India Tyre Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger Cars, Two Wheelers, Light Commercial Vehicles, Heavy Commercial Vehicles, Off the Road Vehicles), by Tyre Type (Radial Tyres, Bias Tyres), by Sales Channel (OEM, Aftermarket), by Price (Economy, Mid Range, Premium), by End User (Individual Consumers, Commercial Fleets, Industrial Users, Institutional Users)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9669 | Industry : Automotive & Transportation | Available Format :

|

Page : 132 |

India Tyre Market Overview

The India tyre market which was valued at approximately USD 13.2 billion in 2025 and is estimated to rise further up to almost USD 14.1 billion in 2026, is projected to reach around USD 26.8 billion in 2035, expanding at a CAGR of about 7.4% during the forecast period from 2026 to 2035.

The market experiences support from three factors which include growing vehicle production, the increase of active vehicles on the road, and higher demand for vehicle replacements in both passenger and commercial markets, together with the rising use of fuel-efficient tyres that have low rolling resistance. The increasing requirement for personal transportation together with the need for freight movement, which urban areas develop and e-commerce systems expand, increases demand for products in all essential sectors.

The government-backed infrastructure development programs, which include the national highway expansion and logistics corridor modernization projects, create enduring demand for high-quality tyres. The domestic manufacturing policy framework together with electric mobility adoption and sustainability standards development, as well as road safety regulations and emission efficiency requirements, enables industrial growth. The ongoing investment in transport networks and industrial corridors, which major regions including Maharashtra, Tamil Nadu, and Uttar Pradesh, supports both current market growth and future industry development.

India Tyre Market Dynamics

Market Trends

The market is undergoing a structural shift toward advanced and sustainable tyre technologies which align with national mobility transformation programs and environmental efficiency frameworks that receive support from government authorities. The policy direction which focuses on emission reduction, fuel efficiency and road safety standards causes increased adoption of low rolling resistance tyres, ecofriendly rubber compounds and improved tread engineering. Public infrastructure agencies support national transport and road safety initiatives which show the need for vehicle performance and safety compliance to boost demand for durable and high-performance tyres in both passenger and commercial vehicle markets.

Growth Drivers

The market expands because automotive production keeps growing while vehicle expansion drives both OEM and replacement segment demand across all product categories. The national highway development, industrial corridor development and logistics infrastructure development lead to increased tyre consumption in freight intensive areas. The government backed programs which enhance road connectivity and transport efficiency create long term demand stability because regulatory agencies focus on vehicle safety and performance standards which drive product adoption across different vehicle types.

Market Restraints / Challenges

The market experiences growth challenges because raw material price fluctuations which particularly affect natural rubber and petroleum based synthetic inputs lead to production cost increases and price uncontrolled situations. The supply chain needs to depend on vital raw material sources which creates cost uncertainty that harms smaller manufacturers in price sensitive markets and mid-scale manufacturers. The market competitiveness of premium and technologically advanced tyre solutions gets restricted by cost driven market conditions which depend on consumer purchasing power.

Market Opportunities

The market presents significant opportunities in the development of sustainable and eco efficient tyre solutions because regulators increasingly demand carbon neutrality and resource efficiency. Companies which receive government support for sustainability initiatives and environmental compliance frameworks will create innovation driven growth through their recycling programs and bio-based rubber material adoption and retreading technology implementation. The companies which develop high performance products that meet environmental standards will acquire additional business from OEM manufacturers and commercial fleet operators.

India Tyre Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 13.2 Billion |

|

Revenue Forecast in 2035 |

USD 26.8 Billion |

|

Growth Rate |

7.4% |

|

Segments Covered in the Report |

Vehicle Type, Tyre Type, Sales Channel, Price, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North India, West India, South India, East India, Rest of India |

|

Key Companies |

Apollo Tyres Ltd., Balkrishna Industries Ltd., Bridgestone Corporation, CEAT Ltd., Continental AG, Goodyear Tire & Rubber Company, JK Tyre & Industries Ltd., Michelin Group, MRF Ltd., Yokohama Rubber Company Ltd. |

|

Customization |

Available upon request |

India Tyre Market Segmentation

By Vehicle Type

Passenger cars accounted for the largest share of approximately 36% in 2025 because more people started to buy personal vehicles and urban areas needed better transportation services while people replaced their cars at regular intervals throughout both metropolitan and tier two cities. The market will grow at 6.9% according to the upcoming time period because more middle-class people will start to use personal cars which are being supported by urban infrastructure development projects.

