India Automotive Accessories Aftermarket Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Interior Accessories, Exterior Accessories, Electronic Accessories, Performance Accessories, Car Care Accessories), by Vehicle Type (Passenger Cars, Two-Wheelers, Light Commercial Vehicles (LCVs), Heavy Commercial Vehicles (HCVs)), by Sales Channel (Online Retail, Offline Retail), by Distribution Channel (OEM Authorized Dealers, Independent Aftermarket Retailers, E-Commerce Platforms)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9664 | Industry : Automotive & Transportation | Available Format :

|

Page : 141 |

India Automotive Accessories Aftermarket Overview

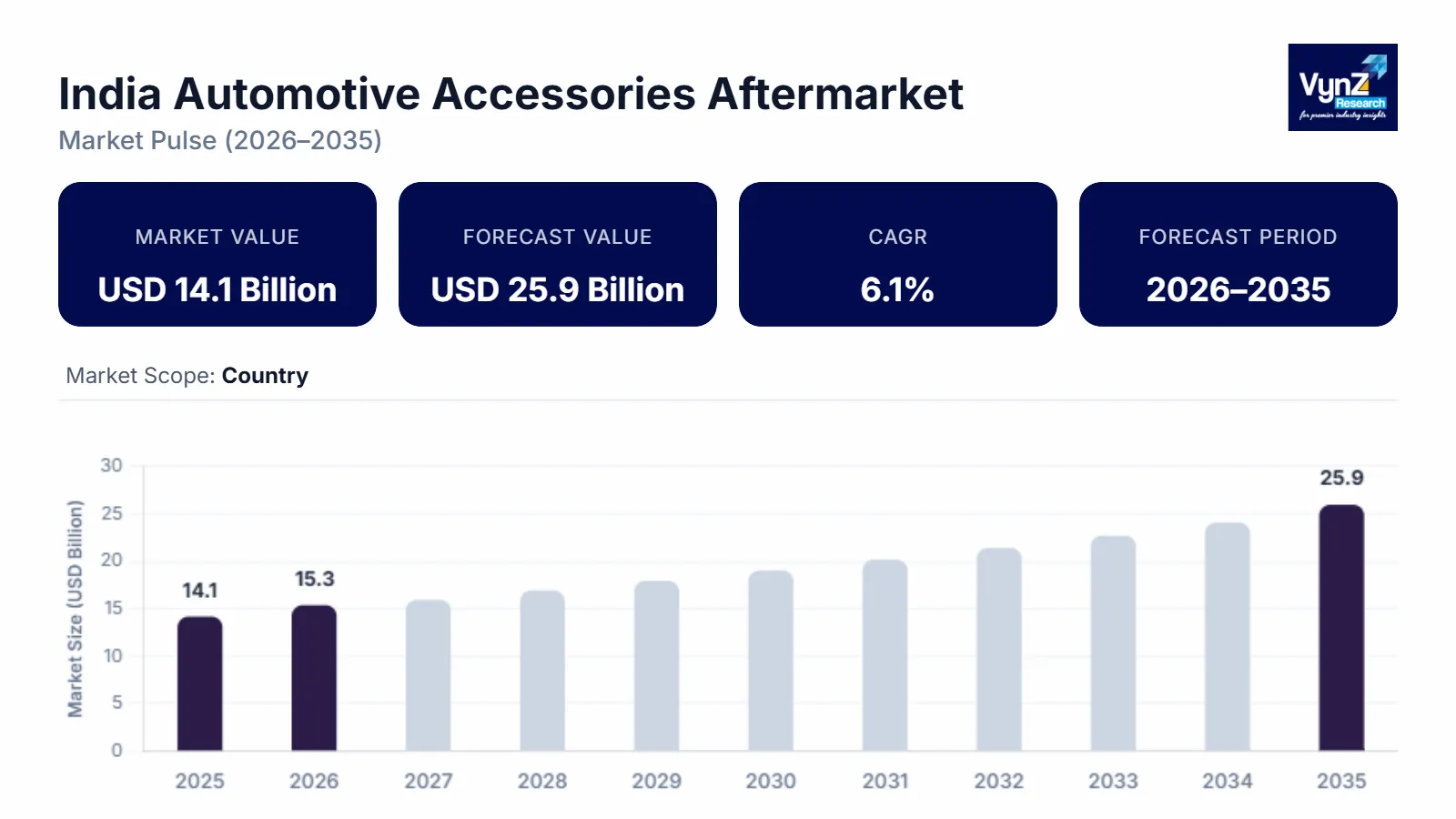

The India automotive accessories aftermarket which was valued at approximately USD 14.1 billion in 2025 and is estimated to reach around USD 15.3 billion in 2026, is projected to reach close to USD 25.9 billion by 2035, expanding at a CAGR of about 6.1% during the forecast period from 2026 to 2035.

The market is primarily driven by the growing vehicle population and rising consumer interest in vehicle customization and comfort. As passenger cars, two-wheelers, and commercial vehicles continue to increase across the country, vehicle owners are increasingly purchasing accessories such as infotainment systems, seat covers, lighting upgrades, alloy wheels, and protective components to improve vehicle aesthetics and functionality. Rising disposable incomes and the expanding middle-class population are also encouraging consumers to spend more on aftermarket upgrades.

In addition, the strong growth of the used vehicle market and longer vehicle ownership cycles increase demand for replacement and upgrade accessories. The rapid expansion of e-commerce platforms and organized automotive accessory retailers has improved product accessibility and price transparency, further supporting market growth. Technological advancements such as smart infotainment systems, parking sensors, and dash cameras are also gaining popularity among consumers. Furthermore, the presence of domestic accessory manufacturers and a strong automotive ecosystem in India ensures wide product availability and competitive pricing.

India Automotive Accessories Aftermarket Dynamics

Market Trends

