Software-Defined Vehicles Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger Vehicles, Commercial Vehicles, Electric Vehicles, Autonomous Vehicles), by Component (Hardware, Software, Services), by Software Layer (Operating System, Middleware, Application Software), by Application (ADAS & Autonomous Driving, Infotainment Systems, Telematics & Connectivity, Powertrain Control, Body Control & Comfort Systems, Vehicle Management & Diagnostics), by End User (OEMs (Original Equipment Manufacturers), Fleet Operators, Mobility Service Providers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9660 | Industry : Automotive & Transportation | Available Format :

|

Page : 210 |

Software-Defined Vehicles Market Overview

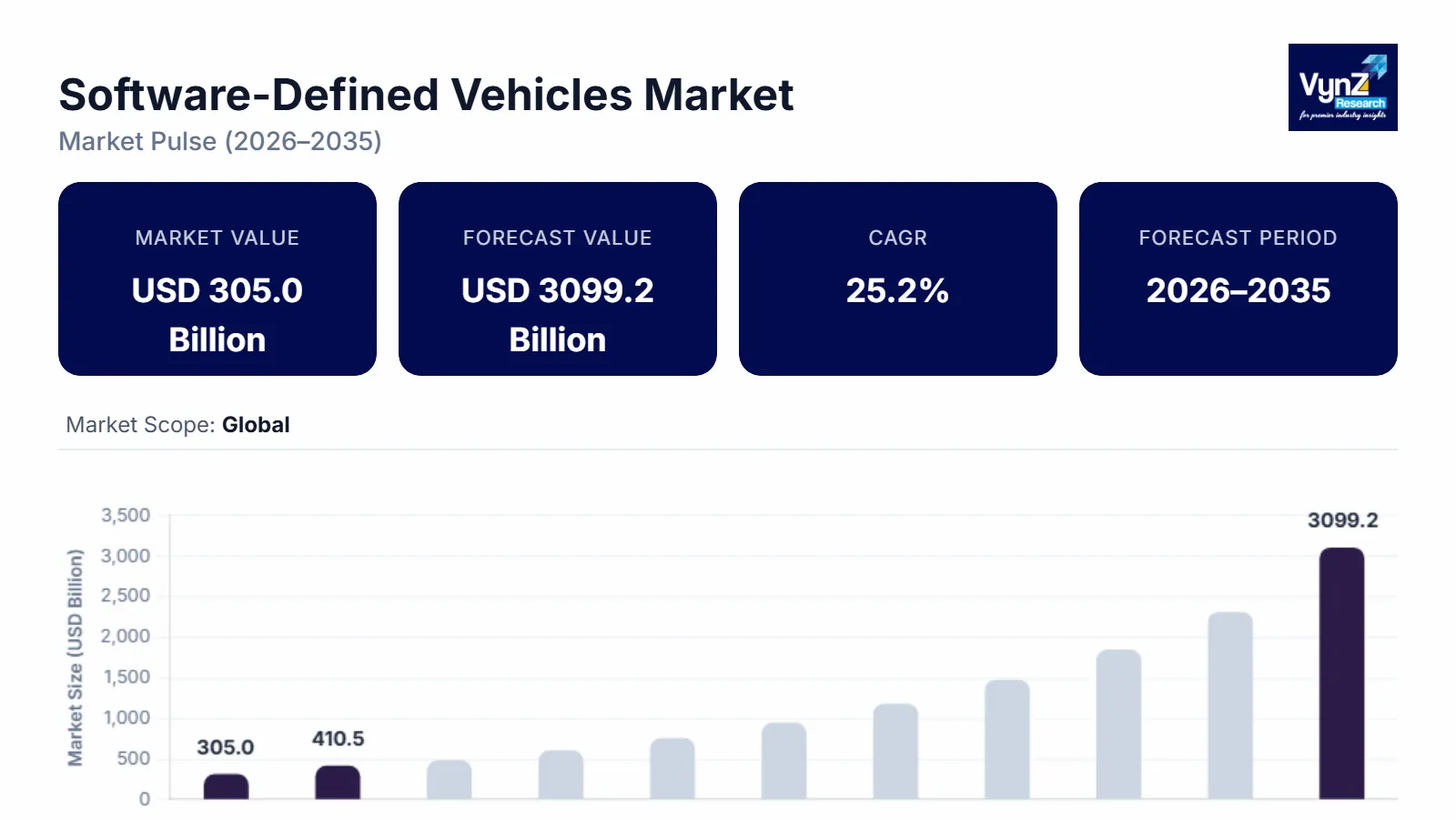

The software-defined vehicles market which was valued at approximately USD 305.0 billion in 2025 and is estimated to reach around USD 410.5 billion in 2026, is projected to reach close to USD 3099.2 billion by 2035, expanding at a CAGR of about 25.2% during the forecast period from 2026 to 2035.

