Europe TIC Market for Automotive Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing Services, Inspection Services, Certification Services), by Sourcing Type (In House, Outsourced), by Application (Vehicle Inspection and Homologation, Electric Vehicle Testing, ADAS and Autonomous Systems Validation, Emission and Environmental Testing), by End Use (Automotive Manufacturers, Suppliers, Aftermarket Service Providers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9667 | Industry : Automotive & Transportation | Available Format :

|

Page : 165 |

Europe TIC Market for Automotive Industry Overview

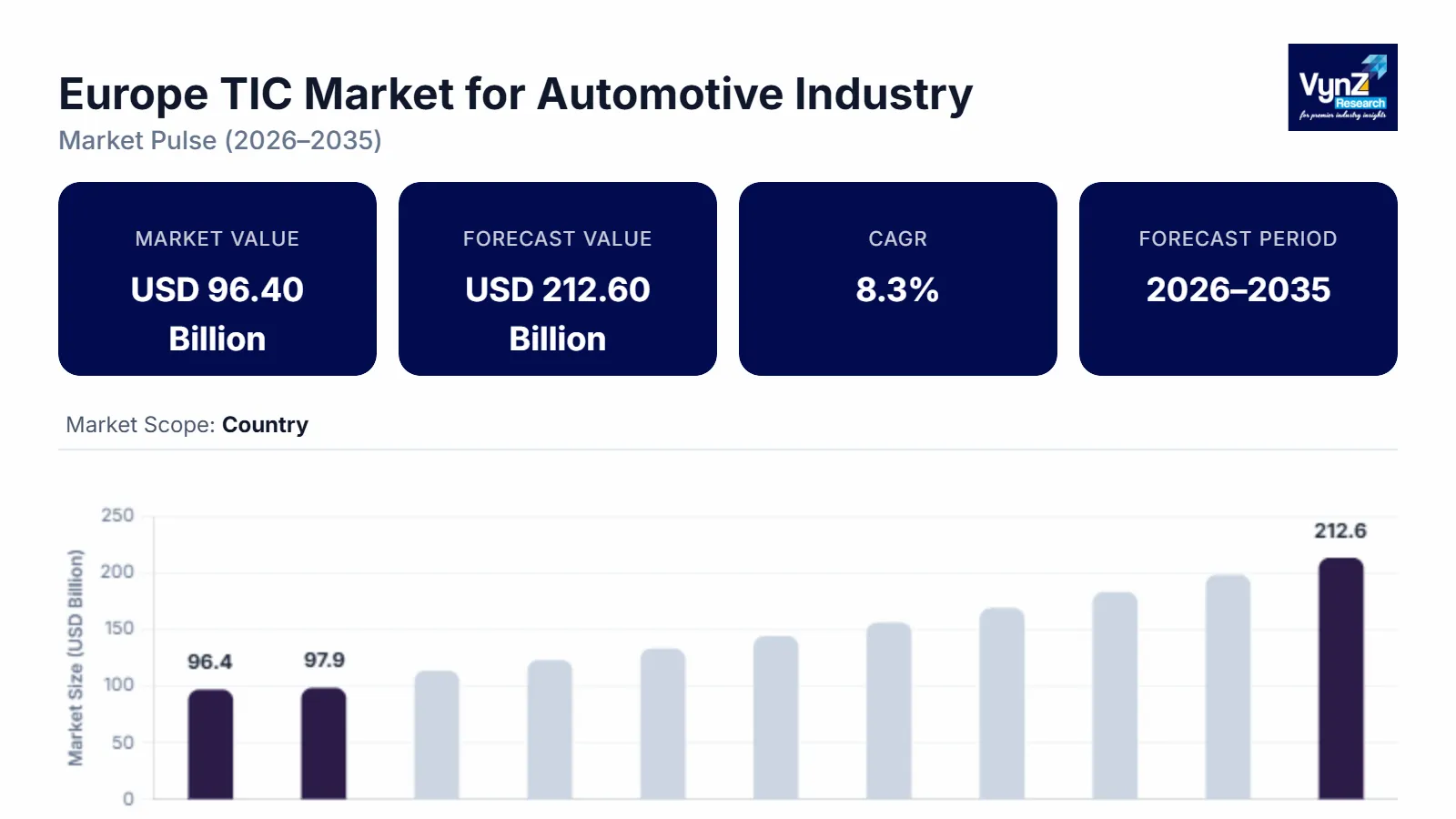

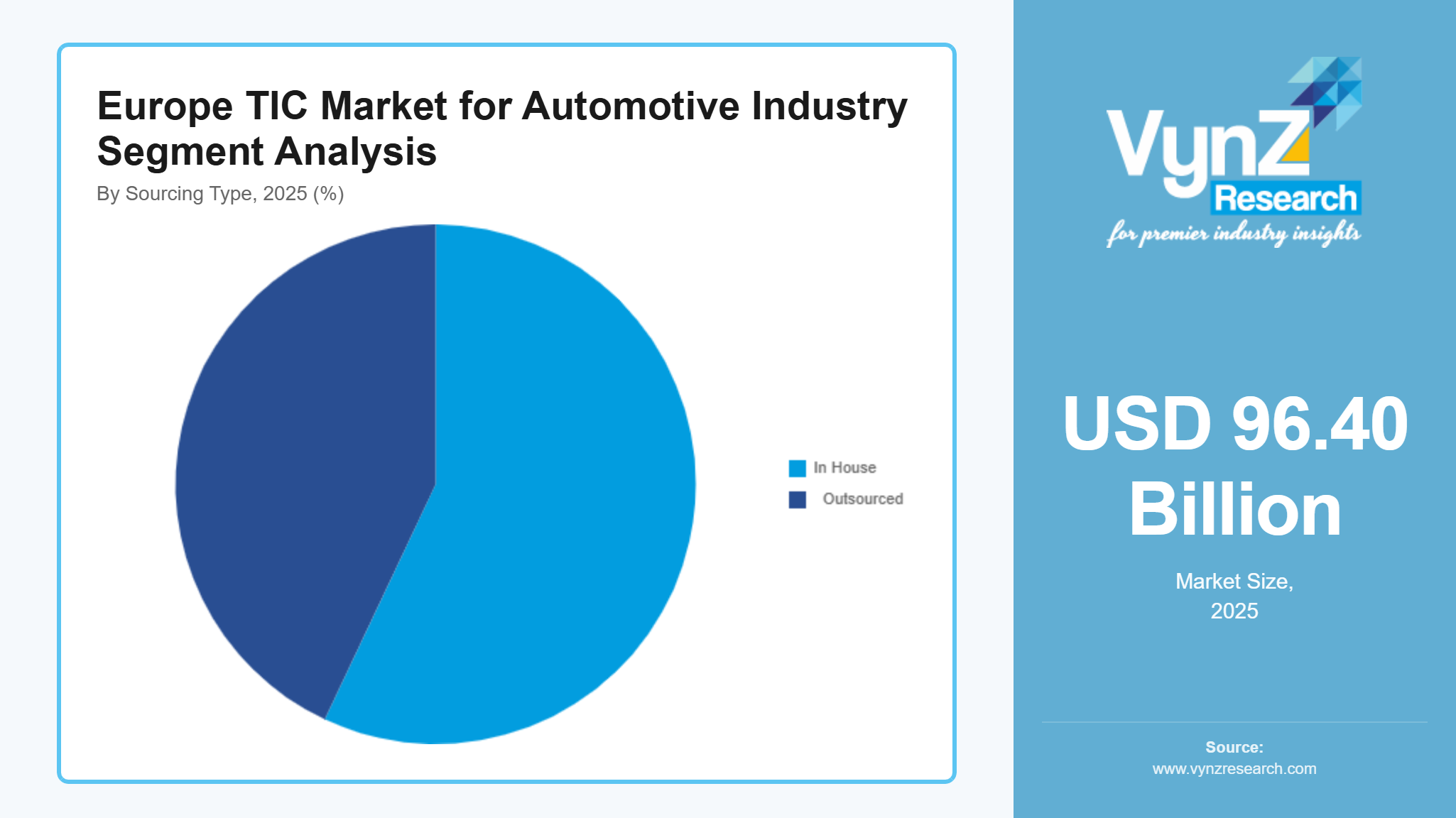

The Europe TIC market for automotive industry market which was valued at approximately USD 96.40 billion in 2025 and is estimated to rise further up to almost USD 97.90 billion in 2026, will reach a value of approximately USD 212.60 billion by 2035 while it expands at a compound annual growth rate of 8.3% between the years 2026 to 2035.

The market experiences growth because of strict regulations which govern vehicle safety and emission standards, the increasing use of advanced vehicle electronics and software, and the rising need for electric and autonomous mobility systems to obtain certification through digital testing and remote inspection and automated validation procedures. The automotive manufacturing industry shows increased demand for regulatory compliance which combined with investments in sustainable mobility initiatives, leads to expansion across major regions that include Germany, France and Italy. Testing, inspection, and certification services in the automotive value chain gain importance through government policies which support climate neutrality targets and electric vehicle adoption.

