Automotive Wiring Harness Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Electric Wires, Connectors, Terminals, Others), by Material (Copper, Aluminum), by Voltage (Low Voltage Wiring Harness, High Voltage Wiring Harness), by Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs), Electric Vehicles (EVs)), by Application (Engine Wiring Harness, Body Wiring Harness, Chassis Wiring Harness, HVAC Wiring Harness, Sensor Wiring Harness, Dashboard / Cabin Wiring Harness), by Distribution Channel (OEM (Original Equipment Manufacturer), Aftermarket)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9665 | Industry : Automotive & Transportation | Available Format :

|

Page : 172 |

Automotive Wiring Harness Market Overview

The automotive wiring harness market which was valued at approximately USD 54.4 billion in 2025 and is estimated to reach around USD 59.2 billion in 2026, is projected to reach close to USD 103.7 billion by 2035, expanding at a CAGR of about 6.4% during the forecast period from 2026 to 2035.

.webp)

The market is primarily driven by the rapid electrification of vehicles and the growing integration of advanced electronic systems in modern automobiles. With the growing use of technologies like advanced driver assist systems (ADAS), infotainment systems, connected vehicle systems, etc., the requirements of complex and high-capacity wiring harness systems have grown substantially. This demand is further precipitated by the global revolution towards electric and hybrid automobiles, which demand large amounts of wiring networks to coordinate battery systems, power distribution and electronic control units.

Besides that, harsh government laws relating to safety and emissions of vehicles are making automakers enhance their vehicles with more sensors, control modules and electronic safety systems, all of which are based on effective wiring harness designs. The emergence of the charge grid for electric cars and government subsidies in favor of the electrification of vehicles are also increasing the production of the EV, thus increasing the consumption of wiring harness. More so, automotive manufacturers are increasingly adopting lightweight material and modular wiring systems, which are enhancing vehicle efficiency as well as expanding the complexity of harness design. Increasing vehicle output in the third world markets more specifically in Asia-Pacific is also boosting the automotive wiring solutions.

Automotive Wiring Harness Market Dynamics

Market Trends

The shift toward lightweight and high-voltage wiring harness systems has become a major trend in the automotive wiring harness market as vehicle manufacturers aim to improve energy efficiency and support advanced vehicle electrification. Electric and hybrid cars, as well as modern cars, need designs operating at high voltage to transmit power between batteries, electric motors, and electronic control systems. Consequently, car manufacturers are moving toward the use of special high-voltage wiring harnesses that can increase the current throughput at the same time providing safety and thermal stability. Meanwhile, the weight reduction is one of the priority tasks since the lighter vehicles are, the fuel efficiency improves, and the driving range of electric vehicles is increased. The Government of India launched the FAME India Scheme Phase-II with a budget of about ₹11,500 crore to accelerate electric vehicle adoption and strengthen EV infrastructure across the country. Moreover, other techniques such as improved cable routing and modular harness designs are also contributing towards a reduction in the complexity and weight of the total wiring. Moreover, the high-voltage harness systems are also equipped with advanced shielding and insulation technologies to compensate thermal, electromagnetic, and electrical faults. Such innovations are in line with the increased use of electric powertrain and high-tech vehicle electronics.

Growth Drivers

The increasing integration of advanced vehicle electronics is a major driver of growth in the automotive wiring harness market. Modern cars are being fitted with a plethora of electronic devices including advanced driver assistance systems (ADAS), infotainment units, digital instrument clusters, navigation systems, and connectivity units. Such technologies are based on complicated electrical networks which demand a lot of wiring harness systems to provide power and data in between various electronic parts and control units. Due to the continued addition of technologies, including adaptive cruise control, lane-keeping assistance, automatic emergency braking, and vehicle-to-everything (V2X) communication, the quantity of sensors, cameras, and electronic control units installed in vehicles only grows. Such an increase in electronic complexity greatly increases the need to have advanced wiring harness design to handle high data transmission and reliable electrical interconnection. The United States government enacted the CHIPS and Science Act, allocating about $106 billion to strengthen domestic semiconductor manufacturing, research, and advanced electronics development. Additionally, the emergence of connected cars and over-the-air software updates enhances further the necessity of effective electrical and data communication systems in cars. In the case of automotive manufacturers, they are also incorporating additional comfort and convenience electronics in the form of sophisticated climate control systems, smart lighting systems, and seat control systems. All these developments raise the amount of wiring per vehicle.

