China Hydrogen Fuel Cell Vehicles Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger Cars, Buses, Trucks, Light Commercial Vehicles (LCV), Heavy Commercial Vehicles (HCV), Special Purpose Vehicles), by Technology (Proton Exchange Membrane Fuel Cell (PEMFC), Phosphoric Acid Fuel Cell (PAFC), Solid Oxide Fuel Cell (SOFC), Others), by Range (Short Range (Below 300 km), Medium Range (300–500 km), Long Range (Above 500 km)), by Hydrogen Source (Grey Hydrogen, Blue Hydrogen, Green Hydrogen), by End User (Public Transport, Logistics & Distribution, Industrial & Construction, Municipal Services, Private Use)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9663 | Industry : Automotive & Transportation | Available Format :

|

Page : 140 |

China Hydrogen Fuel Cell Vehicles Market Overview

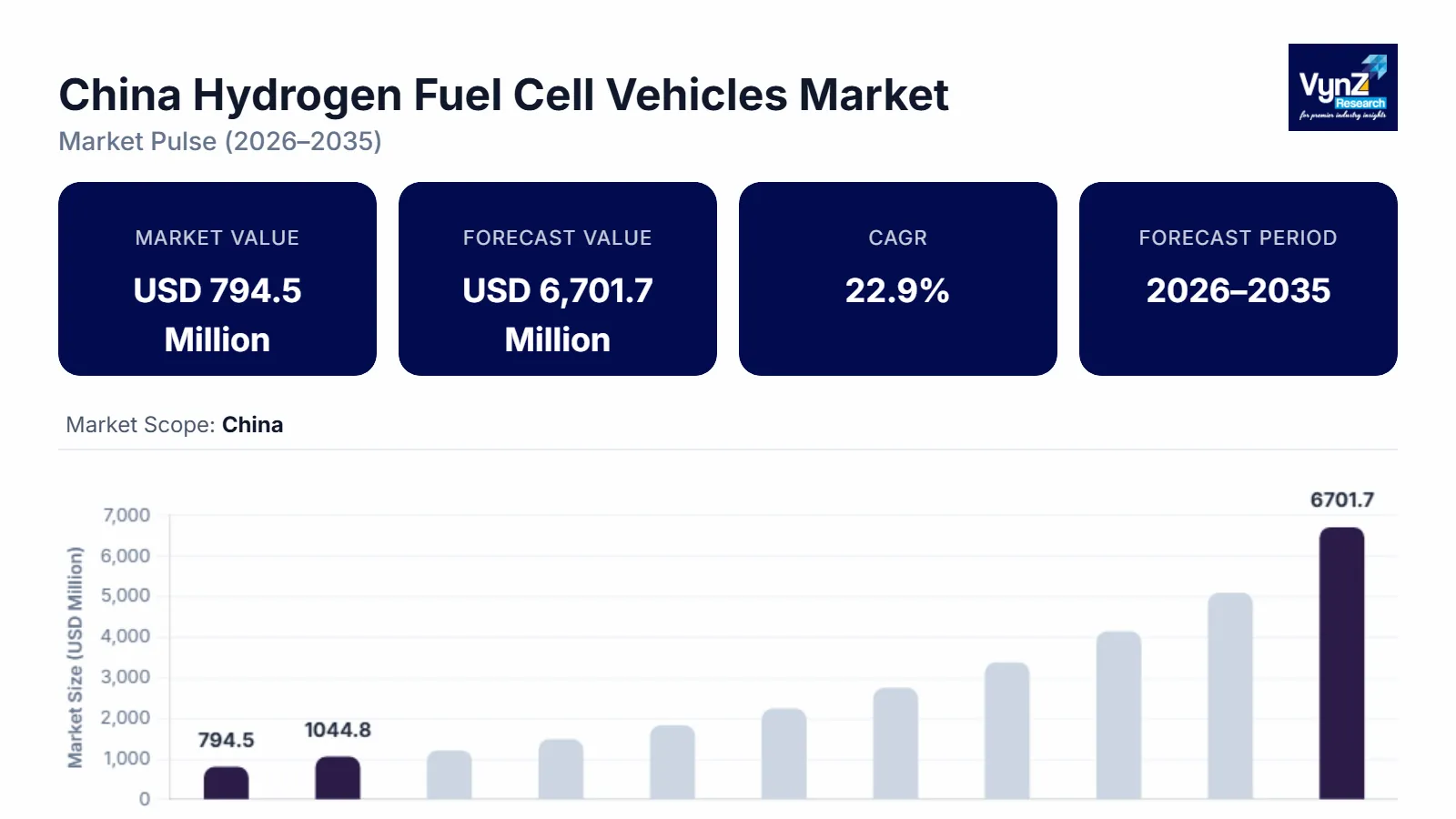

The China hydrogen fuel cell vehicles market which was valued at approximately USD 794.5 million in 2025 and is estimated to reach around USD 1,044.8 million in 2026, is projected to reach close to USD 6,701.7 million by 2035, expanding at a CAGR of about 22.9% during the forecast period from 2026 to 2035.

This market is driven by strong government support, large-scale hydrogen energy planning, and increasing focus on reducing emissions from commercial transportation. China has identified hydrogen fuel cell vehicles as a key technology for decarbonizing heavy-duty trucks, buses, and logistics fleets where battery electric vehicles are less efficient. The government has introduced subsidies, demonstration city-cluster programs, and long-term hydrogen development plans to accelerate vehicle deployment and hydrogen infrastructure construction.

Significant investments in hydrogen refuelling stations, domestic fuel-cell manufacturing, and renewable hydrogen production are improving the commercial feasibility of fuel-cell vehicles. In addition, provincial governments are offering financial incentives and industrial support to create regional hydrogen hubs. China’s carbon-neutrality targets and clean-energy transition policies are further encouraging the adoption of hydrogen mobility solutions. The growing use of fuel-cell vehicles in public transport and freight corridors is helping scale the technology faster.

China Hydrogen Fuel Cell Vehicles Market Dynamics

Market Trends