Europe TIC Market for Automotive Industry Dynamics

Market Trends

The industry sector experiences substantial changes in technology implementation and regulatory compliance because of the industry shift toward electric vehicle technology and software-controlled automobiles. Digital and automated testing solutions have gained increasing market adoption as the primary market trend because they provide improved operational efficiency, testing accuracy and allow for immediate verification of compliance with regulations. The European Commission develops vehicle approval systems that harmonize their operations with digitalization and mobility frameworks and their inspection systems that use data for operational testing which leads to quicker certification processes between member states.

The automotive testing field now uses cybersecurity and software validation practices, which emerged as a new standard, because of UNECE WP.29 regulations that mandate vehicle cybersecurity and software update testing. The developments in this field lead to new service offerings, which companies use to build their operational capabilities through compliance solutions, validation processes, and simulation technologies that help them achieve market advantages while enabling them to monitor their connected vehicle systems according to government digital transport policies.

Growth Drivers

The market expands because mandatory regulatory standards create a continuous need for testing services which automotive manufacturers retail companies automotive fleet operators and electric vehicle producers need. The automotive manufacturing industry and electric vehicle charging station development receive increasing investment, which drives market growth in Germany, France and Italy. The European Environment Agency requires regular testing and certification via testing activities because its emission reduction targets and vehicle safety standards have become more stringent.

The rising numbers of electric vehicle and autonomous vehicle models create a major impact on driving their market adoption. The automotive sector requires advanced testing and certification solutions because manufacturers need to validate safety performance and obtain regulatory approvals. The European Green Deal and sustainable mobility programs implement government supported initiatives, which establish testing framework standards and testing facility standards.

Market Restraints / Challenges

The market experiences present growth barriers, which will prevent it from achieving its full development potential. The regulatory system of multiple jurisdictions creates operational inefficiencies and cost problems that particularly harm smaller service providers and new market entrants. The European Commission regulatory assessments show that organizations need to update their operations to meet new homologation standards, which leads to more administrative work and extended certification processes.

The service providers face operational difficulties because they need to invest in expensive testing equipment and hire specialized workers who operate the advanced testing operations. The costs of specialized technologies and imported equipment and the requirement for technical expertise lead to operational challenges, which become more pronounced during economic downturns. The implementation of advanced testing solutions becomes delayed because of these factors, which also affect the availability of services in specific automotive value chain segments.