Rising demand for vehicle personalization and customization is a major trend in the India automotive accessories aftermarket as consumers increasingly seek to modify their vehicles to reflect personal style, comfort, and functionality. Vehicle owners are investing in accessories such as custom seat covers, alloy wheels, ambient lighting, infotainment systems, body kits, and decorative exterior elements to enhance both the appearance and performance of their vehicles. The growing middle-class population and increasing disposable incomes have encouraged consumers to spend more on non-essential automotive upgrades after purchasing vehicles. The Government of India introduced the Production Linked Incentive (PLI) scheme for the automobile and auto-component sector with a budget of about ₹25,938 crore to strengthen domestic manufacturing and encourage investment in advanced automotive technologies and components. Additionally, younger buyers and car enthusiasts are particularly interested in styling modifications that differentiate their vehicles from standard factory models. The popularity of SUVs and lifestyle vehicles has also boosted demand for customized accessories such as roof racks, spoilers, and premium interior upgrades. Social media and automotive influencer culture further encourage personalization trends by showcasing modified vehicles and new accessory products.

Growth Drivers

Increasing vehicle ownership across India is a major growth driver for the automotive accessories’ aftermarket. As the number of passenger cars, two-wheelers, and commercial vehicles continues to rise, the demand for various aftermarket accessories also increases. Vehicle owners often purchase accessories such as seat covers, floor mats, infotainment systems, lighting upgrades, and protective components to improve comfort, functionality, and appearance. The PM E-DRIVE scheme, launched with an outlay of about ₹10,900 crore, aims to accelerate the adoption of electric vehicles such as electric two-wheelers, three-wheelers, trucks, buses, and ambulances. Rapid urbanization, improving road infrastructure, and easier access to vehicle financing have made vehicle ownership more accessible to a larger population. In addition, the growing middle-class population and rising income levels are encouraging more consumers to buy personal vehicles. As the overall vehicle parc expands, the potential customer base for automotive accessories grows significantly. Both new and existing vehicle owners contribute to aftermarket demand by upgrading or replacing accessories over time. This expanding vehicle base continues to support steady growth in the India automotive accessories aftermarket.

