Global Tyre Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger cars, Two wheelers, Light commercial vehicles, Heavy commercial vehicles, Others), by Tyre Type (Radial tyres, Bias tyres), by Sales Channel (OEM, Aftermarket), by Price (Economy, Mid-range, Premium), by End User (Individual consumers, Commercial fleet, Industrial users, Institutional users)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9670 | Industry : Automotive & Transportation | Available Format :

|

Page : 171 |

Global Tyre Market Overview

The tyre market which was valued at approximately USD 147.4 billion in 2025 and is estimated to rise further up to almost USD 150.8 billion in 2026, is projected to reach around USD 205.0 billion in 2035, expanding at a CAGR of about 3.6% during the forecast period from 2026 to 2035.

The market expands because more vehicles get produced and the number of vehicles on the road increases needing people to replace tyres while they choose better tyres that provide both high performance and better fuel efficiency. Road safety measures get support from public health concerns about traffic accidents which the world organizations use to assess road traffic injuries while emissions reduction and mobility efficiency regulations enable long term growth in North America, Europe and Asia Pacific regions.

The tyre market across commercial and passenger vehicle segments grows stronger because of ongoing investments in transport infrastructure projects and increased electric vehicle adoption and smart tyre technology progress. Tyre quality standards improvement and sustainable materials development through lifecycle efficiency innovation programs, which the government backs, as well as programs that modernize mobility systems for safety compliance, create demand in both OEM and aftermarket markets.

Global Tyre Market Dynamics

Market Trends

The tyre industry is undergoing a fundamental transformation as it shifts toward advanced mobility-centered tyre design because of changing vehicle engineering standards and new environmental rules established by worldwide transport safety and emission reduction treaties. The United Nations road safety action frameworks and World Health Organization road safety reports together demonstrate that vehicle safety performance must improve to satisfy demand for high durability tyres that have low rolling resistance and fuel-efficient performance. The product development process has gained extra momentum from this situation because manufacturers now focus their research on developing sustainable rubber compounds and silica reinforced materials and noise reducing tread designs which will meet regulatory standards while providing customers with efficient results.

Growth Drivers

The tyre market experiences growth because of two factors which include the increasing number of vehicles worldwide and the higher levels of vehicle production which results in ongoing demand from both replacement and original equipment manufacturers for passenger cars and commercial vehicles. The expansion of transport infrastructure, logistics networks and urban mobility systems has caused tyre consumption to grow faster in areas with heavy traffic and high freight volumes. The government-backed mobility development programs together with road infrastructure upgrades in emerging and developed economies will create lasting demand stability between road safety frameworks established by public health agencies and the requirement for better tyre performance.

Market Restraints / Challenges

The tyre market struggles to meet strong demand because raw material price swings create operational challenges that particularly affect natural rubber and synthetic rubber derivative materials which result in price instability and decreased manufacturing profitability. The supply chain system handles cost unpredictability because it depends on main exporting regions while crude oil input costs experience price changes which affects profitability for both major manufacturers and mid-sized suppliers. Price sensitive markets experience these constraints at their highest intensity because end users in these markets choose affordable options while technical advancements remain out of their budget which results in lower adoption rates for premium tyre technologies.

Market Opportunities

Sustainable and eco-friendly tyre development creates major market opportunities because regulations now prioritize carbon neutrality and circular economy practices as essential market requirements. Government sustainability programs and environmental protection standards create market opportunities for innovation because they enable companies to process recycled materials and biobased rubber compounds and retread technologies. The tyre industry will experience growth because companies who develop high performance tyres which meet environmental standards will attract original equipment manufacturers and fleet operators who need cost effective solutions that comply with regulations.

