India Electric Three Wheeler Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Product (Passenger carriers, Cargo carriers, Others), by Type (Battery operated, Hybrid electric), by Motor Power (Below 1000 W, 1000 W to 1500 W, Above 1500 W), by Driving Range (Below 50 km, 50 km to 100 km, Above 100 km), by Region (North India, East India, West and Central India, South India)

| Status : Published | Published On : Jun, 2026 | Report Code : VRAT9675 | Industry : Automotive & Transportation | Available Format :

|

Page : 124 |

India Electric Three Wheeler Market Overview

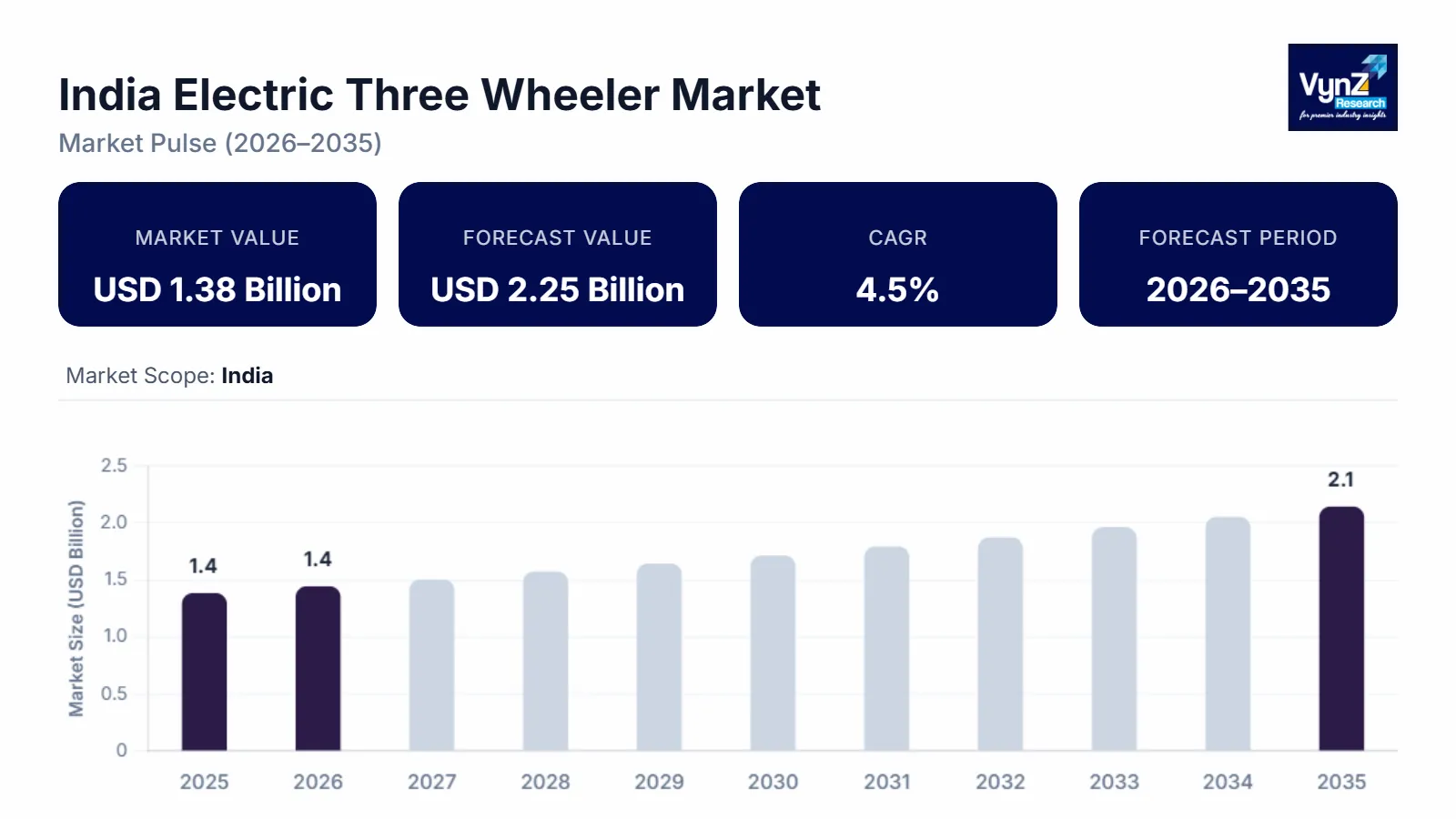

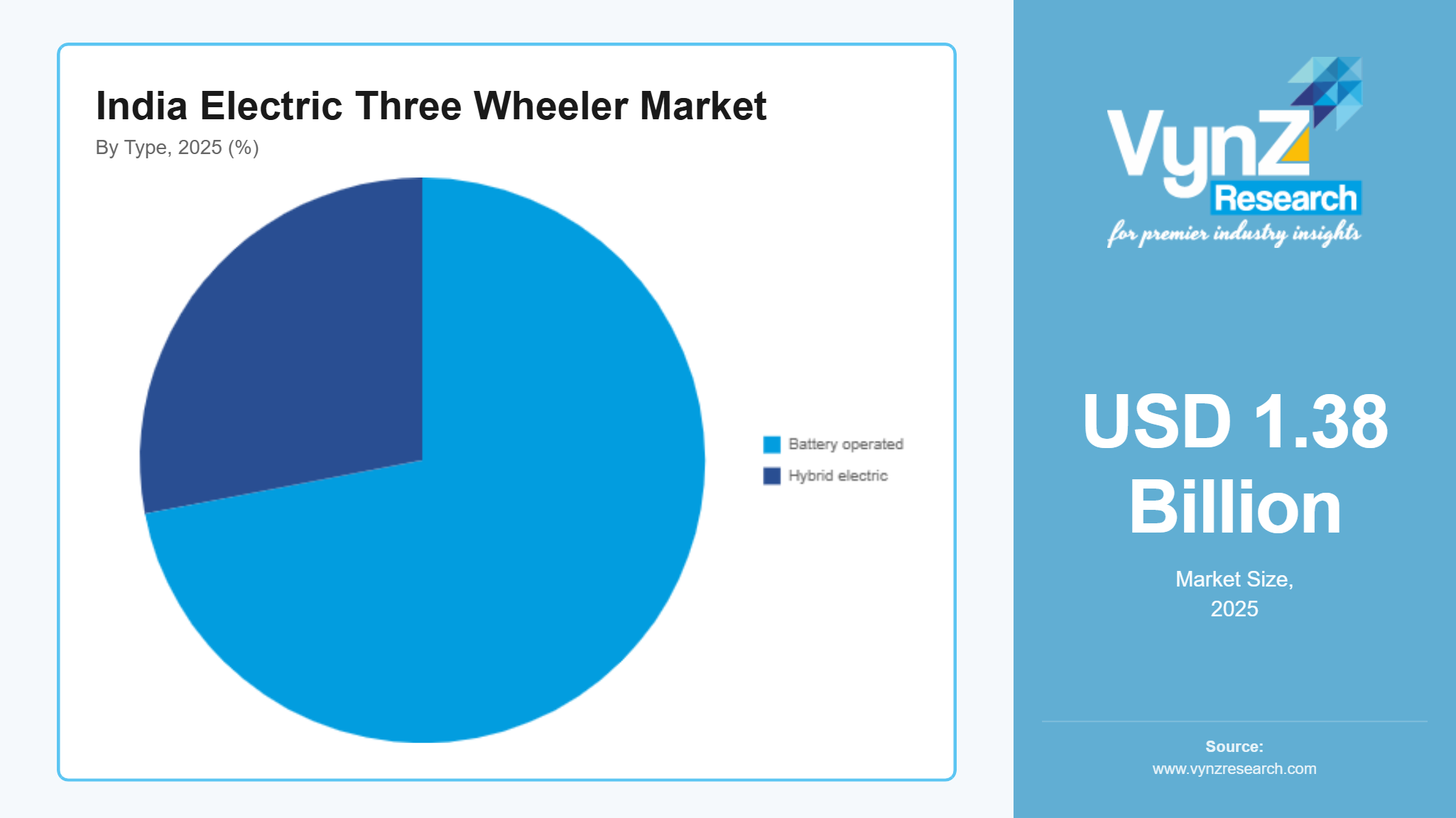

The India electric three-wheeler market size was estimated at about USD 1.38 billion in 2025 and is expected to reach around USD 1.46 billion in 2026 rising up to roughly USD 2.25 billion in 2035, growing at approximately 4.5% CAGR from 2026 to 2035.

Research Highlights

- Passenger carriers led with 58% share in 2025 due to urban mobility demand.

- Cargo carriers projected fastest growth at 5.2% CAGR driven by e commerce logistics.

- Battery operated segment dominated with 72% share supported by strong policy incentives.

- 1000 W to 1500 W motor segment held 49% share due to balanced performance.

- North India led with 28% share driven by dense urban transport demand.

The market expansion is supported by the growing need in the urban region for short distance travel which pushes the demand for electric commercial vehicles due to better batteries and higher acceptance of electric three wheelers as a greener way to travel short distances or move goods. The government is also helping with policies like the FAME India Scheme and the National Electric Mobility Mission Plan and support from the Ministry of Heavy Industries and NITI Aayog are also boosting the market especially in cities like Delhi NCR, Mumbai and Bengaluru where the electric three wheelers are a last mile remedy.

