E-Commerce Automotive Aftermarket Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Engine Parts, Brake Parts, Suspension & Steering Parts, Electrical & Lighting Components, Filters (Air, Oil, Fuel, Cabin), Batteries, Wheels & Tires, Accessories), by Vehicle Type (Passenger Cars, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), by End User (Do-It-Yourself (DIY) Consumers, Professional Repair Workshops / Do-It-For-Me (DIFM)), by Sales Channel (Third-Party Marketplaces, Direct-to-Consumer (D2C) Websites, Online Retailers / E-Commerce Platforms)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9666 | Industry : Automotive & Transportation | Available Format :

|

Page : 172 |

E-Commerce Automotive Aftermarket Overview

The e-commerce automotive aftermarket, valued at approximately USD 306.3 billion in 2025 and estimated to reach around USD 345.5 billion in 2026, is projected to reach close to USD 1,021.4 billion by 2035, expanding at a CAGR of about 12.8% from 2026 to 2035.

.webp)

The market is primarily driven by the rapid growth of digital retail platforms that enable consumers and automotive repair professionals to purchase vehicle parts and accessories conveniently online. The rising internet penetration, use of smartphones, and rising consumer confidence with online payment systems have greatly transformed the purchasing behavior of customers who formerly used the conventional auto parts stores to online markets. These sites provide an extensive range of authentic and counterfeit parts, good prices, comparison of products, and easy delivery of products at home, which are very appealing to customers.

Moreover, the increasing age of vehicles in the world increases the demand of replacement parts, maintenance products, and repair components, which are increasingly being procured online. There are also e-commerce sites that offer car-specific search engines that enable buyers to easily locate parts that are compatible with their car to enhance the accuracy of their purchases and to save on time. Moreover, manufacturers and distributors are increasing their direct-to-consumer online approaches and collaborating with large e-commerce marketplaces to access more clients.

E-Commerce Automotive Aftermarket Dynamics

Market Trends

The expansion of online automotive parts marketplaces is a major trend shaping the e-commerce automotive aftermarket. Online stores are becoming rapidly available with large parts databases of both OEM and aftermarket parts, accessories, tools and maintenance products that enable customers to be able to compare and shop at a single source. These online stores bring together manufacturers, distributors, retailers, and consumers in one online platform and this has greatly enhanced the accessibility and availability of products. The FAME II (Faster Adoption and Manufacturing of Electric Vehicles in India Phase II) program was launched by the Government of India in 2019 with a budget allocation of ₹10,000 crore to promote electric vehicle adoption through subsidies for EVs and the development of charging infrastructure across the country. Special car segments within many large automotive retailers and international e-commerce platforms are also being invested in to offer car parts specific search filters and compatibility checks to be used in the proper selection of parts. There is also a growth of partnerships between components suppliers and online services that are increasing the product exposure and the possibility of direct sales to the final consumer. Better logistical systems, faster delivery services and effective inventory management systems also help these marketplaces to expand.

Growth Drivers

Rising internet penetration and smartphone usage is a significant growth driver for the e-commerce automotive aftermarket. The rising access to fast internet and low-cost smartphones has made more consumers able to access online automotive marketplaces with ease. Under mobile devices, owners and repair experts will have the opportunity to search, compare, and shop automotive parts wherever and whenever. The online apps created in smartphones and the websites that are mobile optimized offer easy user interfaces, safe online payment methods, and fast product search, and all these contribute to the overall purchasing experience. The U.S. government allocated about USD 65 billion under the Infrastructure Investment and Jobs Act (2021) to expand broadband internet access nationwide. Moreover, mobile connectivity enables a customer to review, detect the compatibility of products, and obtain installation instructions as well as making purchase decisions. The increasing popularity of mobile commerce has promoted investment in specific mobile platforms and online catalogues by automotive retailers and manufacturers.

Market Restraints / Challenges

Risk of counterfeit and low-quality automotive parts is a major challenge in the e-commerce automotive aftermarket. The character of the online markets as an open market enables a few third-party sellers to sell automotive components, exposing the industry to the threat of fake, substandard, or uncertified parts making their way into the market. Such low-quality products can be like real parts yet in most cases they are not as safe or perform as well hence thus affecting the reliability and trust of the customers towards the vehicles. Customers who buy products through the internet might be unable to authenticate products, particularly when purchasing the products of a new vendor or bookstore. The reputation of a genuine manufacturer and distributor can also be harmed due to the use of counterfeit parts. Moreover, the use of poor-quality components can cause car malfunction, increased maintenance and possible risk of accidents.