The expansion of hydrogen refuelling infrastructure across major provinces is a key trend driving the China Hydrogen Fuel Cell Vehicles Market, as the availability of fuelling stations is essential for large-scale adoption of fuel cell vehicles. The Chinese government is actively supporting the construction of hydrogen refuelling stations in industrial regions, logistics corridors, and demonstration city clusters to ensure a stable hydrogen supply. Provinces such as Guangdong, Hebei, Shandong, and Shanghai are investing heavily in hydrogen energy projects to build complete hydrogen ecosystems that include production, storage, transportation, and refuelling facilities. Hydrogen recognized as a strategic emerging energy sector to support transport decarbonization. Target to deploy 50,000 hydrogen fuel-cell vehicles and large-scale hydrogen refuelling infrastructure by 2025. These developments are reducing range anxiety and improving the operational efficiency of fuel-cell buses and trucks. Government incentives and subsidies for station construction are encouraging energy companies and local authorities to accelerate deployment. The growing network of refuelling stations is also helping commercial fleet operators adopt hydrogen vehicles with greater confidence. In addition, integration with renewable hydrogen production projects is supporting cleaner fuel supply.

Growth Drivers

The development of green hydrogen production projects is a major growth driver for the China Hydrogen Fuel Cell Vehicles Market, as clean hydrogen supply is essential for the long-term sustainability of fuel cell transportation. China is investing heavily in producing hydrogen using renewable energy sources such as solar, wind, and hydropower to reduce dependence on fossil-fuel-based hydrogen. Several large-scale green hydrogen projects are being developed in provinces like Inner Mongolia, Gansu, and Xinjiang, where renewable energy resources are abundant. Hydrogen was officially recognized as a strategic energy source supporting China’s carbon-neutrality goals. The plan sets a target of producing 100,000–200,000 tonnes of renewable (green) hydrogen annually by 2025. These projects help lower carbon emissions across the hydrogen value chain and support the country’s carbon-neutrality goals. Government policies encourage state-owned energy companies and private firms to build integrated facilities for hydrogen production, storage, and distribution. The availability of low-cost green hydrogen improves the economic feasibility of fuel cell buses and trucks. In addition, renewable hydrogen supports the use of fuel cell vehicles in long-distance and heavy-duty transport.