India Electric Three Wheeler Market Dynamics

Market Trends

The industry is moving to better electrification patterns and infrastructure and large number of people are buying these vehicles for their fleets. A major part of this change is the move towards using lithium-ion battery powered three wheelers because they are more efficient can go further and cost less to run. The ability to swap batteries and connect vehicles to platforms is helping to make urban fleets work better. Companies are starting to make products that focus on battery systems fleets that use telematics and ways to save energy, which is changing the way companies compete with each other in the market.

Growth Drivers

The market is growing because people want ways to get around easily and quickly especially for short trips and cities are investing in transportation and setting up charging stations which is helping the market grow even faster. As fuel prices go up and rules about emissions get stricter more people are turning to electric three wheelers and when fleet operators and individual drivers start to think about saving money and following the rules electric three wheelers are likely to stay popular. Government programs like the FAME India Scheme, National Electric Mobility Mission Plan and support from the Ministry of Road Transport and Highways are helping to make electric vehicles more popular.

Market Restraints / Challenges

There are some problems with the market like the cost of buying an electric three-wheeler and the fact that it can be hard for small fleet operators to get financing which makes it hard to sell these vehicles in areas where people are sensitive about price. There are not enough charging stations which is a problem for both the companies that make the vehicles and the people who use them as they have to depend on imported batteries. Problems with the supply chain is also escalating costs and making it hard to grow the market.