Market Opportunities

Expansion of online sales for electric vehicle (EV) components is creating significant opportunities in the e-commerce automotive aftermarket. The need to manufacture more electric vehicles across the globe has also led to an increase in the demand of specialized electric vehicle parts, including batteries, charging cables, power electronics, thermal management system, and electronic control modules. Through online platforms, EV owners, service centers, and fleet operators can simply locate an extensive array of EV parts and accessories in various manufacturers and suppliers. Chinese battery manufacturer Contemporary Amperex Technology Co., Limited (CATL) announced an investment of about €7.3 billion (approximately USD 8–8.5 billion) to build a large EV battery manufacturing plant in eastern Hungary. The facility is planned with an annual production capacity of around 100 GWh and is expected to supply batteries to major automakers such as BMW, Stellantis, and Volkswagen in Europe. E-commerce channels also allow specifications on products, compatibility, and customer reviews; this assists the buyers to make informed choices of purchasing products. Also, most EV component makers continue to extend their online sales and integrate into online retailers to reach more consumers. Better logistic networks and quicker delivery services enhance even further the accessibility of EV parts via the online platform.

Global E-Commerce Automotive Aftermarket Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 306.3 Billion |

|

Revenue Forecast in 2035 |

USD 1021.4 Billion |

|

Growth Rate |

12.8% |

|

Segments Covered in the Report |

Product Type, Vehicle Type, End User, Sales Channel |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Rest of the World |

|

Key Companies |

Amazon.com, Inc., Alibaba Group Holding Limited, eBay Inc., AutoZone, Inc., Advance Auto Parts, Inc., O’Reilly Automotive, Inc., National Automotive Parts Association (NAPA Auto Parts), U.S. Auto Parts Network, Inc. (CarParts.com, Inc.), RockAuto, LLC, CARiD.com, LKQ Corporation, The Pep Boys. |

|

Customization |

Available upon request |

E-Commerce Automotive Aftermarket Segmentation

By Product Type

Electrical & lighting components are the largest category with a market share of about 20% in 2025, because of their frequent replacement rates and the need within various types of vehicles. Other common products to be sold via e-commerce include headlights, sensors, alternators, starters, and wiring harnesses, which are not very expensive to ship and are relatively standardized. The trend of electronic systems in the modern cars also intensifies the demand of these components. There are also broad lists of products and compatibility features available online marketplaces that enable customers to conveniently find the right electrical parts. Also, the various electrification and digitalization of vehicles have greatly diversified the number of electrical aftermarket products sold over the Web.

Accessories are the fastest-growing category with a CAGR of around 13.2% during the forecast period, driven by increasing consumer interest in vehicle customization and convenience features. There are many accessories including infotainment systems, seat covers, phone mounts, interiors light kits, and exterior styling products that can be easily accessed online. The effect of social media, online reviews and online marketing campaigns is pushing vehicle owners to upgrade their vehicles with aftermarket accessories. They are also more appealing to DIY consumers since the products are easy to install when, in comparison, installed mechanical parts are difficult to install. In addition, online car dealers have been growing at a rapid pace, and this has enhanced the availability of products and the speed at which they can be delivered.