The market is driven by the rapid shift of the automotive industry toward software-centric vehicle architecture, where core functions such as safety, infotainment, connectivity, and powertrain management are controlled through centralized software platforms instead of hardware components. Developers are moving towards software-defined systems to allow over-the-air (OTA) updates, quicker development of new features, and better vehicle performance without necessarily physically modifying them, further lowering the development cost and time. The increased request towards more sophisticated systems of driver-assistance (ADAS), self-driving technologies, and connected car services is also contributing to the accelerated requirement of high-performance computing and adaptable software architectures in the automotive industry.

Moreover, an increasing number of consumer demands over smartphone-like car experiences, including the ability to integrate applications, cloud support, and subscription services, are compelling manufacturers to invest in software platforms. The market is also growing well with the strength of electric vehicles which have a high dependence on software to handle battery management, energy optimization, and remote diagnostics. Governments in key jurisdictions are supporting intelligent movement, automotive safety, and cyber infrastructure, pushing automobile companies to embrace software defined architecture.

Software-Defined Vehicles Market Dynamics

Market Trends

The shift toward centralized vehicle computing architecture is a major trend driving the software-defined vehicles market, as automakers move away from traditional distributed electronic control unit (ECU) systems to more integrated and powerful central computing platforms. Traditional cars frequently have dozens of individual ECUs to manage various functions, and this adds complexity, wiring, and cost to the system along with making it more difficult to maintain. the European Commission under Horizon Europe and the Chips Joint Undertaking, is backed by direct funding through the FEDERATE coordination project, which has a total investment of €1,999,996.25 (≈ €2 million) for the 2023–2026 period. On the contrary, centralized architecture incorporates high performance processors and domain controllers to control various functions of a vehicle using a single software platform which enhances efficiency and scalability. This would allow the software to be updated more quickly, integration of new features to be easier, and the coordination of safety, infotainment, and powertrain systems would be better. It also enables high computing power like autonomous driving, real time data processing, and cloud connectivity. Centralized systems are being embraced by automakers to minimize hardware dependencies and enable constant improvement by updating software.

Growth Drivers

The rising adoption of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies is a major growth driver for the software-defined vehicles market, as these systems rely heavily on complex software, sensors, and high-performance computing platforms. Additional capabilities like adaptive cruise control, lane-keeping aid, automatic emergency breaking, and parking assistance demand real-time information processing and consistent software management, which fits with software-defined vehicle architecture. With the automotive industry progressing to higher automated levels, vehicles must have scalable software platforms that can accommodate artificial intelligence, machine learning, and sensor fusion technologies. There is also the emergence of more stringent safety rules by governments in key automotive markets, with most of them supporting the implementation of ADAS functionality on passenger and commercial vehicles. The European Union Cooperative, Connected and Automated Mobility (CCAM) program includes about €500 million public-private investment to develop automated driving, ADAS, and intelligent transport systems across Europe. Moreover, the development of autonomous driving needs regular software updates, testing, and performance enhancement, which could be effectively provided via software-defined systems and over-the-air updates. Car manufacturers are pouring money into the centralized computing and sophisticated operating systems to help them with these features.

Market Restraints / Challenges

Cybersecurity risks and data privacy concerns in connected vehicles are a major challenge for the software-defined vehicles market, as modern vehicles rely heavily on internet connectivity, cloud platforms, and software-driven functions that can be vulnerable to cyberattacks. The constant communication of software-defined vehicles with the outside networks, mobile applications and infrastructure systems poses the threat of hacking, unauthorized access, and data leakages. A successful cyber-attack may compromise important vehicle operation systems like braking, steering or engine control, posing severe safety consequences on the passengers and other road users. Moreover, the automobiles are connected, thus collecting extents of personal and driving information and the question is on how this information is stored, accessed, and secured. Proposals by governments and regulatory agencies are coming up with stringent cybersecurity and data protection guidelines that heighten the complexity of developments and compliance expenses among automakers. Constant monitoring and highly advanced encryption measures are also needed to ensure safe over-the-air (OTA) updates and safeguard vehicle software against malware.