Market Opportunities

The market offers opportunities for growth especially in shared mobility sector making it more electric oriented to meet the growing demand of people living in cities and their need for an efficient and quick last mile delivery service. Companies that can offer electric three wheelers that are designed for fleets are likely to get new business from companies that deliver packages and offer ride hailing services. Another big opportunity is in creating systems that allow batteries to be swapped easily and in managing fleets and higher investment in digital mobility infrastructure that creates chances to make efficient systems and offer new ways to make money that can be repeated over time.

India Electric Three Wheeler Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.38 Billion |

|

Revenue Forecast in 2035 |

USD 2.25 Billion |

|

Growth Rate |

4.5% |

|

Segments Covered in the Report |

By Product, By Type, By Motor Power, By Driving Range |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North India, East India, West and Central India, South India |

|

Key Companies |

Atul Auto Ltd, Bajaj Auto Ltd, Clean Motion India, Hero Electric Vehicles Pvt. Ltd., Kinetic Green Energy and Power Solutions Ltd., Lohia Auto Industries, Mahindra Last Mile Mobility Limited, Omega Seiki Mobility Pvt Ltd, Piaggio Vehicles Pvt Ltd, Saera Electric Auto Limited, Terra Motors Corporatio |

|

Customization |

Available upon request |

India Electric Three Wheeler Market Segmentation

By Product

Passenger carriers dominated the market in 2025 with about 58% of the total revenue because many people use shared mobility and last mile public transport, cities are very crowded and people use these services a lot and the government programs like the FAME India Scheme help make passenger mobility better.