By Vehicle Type

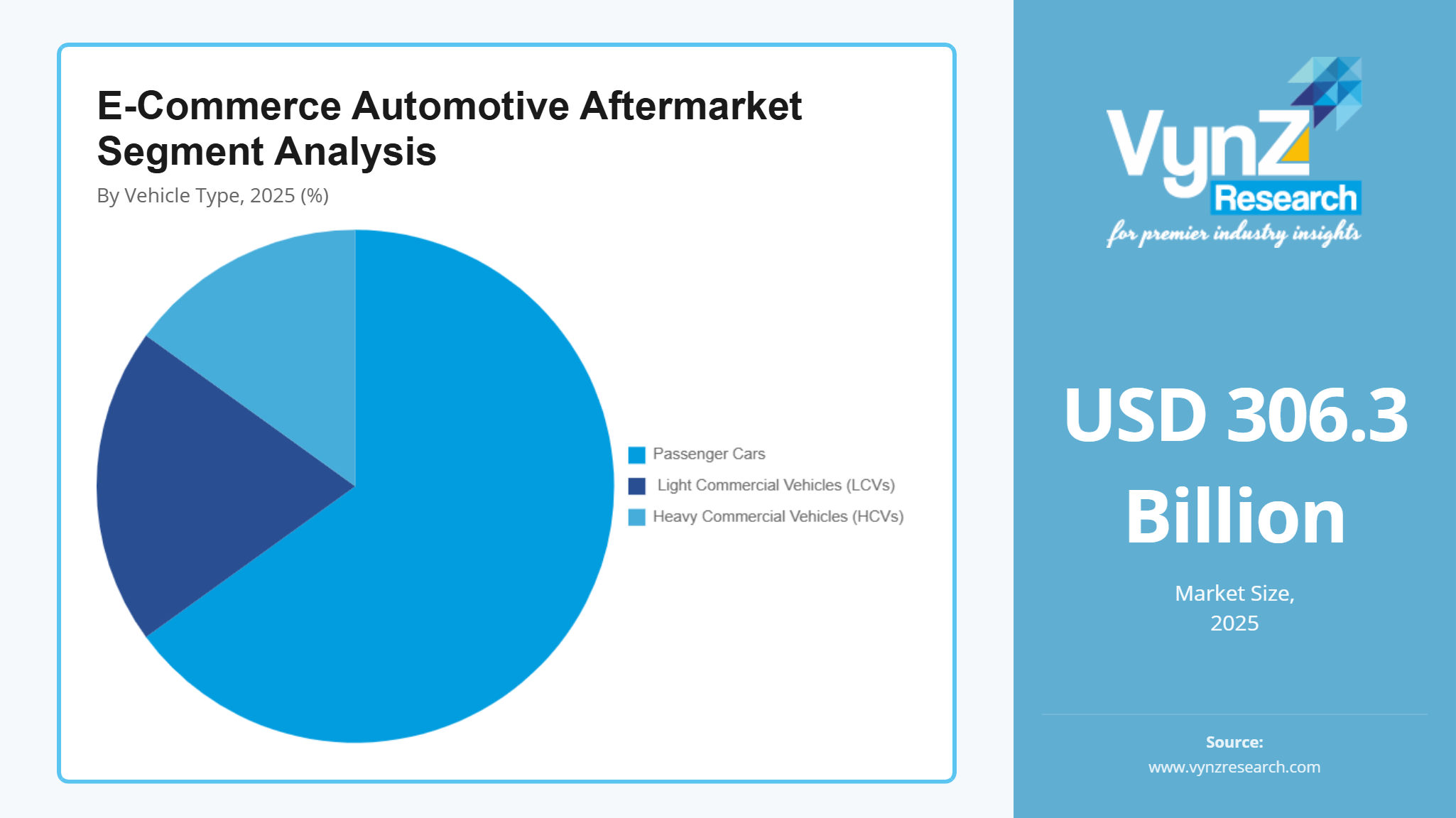

Passenger cars are the largest category with a market share of about 65% in 2025, supported by the massive global passenger vehicle fleet and higher consumer participation in online purchasing. Passenger car owners frequently purchase replacement parts such as filters, brake pads, lighting systems, and accessories through e-commerce platforms. The growing adoption of digital retail platforms among individual consumers further strengthens demand in this segment. In addition, passenger vehicles generally require more frequent maintenance compared to commercial fleets, increasing the demand for replacement components. E-commerce platforms also provide vehicle-specific compatibility tools that make it easier for passenger car owners to identify correct parts.

Light Commercial Vehicles (LCVs) are the fastest-growing category during the forecast period, driven by the rapid expansion of e-commerce logistics and last-mile delivery services. Many businesses operating delivery fleets increasingly rely on online platforms to procure maintenance parts quickly and cost-effectively. The growth of urban logistics networks has significantly increased the number of LCVs used for commercial operations. Fleet operators are also adopting digital procurement channels to streamline purchasing and reduce downtime. Online platforms provide faster delivery and competitive pricing, making them highly attractive for fleet maintenance.