The market will see rapid expansion for heavy commercial vehicles which will achieve a compound annual growth rate of 7.9% throughout the upcoming time frame. This growth occurs because logistics networks have expanded and industrial cargo movement has increased while government funding has helped build new highways and create dedicated freight corridors. The transport industry needs high load capacity and long-lasting tyres which drives the development of this specific tyre segment.

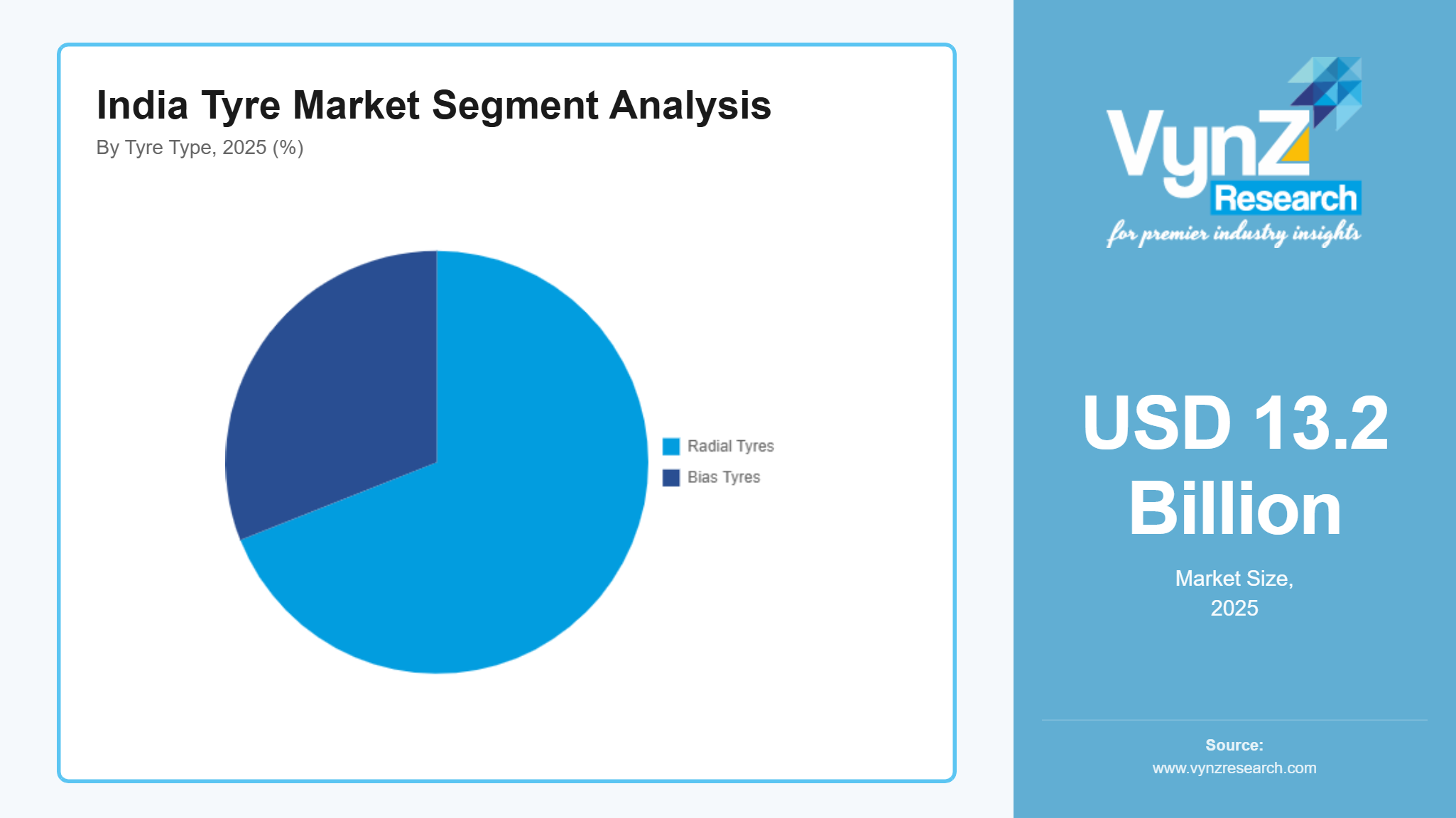

By Tyre Type

Radial tyres controlled the market with a share of about 69% in 2025 because they provide better durability and fuel efficiency which people now use more in both passenger and commercial vehicles. The segment will grow 7.2% before 2025 because customers choose radial configurations as their preferred option and regulations require better fuel efficiency in vehicles.