Market Restraints / Challenges

The presence of low-quality and counterfeit automotive accessories is a significant challenge for the India automotive accessories aftermarket. A large portion of the market is dominated by unorganized manufacturers and informal retail channels that offer inexpensive but substandard products. These accessories often fail to meet safety, durability, and performance standards, which can lead to frequent replacements and reduced customer trust. Counterfeit products that imitate well-known brands also create unfair competition for legitimate manufacturers and reduce brand credibility in the market. Many consumers are attracted to these low-cost alternatives due to price sensitivity, especially in price-conscious segments. However, the use of poor-quality accessories can damage vehicle components or affect vehicle safety and reliability. In addition, the widespread availability of such products makes it difficult for organized and branded accessory suppliers to maintain consistent market share. This issue continues to limit the overall growth potential and quality standards of the India automotive accessories aftermarket.

Market Opportunities

The rapid expansion of e-commerce platforms presents a significant opportunity for the India automotive accessories aftermarket. Online marketplaces allow consumers to easily browse, compare, and purchase a wide variety of automotive accessories such as infotainment systems, lighting products, seat covers, and mobile mounts. E-commerce platforms provide access to a broader product range and competitive pricing, which attracts price-sensitive and tech-savvy consumers. The Indian government allows 100% foreign direct investment (FDI) under the automatic route in the marketplace model of e-commerce platforms. This policy encourages global investment in online marketplaces, technology platforms, and logistics infrastructure. The growing penetration of smartphones, digital payment systems, and internet connectivity across India has further accelerated online automotive accessory sales. In addition, many platforms offer customer reviews, ratings, and product demonstrations that help buyers make informed purchasing decisions. E-commerce also enables accessory manufacturers and brands to reach customers in tier-2 and tier-3 cities where physical retail networks may be limited. Faster delivery services and easy return policies further improve customer confidence in online purchases.

India Automotive Accessories Aftermarket Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 14.1 Billion |

|

Revenue Forecast in 2035 |

USD 25.9 Billion |

|

Growth Rate |

6.1% |

|

Segments Covered in the Report |

Product Type, Vehicle Type, Sales Channel, Distribution Channel, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North, South, East, West |

|

Key Companies |

Bosch Limited, Uno Minda Limited, Lumax Industries Limited, Samvardhana Motherson International Limited, Varroc Engineering Limited, Schaeffler India Limited, Denso Corporation, Panasonic Corporation, Faurecia SE, Lear Corporation, Adient plc, Grupo Antolin |

|

Customization |

Available upon request |

India Automotive Accessories Aftermarket Market Segmentation

By Product Type

Electronic accessories are the largest category with a market share of about 30% in 2025, due to the increasing demand for infotainment systems, parking sensors, reverse cameras, dash cameras, and smartphone connectivity devices. Consumers are increasingly upgrading their vehicles with advanced electronic features to enhance convenience, safety, and entertainment. Many vehicles, particularly in the mid-range segment, are purchased with basic configurations, which encourages owners to install additional electronic accessories after purchase. The growing integration of digital technologies in vehicles and the popularity of connected driving features are also supporting demand. Additionally, rising awareness of driver-assistance and safety technologies is encouraging adoption across passenger cars and commercial vehicles.

Interior Accessories is the fastest-growing category with a CAGR of 6.3% during the forecast period, due to increasing consumer focus on comfort, aesthetics, and interior protection. Products such as premium seat covers, floor mats, dashboard trims, organizers, and ambient lighting are becoming highly popular among vehicle owners. As vehicle owners spend more time commuting, demand for comfortable and visually appealing interiors is increasing. The rise of premium vehicle segments and growing consumer willingness to personalize vehicle interiors are further accelerating demand. Additionally, interior accessories are relatively affordable and easy to install, making them accessible to a large customer base.

By Vehicle Type

Passenger cars are the largest category with a market share of about 50% in 2025, due to the large and expanding passenger vehicle fleet across India. Car owners are more likely to invest in accessories such as infotainment systems, seat covers, lighting upgrades, and exterior styling components to enhance vehicle appearance and comfort. The increasing popularity of SUVs and compact SUVs has also boosted accessory demand, as these vehicles are often customized with roof racks, body kits, and advanced electronic accessories. In addition, rising disposable incomes and growing urbanization have significantly increased passenger car ownership.