Market Restraints / Challenges

The high cost of green hydrogen production and storage is a major challenge for the China Hydrogen Fuel Cell Vehicles Market, as fuel price plays a critical role in the commercial adoption of fuel cell vehicles. Green hydrogen is produced using renewable energy sources such as solar and wind through electrolysis, which requires expensive equipment, high electricity consumption, and advanced technology. In addition, the cost of storing and transporting hydrogen is high because it must be kept under high pressure or at very low temperatures, requiring specialized tanks and safety systems. These factors make hydrogen fuel more expensive compared to conventional fuels and electricity used in battery electric vehicles. The need for large investments in production plants, pipelines, and storage facilities further increases the overall cost of the hydrogen ecosystem. Smaller regions and private operators often find it difficult to invest in such expensive infrastructure.

Market Opportunities

The growth of green hydrogen production using renewable energy sources presents a major opportunity for the China Hydrogen Fuel Cell Vehicles Market, as it enables the use of clean fuel for zero-emission transportation. China is expanding hydrogen production through solar, wind, and hydropower projects, especially in regions with abundant renewable resources such as Inner Mongolia, Xinjiang, and Gansu. Producing hydrogen from renewable electricity helps reduce carbon emissions and supports the country’s long-term carbon neutrality targets. Government policies are encouraging energy companies to develop integrated projects that combine renewable power generation with hydrogen production and storage facilities. The Sinopec Kuqa Green Hydrogen Demonstration Project in Xinjiang is one of the largest renewable hydrogen facilities in China. Investment of approximately RMB 3 billion (~USD 450 million). Uses solar photovoltaic power to produce hydrogen via electrolysis, generating around 20,000 tonnes of green hydrogen annually. As production capacity increases, the cost of green hydrogen is expected to decline, making fuel cell vehicles more economically viable. Lower fuel cost will support wider adoption of hydrogen buses, trucks, and logistics vehicles. In addition, clean hydrogen improves the environmental benefits of fuel cell transportation compared to fossil-fuel-based hydrogen. This growing renewable hydrogen supply is expected to create strong long-term growth opportunities for the hydrogen fuel cell vehicle market in China.

China Hydrogen Fuel Cell Vehicles Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 794.5 Million |

|

Revenue Forecast in 2035 |

USD 6701.7 Million |

|

Growth Rate |

22.9% |

|

Segments Covered in the Report |

Vehicle Type, Technology, Range, Hydrogen Source, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

East China, South China, North China, Central China, West China |

|

Key Companies |

SAIC Motor Corporation Limited, Dongfeng Motor Corporation, FAW Group Co. Ltd., Beiqi Foton Motor Co. Ltd., Yutong Bus Co. Ltd., Weichai Power Co. Ltd., Beijing SinoHytec Co. Ltd., Shanghai REFIRE Technology Co. Ltd., Sinosynergy Hydrogen Energy Technology Co. Ltd., China Petroleum & Chemical Corporation (Sinopec), China National Petroleum Corporation (CNPC), Horizon Fuel Cell Technologies |

|

Customization |

Available upon request |

China Hydrogen Fuel Cell Vehicles Market Segmentation

By Vehicle Type

Heavy Commercial Vehicles (HCV) is the largest category with a market share of about 35% in 2025, because China is primarily promoting hydrogen fuel cell technology for heavy-duty trucks, long-haul transport, and industrial logistics where battery electric vehicles are less efficient. Fuel cell systems provide longer driving range, faster refuelling, and higher load capacity, making them suitable for freight corridors and mining operations. Government demonstration projects in China mainly focus on heavy trucks and buses to reduce emissions in commercial transport. Large fleet operators prefer hydrogen trucks due to operational efficiency and reduced downtime. The government also provides higher subsidies for heavy-duty fuel cell vehicles, which increases their adoption. Hydrogen-powered trucks are widely used in port transport, steel plants, and industrial zones.

Buses is the fastest-growing category with a CAGR of 23.2% during the forecast period, because many Chinese cities are expanding hydrogen-powered public transportation to reduce urban pollution. Municipal governments are replacing diesel buses with fuel cell buses under clean transportation programs. Hydrogen buses offer long range and fast refuelling, which makes them suitable for continuous daily operation. Several city-cluster pilot programs focus on deploying fuel cell buses in public transit fleets. Government funding for zero-emission public transport is accelerating adoption. In addition, fuel cell buses help cities meet air-quality and carbon-reduction targets.