Market Opportunities

The market offers extensive chances to succeed through digital and remote inspection solutions, which have gained popularity because of connected and autonomous vehicles becoming more widely used. Automated testing solutions that use data and deliver high performance level testing results to companies, provide companies with testing solutions that match their demand needs. The European Union digital transport initiatives create smart mobility ecosystems, which lead to testing and certification services that will experience future growth through technological advancements.

Another key opportunity lies in the expansion of electric vehicle validation and battery testing services, where rising investments in sustainable mobility infrastructure are creating avenues for long term growth. The operational performance of organizations will increase after they implement advanced simulation technologies, artificial intelligence validation systems and integrated compliance platforms. The government climate and mobility initiatives continue to help develop the new certification frameworks, which align with industry requirements for future certification systems.

Europe TIC Market for Automotive Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 96.40 Billion |

|

Revenue Forecast in 2035 |

USD 212.60 Billion |

|

Growth Rate |

8.3% |

|

Segments Covered in the Report |

By service type, By sourcing type, By application, By end use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, France, Italy, Rest of Europe |

|

Key Companies |

Applus+, Bureau Veritas, DEKRA SE, DNV GL, Eurofins Scientific, Intertek Group plc, Lloyd Register Group Limited, SGS SA, TUV Rheinland, UL LLC |

|

Customization |

Available upon request |

Europe TIC Market for Automotive Industry Segmentation

By Service Type

The industry in 2025 experienced its highest testing services share which generated about 48% of total market revenue. The automotive industry dominance in this market stems from increasing system complexity which requires ongoing safety, emission and performance testing for electric and software driven vehicles. The European Commission and UNECE established regulatory frameworks which mandate standardized testing protocols for vehicle homologation and environmental compliance, thus creating demand throughout the entire manufacturing and supply chain process. The segment continues to grow because organizations increase their investments in advanced laboratory and simulation-based validation technologies.

The fastest growing sector will be inspection and certification services which expect to achieve an 8.6% CAGR from 2026 to 2035 according to current projections. The automotive industry requires periodic compliance checks, lifecycle assessments and third-party validation for both production and aftermarket operations which drives industry growth. The combination of rising regulatory requirements and government-sponsored road safety programs supports technology adoption while digital inspection solutions enhance operational efficiency and scalability throughout the entire supply chain.

By Sourcing Type

The 2025 revenue distribution showed that in-house services accounted for the largest share with approximately 57% of total segment revenue. Automotive manufacturers keep building their internal testing and validation capabilities to protect their quality standards, intellectual property rights and their compliance schedules. European industrial policies which support local manufacturing and innovation ecosystems now encourage OEMs to boost their internal TIC infrastructure development through electric powertrain testing and software validation. The current trend shows that production facilities are integrating advanced diagnostics systems which include real-time monitoring capabilities into their operations.

The projected growth rate for outsourced services shows an estimated CAGR of 8.9% between 2026 and 2035. The market expansion occurs because organizations implement cost optimization methods and regulatory requirements become more complex and they need to obtain independent certification. The demand for specialized expertise combined with accredited testing capabilities has increased for third-party providers who serve small and mid-sized suppliers. The government-backed accreditation frameworks and harmonized compliance standards have created an environment that enables TIC service providers to expand their operations throughout the region.

By Application

The vehicle inspection and homologation sector generated the highest revenue in 2025 which accounted for about 46% of total segment revenue. The dominance of this market exists because all European markets require vehicle approval, emissions compliance and roadworthiness certification as mandatory regulations. The European Green Deal policies together with emission reduction targets create a demand for ongoing vehicle performance and environmental impact assessments. The segment growth has increased because member states now implement standardized testing procedures across their territories.

The validation process for advanced driver assistance systems and electric vehicles will experience rapid growth which will achieve a 9.2% CAGR during the upcoming forecast period. The automotive industry growth comes from three factors which include electrification, autonomous feature deployment and the introduction of new safety standards for connected mobility. Government-backed initiatives create a demand for specialized testing and certification services in this segment because they promote electric vehicle adoption and intelligent transport systems.