Light Commercial Vehicles (LCVs) are the fastest-growing category with a CAGR of 6.6% during the forecast period, driven by the rapid expansion of logistics, e-commerce delivery services, and urban transportation networks. Businesses are increasingly equipping LCVs with accessories such as GPS systems, dash cameras, cargo protection accessories, and safety devices to improve operational efficiency and vehicle durability. The growth of last-mile delivery services and small business logistics fleets is significantly increasing the demand for such accessories. Additionally, fleet operators are investing in interior and electronic accessories that enhance driver comfort and vehicle monitoring capabilities.

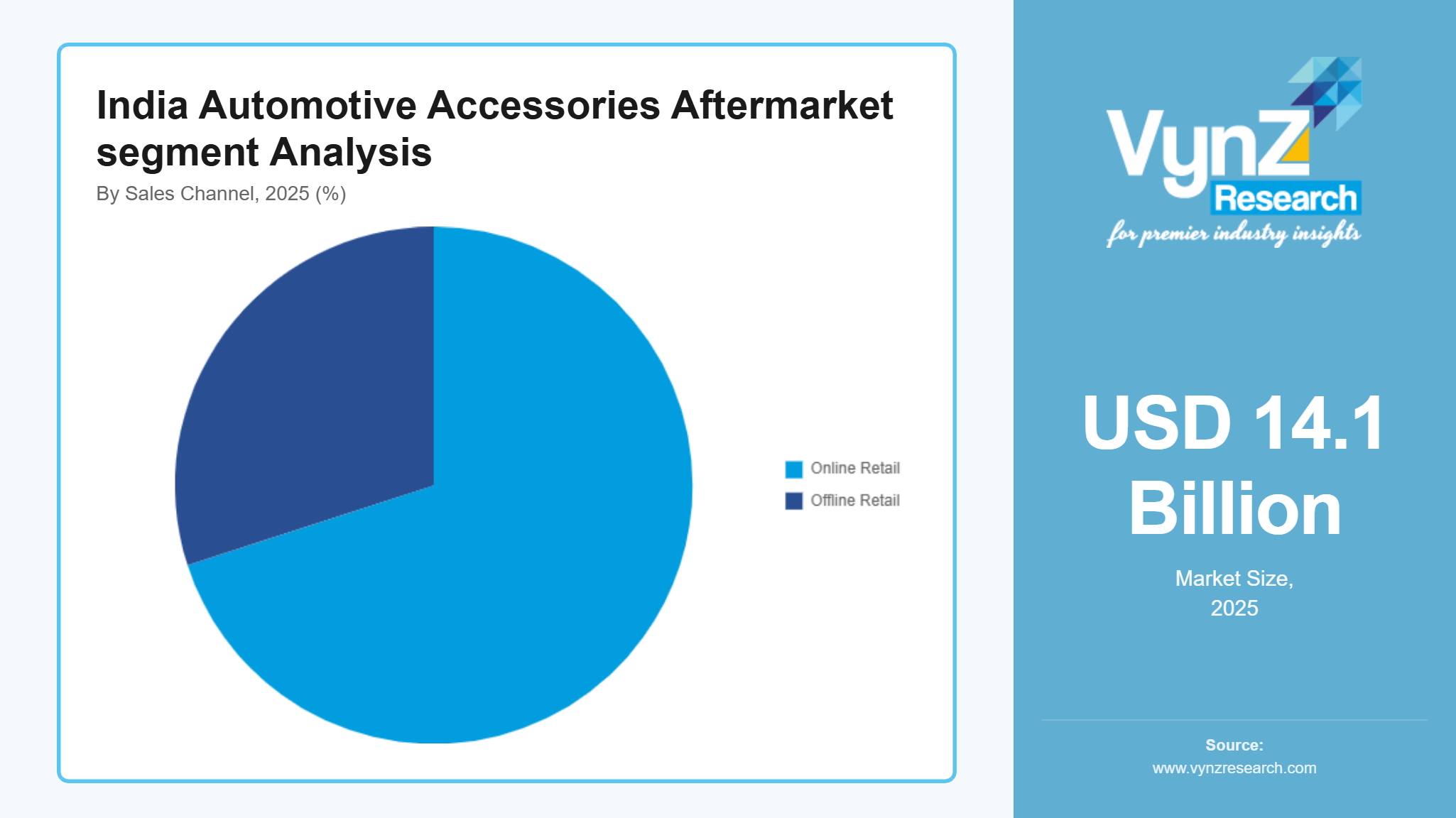

By Sales Channel

Offline retail is the largest category with a market share of about 70% in 2025, primarily due to the strong presence of local automotive accessory shops, service centers, and dealership accessory outlets across India. Many consumers prefer purchasing accessories offline because they can physically inspect products and receive professional installation services. Automotive accessory retailers also provide bundled accessory packages for new vehicles, which further strengthens offline sales. In addition, customers often rely on recommendations from mechanics and installers when selecting accessories. This widespread retail network and installation support continue to make offline retail the dominant sales channel in the India automotive accessories aftermarket.

Online retail is the fastest-growing category during the forecast period, driven by the rapid expansion of e-commerce platforms and increasing internet penetration across India. Online marketplaces allow consumers to compare prices, access a wider range of brands, and read product reviews before making purchases. The availability of doorstep delivery and convenient return policies also enhances consumer confidence in online accessory purchases. Many accessory manufacturers are now partnering with digital marketplaces to expand their reach beyond major cities.

By Distribution Channel

Independent aftermarket retailers are the largest category with a market share of about 55% in 2025, as these retailers dominate the automotive accessory ecosystem across India. Thousands of local accessory shops operate in urban and semi-urban markets, offering a wide range of products at competitive prices. These retailers often provide installation services and customized solutions based on consumer preferences. Their strong local presence and ability to offer affordable products make them highly accessible to vehicle owners. In addition, many consumers prefer independent retailers for quick upgrades and modifications.