Bias tyres are expected to register steady growth at approximately 5.8%, primarily supported by demand in agricultural and off highway applications. The non-urban market continues to buy this product because rural and industrial users need cost-efficient and durable solutions.

By Sales Channel

The aftermarket segment accounted for the largest share of approximately 63% in 2025 because people needed to replace their tyres and the number of vehicles on the road increased while tyres needed to be replaced more frequently in urban and semi-urban areas. The market will expand 7.5% because people now understand how tyre maintenance affects safety and tire maintenance, they need to run their retail operations and service facilities.

The OEM segment will grow 6.6% because automotive production remains stable and new vehicles keep using advanced tyre technology. The government programs that support local manufacturing and automotive sector growth create stronger demand from OEMs throughout the nation.

By Price

The mid-range segment controlled the market with a 45% share in 2025 because value-oriented customers wanted products which offered decent performance at reasonable prices. The segment will grow 7.1% because more middle-class families acquire vehicles and people want affordable transportation options.

The premium segment is expected to experience the highest development rate because it will achieve an 8.2% compound annual growth rate throughout the upcoming period. The market expands because more people want high-performance vehicles and customers prefer safety and durability while new tyre technologies become common in urban centers. The segment becomes a vital business area because it creates better profit margins for companies which use strong brand strategies.

By End User

Individual consumers held the largest market share with 42% in 2025 because more people owned private vehicles and they needed to replace their tyres for safety and performance reasons. The segment will grow 6.8% because people have more disposable income and urbanization spreads in important regions.

Commercial fleets will develop at the highest speed because they are expected to grow 7.8% during the upcoming time period. The logistics sector expands rapidly because e-commerce networks build delivery systems which organized transportation companies operate. The demand for long-lasting tyres that provide excellent performance increases because fleets need to operate efficiently while they do predictive maintenance and spend less money during their daily operations.

Regional Insights

North India

The market is expected to reach a 2025 market share of 26% because people want to buy cars and logistics operations are growing and there are many vehicles on the roads in Delhi NCR, Uttar Pradesh and Haryana. Most of both OEM and replacement tyre demand for passenger and commercial vehicles comes from major industrial and consumption hubs which include Delhi, Gurugram and Lucknow. The government-funded infrastructure programs which include expressway construction and freight corridor development work to create better regional connections while more people use their vehicles which results in higher tyre consumption.

West India

West India accounts for 22% of the market in 2025 because industrial activity, automotive manufacturing and port-based trade operations exist throughout Maharashtra and Gujarat. The primary OEM and aftermarket demand for parts comes from Mumbai, Pune and Ahmedabad which act as important automotive and logistics centers. The existence of manufacturing clusters and export-oriented industrial zones produces additional support for tyre consumption by commercial vehicle fleets.

South India

The automotive manufacturing ecosystem in Tamil Nadu, Karnataka and Telangana leads to South India achieving 21% of the automotive tire market by 2025. The cities of Chennai, Bengaluru and Hyderabad operate as major automotive and technology hubs which create demand for both advanced and replacement tyre solutions. The region expands because urbanization increases and personal mobility networks and commercial transport networks expand.

East India

The market in East India reached an 11% share by 2025 because infrastructure development progressed and vehicle usage rose and rural transportation services expanded in West Bengal, Odisha and Bihar. The cities of Kolkata and Bhubaneswar operate as key consumption centers which drive demand for replacement tyres used in passenger and light commercial vehicles. The region expands through better vehicle maintenance understanding and improved safety standards recognition.

Rest of India

The central and northeastern states account for about 20% of the market in 2025 because automotive use and infrastructure development are gradually growing in these areas. The market experiences growth through better road access and increasing vehicle ownership and more people engaging in regional trade and logistics work. The government development initiatives for regional connectivity and economic development and mobility services access lead to increased market demand in these regions.

Competitive Landscape / Company Insights

The market in India operates with moderate to intense competition because both domestic and international manufacturers strive to develop new products while reducing costs and extending their market reach in both original equipment manufacturer and aftermarket segments. Companies are making more research development investments because they want to build their market strength. Government policies that support domestic manufacturing and localization and national industrial programs which establish quality standards create competitive advantages for businesses by driving them to expand their production capacity and modernize their technological systems.

Mini Profiles

Apollo Tyres Ltd. focuses on passenger and commercial tyre solutions, supported by strong domestic distribution network and expanding global presence, enabling consistent demand across replacement and OEM segments in India.