Market Restraints / Challenges

The high cost and weight of complex wiring harness systems act as a significant challenge for the automotive wiring harness market. Modern vehicles require extensive electrical networks to support advanced electronic features, electric powertrains, infotainment systems, and safety technologies, which increases the amount of wiring used in each vehicle. As the number of electronic components and control units grows, wiring harness assemblies become more complex, leading to higher material and production costs. Copper, which is widely used in wiring harnesses due to its excellent conductivity, is expensive and subject to price fluctuations, further increasing manufacturing costs. In addition, large wiring bundles can add considerable weight to vehicles, which negatively impacts fuel efficiency and reduces the driving range of electric vehicles. Automakers are continuously seeking ways to reduce vehicle weight to meet efficiency and emission targets, making heavy wiring systems a design challenge. The installation and assembly of complex harness systems also require significant labor and precision, increasing production time and operational costs. Furthermore, routing large wiring networks within limited vehicle space adds design and engineering difficulties.

Market Opportunities

The rising production and adoption of electric vehicles (EVs) present a significant opportunity for the automotive wiring harness market. EV vehicles have much more complicated electrical systems than hybrid vehicles with internal combustion engines and thus require more advanced wiring harness solutions. EVs have large wiring networks, which control battery packs, electric motors, power electronics, charging systems, and electronics control units. Harcritel The high voltage of EV is especially crucial since it provides safe and efficient power delivery between essential components. The European Union has mobilized more than €250 billion in public and private investment through the European Battery Alliance to develop a regional EV battery and electric mobility ecosystem. With governments in different parts of the globe enacting policies, subsidies, and emission standards to encourage the use of clean transportation, automotive companies are hastening to invest in the production of electric vehicles. This accelerated electrification trend adds additional wiring content per vehicle, generating a great demand of special wiring harness systems. Besides this, the appearance of the fast-charging infrastructure and battery management technologies also contributes to the necessity of the sophisticated electrical connectivity solutions.

Global Automotive Wiring Harness Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 54.4 Billion |

|

Revenue Forecast in 2035 |

USD 103.7 Billion |

|

Growth Rate |

6.4% |

|

Segments Covered in the Report |

Component, Material, Voltage, Vehicle Type, Application, Distribution Channel |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Yazaki Corporation, Sumitomo Electric Industries, Ltd., Aptiv PLC, Leoni AG, Furukawa Electric Co., Ltd., Lear Corporation, THB Group (Kromberg & Schubert), Samvardhana Motherson International Limited, Nexans S.A., Yura Corporation, Fujikura Ltd., PKC Group |

|

Customization |

Available upon request |

Automotive Wiring Harness Market Segmentation

By Component

Electric wires are the largest category with a market share of about 45% in 2025, owing to their necessary functions of carrying electrical power and signals across the entire electrical architecture of the vehicle. Wiring harness systems Wiring harness systems are highly dependent on insulated electric wires to interconnect electronic control units, sensors, battery systems, and infotainment modules. Since vehicles include increasingly more electronic systems like ADAS, connectivity systems, and highly sophisticated safety systems, the number of electric wires needed in each vehicle is growing. They consist of these wires that comprise the backbone of the harness assembly, and they represent a vast share of the material that is used. They are also very reliable, conductive, and flexible and therefore impossible to do away with in automotive electrical networks.

Connectors are the fastest-growing category with a CAGR of about 6.6% during the forecast period, as vehicle electronics have become more complex, and there is the need to have reliable electrical connections to the various systems. Many sensors, control modules, and communication networks are incorporated into the modern vehicles and demand stable connector interfaces. Advanced connectors are in demand due to high-speed data connections, electric vehicle power systems, and modular electrical systems. Compact and high-performance connectors are also becoming a thing in automotive manufacturers to enable them to adopt lightweight designs and enhance durability.

By Material

Copper is the largest category with a market share of about 85% in 2025, primarily due to its superior electrical conductivity, durability, and reliability in automotive electrical systems. Copper wiring is widely used in wiring harnesses because it ensures efficient power transmission and minimal electrical resistance. It also offers excellent thermal stability and corrosion resistance, making it suitable for demanding automotive environments. Most conventional and electric vehicles rely heavily on copper-based wiring for battery systems, sensors, lighting, and infotainment components. Additionally, well-established manufacturing processes and supply chains for copper wiring further support its dominant market share. These factors collectively make copper the preferred material in automotive wiring harness production.