Global Global Tyre Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 147.4 Billion |

|

Revenue Forecast in 2035 |

USD 205 Billion |

|

Growth Rate |

3.6% |

|

Segments Covered in the Report |

By Vehicle Type, By Tyre Type, By Sales Channel, By Price, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Asia Pacific, North America, Europe, Latin America, Rest of the World |

|

Key Companies |

Bridgestone Corporation, Continental AG, Michelin Group, The Goodyear Tire and Rubber Company, Hankook Tire & Technology Co., Ltd., Pirelli Tyre S.p.A, Yokohama Tire Corporation, Sumitomo Corporation, Toyo Engineering Corporation, Kumho Tyre (Australia) Pty Ltd. |

|

Customization |

Available upon request |

Global Tyre Market Segmentation

By Vehicle Type

The passenger car segment accounted for about 38% of the market share in 2025 because of high vehicle ownership levels, frequent vehicle replacement cycles and personal mobility remained the major transportation mode in urban areas throughout the world. The segment will expand at a rate of 3.4% during the forecast period because of ongoing growth in passenger vehicle fleets and increased demand for tyre replacement in the aftermarket sector. Regulatory bodies establish road safety standards and efficiency standards which constitute major drivers of growth because these standards receive backing from international transport safety organizations and national programs for improving mobility.

The heavy commercial vehicle segment will experience the highest growth rate of 4.1% because logistics expansion and freight corridor development and rising industrial trade movement drive this growth. The growing highway infrastructure investment by government and cross border transportation network investment by government creates demand for tyre solutions which provide high durability and extended product lifespan.

