China EV Charging Infrastructure Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Charging Type (AC Charging, DC Fast Charging, Ultra-Fast / High-Power Charging), by Installation Type (Fixed Charging Station, Portable Charger), by Application (Residential Charging, Commercial Charging, Public Charging), by Vehicle Type (Passenger Cars, Electric Buses, Light Commercial Vehicles, Heavy Commercial Vehicles), by End User (Private Users, Fleet Operators, Public Transport Authorities, Commercial Charging Providers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9662 | Industry : Automotive & Transportation | Available Format :

|

Page : 145 |

China EV Charging Infrastructure Market Overview

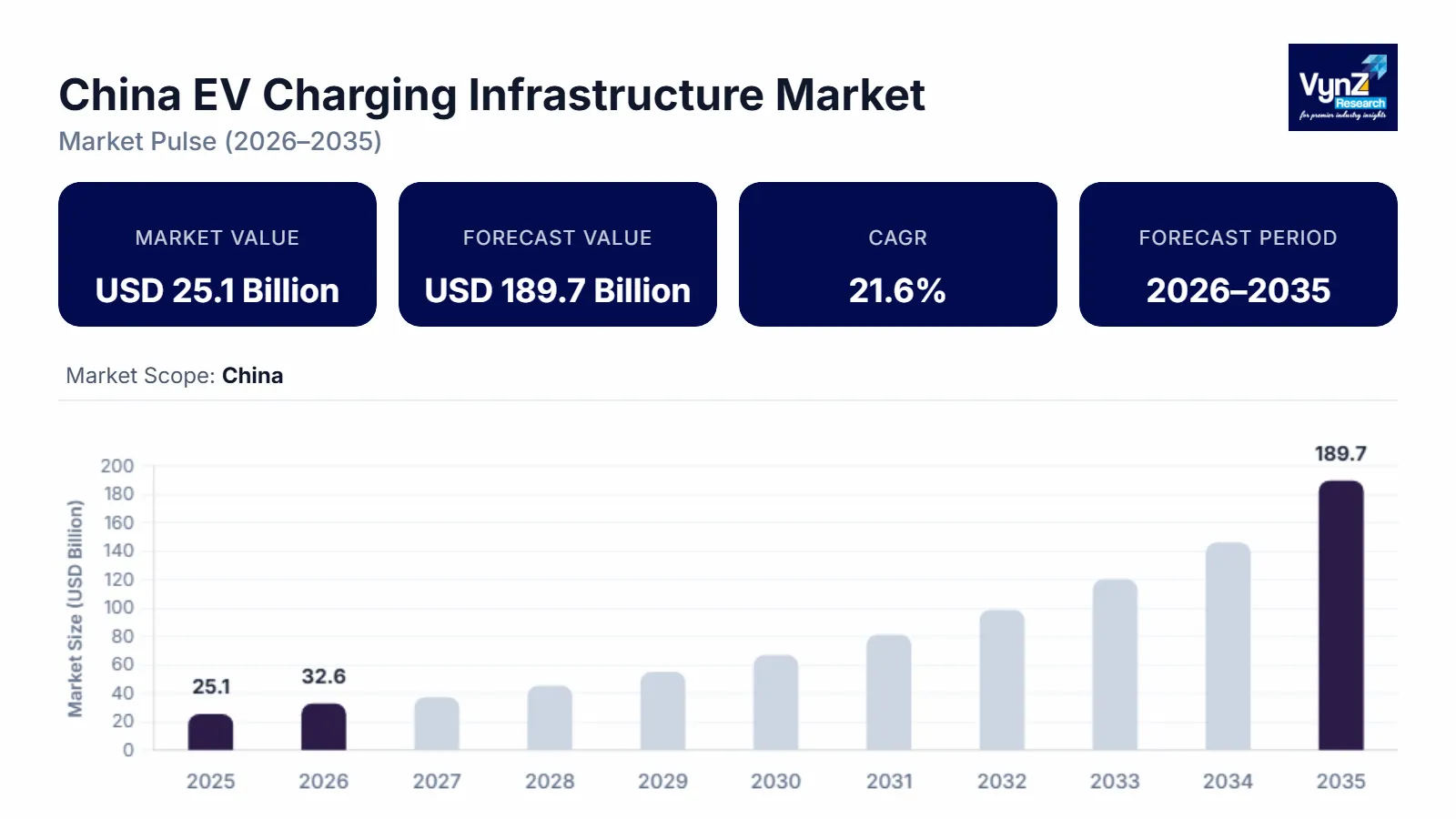

The China electric vehicle (EV) charging infrastructure market which was valued at approximately USD 25.1 billion in 2025 and is estimated to reach around USD 32.6 billion in 2026, is projected to reach close to USD 189.7 billion by 2035, expanding at a CAGR of about 21.6% during the forecast period from 2026 to 2035.

The market is driven by strong government policies, rapid growth in electric vehicle adoption, and large-scale investments in clean transportation and energy systems. The Chinese government has already introduced national efforts as a part of carbon neutrality targets and New Energy Vehicle (NEV) policies that mandate the growth of the public, residential, and highway charge networks nationwide. The rising manufacturing and sales of electric vehicles, buses and commercials in China have generated the need to have a dependable and quick-charging system. State-owned utilities and privately owned companies are making huge investments in ultra-fast chargers, battery swapping stations, and smart charging platforms to facilitate the increased EV ecosystem.

Moreover, the advancement of the charging technologies is being promoted by the integration of charging points with the smart grids and renewable energy sources. Public transport infrastructure is also adding to infrastructure needs with electrification of the major cities of Beijing, Shanghai, and Shenzhen. Long-range EV travel is also being supported by the development of expressway fast-charging corridors, and range anxiety is coming down.

China EV Charging Infrastructure Market Dynamics

Market Trends

