, autonomous driving platforms, and integrated vehicle intelligence solutions. These firms have advantages of having good research and development potential, being strategic partners with car makers and huge manufacturing capacity that enables them to ensure a competitive edge. They are enhancing their market presence through continuous investment in high-performance processors, sensor technologies, and software-defined vehicle architecture.

The industry of large automotive suppliers and technology companies such as Continental AG, Denso Corporation, Aptiv PLC, and ZF Friedrichshafen AG are significant contributors to the delivery of AI-enabled driver assistance systems, vehicle control unit, and intelligent safety technologies applied by global OEMs. Meanwhile, the main technology corporations like Alphabet Inc., Microsoft Corporation, and Amazon Web Services, Inc. are broadening their presence in car AIs by using cloud computing, autonomous driving systems, and vehicle networks. Businesses are moving towards collaborations, joint ventures, and acquisitions to fast-track innovation in autonomous driving, edge computing, and AI-based mobility services. Increasing investment in software platforms, real-time data processing, and cybersecurity solutions are also being seen in the market as manufacturers are looking to establish safer, smarter and fully connected vehicles to accommodate the future mobility needs.

Mini Profiles

Henkel AG & Co. KGaA is a leading global provider of specialty adhesives and electronic materials, NVIDIA Corporation is a leading developer of artificial intelligence computing platforms and automotive AI hardware, offering advanced GPU and AI processor solutions used in autonomous driving, ADAS, and in-vehicle infotainment systems.

Intel Corporation is a major semiconductor and technology company providing AI processors, edge computing solutions, and autonomous driving technologies for the automotive industry. Through its Mobileye division, the company delivers computer vision and driver assistance systems widely used in modern vehicles for safety and automation.

Qualcomm Incorporated is a key provider of automotive AI chipsets and connectivity platforms, offering solutions for connected cars, digital cockpit systems, and advanced driver assistance technologies. Its Snapdragon automotive platforms enable high-performance processing, AI acceleration, and 5G connectivity for next-generation smart vehicles.

Tesla, Inc. is a leading electric vehicle manufacturer known for integrating artificial intelligence into autonomous driving, battery management, and vehicle software systems. The company develops its own AI chips and self-driving software, enabling advanced automation, over-the-air updates, and intelligent vehicle control.

Robert Bosch GmbH is a global automotive technology supplier providing AI-based driver assistance systems, sensors, and vehicle control software used in passenger and commercial vehicles. The company focuses on intelligent mobility, automated driving, and connected vehicle technologies to improve safety and efficiency.

Key Players

- NVIDIA Corporation

- Intel Corporation

- Qualcomm Incorporated

- Tesla, Inc.

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- Aptiv PLC

- ZF Friedrichshafen AG

- Alphabet Inc.

- Microsoft Corporation

- Amazon Web Services, Inc.

Recent Developments

January 2026 – NVIDIA Corporation announced the expansion of its DRIVE automotive AI platform with next-generation AI processors designed to support higher levels of autonomous driving, improved real-time sensor processing, and enhanced safety features for software-defined vehicles.

December 2025 – Intel Corporation, through its Mobileye division, introduced an upgraded autonomous driving system with enhanced computer vision and mapping capabilities aimed at supporting Level 3 and Level 4 automated driving in passenger and commercial vehicles.

October 2025 – Qualcomm Incorporated launched a new Snapdragon automotive AI chipset with improved edge computing performance and integrated 5G connectivity, enabling faster data processing for connected cars, digital cockpit systems, and advanced driver assistance applications.

September 2025 – Tesla, Inc. announced updates to its Full Self-Driving (FSD) software, improving neural network training and real-time decision-making capabilities, along with enhanced over-the-air update features for its electric vehicle lineup.

August 2025 – Robert Bosch GmbH introduced a new generation of AI-based driver assistance sensors combining radar, camera, and ultrasonic technologies to improve object detection accuracy and support future autonomous vehicle platforms.

Global Automotive AI Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Technology Insight and Forecast 2026 - 2035

- Machine Learning

- Deep Learning

- Computer Vision

- Natural Language Processing (NLP)

- Context Awareness

Application Insight and Forecast 2026 - 2035

- Advanced Driver Assistance Systems (ADAS)

- Autonomous Driving

- Human–Machine Interface (HMI)

- Predictive Maintenance

- Infotainment Systems

- Fleet Management

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Autonomous Vehicles

Level of Automation Insight and Forecast 2026 - 2035

- Level 1 (Driver Assistance)

- Level 2 (Partial Automation)

- Level 3 (Conditional Automation)

- Level 4 (High Automation)

- Level 5 (Full Automation)

End Use Insight and Forecast 2026 - 2035

- OEMs (Original Equipment Manufacturers)

- Aftermarket

Global Automotive AI Market by Region

- North America

- By Component

- By Technology

- By Application

- By Vehicle Type

- By Level of Automation

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Technology

- By Application

- By Vehicle Type

- By Level of Automation

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Technology

- By Application

- By Vehicle Type

- By Level of Automation

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Technology

- By Application

- By Vehicle Type

- By Level of Automation

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Automotive AI Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

Vehicle Type

1.2.5. By

Level of Automation

1.2.6. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Machine Learning

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Deep Learning

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Computer Vision

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Natural Language Processing (NLP)

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Context Awareness

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Advanced Driver Assistance Systems (ADAS)

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Autonomous Driving

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Human–Machine Interface (HMI)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Predictive Maintenance

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Infotainment Systems

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Fleet Management

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Vehicle Type

5.4.1. Passenger Vehicles

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Commercial Vehicles

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Electric Vehicles

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Autonomous Vehicles

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Level of Automation

5.5.1. Level 1 (Driver Assistance)

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Level 2 (Partial Automation)

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Level 3 (Conditional Automation)

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Level 4 (High Automation)

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Level 5 (Full Automation)

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.6. By End Use

5.6.1. OEMs (Original Equipment Manufacturers)

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Aftermarket

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Technology

6.3. By

Application

6.4. By

Vehicle Type

6.5. By

Level of Automation

6.6. By

End Use

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Technology

7.3. By

Application

7.4. By

Vehicle Type

7.5. By

Level of Automation

7.6. By

End Use

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Technology

8.3. By

Application

8.4. By

Vehicle Type

8.5. By

Level of Automation

8.6. By

End Use

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Technology

9.3. By

Application

9.4. By

Vehicle Type

9.5. By

Level of Automation

9.6. By

End Use

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

NVIDIA Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Intel Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Qualcomm Incorporated

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Tesla, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Robert Bosch GmbH

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Continental AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Denso Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Aptiv PLC

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

ZF Friedrichshafen AG

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Alphabet Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Microsoft Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Amazon Web Services, Inc.

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Automotive AI Market