By End Use

The automotive manufacturer sector achieved the highest market share in 2025 which accounted for approximately 54% of total market revenue. Large scale production, continuous innovation and strict compliance requirements enable these companies to dominate the market. The European Commission industrial and mobility strategies focus on quality assurance and safety compliance which drives manufacturers to spend on TIC services for regulatory compliance and competitive market position.

The supplier and aftermarket service provider market will expand at a CAGR of 8.4% between 2026 and 2035 according to industry forecasts. The market growth occurs because businesses enter global supply chain, customers need component level certification and companies expand their maintenance and inspection services across the entire vehicle lifecycle. The government-backed road safety programs together with regulatory enforcement have driven industry adoption which leads to continuous market growth throughout the region.

Regional Insights

Germany

Germany produced about 28% of the sector in 2025 because the country possessed a strong automotive manufacturing industry and advanced engineering skills. Major industrial hubs such as Stuttgart, Munich, and Wolfsburg continue to support high demand for testing, inspection, and certification services across vehicle production and component validation. The need for ongoing compliance assessment increases because regulatory enforcement operates according to European Commission vehicle safety and emission standards. Government initiatives which back electric mobility and Industry 4.0 integration are resulting in advanced testing infrastructure investment, while digital validation system growth improves both operational efficiency and market performance.

France

France will hold approximately 21% of the market in 2025 because investors are increasingly supporting sustainable mobility and automotive innovation. Cities such as Paris, Lyon, and Toulouse are witnessing steady adoption of TIC services across electric vehicle manufacturing and component testing. National policies which align with emission reduction targets and clean transport initiatives create ongoing demand for certification and inspection services. Government backed programs which promote electric vehicle adoption and infrastructure development lead manufacturers to enhance their compliance skills, while the use of digital inspection technologies enables further regional expansion.

Italy

Italy will provide approximately 17% of the market in 2025 because automotive component manufacturing and export-oriented production will drive market growth. Industrial regions including Turin, Milan, and Bologna continue to drive demand for testing and certification services across supply chain networks. European regulatory frameworks on vehicle safety and environmental performance are reinforcing the need for standardized validation processes. Government backed industrial modernization initiatives and investments in smart manufacturing are encouraging adoption of advanced TIC solutions, particularly among small and medium sized enterprises seeking compliance with evolving standards.

Rest of Europe

The rest of Europe, including countries such as Spain, the Netherlands, Sweden, and Central and Eastern European economies, accounts for approximately 14% of the market in 2025. The regions experience growth because automotive production expands and foreign investment increases while they establish connections with regional supply chains. Government backed transport policies together with EU level regulatory harmonization create conditions which drive adoption of testing and certification services at new manufacturing centers. The combined share of Germany, France, Italy, and the rest of Europe represents approximately 80% of the market, while the remaining share is distributed across smaller and developing automotive markets within the region not specifically covered above, contributing to long term growth potential.

Competitive Landscape / Company Insights

The market has a competitive environment which ranges from moderate to high because both global and regional companies operate in the market to develop new services and set pricing policies and expand their operations to new regions. The companies in the market need to boost their testing capabilities through advanced testing technologies, digital inspection platforms and automation tools because these technologies will help them achieve better market results. The automotive sector receives support for its certification infrastructure development through EU and UNECE regulatory frameworks and government-funded mobility and safety programs which promote compliance with standards.

Mini Profiles

Applus+ focuses on automotive testing and certification services, supported by strong global presence, regulatory expertise, and integrated solutions that enhance compliance efficiency and strengthen position across European automotive value chains.

Bureau Veritas operates in premium and mass compliance segments, emphasizing quality assurance, safety validation, and sustainability services, supported by extensive inspection networks and strong brand recognition across automotive and industrial sectors.