E-Commerce platforms are the fastest-growing category with a CAGR of 6.9% during the forecast period, supported by the rapid digitalization of retail and the growing preference for online shopping. Automotive accessory brands are increasingly using e-commerce channels to reach a broader customer base across metropolitan and smaller cities. Online platforms provide greater product variety, competitive pricing, and convenient home delivery options. The availability of installation support through partner service providers also improves the customer experience.

Regional Insights

North

North is the largest regional market for the automotive accessories’ aftermarket in India, supported by a high concentration of vehicle ownership and well-developed automotive retail networks. Major states such as Delhi, Uttar Pradesh, Haryana, and Punjab contribute significantly to accessory demand due to their large passenger car and SUV population. Cities like Delhi are known for extensive automotive accessory markets that supply products not only locally but also to surrounding regions. The Government of India introduced the Vehicle Scrappage Policy to phase out old and polluting vehicles and encourage consumers to replace them with new, safer, and more fuel-efficient vehicles. The policy is expected to attract investments of around ₹10,000 crore in vehicle scrapping infrastructure and automotive recycling facilities. Strong consumer interest in vehicle styling, infotainment upgrades, and interior accessories drives steady aftermarket spending. The region also benefits from a high number of dealerships, service centers, and independent accessory retailers offering installation services. Additionally, rising disposable incomes and a strong culture of vehicle personalization further support demand.

South

South is the fastest-growing regional market in the India automotive accessories aftermarket, driven by increasing automobile sales and rising urbanization. States such as Karnataka, Tamil Nadu, Telangana, and Kerala are experiencing strong growth in passenger vehicle ownership, particularly in major cities like Bengaluru, Chennai, and Hyderabad. The National Automotive Testing and R&D Infrastructure Project (NATRiP) are a major government initiative aimed at strengthening automotive research, development, and testing infrastructure across India. The project involved investments of around ₹1,718 crore to establish multiple advanced automotive testing and validation facilities across the country. Consumers in these urban centers are increasingly investing in premium accessories, electronic upgrades, and interior customization products. The region also has a strong automotive manufacturing ecosystem, which supports accessory production and distribution networks. Growth in the IT sector and rising disposable incomes are encouraging higher spending on vehicle comfort and styling enhancements. Additionally, the expansion of organized automotive accessory retailers and e-commerce platforms is improving product availability across the region.