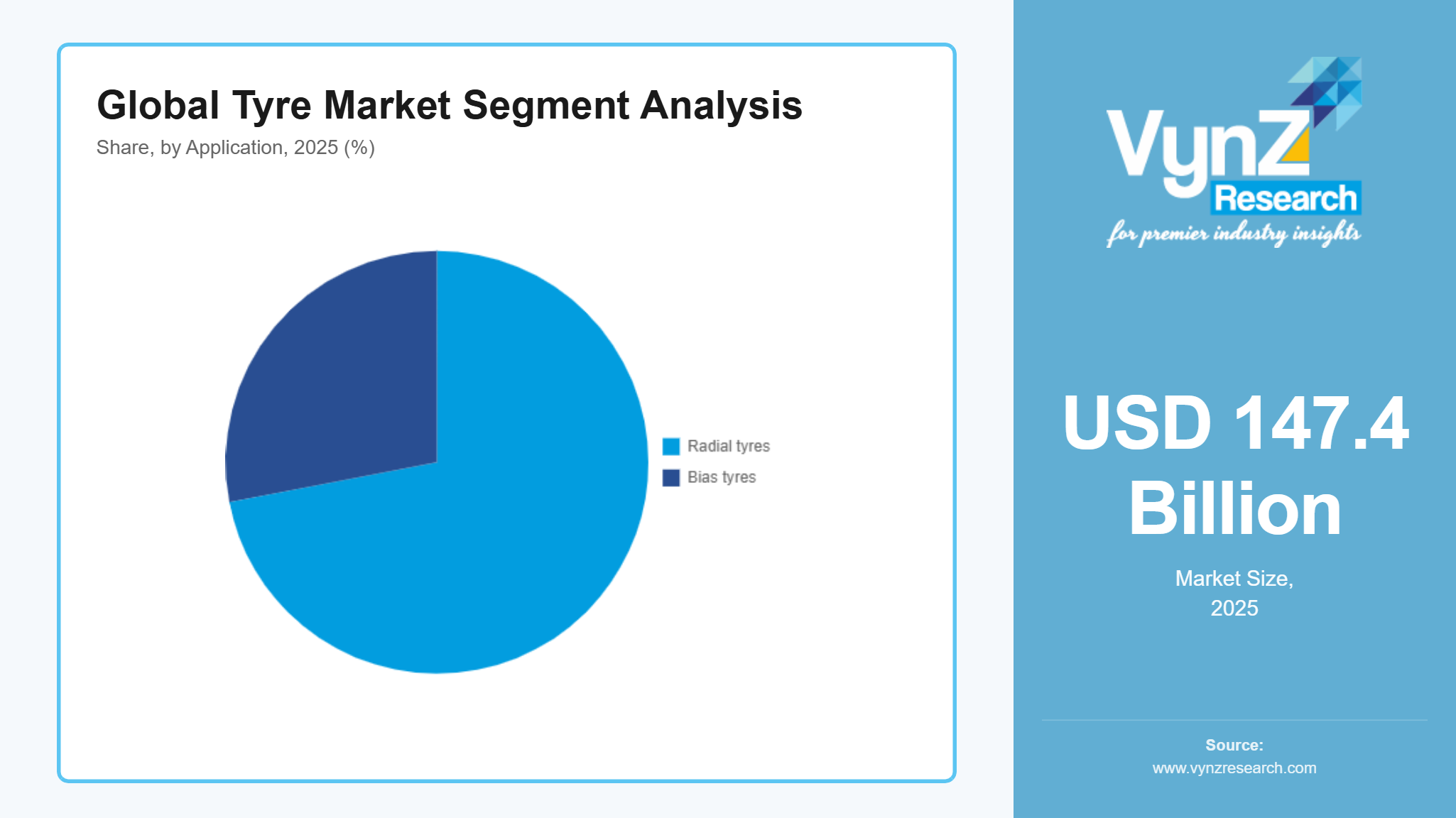

By Tyre Type

The radial tyre segment owned the largest market share with 72% in 2025 because this tyre type offers better fuel efficiency, longer durability and higher heat resistance and this tyre type received widespread use in both passenger and commercial vehicles. The segment will expand at a rate of 3.6% during the forecast period because tread design, material engineering and performance optimization achieve ongoing technological progress. Regulatory agencies enforce fuel economy and emission reduction standards which help increase the market presence of radial tyres in both OEM and replacement tyre segments.

The bias tyre segment will expand at a rate of 2.8% because agricultural and construction and off highway vehicles create demand for this tyre type. The passenger mobility segment shows limited adoption of this technology because its structural strength and cost efficiency make it suitable for use in harsh operating conditions where customers prioritize durability and low initial cost.

By Sales Channel

The aftermarket segment held 61% of the market share in 2025 because customers frequently require tyre replacements and customers consume tyres based on their wear patterns. The segment will grow at a rate of 3.7% because increased vehicle usage and global vehicle fleets reaching their aging point and consumers becoming more aware of tyre maintenance needs and safety compliance requirements. Government road safety programs and vehicle inspection regulations create a system which drives replacement cycles throughout major automotive markets.

The OEM segment will expand at a rate of 3.2% because automotive production remains stable while manufacturers introduce advanced tyre technologies in their new vehicle designs. The tyre industry benefits from automotive manufacturers and tyre producers working together to establish product standards while their collaboration improves supply chain efficiency and maintains steady demand for factory fitted tyre solutions.

By Price

The mid-range segment held 46% of the market share in 2025 because cost conscious consumers showed strong demand for tyres which offered balanced performance and durability and price affordability. The segment will grow at a rate of 3.5% because middle income populations and vehicle ownership and demand for value-oriented mobility solutions increase in emerging markets.

The premium tyre segment will grow at the fastest rate of 4.2% because demand for high performance vehicles, luxury mobility solutions, superior safety features and enhanced driving performance capabilities increase. This segment provides better profit margins because it has strong brand positioning and the company develops new material technologies and tread engineering solutions.

By End User

The individual consumer segment held 44% of the market share in 2025 because most people own private vehicles and they need to replace their vehicles for safety and performance reasons. The segment will grow at a rate of 3.3% because rising disposable incomes and urbanization and people needing personal mobility solutions create demand in global markets.

The commercial fleet segment will grow at 4.0% because logistics networks, e-commerce distribution systems and organized transportation services keep expanding. The commercial sector requires high durability tyre solutions which provide performance optimization because they need to maintain fleet efficiency and predictive maintenance and cost optimization.