The rapid growth of battery swapping infrastructure is one of the key trends in the China EV Charging Infrastructure Market, driven by the need for faster and more efficient alternatives to traditional charging. With battery swapping, the user of electric vehicles can swap a collapsed battery with a fully charged one within a few minutes hence minimizing the waiting time, unlike in traditional ways of charging batteries. The Chinese government is also promoting battery swapping to cut down global pollution by encouraging it through policy incentives and pilot projects, particularly with taxis, buses, heavy trucks, and commercial fleets that need to utilize their vehicles on a high basis. The Shanghai municipal government offers up to 40% subsidy on equipment investment for battery swap stations that support multiple EV brands. In addition to construction incentives, Shanghai also offers operational support through electricity subsidies of up to RMB 600 per kilowatt (kW) of installed capacity. Historical automakers and energy firms are piling their money on swapping stations to enhance convenience and decrease the range anxiety. To a large city, this technology is becoming especially popular as the ride-hailing and logistics vehicles must have a fast turnaround time. Battery swapping is also used to ease the burden on the power grid since the batteries can be recharged when there are no people who use them. Swapping systems are also getting more acceptance as there is the development of standardized battery designs.

Growth Drivers

The rapid increase in electric vehicle sales in China is a major growth driver for the China EV Charging Infrastructure Market, as the rising number of EVs on the road directly increases the demand for reliable and widespread charging facilities. China is the biggest market of electric vehicles in the globe, and the governmental incentives and stringent emissions rules have led to high growth of passenger EVs, electric buses, and commercial electric vehicles. The Chinese government launched large-scale purchase subsidies for New Energy Vehicles (NEVs) to accelerate EV adoption. Consumers purchasing electric vehicles received subsidies that could reach up to RMB 50,000 per vehicle, significantly reducing the upfront cost of EV ownership. The requirement of residential chargers, public charging stations and high-power fast chargers is increasing as more consumers abandon their fuel powered vehicles to the electric mobility. Expansion of domestic auto and battery producers has also increased the EV adoption, putting more pressure in the construction of adequate charging infrastructure. Besides that, major cities are facilitating electric cabs, ride-hailing cars, and fleet of delivery vehicles, which not only demand frequent charging, but also reliable charging infrastructure. The growing number of affordable EV models also increases the number of vehicles sold and requires infrastructure. To facilitate this high expansion, governmental agencies and the businesses are spending a lot of money in establishing new charging stations in cities, highways, as well as industrial regions.