West

West holds a significant share of the automotive accessories’ aftermarket due to strong economic activity and high vehicle ownership in states such as Maharashtra and Gujarat. Major cities including Mumbai, Pune, and Ahmedabad have large automotive consumer bases and well-established accessory retail networks. The region has a strong presence of automobile manufacturers and component suppliers, which supports accessory availability and competitive pricing. The Automotive Mission Plan (AMP) provides a long-term roadmap for the development of India’s automotive industry through coordinated efforts between government, industry, and research institutions. The roadmap aims to increase vehicle production to about 50 million units by 2030 and around 200 million units by 2047, positioning India among the top global automobile producers. Urban consumers frequently invest in infotainment systems, interior upgrades, and exterior styling accessories. In addition, the expansion of ride-hailing services and commercial vehicle fleets in major metropolitan areas contributes to demand for functional accessories such as GPS systems and protective equipment. Rising disposable incomes and expanding urban infrastructure further support the growth of the aftermarket across West India.

East

East represents an emerging market for automotive accessories, supported by increasing vehicle ownership and improving economic conditions. States such as West Bengal, Odisha, and Bihar are witnessing gradual growth in passenger vehicle sales, which is creating new opportunities for accessory retailers. Urban centers such as Kolkata are developing stronger automotive retail ecosystems with growing numbers of accessory stores and service providers. Consumers in the region are increasingly purchasing essential accessories such as seat covers, floor mats, lighting systems, and mobile holders. The expansion of e-commerce platforms is also improving product accessibility in areas where organized retail networks are limited.

Competitive Landscape / Company Insights

The India automotive accessories aftermarket is highly fragmented, characterized by the presence of numerous domestic manufacturers, international accessory brands, and many independent aftermarket retailers. The market includes both organized and unorganized players, with local accessory manufacturers and small-scale suppliers dominating price-sensitive segments through affordable products and extensive retail networks. Organized automotive component companies and global suppliers compete by offering branded, high-quality accessories that emphasize durability, advanced features, and compatibility with modern vehicles. Major automotive component manufacturers and Tier-1 suppliers such as Uno Minda Limited, Bosch Limited, and Lumax Industries Limited leverage strong manufacturing capabilities, established distribution channels, and partnerships with vehicle manufacturers to expand their aftermarket presence. Global automotive suppliers including Continental AG and Denso Corporation compete through advanced electronic accessories, sensors, and safety technologies that appeal to consumers seeking premium upgrades. In addition, organized accessory retailers and dealership networks play a crucial role in product distribution and professional installation services. E-commerce platforms are also reshaping competition by enabling direct-to-consumer sales and expanding product availability across smaller cities.

Mini Profiles

Bosch Limited is one of the leading automotive technology and component suppliers in India, providing a broad range of automotive aftermarket products including braking systems, filters, spark plugs, batteries, sensors, lighting components, and diagnostic equipment while supporting vehicle maintenance and performance upgrades through an extensive network of distributors, retailers, and service centers across the country.

Uno Minda Limited is a major Indian automotive component manufacturer offering a wide portfolio of aftermarket accessories such as lighting systems, switches, horns, sensors, alloy wheels, and electronic accessories while leveraging its strong manufacturing capabilities and nationwide distribution network to supply products for passenger cars, two-wheelers, and commercial vehicles.

Lumax Industries Limited specializes in automotive lighting solutions, supplying headlamps, tail lamps, fog lamps, and other advanced lighting systems for the aftermarket while maintaining strong partnerships with vehicle manufacturers and a well-established distribution network across India to support replacement and upgrade demand.