Regional Insights

Asia Pacific

Asia Pacific region will contribute 34% of the tyre market in 2025 because automotive production increases, vehicle fleet growth and urban transportation systems expand throughout major markets which include China, India and Japan. The manufacturing hubs of Shanghai, Tokyo and Delhi deliver tyre demand to OEMs and aftermarket customers because of increased freight traffic which drives up commercial vehicle tyre needs. National highway creation policies and mobility safety standards together with government-sponsored transport modernization projects and road infrastructure development initiatives increase the market need for long-lasting and fuel-efficient tyre products. The region will experience continuous market growth because of two factors which are the increased use of electric vehicles and the development of logistics networks.

North America

The tyre market in North America will reach 24% by 2025 because of high vehicle ownership and strong demand for replacements which occur throughout the automotive infrastructure in the United States, Canada and Mexico. The urban and industrial centers of New York, Los Angeles, Chicago and Toronto create ongoing demand for tyres which serve both passenger vehicles and commercial vehicles. The existing transportation safety standards and environmental efficiency policies encourage businesses to choose low rolling resistance tyres which deliver high performance capabilities. Government programs which enhance road safety and develop intelligent transport systems create market expansion opportunities while aftermarket distribution networks deliver product distribution and replacement services to customers.

Europe

Europe will hold 17% of the tyre market in 2025 because its automotive manufacturing sectors have reached maturity and its safety regulations have become extremely strict and its automotive production systems require environmentally sustainable operations. The main vehicle markets in Germany, the United Kingdom, France and Italy together with their high vehicle count and premium tyre market uptake drive regional tyre demand. The existing European transportation and environmental compliance frameworks create regulatory authority which drives tyre manufacturers to adopt energy-efficient and low-emission tyre production methods. The market requires increasing focus on circular economy policies and sustainable mobility initiatives which lead to higher demand from OEM channels and high-performance vehicle segments.

Latin America

Latin America holds 10% of the tyre market for 2025 because of increasing automotive aftermarket needs, rising commercial transportation activity and gradual infrastructure development across Brazil, Argentina and Mexico. The demand for replacement tyres continues to grow in passenger and light commercial vehicle markets because of expanded logistics networks and urban mobility system development. The government-led transportation improvement initiatives together with road expansion programs establish better regional transport connections which increase vehicle usage rates. The increase in vehicle maintenance knowledge and safety standard understanding leads to continuous tyre replacement activities in major urban areas.

Rest of the World

The tyre market in Middle East and Africa will reach 15% for 2025 because of infrastructure development and expanding logistics corridors and increasing vehicle imports which take place in GCC countries and South Africa. The principal driving forces for economic growth come from construction activity, industrial expansion and commercial transportation needs which major hubs like Dubai, Riyadh and Johannesburg experience. The smart city development, highway expansion and economic diversification programs which the government funds establish conditions for increased demand in transportation throughout the long term.

Competitive Landscape / Company Insights

The tyre market is moderately to highly competitive, with the presence of global and regional manufacturers focusing on product innovation, cost optimization, and geographic expansion across OEM and aftermarket channels. Companies are increasingly investing in research and development, advanced material engineering, and smart mobility integration to strengthen product performance, durability, and sustainability compliance. Regulatory emphasis on road safety standards, environmental efficiency guidelines issued by transportation and public safety authorities is further influencing competitive strategies. Expansion of manufacturing capacity, strategic partnerships with automotive producers, and digital distribution capabilities are strengthening market positioning across major automotive regions globally.

Mini Profiles

Bridgestone Corporation focuses on premium and mass market tire solutions, supported by strong global distribution network and advanced mobility technologies, enabling consistent performance across passenger, commercial, and industrial vehicle applications.

Continental AG operates in premium tire and automotive technology segments, emphasizing high performance engineering, safety innovation, and integrated mobility systems that strengthen its position across OEM and replacement tire markets globally.