By End User

Professional Repair Workshops / Do-It-For-Me (DIFM) are the largest category with a market share of about 60% in 2025, because most vehicle owners continue to prefer professional technicians to conduct maintenance and repair services. Service centers and shops tend to buy parts and automotive products online at large quantities to save money and be able to find a broader variety of goods. E-commerce sites would offer the repair experts speedy price comparison, availability information on the products and expedited delivery services. There are also numerous distributors with specialized digital platforms that are used by workshops and automotive services providers. Also, advanced vehicle technologies demand professional skills to install them, which perpetuates the demand of professional repair networks.

Do-It-Yourself (DIY) Consumers are the fastest-growing category during the forecast period, due to the rising consumer awareness and accessibility of internet automotive resources. The online platform offers installation instructions, product reviews, and other technical instructions that persuade vehicle owners to do some basic maintenance on their own. DIY consumers are especially fond of accessories, lighting-related products, filters, and other small spare parts. This trend is also supported by availability of low-priced tools and products that can be installed easily. Moreover, younger vehicle owners feel less hesitant to buy the parts online and make simple upgrades to the vehicle on their own.

By Sales Channel

Third-Party marketplaces are the largest category with a market share of about 55% in 2025, as these platforms aggregate products from numerous suppliers, manufacturers, and distributors. Large online marketplaces provide customers with extensive product catalogs, competitive pricing, and convenient delivery options. They also offer product reviews, ratings, and compatibility filters that help consumers make informed purchasing decisions. Many automotive parts sellers prefer third-party platforms because they provide access to a broad customer base without requiring large investments in independent digital infrastructure. Additionally, integrated logistics and payment systems simplify the purchasing process. Consequently, third-party marketplaces dominate the sales channel landscape in the E-Commerce automotive aftermarket.

Direct-to-Consumer (D2C) websites are the fastest-growing category with a CAGR of around 13.5% during the forecast period, as automotive parts manufacturers increasingly develop their own digital sales channels. By selling directly through branded websites, companies can strengthen customer relationships, improve profit margins, and maintain greater control over product pricing and authenticity. Many manufacturers are also offering exclusive online promotions, warranties, and product bundles through their official platforms. Digital marketing strategies and brand-focused e-commerce stores are helping manufacturers reach customers more effectively. In addition, concerns regarding counterfeit products on open marketplaces are encouraging consumers to purchase directly from official brand websites.

Regional Insights

North America

North America is the largest regional market for the e-commerce automotive aftermarket, supported by a highly developed digital commerce ecosystem and strong vehicle ownership rates. The United States controls the regional market because of the popularity of online retailing systems of buying automotive parts and accessories. Price comparison, products availability and quick delivery services rapidly gain popularity among consumers as well as professional repair workshops through the digital marketplace. The area is also blessed by the fact that there is an effective logistics network, and thus automotive parts can be saved in the area and delivered within the day or the next day. The Automotive Supplier Innovation Program (ASIP) was launched by the Government of Canada with an investment of CAD 100 million (about USD 75 million) over five years to support research, development, and demonstration projects in the automotive supply chain. Additionally, the presence of high non-buying power of e-commerce and aftermarket parts also enhances growth of the market further. The high level of consumer awareness, improved payment systems, and high number of old vehicles on the road remains a strong driver in online automotive parts purchase among the North American region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the e-commerce automotive aftermarket, driven by rapid digitalization, increasing internet penetration, and expanding vehicle ownership across emerging economies. The sales of online automotive parts are growing tremendously in the countries like China, India, Japan, and South Korea due to the rise in consumer use of online retail information. Due to the high growth of e-commerce systems and mobile commerce apps, automotive parts are now more accessible to consumers as well as repair shops. The Government of India introduced the PLI scheme for automobiles and auto components with a budget outlay of ₹25,938 crore to boost domestic manufacturing of advanced automotive technology components. An increase in the disposable income and the increased trend in vehicle customization is also adding into the demand of aftermarket accessories. Moreover, this high population of vehicles in the region of large and old age needs common maintenance and parts of replacement. Rapid development of the logistics networks and online payment systems makes the transition to online automotive aftermarket platforms in Asia-Pacific even faster.