Samvardhana Motherson International Limited is a global automotive component supplier providing aftermarket solutions including wiring harness systems, mirrors, interior components, and electronic modules while serving passenger and commercial vehicle markets through its extensive manufacturing and distribution presence across multiple regions.

Key Players

- Bosch Limited

- Uno Minda Limited

- Lumax Industries Limited

- Samvardhana Motherson International Limited

- Varroc Engineering Limited

- Schaeffler India Limited

- Denso Corporation

- Panasonic Corporation

- Faurecia SE

- Lear Corporation

- Adient plc

- Grupo Antolin

Recent Developments

January 2026 – Bosch Limited introduced an upgraded range of smart automotive aftermarket accessories in India, including advanced parking sensors, connected dash cameras, and AI-enabled driver assistance devices designed to enhance vehicle safety and convenience.

December 2025 – Uno Minda Limited expanded its automotive accessories portfolio with new premium interior lighting systems, digital horns, and advanced vehicle electronics aimed at the growing demand for vehicle customization in the Indian aftermarket.

October 2025 – Lumax Industries Limited announced the launch of next-generation LED automotive lighting solutions for the aftermarket, focusing on energy efficiency, longer product life, and improved visibility for passenger and commercial vehicles.

August 2025 – Samvardhana Motherson International Limited strengthened its aftermarket distribution network in India by expanding partnerships with regional automotive retailers and service centers to improve the availability of replacement components and accessories.

June 2025 – Varroc Engineering Limited introduced advanced automotive lighting and exterior styling components designed specifically for SUVs and premium passenger vehicles to support the increasing trend of vehicle personalization in the Indian market.

India Automotive Accessories Aftermarket Coverage

Product Type Insight and Forecast 2026 - 2035

- Interior Accessories

- Exterior Accessories

- Electronic Accessories

- Performance Accessories

- Car Care Accessories

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Two-Wheelers

- Light Commercial Vehicles (LCVs)

- Heavy Commercial Vehicles (HCVs)

Sales Channel Insight and Forecast 2026 - 2035

- Online Retail

- Offline Retail

Distribution Channel Insight and Forecast 2026 - 2035

- OEM Authorized Dealers

- Independent Aftermarket Retailers

- E-Commerce Platforms

India Automotive Accessories Aftermarket by Region

- North

- By Product Type

- By Vehicle Type

- By Sales Channel

- By Distribution Channel

- South

- By Product Type

- By Vehicle Type

- By Sales Channel

- By Distribution Channel

- East

- By Product Type

- By Vehicle Type

- By Sales Channel

- By Distribution Channel

- West

- By Product Type

- By Vehicle Type

- By Sales Channel

- By Distribution Channel

Table of Contents for India Automotive Accessories Aftermarket Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Vehicle Type

1.2.3. By

Sales Channel

1.2.4. By

Distribution Channel

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Interior Accessories

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Exterior Accessories

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Electronic Accessories

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Performance Accessories

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Car Care Accessories

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Vehicle Type

5.2.1. Passenger Cars

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Two-Wheelers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Light Commercial Vehicles (LCVs)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Heavy Commercial Vehicles (HCVs)

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Sales Channel

5.3.1. Online Retail

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Offline Retail

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Distribution Channel

5.4.1. OEM Authorized Dealers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Independent Aftermarket Retailers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. E-Commerce Platforms

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Vehicle Type

6.3. By

Sales Channel

6.4. By

Distribution Channel

7. South Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Vehicle Type

7.3. By

Sales Channel

7.4. By

Distribution Channel

8. East Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Vehicle Type

8.3. By

Sales Channel

8.4. By

Distribution Channel

9. West Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Vehicle Type

9.3. By

Sales Channel

9.4. By

Distribution Channel

10. Company Profiles

10.1.

Bosch Limited

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Uno Minda Limited

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Lumax Industries Limited

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Samvardhana Motherson International Limited

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Varroc Engineering Limited

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Schaeffler India Limited

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Denso Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Panasonic Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Faurecia SE

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Lear Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Adient plc

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Grupo Antolin

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Automotive Accessories Aftermarket