The Goodyear Tire and Rubber Company leverages strong brand recognition and extensive retail distribution networks to expand market presence, focusing on innovative tire designs, durability enhancement, and performance driven mobility solutions.

Hankook Tire & Technology Co., Ltd. operates in mid range and premium segments, emphasizing advanced manufacturing capabilities, design innovation, and strategic global partnerships to strengthen its competitive positioning across key automotive regions.

Michelin Group focuses on premium tire solutions and sustainable mobility offerings, supported by strong research and development capabilities and global brand leadership, enabling high efficiency and performance across diverse transportation segments.

Key Players

- Bridgestone Corporation

- Continental AG

- Hankook Tire & Technology Co., Ltd.

- Kumho Tyre (Australia) Pty Ltd.

- Michelin Group

- Pirelli Tyre S.p.A

- Sumitomo Corporation

- The Goodyear Tire and Rubber Company

- Toyo Engineering Corporation

- Yokohama Tire Corporation

Recent Developments

In January 2026, Michelin Group advanced its sustainability strategy in January 2026 by expanding production of low rolling resistance and eco-efficient tire lines across Europe and Asia manufacturing hubs. The company continues to focus on reducing lifecycle emissions while aligning with global transportation decarbonization targets supported by international road safety and environmental frameworks.

In January 2026, Bridgestone Corporation announced in January 2026 a strategic restructuring of its Asian supply chain network to improve cost efficiency and manufacturing agility. The initiative aligns with broader mobility safety and infrastructure modernization programs supported by government transport authorities, strengthening its OEM and aftermarket positioning.

In May 2025, Continental AG expanded its next generation intelligent tire technology portfolio in May 2025, focusing on sensor enabled solutions for connected vehicles. This development supports increasing regulatory emphasis on road safety and digital mobility systems across European automotive frameworks.

In April 2025, Goodyear introduced upgraded all season and EV optimized tire solutions in April 2025, targeting improved durability and energy efficiency performance. The development aligns with rising government backed EV adoption policies and sustainable mobility initiatives across North America and Europe.

In January 2025, Hankook Tire & Technology launched its new Optimo sub brand in Europe in January 2025 to strengthen its mid-range passenger tire segment presence. The expansion supports growing demand for cost efficient yet performance-oriented tire solutions across emerging mobility markets and OEM partnerships.

Global Global Tyre Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger cars

- Two wheelers

- Light commercial vehicles

- Heavy commercial vehicles

- Others

Tyre Type Insight and Forecast 2026 - 2035

- Radial tyres

- Bias tyres

Sales Channel Insight and Forecast 2026 - 2035

- OEM

- Aftermarket

Price Insight and Forecast 2026 - 2035

- Economy

- Mid-range

- Premium

End User Insight and Forecast 2026 - 2035

- Individual consumers

- Commercial fleet

- Industrial users

- Institutional users

Global Global Tyre Market by Region

- North America

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Global Tyre Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Tyre Type

1.2.3. By

Sales Channel

1.2.4. By

Price

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger cars

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Two wheelers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Light commercial vehicles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Heavy commercial vehicles

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Others

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Tyre Type

5.2.1. Radial tyres

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bias tyres

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Sales Channel

5.3.1. OEM

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Aftermarket

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Price

5.4.1. Economy

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Mid-range

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Premium

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Individual consumers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial fleet

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial users

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Institutional users

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Tyre Type

6.3. By

Sales Channel

6.4. By

Price

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Tyre Type

7.3. By

Sales Channel

7.4. By

Price

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Tyre Type

8.3. By

Sales Channel

8.4. By

Price

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Tyre Type

9.3. By

Sales Channel

9.4. By

Price

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Bridgestone Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Continental AG

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Hankook Tire & Technology Co., Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Kumho Tyre (Australia) Pty Ltd.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Michelin Group

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Pirelli Tyre S.p.A

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Sumitomo Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

The Goodyear Tire and Rubber Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Toyo Engineering Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Yokohama Tire Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Global Tyre Market