Market Restraints / Challenges

Power grid capacity limitations and load management issues are a major challenge for the China EV Charging Infrastructure Market, as the rapid increase in electric vehicles is creating high electricity demand that puts pressure on existing power networks. Fast-charging stations consume power in small intervals, but in large quantities, thus straining local distribution grids, particularly in high-density urban areas. Particularly in certain areas, the existing grid system was not initially designed to allow widespread EV charging so upgrade must be performed before the new stations can be added. It has also become hard to control the peak time of electricity demand because most people decide to charge their vehicles simultaneously especially in the evening. Not to cause grid instability, operators need to invest into smart charging systems, storage energy and load balancing technologies, which raise the cost of infrastructure. Besides this, charging networks also demand modernization and the implementation of sophisticated grid management to combine renewable energy with it. These technical and economic issues may slow the process of introduction of new charging stations.

Market Opportunities

The expansion of ultra-fast and high-power charging networks is a major opportunity in the China EV Charging Infrastructure Market, as the growing number of electric vehicles requires faster and more efficient charging solutions. The ultra-fast chargers can substantially decrease the charging time so that vehicles can be charged in a matter of minutes as compared to hours, a factor that enhances convenience to users and long-distance travel. Chinese government is promoting the use of high-power DC charging facilities along the highways, urban centers as well as commercial areas to facilitate the fast introduction of electric mobility. China’s central government released a three-year development plan to expand EV charging capacity, targeting the establishment of around 28 million charging facilities nationwide by 2027. The plan includes upgrading existing stations with high-power fast-charging technologies and expanding urban fast-charging hubs. Electric buses, trucks, and ride-hailing fleets notably need such charging networks due to the need to turnaround within a short period of time. The next generation of charging technology of higher voltage and energy efficiency is being invested by energy companies and charging operators. Besides that, the presence of high-power charging infrastructure facilitates the creation of long-range EVs, which enhances consumer confidence in electric vehicles. Combination of smart grid technology and fast charge equipment is also contributing to the fact that power demand is more effectively managed.

China EV Charging Infrastructure Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 25.1 Billion |

|

Revenue Forecast in 2035 |

USD 189.7 Billion |

|

Growth Rate |

21.6% |

|

Segments Covered in the Report |

Charging Type, Installation Type, Application, Vehicle Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

East China, South China, North China, West China, Central China |

|

Key Companies |

State Grid Corporation of China, China Southern Power Grid Co. Ltd., TELD New Energy Co. Ltd., Star Charge (Wanbang Digital Energy Co., Ltd.), NIO Inc., BYD Company Limited, Potevio New Energy Co. Ltd., Xiaoju Charging, Tesla, Inc., XPENG Inc., China Tower Corporation Limited, TGOOD Electric Co. Ltd. |

|

Customization |

Available upon request |

China EV Charging Infrastructure Market Segmentation

By Charging Type

DC Fast Charging is the largest category with a market share of about 45% in 2025, because it is widely used in the charges of the public charging stations, highways, and commercial charging hubs within China. The high population of electric vehicles in cities would also be supported by the fast charging which is done by installing of fast chargers. Rates of installations have also been encouraged by government policies of fast-charging corridors and high-power stations. DC fast charging is also a vital component of the public transport fleets and ride-hailing vehicles to minimize downtime. It is the choice of large-scale infrastructure development because it offers quick and dependable charging.

Ultra-Fast / High-Power Charging is the fastest-growing category with a CAGR of 21.8% during the forecast period, because the demand in terms of charging time is becoming shorter and traveling long distances with EV. Expressway chargers of high power are being installed and major cities to accommodate next generation electric cars that have larger batteries. Government programs that promote ultra-fast charging networks are driving up the implementation. High-power charging is also being implemented to enhance efficiency by commercial fleets and logistics operators. The growth in the battery and power electronics technology is making it possible to have greater charging capacity.