Market Opportunities

The growth of subscription-based and feature-on-demand vehicle services is creating significant opportunities in the software-defined vehicles market, as automakers shift from one-time vehicle sales to recurring revenue models enabled by software platforms. Software-defined vehicles allow numerous features, including advanced driver assistance functions, infotainment upgrades, navigation services, and performance upgrades, to be turned on or upgraded with software without hardware modification. It will enable the manufacturers to sell subscriptions on a paid basis, temporary unlocking of features, or after-sales upgrades, which can create a stream of income throughout the lifecycle of the vehicle. People are also eager to spend more money on customized and on-demand options, like those found in mobile apps and streaming services, which is pushing car manufacturers to engineer their cars with software capabilities inherent to them. The Japan government-supported mobility platform investment with Toyota and NTT (≈ ¥500 billion / USD 3.3 billion) focuses on building AI-based mobility software platforms, data infrastructure, and connected vehicle ecosystems. These platforms are designed to support advanced driver services, remote updates, and digital vehicle functions that enable feature-on-demand and software-based revenue models. The over-the-air (OTA) update technology provides the capability of providing new services without necessarily having to visit the dealership.

Global Software-Defined Vehicles Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 305.0 Billion |

|

Revenue Forecast in 2035 |

USD 3099.2 Billion |

|

Growth Rate |

25.2% |

|

Segments Covered in the Report |

Vehicle Type, Component, Software Layer, Application, Architecture Type, End User, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Robert Bosch GmbH, Continental AG, Denso Corporation, ZF Friedrichshafen AG, NVIDIA Corporation, Qualcomm Incorporated, Intel Corporation, Aptiv PLC, BlackBerry Limited, Elektrobit Automotive GmbH, Tesla, Inc., Bayerische Motoren Werke AG (BMW AG) |

|

Customization |

Available upon request |

Software-Defined Vehicles Market Segmentation

By Vehicle Type

Passenger Vehicles is the largest category with a market share of about 45% in 2025, due to the high production volume of passenger cars globally and the fast adoption of digital technologies in modern cars. Infotainment, connectivity, ADAS, and over-the-air updates Software-defined architecture is being introduced in passenger vehicles by most automakers. The desire to have a smart feature, personalized settings, and a connected service is in demand among consumers and is increasing the rate of adoption.

Autonomous Vehicles is the fastest-growing category with a CAGR of 25.6% during the forecast period, because of the high rate of development of self-driving machines and AI based vehicle control systems. Autonomous vehicles need high-performance computing, sensor fusion, and real-time software processing, which is a firm fit with the software-defined architecture. Technology firms and governments are putting a lot of money in autonomous mobility initiatives. The necessity of constant software updates and distant diagnostics contribute to SDV acceptance even more.

By Component

Software is the largest category with a market share of around 45% in 2025, due to the transformation of the automotive industry to focus not on hardware but on software in designing a vehicle. Basic vehicle features like infotainment, ADAS, connectivity, and powertrain control are becoming more software controlled. Manufacturers are coming up with own operating systems and middleware that ensures continuous updates and addition of features. Software becomes even more important with the development of subscription-based services.

Services is the fastest-growing category during the forecast period, the growth has been caused by the growing need to integrate software, maintain, connect to clouds, and provide security against cyber-attacks. SDVs need updates, monitoring, and optimization of the system in all its life cycle. Companies in the automotive sector are moving development as well as integration to technology vendors. Recurring service demand is created by over-the-air updates and remote diagnostics. There is also the expansion of cybersecurity and compliance services. Services are also used more through fleet management and mobility platforms.

By Software Layer

Application Software is the largest category with a market share of about 45% in 2025, due to the very broad application of software in infotainment, ADAS, telematics and vehicle control systems. Application software is the most noticeable aspect of SDV architecture as most of the customer-facing features and safety functions are performed by it. Automakers are constantly coming up with new applications that will improve the user experience and performance of the vehicle.

Operating System is the fastest-growing category with a CAGR of 25.8% during the forecast period, as it is premised on the fact that the company needs unified vehicle platforms that can support a variety of functions courtesy of centralized architecture. Car manufacturers are working on their own vehicle operating systems to handle all the areas of the vehicle. One OS makes it easier to update and enhance security and integrate new features. Self-driving and artificial intelligence processing demand a sophisticated system level control.