Cargo carriers are expected to grow fast with a growth rate of 5.2% from 2026 to 2035 mainly due to better ecommerce logistics and hyperlocal delivery services and many small fleet operators want to use cargo carriers because they are cost efficient.

By Type

Battery operated three wheelers lead the market in 2025 with about 72% of the share backed by their energy efficient nature, lower cost to run and higher acceptance by people and the government due to less pollution. The National Electric Mobility Mission Plan and state EV policies are helping to make these vehicles more popular.

Hybrid electric three wheelers are anticipated to grow at a rate of 3.8% from 2026 to 2035 s they are useful in places where it is difficult to charge batteries.

By Motor Power

In 2025 the 1000 W to 1500 W segment was the biggest making up about 49% of the revenue supported by its greater mobility, energy efficiency and ability to carry a lot of weight.

The above 1500 W segment is going to grow fastest at a rate of 5.6% from 2026 to 2035 because it is good for freight transport and city logistics.

By Driving Range

The 50 km to 100 km segment was the biggest in 2025 making up 54% of the market since it is good for city commuting, easy to plan routes and the battery costs are not too high.

The above 100 km segment will grow at a fast pace of 6.1% from 2026 to 2035 due to its suitability for intercity logistics giving fleet operators more flexibility, better battery technology and compatibility with national clean mobility programs.

Regional Insights

North India

North India held nearly 28% of the market in 2025 because many people living in cities use shared rides and last mile passenger transport and the government is helping to make electric three wheelers more popular with programs like the FAME India Scheme.

East India

East India contributed nearly 21% of the market in 2025 mainly due to higher preference for low-cost mobility, faster passenger transport and support of the FAME India Scheme and state EV policies.

West and Central India

West and Central India accounted for 27% of the market in 2025 backed by a strong industrial base, logistics network and higher use and support from the government providing incentives and favorable policies for electric vehicles.

South India

South India held 24% of the market in 2025 because it has a strong urban transit network and many people use electric vehicles and the government offers subsidies, tax reductions and charging infrastructure programs to make electric vehicles more popular.

Competitive Landscape / Company Insights

The market is moderately competitive with established manufacturers and new EV focused players competing on price, innovation and distribution network. They are investing in battery technology, manufacturing and digital fleet management to stay ahead. The Government is also helping to make the industry more competitive with programs like the FAME India Scheme and many companies are focusing on cost optimization and scalable charging ecosystems.

Mini Profiles

Atul Auto Ltd focuses on electric and diesel three-wheeler manufacturing, supported by strong domestic distribution network and cost-efficient production capabilities enabling stable presence across Indian commercial mobility segment.

Bajaj Auto Ltd operates in mass market mobility segment, emphasizing high performance electric three-wheeler platforms, strong brand recognition, and wide dealership network across urban and semi urban regions in India.

Clean Motion India leverages lightweight electric vehicle design, sustainable engineering solutions, and innovation driven development to expand its presence in clean urban mobility and last mile transportation solutions.

Hero Electric Vehicles Pvt. Ltd. focuses on electric two-wheeler and three-wheeler solutions, supported by extensive retail network, strong brand trust, and large-scale urban adoption across India.

Mahindra Last Mile Mobility Limited operates in commercial electric mobility segment, emphasizing robust vehicle engineering, fleet-oriented solutions, and strong manufacturing capabilities supporting large scale deployment across logistics and passenger transport applications.

Key Players

- Atul Auto Ltd

- Bajaj Auto Ltd

- Clean Motion India

- Hero Electric Vehicles Pvt. Ltd.

- Kinetic Green Energy and Power Solutions Ltd.