Aluminum is the fastest-growing category with a CAGR of about 6.9% during the forecast period, driven by the automotive industry's increasing focus on reducing vehicle weight and improving energy efficiency. Aluminum wiring offers significant weight reduction compared with copper, which helps enhance fuel efficiency in conventional vehicles and extend the driving range of electric vehicles. Automakers are gradually adopting aluminum conductors in selected wiring harness applications where lightweight design is critical. Technological advancements in aluminum connectors and insulation materials are also improving reliability and performance.

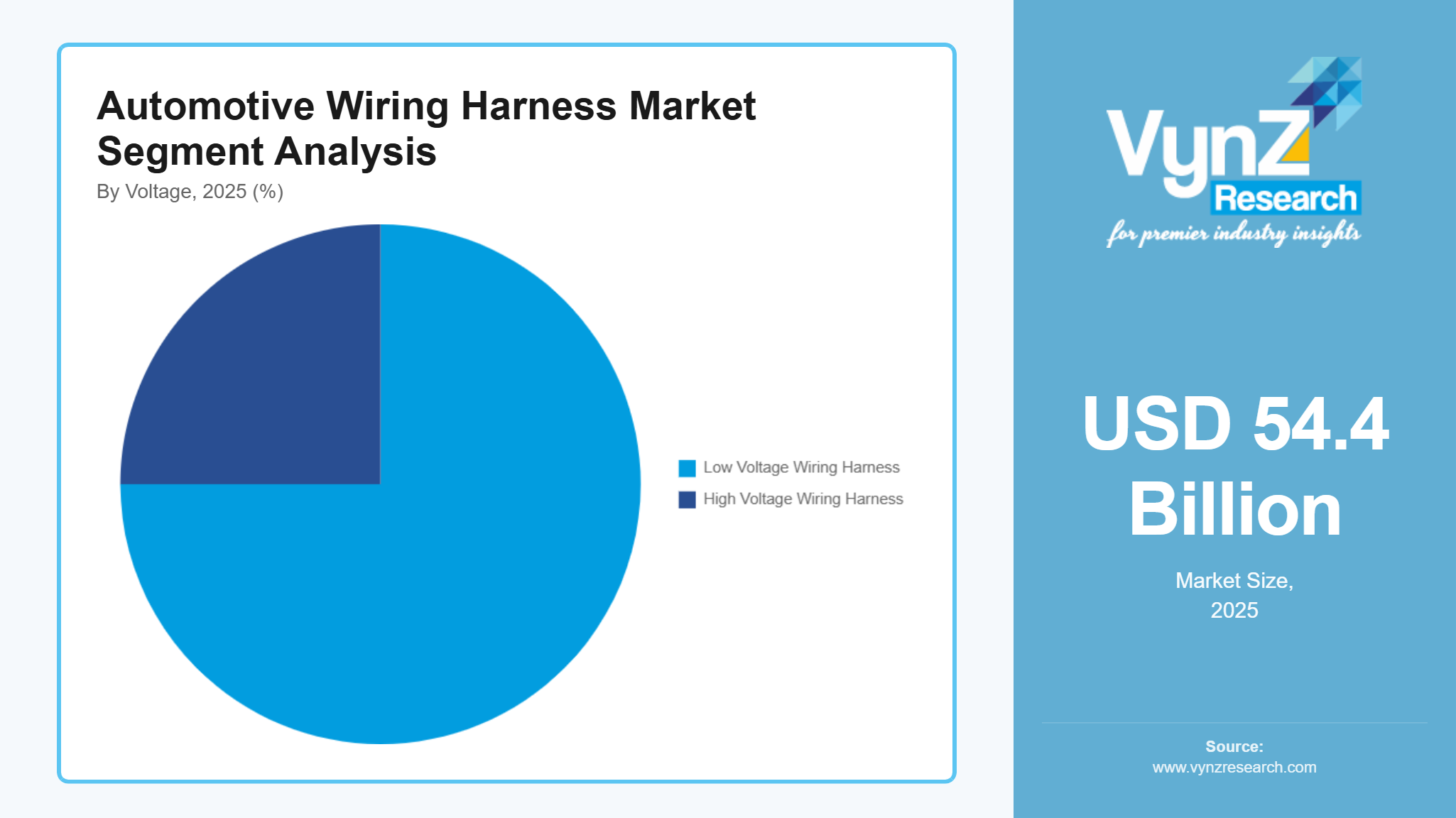

By Voltage

Low voltage wiring harness is the largest category with a market share of about 75% in 2025, as most traditional vehicle electrical systems operate within low-voltage ranges. Lighting systems, infotainment units, sensors, and control modules are some of the components that are dependent on low-voltage electrical networks to operate safely and efficiently. A significant share of vehicle production in the world remains with internal combustion engine vehicles and hybrid vehicles, both of which continue to have high demand of low-voltage wiring harnesses. Such systems are also necessary in comfort, safety, and communication needs in the car. Low-voltage harness systems remain the market leader due to their usage in almost all vehicle platforms.