There Special Purpose Vehicles further classified into followings:

- Logistics

- Municipal

- Construction

By Technology

Proton Exchange Membrane Fuel Cell (PEMFC) is the largest category with a market share of about 85% in 2025, because PEM fuel cells are widely used in vehicles due to their compact size, quick start capability, and high efficiency at low temperatures. Most Chinese fuel cell vehicles use PEM technology because it is suitable for automotive applications and supports fast power response. Government-funded research programs in China are mainly focused on PEM fuel cell development. Domestic manufacturers are also investing heavily in PEM stack production to reduce import dependence. This technology is preferred for buses, trucks, and logistics vehicles.

Solid Oxide Fuel Cell (SOFC) is the fastest-growing category with a CAGR of 23.1% during the forecast period, because research institutions and manufacturers are investing in high-efficiency fuel cell technologies for future mobility applications. SOFC offers higher efficiency and better fuel flexibility compared to other fuel cell types. China is supporting advanced fuel cell research under its hydrogen development plans. Although adoption is currently limited, ongoing innovation is expected to improve performance and reduce costs. Technology is gaining interest in heavy-duty and long-range applications.

By Range

Long Range (Above 500 km) is the largest category with a market share of around 50% in 2025, because hydrogen fuel cell vehicles are mainly used in long-distance transport where extended driving range and quick refuelling are required. Commercial trucks, buses, and logistics fleets in China operate on fixed long routes, making long-range vehicles more practical. Hydrogen technology provides higher energy density than batteries, which supports longer travel distance. Government projects also prioritize long-haul freight corridors for fuel cell deployment. Fleet operators prefer long-range vehicles to reduce refuelling frequency. This makes the long-range category dominant in the market.

Medium Range (300–500 km) is the fastest-growing category with a CAGR of 23.7% during the forecast period, because medium-distance transport and urban logistics are increasing in China. Many municipal buses and delivery trucks operate within this range, making it suitable for hydrogen vehicles. Infrastructure development in cities is supporting medium-range fuel cell vehicles. These vehicles offer a balance between cost and performance. Government pilot programs in city clusters are encouraging adoption in urban transport.

By Hydrogen Source

Grey Hydrogen is the largest category with a market share of approx. 70% in 2025, because most hydrogen in China is currently produced from natural gas and coal due to lower production cost and existing industrial infrastructure. Grey hydrogen is widely available and easier to supply for current fuel cell vehicle projects. Early hydrogen mobility programs rely on conventional hydrogen production to reduce initial costs. Industrial hydrogen from chemical plants is also used for transportation fuel. Although it produces emissions, it remains the most economical option in the short term.

Green Hydrogen is the fastest-growing category during the forecast period, because China is investing heavily in renewable energy-based hydrogen production to support carbon neutrality goals. Solar and wind-powered electrolysis projects are increasing in northern and western China. Government policies encourage clean hydrogen for transportation use. Green hydrogen reduces lifecycle emissions of fuel cell vehicles. Large energy companies are building renewable hydrogen plants.