Europe

Europe maintains a strong presence in the e-commerce automotive aftermarket due to the region’s well-established automotive industry and increasing adoption of digital retail platforms. Countries such as Germany, the United Kingdom, France, Italy, and Spain are major contributors to online automotive parts sales. Consumers across the region increasingly prefer online platforms for purchasing replacement components, accessories, and maintenance products due to price transparency and wider product availability. The growing average age of vehicles in Europe also drives demand for replacement parts through online channels. The European Union allocated about €723.8 billion under the Recovery and Resilience Facility to support economic recovery and digital transformation. A significant portion of this funding is directed toward digital infrastructure, smart logistics, and digital commerce systems, which strengthen the online retail ecosystem and support the growth of e-commerce automotive parts distribution. Moreover, well-established regulatory policies that provide a guarantee of quality products and consumer protection increases confidence in e-commerce dealings. The fact that some of the major automotive parts producers and distributors are present in the region also contributes to the expansion of digital aftermarket solutions in the area.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing steady growth in the e-commerce automotive aftermarket as digital commerce infrastructure continues to develop. In Latin America, countries such as Brazil and Mexico are witnessing rising adoption of online automotive marketplaces due to increasing internet penetration and smartphone usage. The Middle East, particularly the United Arab Emirates and Saudi Arabia, is seeing growing demand for online automotive accessories and replacement parts driven by high vehicle ownership rates. In Africa, expanding mobile connectivity and digital payment solutions are gradually enabling consumers to access online automotive retail platforms. Under Saudi Vision 2030, the Government of Saudi Arabia has planned investments exceeding about USD 1 trillion to diversify the economy and develop sectors such as digital infrastructure, logistics, and e-commerce ecosystems. Although e-commerce infrastructure is still developing in several countries, increasing digital adoption and expanding logistics networks are expected to support steady market growth across these regions.

Competitive Landscape / Company Insights

The e-commerce automotive aftermarket is moderately fragmented, characterized by the presence of global e-commerce platforms, specialized automotive parts retailers, and direct-to-consumer digital channels operated by manufacturers. Major online marketplaces such as Amazon.com, Inc. and eBay Inc. play a significant role by offering extensive product catalogs, competitive pricing, and advanced logistics networks that enable fast delivery of automotive parts and accessories. Dedicated automotive e-commerce stores such as AutoZone, Inc., Advance Auto Parts, Inc. and O'Reilly Automotive, Inc. are rivals with a combination of solid physical retailing stores and their effective online platforms offering omnichannel shopping and in-store pickup services. Online technologies like the CarParts.com, Inc. are based on online catalog, vehicle compatibility features, and effective supply chain management to enhance consumer and repair workshop online shopping experience. Automotive parts producers are as well growing direct-to-consumer (D2C) tactics by building branded online shops to reinforce shopper involvement and lessen reliance on third-party commercials.

Mini Profiles

Amazon.com, Inc. is one of the largest global e-commerce platforms offering a vast range of automotive aftermarket products including replacement parts, accessories, maintenance tools, and performance upgrades through its dedicated automotive marketplace while leveraging advanced logistics networks, fast delivery services, and vehicle compatibility tools to support both individual consumers and professional repair workshops across North America, Europe, and Asia-Pacific.

Alibaba Group Holding Limited operates one of the largest digital commerce ecosystems in the world through platforms such as Alibaba.com, AliExpress, and Tmall, providing automotive aftermarket components, accessories, and replacement parts to global buyers while connecting manufacturers, wholesalers, and retailers through cross-border e-commerce infrastructure and large-scale digital marketplaces.

eBay Inc. is a major global online marketplace that facilitates the buying and selling of automotive parts, accessories, and tools, offering an extensive catalog of new, refurbished, and used components while supporting vehicle compatibility search systems and global seller networks that make it a key platform for both individual car owners and automotive repair professionals.

AutoZone, Inc. is a leading automotive aftermarket retailer that combines a large network of physical retail stores with a strong e-commerce platform offering a wide range of replacement parts including filters, batteries, brake components, lighting systems, and engine parts while supporting customers through online ordering, in-store pickup, and professional repair shop supply services.

Key Players

- Amazon.com, Inc.

- Alibaba Group Holding Limited

- eBay Inc.

- AutoZone, Inc.

- Advance Auto Parts, Inc.

- O’Reilly Automotive, Inc.