High voltage wiring harness is the fastest-growing category during the forecast period, due to the growing popularity of the electric car and hybrid car globally. The electric vehicles need the use of high voltage to effectively transfer energy between battery packs, power electronics and the electric motors. With the current growth in the use of EVs around the world, automakers are also beginning to introduce specialized high-voltage wiring harnesses that can safely accommodate larger current draws. Also advanced insulation and shielding technologies are required in these systems to guarantee performance and safety.

By Vehicle Type

Passenger cars are the largest category with a market share of about 60% in 2025, supported by the high global production and sales of passenger vehicles. These vehicles incorporate numerous electronic systems such as infotainment units, safety sensors, lighting modules, and connectivity technologies that require extensive wiring harness networks. As automakers continue to introduce advanced features such as ADAS and digital dashboards, the wiring content in passenger cars continues to increase. Passenger vehicles also represent the largest category in global automotive manufacturing, especially in regions such as Asia-Pacific and Europe.

Electric vehicles are the fastest-growing category during the forecast period, driven by the global transition toward sustainable and low-emission transportation. Electric vehicles require significantly more wiring compared with conventional vehicles because they include complex battery systems, high-voltage power distribution networks, and advanced electronic control units. Governments across many regions are offering incentives, subsidies, and regulatory support to accelerate EV adoption. Automakers are also investing heavily in EV production and developing new electric platforms.

By Application

Body wiring harness is the largest category with a market share of approx. 35% in 2025, as it supports a wide range of vehicle functions including lighting systems, power windows, door locks, seat controls, and infotainment systems. These wiring harness systems connect various interior and exterior electronic components throughout the vehicle body. The increasing integration of comfort, safety, and connectivity features in modern vehicles has significantly increased the complexity and size of body wiring harness networks. As vehicles continue to adopt advanced electronic systems, the demand for body wiring harnesses remains consistently high.

Sensor wiring harness is the fastest-growing category during the forecast period, driven by the rapid adoption of advanced driver assistance systems and autonomous driving technologies. Modern vehicles are equipped with numerous sensors such as cameras, radar, lidar, and ultrasonic sensors that require dedicated wiring harness connections. These sensors support functions including lane departure warning, adaptive cruise control, and automatic emergency braking.

By Distribution Channel

OEM (Original Equipment Manufacturer) is the largest category with a market share of about 85% in 2025, since majority of the wiring harness systems are fitted during the process of assembling the vehicle. In the automotive sector, wiring harness assemblies are normally procured by specialized vendors to be installed by the automotive manufacturer in the new vehicle during the production lines. These harness systems are tailor packaged to suit vehicle platforms and electronic structures. Due to the ongoing increase of vehicles manufacturing around the world, and the growth of automotive manufacturing plants, the high demand in the OEM category is being sustained.

Aftermarket is the fastest-growing category with a CAGR of about 6.8% during the forecast period, driven by the increasing need for maintenance, repair, and replacement of wiring harness systems in aging vehicles. Over time, the wiring components could wear out, corrode or develop electrical faults that need replacement. The overall vehicle population in the world is increasing, and which means that there is an increase in the automotive repair and servicing demand. Also, customization of vehicles and retrofitting of electronic systems is also playing a role in the demand of aftermarket wiring harness.