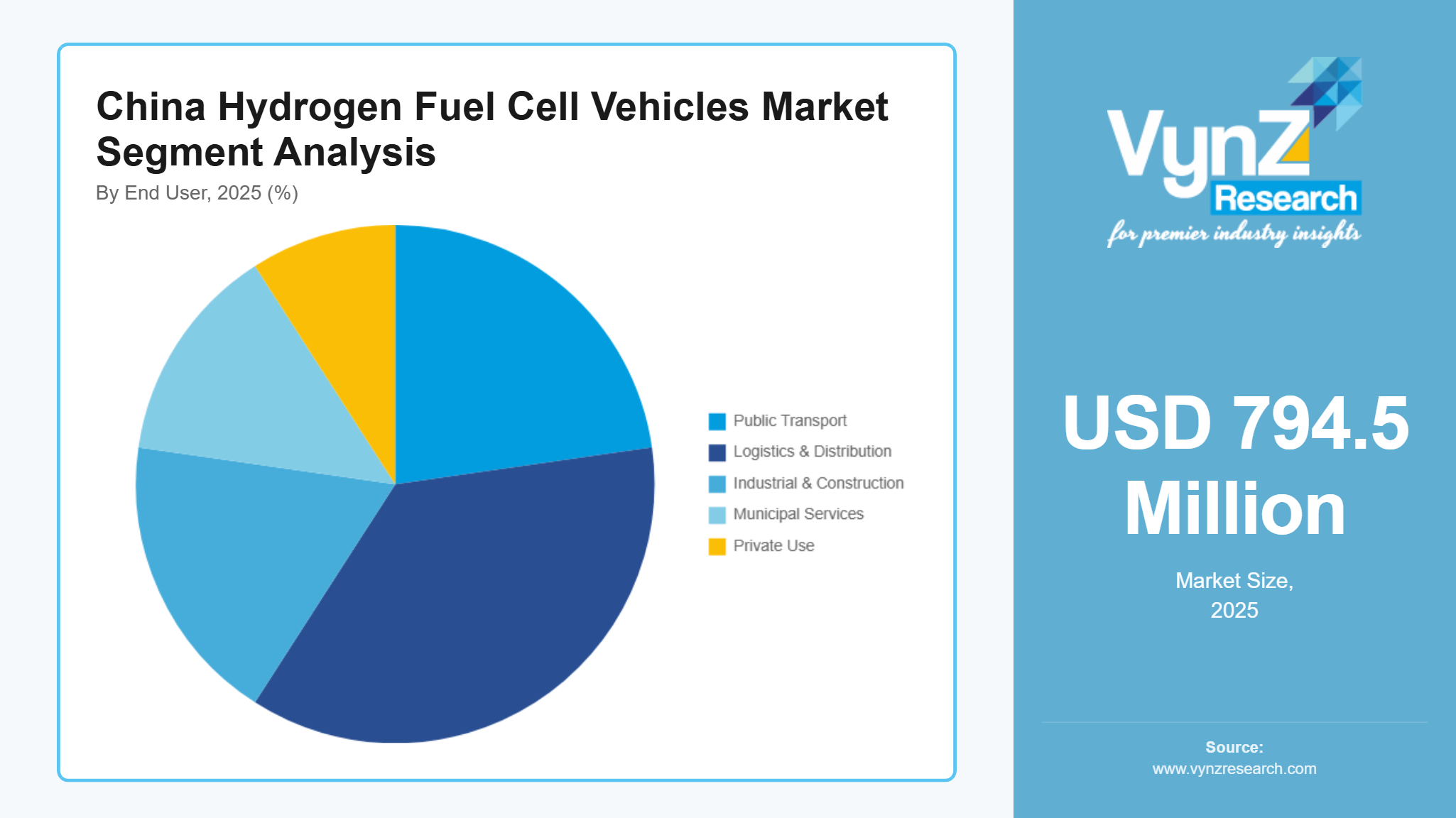

By End User

Logistics & Distribution is the largest category with a market share of around 40% in 2025, because hydrogen fuel cell vehicles are widely used in freight transport, port operations, and industrial logistics where long range and high load capacity are required. China’s large manufacturing and export industry creates high demand for heavy transport vehicles. Fuel cell trucks are suitable for continuous operation with minimal downtime. Government pilot programs focus on logistics fleets to achieve faster commercialization.

Public Transport is the fastest-growing category during the forecast period, because Chinese cities are rapidly adopting hydrogen buses to reduce urban emissions. Municipal governments receive funding for clean transportation projects. Fuel cell buses are suitable for high daily usage due to fast refuelling. Many city-cluster programs prioritize public transport deployment. Air-quality regulations are encouraging replacement of diesel buses. Hydrogen buses help meet carbon-reduction targets.

Regional Insights

East China

East China is the largest regional market for hydrogen fuel cell vehicles, supported by strong industrial development, advanced automotive manufacturing, and extensive government investment in hydrogen energy infrastructure. Major provinces such as Shanghai, Jiangsu, Zhejiang, and Shandong are leading in fuel cell vehicle deployment due to high logistics demand and strong policy support for clean transportation. The region has well-developed hydrogen refueling networks and several city-cluster demonstration projects that promote the use of fuel cell buses, trucks, and municipal vehicles. Local governments provide subsidies, land support, and funding for hydrogen production and refueling stations, which accelerates adoption. The Green Hydrogen Energy Application Project supports demonstration projects in cities such as Ningdong, Dalian, and Shenyang. Focus areas include renewable hydrogen production, infrastructure development, and technology deployment. The initiative aims to reduce 147 million tonnes of CO₂ emissions and create around 50,000 green jobs. East China also has strong participation from automotive manufacturers, energy companies, and research institutions working on fuel cell technology. The presence of large ports, industrial zones, and freight corridors increases the demand for heavy-duty hydrogen vehicles. In addition, the region’s advanced power grid and renewable energy integration support hydrogen production projects.