- National Automotive Parts Association

- U.S. Auto Parts Network, Inc.

- RockAuto, LLC

- CARiD.com

- LKQ Corporation

- The Pep Boys

Recent Developments

January 2026 – Amazon.com, Inc. expanded its automotive marketplace by introducing enhanced vehicle compatibility tools and faster same-day delivery options for automotive parts across major U.S. metropolitan areas, improving the online purchasing experience for DIY consumers and repair workshops.

December 2025 – eBay Inc. launched an upgraded automotive parts fitment system powered by AI-based search technology, enabling buyers to identify compatible replacement parts more accurately using vehicle identification number (VIN) integration.

October 2025 – Alibaba Group Holding Limited expanded its cross-border automotive aftermarket marketplace through Alibaba.com, enabling global automotive parts manufacturers and suppliers to connect with international buyers and distributors more efficiently.

August 2025 – Advance Auto Parts, Inc. enhanced its omnichannel strategy by upgrading its digital commerce platform and expanding same-day delivery services for online automotive parts orders across several U.S. regions.

June 2025 – O’Reilly Automotive, Inc. strengthened its digital retail capabilities by launching new online catalog tools that allow customers and repair shops to quickly identify vehicle-specific parts and access real-time inventory availability.

April 2025 – CarParts.com, Inc. expanded its distribution network in North America by opening additional fulfillment centers aimed at improving delivery speed and supporting the growing demand for online automotive replacement parts.

Global E-Commerce Automotive Aftermarket Coverage

Product Type Insight and Forecast 2026 - 2035

- Engine Parts

- Brake Parts

- Suspension & Steering Parts

- Electrical & Lighting Components

- Filters (Air

- Oil

- Fuel

- Cabin)

- Batteries

- Wheels & Tires

- Accessories

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

End User Insight and Forecast 2026 - 2035

- Do-It-Yourself (DIY) Consumers

- Professional Repair Workshops / Do-It-For-Me (DIFM)

Sales Channel Insight and Forecast 2026 - 2035

- Third-Party Marketplaces

- Direct-to-Consumer (D2C) Websites

- Online Retailers / E-Commerce Platforms

Global E-Commerce Automotive Aftermarket by Region

- North America

- By Product Type

- By Vehicle Type

- By End User

- By Sales Channel

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Vehicle Type

- By End User

- By Sales Channel

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Vehicle Type

- By End User

- By Sales Channel

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Vehicle Type

- By End User

- By Sales Channel

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for E-Commerce Automotive Aftermarket Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Vehicle Type

1.2.3. By

End User

1.2.4. By

Sales Channel

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Engine Parts

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Brake Parts

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Suspension & Steering Parts

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Electrical & Lighting Components

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Filters (Air

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Oil

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Fuel

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Cabin)

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.1.9. Batteries

5.1.9.1. Market Definition

5.1.9.2. Market Estimation and Forecast to 2035

5.1.10. Wheels & Tires

5.1.10.1. Market Definition

5.1.10.2. Market Estimation and Forecast to 2035

5.1.11. Accessories

5.1.11.1. Market Definition

5.1.11.2. Market Estimation and Forecast to 2035

5.2. By Vehicle Type

5.2.1. Passenger Cars

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Light Commercial Vehicles (LCVs)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Heavy Commercial Vehicles (HCVs)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By End User

5.3.1. Do-It-Yourself (DIY) Consumers

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Professional Repair Workshops / Do-It-For-Me (DIFM)

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Sales Channel

5.4.1. Third-Party Marketplaces

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Direct-to-Consumer (D2C) Websites

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Online Retailers / E-Commerce Platforms

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Vehicle Type

6.3. By

End User

6.4. By

Sales Channel

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Vehicle Type

7.3. By

End User

7.4. By

Sales Channel

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Vehicle Type

8.3. By

End User

8.4. By

Sales Channel

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Vehicle Type

9.3. By

End User

9.4. By

Sales Channel

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Amazon.com, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Alibaba Group Holding Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

eBay Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

AutoZone, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Advance Auto Parts, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

O’Reilly Automotive, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

National Automotive Parts Association

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

U.S. Auto Parts Network, Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

RockAuto, LLC

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

CARiD.com

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

LKQ Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

The Pep Boys

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

E-Commerce Automotive Aftermarket