Regional Insights

North America

North America is the largest regional market for automotive wiring harness, supported by the strong presence of major automotive manufacturers and advanced vehicle technology adoption. The United States is the leader of the region as it possesses a significant base of automotive production and is highly integrated in terms of the implementation of electronic systems including advanced driver assistance systems (ADAS), infotainment systems, and connected vehicle systems. There is also growing investments in electric vehicles manufacturing and battery production plants in the region which puts a great deal of strain on high-voltage wiring harness systems demand. Advanced wiring architecture is also being adopted further due to government efforts towards electric mobility and more stringent vehicle safety laws. The U.S. government allocated about $7.5 billion under the Bipartisan Infrastructure Law to expand EV charging infrastructure and support large-scale EV adoption across the country. Additionally, the availability of major component suppliers in the automotive industry and the well-established supply chains enhances the growth rate of the market region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the automotive wiring harness market, driven by rapid expansion of automotive manufacturing and strong growth in electric vehicle production. China, India, Japan, and South Korea are some of the top manufacturing centers of automotive products that have created a large global demand of wiring harness system in both passenger and commercial vehicles. China leads in manufacturing electric vehicles, and battery systems and power electronics need lots of high-voltage wiring harnesses. China has invested over $60 billion in subsidies, tax incentives, and infrastructure programs to accelerate the development of its New Energy Vehicle (NEV) industry. Government policies support EV manufacturing, charging infrastructure deployment, and battery-swapping networks. Government regulations that favor electric mobility and incentives in domestic production and investments in the infrastructure are speeding up the adoption of EVs in the region. The growing disposable incomes and growing level of car ownership is also improving the volume of automotive production.

Europe

Europe maintains a strong position in the automotive wiring harness market due to its advanced automotive industry and strong focus on vehicle electrification. The region is home to several major automotive manufacturers that are actively investing in electric vehicles, hybrid powertrains, and advanced vehicle electronics. Countries such as Germany, France, and the United Kingdom are leading the transition toward electric mobility, supported by strict emission regulations and government incentives for EV adoption. The European Union’s sustainability policies and carbon reduction targets are encouraging automakers to accelerate the development of electric and hybrid vehicles, increasing demand for high-voltage wiring harness systems. Additionally, the region emphasizes advanced safety technologies and connected vehicle platforms, which require complex wiring architectures. Strong research and development capabilities and technological innovation further strengthen Europe’s role in the global market.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is witnessing steady growth in the automotive wiring harness market due to gradual expansion of automotive manufacturing and vehicle sales. In Latin America, countries such as Brazil and Mexico are strengthening their automotive production capabilities and increasing exports of vehicles and automotive components. Middle East is witnessing the increasing demand of advanced cars and the electric mobility programs especially in the United Arab Emirates and Saudi Arabia. In these areas, governments are slowly eco-friendly in their choices of transportation and investing in the new automotive features. The growing demand of wiring harness components is also taking place in Africa where emerging automotive manufacturing centers and rising prevalence of vehicle ownership is leading to increased demand of the component. Even though most of these regions have not yet developed their automotive supply chain, continued industrialization and improvement of infrastructure is likely to underpin the future growth of the market.

Competitive Landscape / Company Insights

The automotive wiring harness market is moderately consolidated, with several large global automotive component manufacturers dominating supply through extensive production networks, long-term contracts with automakers, and advanced electrical system engineering capabilities. The major corporations which include Yazaki Corporation, Sumitomo Electric Industries Ltd and Aptiv PLC have a large market share because they manufacture around the whole world, have a good rapport with the leading automotive OEMs, and expertise in designing the complicated electrical distribution systems employed in contemporary vehicles. Such companies invest much on research and development to meet the increasing demand of high-voltage wiring systems designed in electric and hybrid cars and lightweight harness architectures that enhance the efficiency of vehicles. Companies like Leoni AG, Furukawa Electric Co., Ltd., and Lear Corporation are major suppliers and compete by providing high-technology wiring solutions, built-in modules in harnesses, and integrated electrical distribution technologies, specific to connected cars and autonomous cars. Tier-1 suppliers would in most cases work together with automakers in the initial phases of the vehicle platform development, bolstering long-term supply contracts and establishing significant barriers to entry.

Mini Profiles

Yazaki Corporation is one of the world’s largest automotive wiring harness manufacturers, supplying electrical distribution systems, connectors, and automotive electronics to major global automakers.

Sumitomo Electric Industries, Ltd. is a leading supplier of automotive wiring harnesses, high-voltage cables, and electronic components used in conventional and electric vehicles.

Aptiv PLC specializes in advanced automotive electrical architectures, including high-performance wiring harness systems, connectors, and data distribution networks for modern vehicles.

Leoni AG develops sophisticated wiring systems and cable solutions for the automotive industry, focusing on lightweight designs and high-voltage wiring technologies for electric vehicles.

Furukawa Electric Co., Ltd. provides automotive wiring harnesses, high-voltage cables, and advanced electrical components designed for electric and hybrid vehicles.