Balkrishna Industries Ltd. operates in niche off highway tyre segments, emphasizing durability, performance reliability, and specialized product engineering for agricultural, construction, and industrial vehicle applications across international markets.

CEAT Ltd. leverages strong brand recognition and widespread dealer network to expand market presence, focusing on cost efficient and performance-oriented tyre solutions across passenger, two-wheeler, and commercial vehicle segments.

Continental AG operates in premium tyre and mobility solutions segments, emphasizing advanced engineering, safety innovation, and digital integration to strengthen positioning across high performance and OEM driven automotive markets.

Goodyear Tire & Rubber Company leverages global brand strength and advanced manufacturing capabilities to expand market presence, focusing on innovative tread designs, durability enhancement, and performance optimization across multiple vehicle categories.

Key Players

- Apollo Tyres Ltd.

- Balkrishna Industries Ltd.

- Bridgestone Corporation

- CEAT Ltd.

- Continental AG

- Goodyear Tire & Rubber Company

- JK Tyre & Industries Ltd.

- Michelin Group

- MRF Ltd.

- Yokohama Rubber Company Ltd.

Recent Developments

In March 2026, Bridgestone Corporation announced an investment of approximately USD 85 million to expand its manufacturing capacity in India, focusing on premium passenger tyre production. The initiative supports rising SUV demand and strengthens its premium positioning.

In October 2025, Michelin Group introduced its first made in India premium passenger car tyre from its Chennai facility. This move supports localization strategy and targets growing demand in high performance and SUV segments.

In September 2025, CEAT Ltd. benefited from government tax rationalization measures that improved affordability of tyres in rural and semi urban markets. The company expects stronger demand across tractor and entry level two-wheeler segments.

In July 2025, Apollo Tyres Ltd. expanded its product portfolio by launching advanced high-performance tyres for passenger vehicles in India. The development aligns with increasing consumer preference for durability, safety, and fuel efficiency.

In December 2025, Yokohama Rubber Company Ltd. expanded its India production capacity to strengthen OEM supply capabilities and meet rising demand for passenger car radial tyres. The company is also focusing on EV compatible tyre solutions.

India Tyre Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Cars

- Two Wheelers

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Off the Road Vehicles

Tyre Type Insight and Forecast 2026 - 2035

- Radial Tyres

- Bias Tyres

Sales Channel Insight and Forecast 2026 - 2035

- OEM

- Aftermarket

Price Insight and Forecast 2026 - 2035

- Economy

- Mid Range

- Premium

End User Insight and Forecast 2026 - 2035

- Individual Consumers

- Commercial Fleets

- Industrial Users

- Institutional Users

India Tyre Market by Region

- North India

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- West India

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- South India

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- East India

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

- Rest of India

- By Vehicle Type

- By Tyre Type

- By Sales Channel

- By Price

- By End User

Table of Contents for India Tyre Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Tyre Type

1.2.3. By

Sales Channel

1.2.4. By

Price

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger Cars

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Two Wheelers

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Light Commercial Vehicles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Heavy Commercial Vehicles

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Off the Road Vehicles

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Tyre Type

5.2.1. Radial Tyres

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bias Tyres

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Sales Channel

5.3.1. OEM

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Aftermarket

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Price

5.4.1. Economy

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Mid Range

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Premium

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Individual Consumers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial Fleets

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial Users

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Institutional Users

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North India Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Tyre Type

6.3. By

Sales Channel

6.4. By

Price

6.5. By

End User

7. West India Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Tyre Type

7.3. By

Sales Channel

7.4. By

Price

7.5. By

End User

8. South India Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Tyre Type

8.3. By

Sales Channel

8.4. By

Price

8.5. By

End User

9. East India Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Tyre Type

9.3. By

Sales Channel

9.4. By

Price

9.5. By

End User

10. Rest of India Market Estimate and Forecast

10.1. By

Vehicle Type

10.2. By

Tyre Type

10.3. By

Sales Channel

10.4. By

Price

10.5. By

End User

11. Company Profiles

11.1.

Apollo Tyres Ltd.

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

Balkrishna Industries Ltd.

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

Bridgestone Corporation

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

CEAT Ltd.

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Continental AG

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

Goodyear Tire & Rubber Company

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

JK Tyre & Industries Ltd.

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

Michelin Group

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

MRF Ltd.

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

Yokohama Rubber Company Ltd.

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Tyre Market