By Installation Type

Fixed Charging Station is the largest category with a market share of about 90% in 2025, because most of the Chinese public, commercial, and highway charging facilities are founded on permanent premises. Fixed stations offer reliable power availability, increased charge capacity, and enhanced power grid integration. The government-sponsored charging networks and utility-owned stations are mainly fixed. These stations are very critical to the city charging centres, fleet depots, and expressway networks. They are the choice of large projects because of their reliability and the duration of use.

Portable Charger is the fastest-growing category with a CAGR of 22.2% during the forecast period, because of the rising number of EVs in the home environment and the actuality of mobile charging solutions. Portable chargers are easily used in the home and charging in case of an emergency. This category is supported by an increasing demand among the owners of the EV privately. Portable chargers are becoming safer and more efficient because of technological advances. They can also be applied in places where the infrastructure of people is low. With the growth in the spread of EV adoption to some smaller cities, the demand for the portable charging is rapidly increasing.

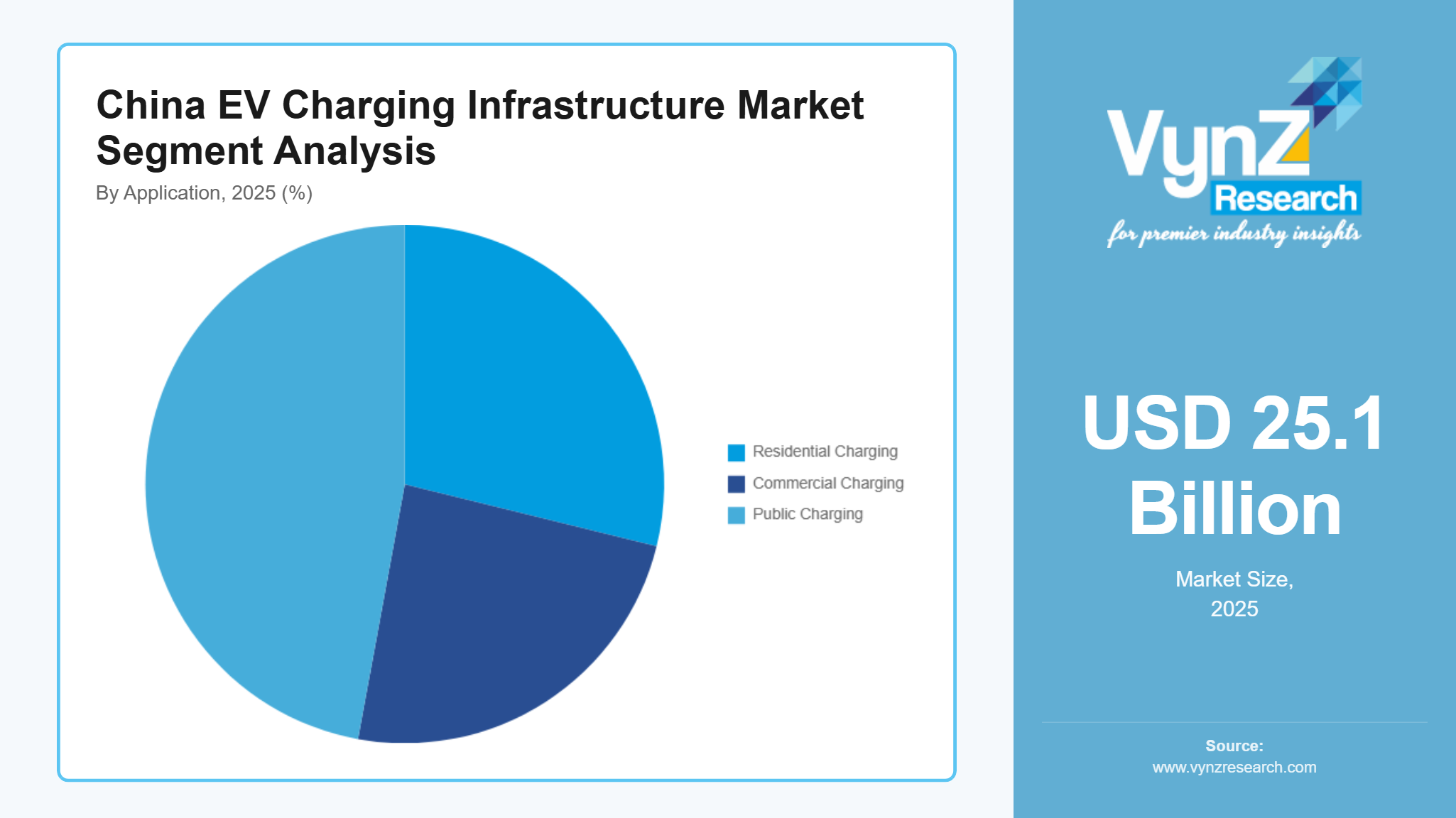

By Application

Public Charging is the largest category with a market share of about 50% in 2025, because the government is keen on developing nationwide charging networks within the urban areas, highways, and commercial premises. The large EV populations without home charging or private parking should rely on public stations to serve the population. Local government and state-run utilities are actively investing in city charging infrastructure. Ride-hailing, taxi, and logistics fleets require the use of public charging stations daily. The basis of the EV ecosystem in China is high utilization rates due to charging in the open.

Commercial Charging is the fastest-growing category during the forecast period, which is boosted by the quick switch to electricity of fleets, logistics vehicles and corporate transport systems. Companies are equipping special charging stations to minimize the operation expenses and enhance efficiency. Charging facilities are also being added in shopping centers, offices, and industrial parks. The increased electric delivery and ride-sharing cars are pushing up demand. The development of charging services by private investors is growing rapidly. This category is growing at a very high rate with the increasing commercial use of the EV.

By Vehicle Type

Passenger Cars is the largest category with a market share of about 70% in 2025, since most of the electric vehicles sold in China are passenger EVs. The increase in the popularity of affordable electric cars has led to the rise of the necessity of charging stations at home, in the vicinity, and at workplaces. The incentives provided by the government and city regulations on the emission of gases are promoting the purchase of EVs privately. Most of the charging infrastructure is intended to accommodate passenger cars. The volume of sale leads to the direct increment of charging demand. Thus, the market is dominated by passenger cars.