Key Players

- Yazaki Corporation

- Sumitomo Electric Industries, Ltd.

- Aptiv PLC

- Leoni AG

- Furukawa Electric Co., Ltd.

- Lear Corporation

- THB Group (Kromberg & Schubert)

- Samvardhana

- Motherson

- International Limited

- Nexans S.A.

- Yura Corporation

- Fujikura Ltd.

- PKC Group

Recent Developments

January 2026 – Yazaki Corporation announced the expansion of its electric vehicle wiring harness production facilities in Mexico to support rising demand from North American EV manufacturers and strengthen its regional supply chain capabilities.

December 2025 – Aptiv PLC introduced a next-generation vehicle electrical architecture platform designed to reduce wiring complexity and weight while supporting high-speed data transmission for connected and autonomous vehicles.

October 2025 – Sumitomo Electric Industries, Ltd. launched a new lightweight high-voltage wiring harness system specifically designed for electric vehicles to improve energy efficiency and thermal performance.

August 2025 – Leoni AG secured a major supply agreement with a European electric vehicle manufacturer to deliver advanced high-voltage cable systems for next-generation battery-electric vehicle platforms.

June 2025 – Samvardhana Motherson International Limited announced the expansion of its wiring harness manufacturing operations in India to meet growing demand from domestic and global automotive OEMs, particularly for electric vehicle platforms.

Global Automotive Wiring Harness Market Coverage

Component Insight and Forecast 2026 - 2035

- Electric Wires

- Connectors

- Terminals

- Others

Material Insight and Forecast 2026 - 2035

- Copper

- Aluminum

Voltage Insight and Forecast 2026 - 2035

- Low Voltage Wiring Harness

- High Voltage Wiring Harness

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

- Electric Vehicles (EVs)

Application Insight and Forecast 2026 - 2035

- Engine Wiring Harness

- Body Wiring Harness

- Chassis Wiring Harness

- HVAC Wiring Harness

- Sensor Wiring Harness

- Dashboard / Cabin Wiring Harness

Distribution Channel Insight and Forecast 2026 - 2035

- OEM (Original Equipment Manufacturer)

- Aftermarket

Global Automotive Wiring Harness Market by Region

- North America

- By Component

- By Material

- By Voltage

- By Vehicle Type

- By Application

- By Distribution Channel

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Material

- By Voltage

- By Vehicle Type

- By Application

- By Distribution Channel

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Material

- By Voltage

- By Vehicle Type

- By Application

- By Distribution Channel

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Material

- By Voltage

- By Vehicle Type

- By Application

- By Distribution Channel

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Automotive Wiring Harness Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Material

1.2.3. By

Voltage

1.2.4. By

Vehicle Type

1.2.5. By

Application

1.2.6. By

Distribution Channel

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Electric Wires

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Connectors

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Terminals

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Others

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Material

5.2.1. Copper

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Aluminum

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Voltage

5.3.1. Low Voltage Wiring Harness

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. High Voltage Wiring Harness

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Vehicle Type

5.4.1. Passenger Cars

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Light Commercial Vehicles (LCVs)

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Heavy Commercial Vehicles (HCVs)

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Electric Vehicles (EVs)

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Engine Wiring Harness

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Body Wiring Harness

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Chassis Wiring Harness

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. HVAC Wiring Harness

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Sensor Wiring Harness

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Dashboard / Cabin Wiring Harness

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

5.6. By Distribution Channel

5.6.1. OEM (Original Equipment Manufacturer)

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Aftermarket

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Material

6.3. By

Voltage

6.4. By

Vehicle Type

6.5. By

Application

6.6. By

Distribution Channel

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Material

7.3. By

Voltage

7.4. By

Vehicle Type

7.5. By

Application

7.6. By

Distribution Channel

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Material

8.3. By

Voltage

8.4. By

Vehicle Type

8.5. By

Application

8.6. By

Distribution Channel

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Material

9.3. By

Voltage

9.4. By

Vehicle Type

9.5. By

Application

9.6. By

Distribution Channel

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Yazaki Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Sumitomo Electric Industries, Ltd.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Aptiv PLC

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Leoni AG

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Furukawa Electric Co., Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Lear Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

THB Group (Kromberg & Schubert)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Samvardhana Motherson International Limited

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nexans S.A.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Yura Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Fujikura Ltd.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

PKC Group

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Automotive Wiring Harness Market