South China

South China is one of the fastest-growing regions in the hydrogen fuel cell vehicles market, driven by rapid industrialization, strong economic growth, and increasing investment in clean energy technologies in provinces such as Guangdong, Guangxi, and Fujian. Cities like Shenzhen and Guangzhou are actively promoting hydrogen buses, logistics trucks, and municipal vehicles as part of their low-carbon transportation programs. The region has strong manufacturing capability in electronics, automotive components, and energy equipment, which supports the development of fuel cell systems and hydrogen infrastructure. Government policies encouraging new energy vehicles and smart city projects are accelerating the construction of hydrogen refuelling stations. China introduced a performance-based subsidy program in 2020 to accelerate hydrogen fuel cell vehicle adoption. The central government allocated up to RMB 17 billion (about USD 2.5 billion) over four years. With additional local government support, total funding could reach around RMB 34 billion (USD 5 billion). The program aims to deploy about 37,500–60,000 hydrogen fuel cell vehicles in demonstration city clusters. In addition, port transportation and export-oriented industries create high demand for heavy-duty fuel cell trucks. Private investment and partnerships between automakers and energy companies are also increasing in the region. Renewable energy projects in South China are supporting the production of cleaner hydrogen fuel. With strong policy backing and industrial demand, South China is witnessing rapid growth in hydrogen fuel cell vehicle adoption.

North China

North China holds a significant share in the hydrogen fuel cell vehicles market due to strong government initiatives, large hydrogen production capacity, and active demonstration projects in Beijing, Tianjin, Hebei, and Inner Mongolia. Inner Mongolia government approved a 200-MW green hydrogen project capable of producing about 14,400 tonnes of hydrogen annually. Additional renewable-hydrogen pilot projects combine 369.5 MW wind power and 1,850 MW solar capacity to produce hydrogen through electrolysis. The region has abundant wind and solar energy resources, which makes it suitable for large-scale green hydrogen production to support fuel cell transportation. Government-supported city-cluster programs are heavily concentrated in North China, encouraging the deployment of hydrogen buses, trucks, and industrial vehicles. The presence of steel, mining, and heavy manufacturing industries increases the demand for heavy-duty fuel cell transport solutions. Local governments are investing in hydrogen refuelling stations, storage facilities, and supply chains to support commercial vehicle fleets. Strict emission control policies in major cities are also pushing the adoption of zero-emission vehicles. State-owned energy companies are actively involved in building hydrogen production and distribution networks.

Central China

Central China is an emerging market for hydrogen fuel cell vehicles, supported by growing industrial activity and government programs aimed at expanding clean energy transportation in provinces such as Hubei, Henan, and Hunan. The region is an important manufacturing and logistics hub, which creates demand for fuel cell trucks and commercial vehicles for freight movement. Government initiatives are encouraging the construction of hydrogen refuelling stations along major transport routes to support long-distance logistics. Central China is also benefiting from national hydrogen development plans that aim to expand fuel cell vehicle deployment beyond coastal regions. Local authorities are promoting pilot projects for hydrogen buses and municipal vehicles to reduce urban emissions. The presence of automobile manufacturing and heavy industry supports the adoption of fuel cell technology. China had over 540 hydrogen refuelling stations by 2024, representing the largest network globally. State-owned energy companies plan large infrastructure expansion programs. The government aims to create the world’s largest hydrogen refuelling network by 2030. Investment in renewable energy projects is also helping future green hydrogen production.

West China

West China is a developing region in the hydrogen fuel cell vehicles market, driven by large renewable energy resources and government efforts to build a long-term hydrogen supply network in provinces such as Sichuan, Shaanxi, Gansu, Xinjiang, and Chongqing. The region has strong potential for green hydrogen production due to abundant solar and wind power, which supports future fuel cell vehicle deployment. Government policies are promoting hydrogen energy projects to support industrial transport, mining, and long-haul freight operations common in this region. Infrastructure development is gradually expanding through national hydrogen corridor and clean transportation programs. Although current vehicle deployment is lower compared to eastern provinces, investment in hydrogen production and storage facilities is increasing. Pilot projects for hydrogen trucks and industrial vehicles are being tested in resource-rich areas. Regional development programs are also encouraging the use of clean energy in transportation.