Heavy Commercial Vehicles is the fastest-growing category with a CAGR of 21.9% during the forecast period, because of electrification of trucks, buses, and logistics fleets. These cars demand power charging and battery replacement. This is due to government schemes of electrifying freights and public transport. Fleet operators are now favoring electric cars to save on fuel and carbon emission. High-capacity charging hubs are being dedicated to commercial use. This category is increasing at the fastest rate as commercial electrification gains momentum.

By End User

Public Transport Authorities is the largest category in 2025, because China has been very aggressive in electrifying buses, taxis, and municipal vehicles. Massive public transportation is mandated by the government that necessitates a shift to electric mobility. These fleets require special charging stations and depots. The cities spend a lot of money on the infrastructure of the public transport system. Buses require high energy consumption, which increases the demand of charging.

Fleet Operators is the fastest-growing category during the forecast period, because the global development of electric logistics, ride-hailing, and delivery services is increasing rapidly. Firms are deploying their own charging infrastructures in bid to cut down the fuel expenses. E-commerce is growing, which is mounting electric delivery vehicles. High capacity and high-charging systems are needed in fleet charging.

Regional Insights

East China

East China is the largest regional market for EV charging infrastructure, supported by the highest electric vehicle adoption rate, strong industrial development, and extensive government investment in charging networks. Major provinces such as Shanghai, Jiangsu, Zhejiang, and Shandong are heavily populated with people and high ratios of EV owners, which means there will be great demand to install both public and personal charging points. China has launched pilot programs to integrate EV charging networks with the national electricity grid through vehicle-to-grid (V2G) technologies. The government plans to deploy around 5,000 bidirectional charging stations by 2027, allowing EVs to store electricity and return power to the grid during peak demand. The local governments in this area are very active in promoting the use of new energy vehicles with subsidies, a mandatory policy to install charging facilities, and massive infrastructure development. The availability of major manufacturing firms of cars, batteries, and technology firms also hastens the establishment of fast-charging and ultra-fast charging locations. Moreover, East China has a high-power grid and therefore, it is easier to support high-power charging systems. There are high populations of electric buses, taxis, and logistics vehicles that add more demands to charging infrastructure. Ongoing smart grid and renewable energy integration initiatives are useful in ensuring the region remains top of the market.