DEKRA SE leverages local infrastructure and strategic partnerships to expand market presence, offering comprehensive inspection and certification services with strong regulatory alignment and advanced testing capabilities across mobility and transport systems.

Eurofins Scientific focuses on specialized testing and analytical services, supported by advanced laboratory networks, technological expertise, and expanding capabilities in automotive materials and environmental compliance assessments across Europe.

Intertek Group plc operates in global assurance and certification segments, emphasizing performance testing and risk mitigation solutions, supported by digital platforms, strong client relationships, and diversified service offerings across automotive supply chains.

Key Players

- Applus+

- Bureau Veritas

- DEKRA SE

- DNV GL

- Eurofins Scientific

- Intertek Group plc

- Lloyd Register Group Limited

- SGS SA

- TUV

- Rheinland

- UL LLC

Recent Developments

SGS SA announced in February 2026 the expansion of its electric vehicle battery testing services across Europe, addressing increasing demand for compliance with safety and performance standards. The initiative supports rapid electrification trends and regulatory requirements in automotive validation.

UL LLC stated in January 2026 the enhancement of its automotive cybersecurity certification programs, focusing on connected and software defined vehicles. This aligns with growing UNECE regulations on vehicle software updates and data protection compliance.

DNV GL revealed in March 2025 the development of digital assurance solutions for automotive supply chains, integrating risk management and compliance verification tools. The move strengthens lifecycle validation capabilities across mobility and transport ecosystems.

TUV Rheinland announced in April 2026 the expansion of autonomous vehicle testing facilities in Europe, focusing on advanced driver assistance systems and safety validation. This supports evolving regulatory frameworks for connected and automated mobility.

Lloyd Register Group Limited reported in November 2025 the launch of integrated compliance and inspection services for automotive manufacturers, emphasizing sustainability and quality assurance. The initiative aligns with increasing regulatory pressure on emission standards and production transparency.

Europe TIC Market for Automotive Industry Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing Services

- Inspection Services

- Certification Services

Sourcing Type Insight and Forecast 2026 - 2035

- In House

- Outsourced

Application Insight and Forecast 2026 - 2035

- Vehicle Inspection and Homologation

- Electric Vehicle Testing

- ADAS and Autonomous Systems Validation

- Emission and Environmental Testing

End Use Insight and Forecast 2026 - 2035

- Automotive Manufacturers

- Suppliers

- Aftermarket Service Providers

Europe TIC Market for Automotive Industry by Region

- Germany

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- U.K.

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- France

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Italy

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Spain

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Russia

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- Rest of Europe

- By Service Type

- By Sourcing Type

- By Application

- By End Use

Table of Contents for Europe TIC Market for Automotive Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Application

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing Services

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In House

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Vehicle Inspection and Homologation

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Electric Vehicle Testing

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. ADAS and Autonomous Systems Validation

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Emission and Environmental Testing

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Automotive Manufacturers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Suppliers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Aftermarket Service Providers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Application

6.4. By

End Use

7. U.K. Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Application

7.4. By

End Use

8. France Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Application

8.4. By

End Use

9. Italy Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Application

9.4. By

End Use

10. Spain Market Estimate and Forecast

10.1. By

Service Type

10.2. By

Sourcing Type

10.3. By

Application

10.4. By

End Use

11. Russia Market Estimate and Forecast

11.1. By

Service Type

11.2. By

Sourcing Type

11.3. By

Application

11.4. By

End Use

12. Rest of Europe Market Estimate and Forecast

12.1. By

Service Type

12.2. By

Sourcing Type

12.3. By

Application

12.4. By

End Use

13. Company Profiles

13.1.

Applus+

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Bureau Veritas

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

DEKRA SE

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

DNV GL

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Eurofins Scientific

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Intertek Group plc

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Lloyd Register Group Limited

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

SGS SA

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

TUV Rheinland

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe TIC Market for Automotive Industry