- Lohia Auto Industries

- Mahindra Last Mile Mobility Limited

- Omega Seiki Mobility Pvt Ltd

- Piaggio Vehicles Pvt Ltd

- Saera Electric Auto Limited

- Terra Motors Corporation

Recent Developments

In January 2026, Piaggio Vehicles Pvt Ltd expanded its electric three-wheeler production capacity in India to meet rising urban fleet demand. The company also strengthened its focus on last mile logistics solutions through upgraded battery efficiency platforms.

In November 2025, Omega Seiki Mobility Pvt Ltd launched an upgraded electric cargo three-wheeler designed for higher payload efficiency and extended driving range. The development aligns with growing demand from e commerce and urban delivery operators.

In October 2025, Kinetic Green Energy and Power Solutions Ltd. introduced new fleet focused electric three-wheeler variants targeting shared mobility operators. The company also expanded its charging ecosystem partnerships to improve operational uptime.

In August 2025, Saera Electric Auto Limited enhanced its production line capabilities to support higher volume electric three-wheeler manufacturing. The initiative aims to strengthen its position in cost sensitive passenger mobility markets across India.

In June 2025, Lohia Auto Industries announced expansion of its electric three-wheeler distribution network across Tier 2 and Tier 3 cities. The move is aimed at improving accessibility and accelerating adoption in semi urban transport corridors.

India Electric Three Wheeler Market Coverage

Product Insight and Forecast 2026 - 2035

- Passenger carriers

- Cargo carriers

- Others

Type Insight and Forecast 2026 - 2035

- Battery operated

- Hybrid electric

Motor Power Insight and Forecast 2026 - 2035

- Below 1000 W

- 1000 W to 1500 W

- Above 1500 W

Driving Range Insight and Forecast 2026 - 2035

- Below 50 km

- 50 km to 100 km

- Above 100 km

Region Insight and Forecast 2026 - 2035

- North India

- East India

- West and Central India

- South India

India Electric Three Wheeler Market by Region

- North India

- By Product

- By Type

- By Motor Power

- By Driving Range

- By Region

- East India

- By Product

- By Type

- By Motor Power

- By Driving Range

- By Region

- West and Central India

- By Product

- By Type

- By Motor Power

- By Driving Range

- By Region

- South India

- By Product

- By Type

- By Motor Power

- By Driving Range

- By Region

Table of Contents for India Electric Three Wheeler Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product

1.2.2. By

Type

1.2.3. By

Motor Power

1.2.4. By

Driving Range

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product

5.1.1. Passenger carriers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Cargo carriers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Others

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Type

5.2.1. Battery operated

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Hybrid electric

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Motor Power

5.3.1. Below 1000 W

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. 1000 W to 1500 W

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Above 1500 W

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Driving Range

5.4.1. Below 50 km

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. 50 km to 100 km

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Above 100 km

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. North India

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. East India

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. West and Central India

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. South India

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North India Market Estimate and Forecast

6.1. By

Product

6.2. By

Type

6.3. By

Motor Power

6.4. By

Driving Range

6.5. By

Region

7. East India Market Estimate and Forecast

7.1. By

Product

7.2. By

Type

7.3. By

Motor Power

7.4. By

Driving Range

7.5. By

Region

8. West and Central India Market Estimate and Forecast

8.1. By

Product

8.2. By

Type

8.3. By

Motor Power

8.4. By

Driving Range

8.5. By

Region

9. South India Market Estimate and Forecast

9.1. By

Product

9.2. By

Type

9.3. By

Motor Power

9.4. By

Driving Range

9.5. By

Region

10. Company Profiles

10.1.

Atul Auto Ltd

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bajaj Auto Ltd

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Clean Motion India

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Hero Electric Vehicles Pvt. Ltd.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Kinetic Green Energy and Power Solutions Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Lohia Auto Industries

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Mahindra Last Mile Mobility Limited

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Omega Seiki Mobility Pvt Ltd

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Piaggio Vehicles Pvt Ltd

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Saera Electric Auto Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Terra Motors Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Electric Three Wheeler Market