South China

South China is one of the fastest-growing regions in the EV charging infrastructure market, driven by strong economic growth, rapid urbanization, and high adoption of electric vehicles in provinces such as Guangdong, Fujian, and Guangxi. Shenzhen and Guangzhou are international leaders of electric public transportation and have huge stocks of electric buses, taxis, and ride-hailing cars, which need large electric battery charging systems. The Chinese government included EV charging infrastructure as a core part of its “New Infrastructure” strategy, which prioritizes advanced energy and digital infrastructure. Under this plan, authorities set a target to deploy around 360,000 high-power charging stations (≥350 kW) nationwide. The policy also provides subsidies covering up to 30% of equipment costs for high-power charging systems. Clean transportation and smart city development programs promoted by governments are accelerating the deployment of fast-charging stations and battery swapping. Manufacturing capabilities are also strong in the region in terms of their electronic and battery products and this aids with the growth of the infrastructure locally. The deployment of the charging networks is enhanced by increasing the private investment and the introduction of large EV manufacturers. Rapid growth is also being brought about by highway charging corridor projects and commercial fleet electrification.

North China

North China holds a significant share in the EV charging infrastructure market due to strong government policies and large-scale electrification programs in cities such as Beijing, Tianjin, and Hebei. The region is characterized by a high demand of charging stations due to the severity of emission regulation, as well as the encouragement of using electric cars to minimise air pollution. The electrification of public transport (electric buses and taxis) has resulted in the creation of large charging stations and rapid charging stations. Government owned utilities are heavily investing in smart charging networks and grid upgrade to accommodate rising numbers of electricity demand. Also, there is a need to promote the use of advanced charging systems because winter climatic conditions in this region demand a reliable charging infrastructure with high performance. Infrastructure is also being expanded by industrial and commercial fleet electrification. There is constant urbanization of the region and policy reinforcement to guarantee constant increase in the market in North China.

West China

West China is a developing market for EV charging infrastructure, supported by government programs aimed at improving energy access, reducing emissions, and promoting electric mobility in provinces such as Sichuan, Chongqing, Shaanxi, Yunnan, and Xinjiang. EV penetration in the region is lower than on the eastern coasts, although the government is investing in charging stations on national highways and other major transport routes to facilitate long distances and electrification of commercial vehicles. Projects in infrastructure development under the regional economic development programs are contributing to the expansion of the charge networks in the growing cities. The electrification of mining, logistics and industrial transport is also causing the demand of the high-capacity charging systems. China introduced a national action plan to strengthen EV charging infrastructure, focusing heavily on fast and ultra-fast charging corridors. The plan aims to deploy or upgrade around 40,000 ultra-fast charging points along highway service areas by 2027, ensuring that nearly all motorway service stations provide high-speed charging access. EV charging stations are integrated with renewable energy projects in West China to enhance the energy efficiency.

Central China

Central China is an emerging regional market for EV charging infrastructure, driven by increasing government investment, rising electric vehicle adoption, and expanding urban development in provinces such as Hubei, Henan, Hunan, Anhui, and Jiangxi. Chinese government is enhancing clean transportation in inland cities as a means of balancing the development of the coastal and the interior regions, which is stimulating the setting up of public and residential charging stations. The demand in the reliable charging networks is also growing due to the increase in manufacturing, logistics, and public transportation electrification. A few provincial governments are putting in highway fast-charging corridors to enhance access to East China and South China economic zones. Moreover, the infrastructure expansion of smart grids is simplifying the process of implementing the high-power charging systems. Though the charging network is not as dense as in the coastal areas, the rates of installation are increasing.