Competitive Landscape / Company Insights

The China hydrogen fuel cell vehicles market is moderately consolidated, led by large state-owned automotive groups, major energy companies, and fuel cell technology manufacturers that have strong financial capability and government support for hydrogen development projects. State-owned enterprises such as SAIC Motor Corporation Limited, Dongfeng Motor Corporation, and FAW Group Co., Ltd. play a major role in vehicle production, supported by national policies promoting hydrogen mobility in commercial transport and public transportation fleets. Large energy companies including China Petroleum & Chemical Corporation (Sinopec), China National Petroleum Corporation (CNPC), and China Energy Investment Corporation are expanding hydrogen production and refuelling infrastructure, giving them a strong advantage in building nationwide hydrogen supply networks. Their ability to integrate fuel production, storage, and distribution with transportation projects supports large-scale deployment of fuel cell vehicles across industrial regions and logistics corridors.

Technology providers such as Weichai Power Co., Ltd., Shanghai REFIRE Group, and Ballard Power Systems Inc. are competing by developing fuel cell stacks, hydrogen systems, and powertrain components with improved efficiency and durability. Automotive manufacturers including Foton Motor Inc., Yutong Bus Co., Ltd., and Great Wall Motor Company Limited are focusing on hydrogen buses, trucks, and heavy-duty vehicles to meet government targets for zero-emission transport. Energy companies are also converting existing fuel stations into hydrogen refuelling stations to expand infrastructure quickly using existing retail networks. In addition, joint ventures between automakers, research institutes, and local governments are common in China to accelerate technology development and reduce production costs.

Mini Profiles

SAIC Motor Corporation Limited is one of the largest automotive manufacturers in China and a key developer of hydrogen fuel cell vehicles, producing fuel cell passenger cars, buses, and commercial vehicles while participating in national hydrogen demonstration projects and clean transportation programs.

Dongfeng Motor Corporation is a major state-owned vehicle manufacturer involved in hydrogen fuel cell technology development, focusing on fuel cell trucks, buses, and logistics vehicles supported by government pilot projects and partnerships with fuel cell system suppliers.

FAW Group Co., Ltd. is a leading Chinese automotive group developing hydrogen fuel cell vehicles and powertrain systems, with strong involvement in national new-energy vehicle programs and collaboration with research institutes to advance fuel cell technology.

Beiqi Foton Motor Co., Ltd. is one of the pioneers in hydrogen fuel cell commercial vehicles in China, producing fuel cell buses and heavy-duty trucks widely used in demonstration city clusters and industrial transport applications.

Yutong Bus Co., Ltd. is a major bus manufacturer actively deploying hydrogen fuel cell buses for public transportation fleets, supplying vehicles for municipal clean transport projects and government-supported hydrogen mobility programs across several Chinese cities.

Weichai Power Co., Ltd. is a leading fuel cell technology developer in China, investing in hydrogen powertrain systems, fuel cell stacks, and commercial vehicle applications, while collaborating with domestic and international partners to improve efficiency and durability.

Key Players

- SAIC Motor Corporation Limited

- Dongfeng Motor Corporation

- FAW Group Co., Ltd.

- Beiqi Foton Motor Co., Ltd.

- Yutong Bus Co., Ltd.

- Weichai Power Co., Ltd.

- Beijing SinoHytec Co., Ltd.

- Shanghai REFIRE Technology Co., Ltd.

- Sinosynergy Hydrogen Energy Technology Co., Ltd.

- China Petroleum & Chemical Corporation (Sinopec)

- China National Petroleum Corporation (CNPC)

- Horizon Fuel Cell Technologies

Recent Developments

January 2026 – China Petroleum & Chemical Corporation (Sinopec) announced expansion of hydrogen refuelling stations across major logistics corridors in China to support large-scale deployment of hydrogen fuel cell trucks and buses.

December 2025 – SAIC Motor Corporation Limited introduced a new generation hydrogen fuel cell commercial vehicle platform designed for long-distance freight transport with improved efficiency and longer driving range.

October 2025 – Weichai Power Co., Ltd. expanded its fuel cell engine production capacity to support growing demand for hydrogen buses and heavy-duty trucks under national hydrogen demonstration programs.

August 2025 – Beijing SinoHytec Co., Ltd. launched an upgraded fuel cell stack system with higher durability and power output for commercial vehicles used in city-cluster hydrogen mobility projects.