Competitive Landscape / Company Insights

The China EV charging infrastructure market is moderately consolidated, led by large state-owned utilities, major EV manufacturers, and leading charging network operators that combine strong financial capability with nationwide deployment capacity. The presence of large markets controlled by large corporations like the State Grid Corporation of China and China Southern Power grid with their large networks of public charging, deep integration of their grid and support by government infrastructure projects give them a major advantage in large scale installation and long-term operation. The expansion of their own charging platforms to facilitate the sale of vehicles is supported by the leading EV manufacturers, such as BYD Company Limited, NIO Inc., and Tesla, Inc. and the investments in fast-charging, battery swap, and smart charging platforms that empower them in the market.

Competitors like TELD New Energy Co., Ltd. and Star Charge (Wanbang Digital Energy Co., Ltd.) compete by establishing high-density urban charging networks, providing a platform of digital payment, and installing ultra-fast charging devices to enhance user convenience. The companies in oil and energy such as China Petroleum and Chemical Corporation (Sinopec) and China National Petroleum Corporation (CNPC) are also coming into the market by installing charging stations in the fuel stations to utilize the national retail network to increase the coverage of EV charging. The providers of technology and equipment are competing by providing high-power chargers, power electronics, and energy management systems which are needed to smart charging networks. Moreover, newcomers concentrating on battery swap, energy storage combined charging and vehicle-to-grid systems are becoming popular, where they frequently collaborate with larger utilities or car makers to scale the implementation.

Mini Profiles

State Grid Corporation of China is the largest power utility in the world and a leading developer of EV charging infrastructure, operating extensive nationwide charging networks integrated with smart grid systems and high-power fast-charging stations across urban and highway corridors.

China Southern Power Grid Co., Ltd. provides electricity distribution and large-scale EV charging solutions in southern provinces, investing heavily in smart charging, grid modernization, and renewable-energy-integrated charging stations to support rapid electric vehicle adoption.

TELD New Energy Co., Ltd. is one of the largest EV charging network operators in China, offering public charging platforms, cloud-based energy management, and ultra-fast charging technologies with millions of connected charging points across major cities.

Star Charge (Wanbang Digital Energy Co., Ltd.) develops intelligent EV charging equipment and network services, focusing on high-power charging stations, digital charging platforms, and energy storage integrated charging systems for commercial and public applications.

NIO Inc. operates one of the most advanced battery swapping and fast-charging networks in China, providing integrated charging, swapping, and energy services designed to support its electric vehicle ecosystem and improve user convenience.

Key Players

- State Grid Corporation of China

- China Southern Power Grid Co., Ltd.

- TELD New Energy Co., Ltd. (TGOOD Group)

- Star Charge (Wanbang Digital Energy Co., Ltd.)

- NIO Inc.

- BYD Company Limited

- TGOOD Electric Co., Ltd.

- Potevio New Energy Co., Ltd.

- Xiaoju Charging (Didi Chuxing Technology Co.)

- Tesla, Inc.

- XPENG Inc.

- China Tower Corporation Limited

Recent Developments

January 2026 – State Grid Corporation of China announced expansion of its nationwide ultra-fast EV charging corridor program, adding high-power charging stations along major expressways to support long-distance electric vehicle travel and heavy-duty electric trucks.

December 2025 – NIO Inc. launched a new generation battery swapping station in China capable of completing a full battery swap in a few minutes, aimed at supporting taxis, ride-hailing fleets, and commercial electric vehicles.

October 2025 – BYD Company Limited partnered with several Chinese municipalities to deploy large-scale charging hubs for electric buses and logistics fleets, strengthening urban clean transportation infrastructure.

August 2025 – China Southern Power Grid Co., Ltd. announced investment in smart charging and vehicle-to-grid (V2G) pilot projects to improve grid stability and enable renewable energy integration with EV charging networks.

June 2025 – TELD New Energy Co., Ltd. expanded its public charging platform with new high-power DC fast chargers and cloud-based energy management systems to support growing EV adoption in major Chinese cities.