June 2025 – Dongfeng Motor Corporation partnered with several provincial governments to deploy hydrogen fuel cell logistics trucks in industrial zones and port transportation fleets.

April 2025 – Yutong Bus Co., Ltd. delivered a new batch of hydrogen fuel cell buses for municipal public transport fleets as part of China’s clean energy transportation initiative.

China Hydrogen Fuel Cell Vehicles Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Buses

- Trucks

- Light Commercial Vehicles (LCV)

- Heavy Commercial Vehicles (HCV)

- Special Purpose Vehicles

Technology Insight and Forecast 2026 - 2035

- Proton Exchange Membrane Fuel Cell (PEMFC)

- Phosphoric Acid Fuel Cell (PAFC)

- Solid Oxide Fuel Cell (SOFC)

- Others

Range Insight and Forecast 2026 - 2035

- Short Range (Below 300 km)

- Medium Range (300–500 km)

- Long Range (Above 500 km)

Hydrogen Source Insight and Forecast 2026 - 2035

- Grey Hydrogen

- Blue Hydrogen

- Green Hydrogen

End User Insight and Forecast 2026 - 2035

- Public Transport

- Logistics & Distribution

- Industrial & Construction

- Municipal Services

- Private Use

China Hydrogen Fuel Cell Vehicles Market by Region

- East China

- By Vehicle Type

- By Technology

- By Range

- By Hydrogen Source

- By End User

- South China

- By Vehicle Type

- By Technology

- By Range

- By Hydrogen Source

- By End User

- North China

- By Vehicle Type

- By Technology

- By Range

- By Hydrogen Source

- By End User

- Central China

- By Vehicle Type

- By Technology

- By Range

- By Hydrogen Source

- By End User

- West China

- By Vehicle Type

- By Technology

- By Range

- By Hydrogen Source

- By End User

Table of Contents for China Hydrogen Fuel Cell Vehicles Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Technology

1.2.3. By

Range

1.2.4. By

Hydrogen Source

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. China Market Estimate and Forecast

4.1. China Market Overview

4.2. China Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger Cars

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Buses

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Trucks

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Light Commercial Vehicles (LCV)

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Heavy Commercial Vehicles (HCV)

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Special Purpose Vehicles

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Proton Exchange Membrane Fuel Cell (PEMFC)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Phosphoric Acid Fuel Cell (PAFC)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Solid Oxide Fuel Cell (SOFC)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Others

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Range

5.3.1. Short Range (Below 300 km)

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Medium Range (300–500 km)

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Long Range (Above 500 km)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Hydrogen Source

5.4.1. Grey Hydrogen

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Blue Hydrogen

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Green Hydrogen

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Public Transport

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Logistics & Distribution

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial & Construction

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Municipal Services

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Private Use

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. East China Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Technology

6.3. By

Range

6.4. By

Hydrogen Source

6.5. By

End User

7. South China Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Technology

7.3. By

Range

7.4. By

Hydrogen Source

7.5. By

End User

8. North China Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Technology

8.3. By

Range

8.4. By

Hydrogen Source

8.5. By

End User

9. Central China Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Technology

9.3. By

Range

9.4. By

Hydrogen Source

9.5. By

End User

10. West China Market Estimate and Forecast

10.1. By

Vehicle Type

10.2. By

Technology

10.3. By

Range

10.4. By

Hydrogen Source

10.5. By

End User

11. Company Profiles

11.1.

SAIC Motor Corporation Limited

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

Dongfeng Motor Corporation

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

FAW Group Co., Ltd.

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Beiqi Foton Motor Co., Ltd.

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Yutong Bus Co., Ltd.

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

Weichai Power Co., Ltd.

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

Beijing SinoHytec Co., Ltd.

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

Shanghai REFIRE Technology Co., Ltd.

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

Sinosynergy Hydrogen Energy Technology Co., Ltd.

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

China Petroleum & Chemical Corporation (Sinopec)

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

11.11.

China National Petroleum Corporation (CNPC)

11.11.1.

Snapshot

11.11.2.

Overview

11.11.3.

Offerings

11.11.4.

Financial

Insight

11.11.5.

Recent

Developments

11.12.

Horizon Fuel Cell Technologies

11.12.1.

Snapshot

11.12.2.

Overview

11.12.3.

Offerings

11.12.4.

Financial

Insight

11.12.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

China Hydrogen Fuel Cell Vehicles Market