April 2025 – Star Charge introduced ultra-fast charging equipment with higher voltage capacity designed for next-generation electric vehicles, enabling shorter charging time and improved energy efficiency.

February 2025 – Sinopec began installing EV charging stations at fuel retail locations across China, converting traditional petrol stations into integrated energy service hubs supporting both fuel and electric vehicles.

China EV Charging Infrastructure Market Coverage

Charging Type Insight and Forecast 2026 - 2035

- AC Charging

- DC Fast Charging

- Ultra-Fast / High-Power Charging

Installation Type Insight and Forecast 2026 - 2035

- Fixed Charging Station

- Portable Charger

Application Insight and Forecast 2026 - 2035

- Residential Charging

- Commercial Charging

- Public Charging

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Electric Buses

- Light Commercial Vehicles

- Heavy Commercial Vehicles

End User Insight and Forecast 2026 - 2035

- Private Users

- Fleet Operators

- Public Transport Authorities

- Commercial Charging Providers

China EV Charging Infrastructure Market by Region

- East China

- By Charging Type

- By Installation Type

- By Application

- By Vehicle Type

- By End User

- South China

- By Charging Type

- By Installation Type

- By Application

- By Vehicle Type

- By End User

- North China

- By Charging Type

- By Installation Type

- By Application

- By Vehicle Type

- By End User

- West China

- By Charging Type

- By Installation Type

- By Application

- By Vehicle Type

- By End User

- Central China

- By Charging Type

- By Installation Type

- By Application

- By Vehicle Type

- By End User

Table of Contents for China EV Charging Infrastructure Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Charging Type

1.2.2. By

Installation Type

1.2.3. By

Application

1.2.4. By

Vehicle Type

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. China Market Estimate and Forecast

4.1. China Market Overview

4.2. China Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Charging Type

5.1.1. AC Charging

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. DC Fast Charging

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Ultra-Fast / High-Power Charging

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Installation Type

5.2.1. Fixed Charging Station

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Portable Charger

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Residential Charging

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial Charging

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Public Charging

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Vehicle Type

5.4.1. Passenger Cars

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Electric Buses

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Light Commercial Vehicles

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Heavy Commercial Vehicles

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Private Users

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Fleet Operators

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Public Transport Authorities

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Commercial Charging Providers

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. East China Market Estimate and Forecast

6.1. By

Charging Type

6.2. By

Installation Type

6.3. By

Application

6.4. By

Vehicle Type

6.5. By

End User

7. South China Market Estimate and Forecast

7.1. By

Charging Type

7.2. By

Installation Type

7.3. By

Application

7.4. By

Vehicle Type

7.5. By

End User

8. North China Market Estimate and Forecast

8.1. By

Charging Type

8.2. By

Installation Type

8.3. By

Application

8.4. By

Vehicle Type

8.5. By

End User

9. West China Market Estimate and Forecast

9.1. By

Charging Type

9.2. By

Installation Type

9.3. By

Application

9.4. By

Vehicle Type

9.5. By

End User

10. Central China Market Estimate and Forecast

10.1. By

Charging Type

10.2. By

Installation Type

10.3. By

Application

10.4. By

Vehicle Type

10.5. By

End User

11. Company Profiles

11.1.

State Grid Corporation of China

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

China Southern Power Grid Co., Ltd.

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

TELD New Energy Co., Ltd. (TGOOD Group)

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Star Charge (Wanbang Digital Energy Co., Ltd.)

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

NIO Inc.

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

BYD Company Limited

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

TGOOD Electric Co., Ltd.

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

Potevio New Energy Co., Ltd.

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

Xiaoju Charging (Didi Chuxing Technology Co.)

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

Tesla, Inc.

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

11.11.

XPENG Inc.

11.11.1.

Snapshot

11.11.2.

Overview

11.11.3.

Offerings

11.11.4.

Financial

Insight

11.11.5.

Recent

Developments

11.12.

China Tower Corporation Limited

11.12.1.

Snapshot

11.12.2.

Overview

11.12.3.

Offerings

11.12.4.

Financial

Insight

11.12.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

China EV Charging Infrastructure Market