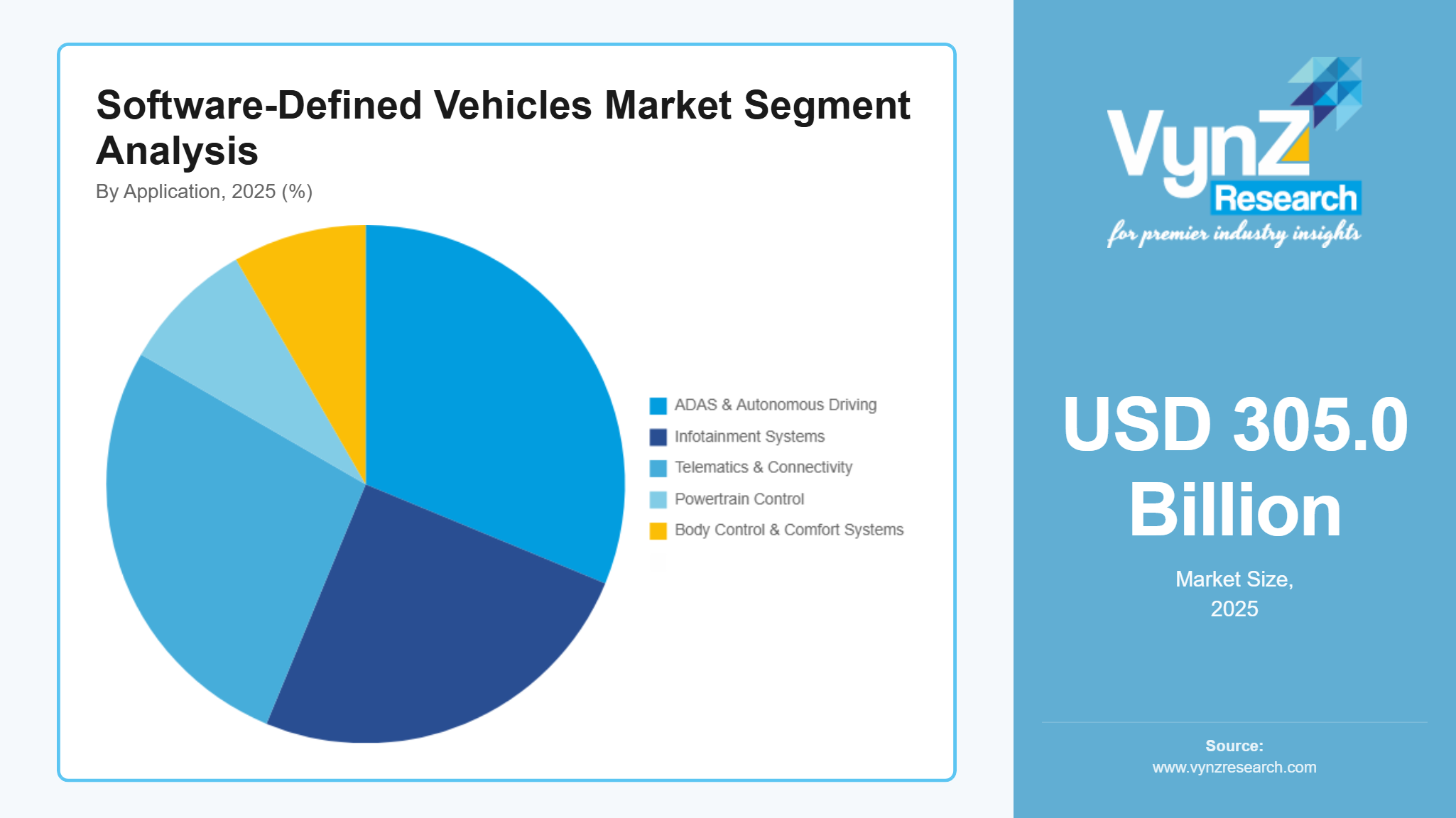

By Application

ADAS & Autonomous Driving is the largest category with a market share of about 30% in 2025, due to the growing integration of safety and automation feature in the contemporary cars. Lane assist, adaptive cruise control, collision warning, and automated parking functions are functions that are based on sophisticated software solutions. Governments are becoming stricter on the safety rules and the ADAS are required in most of the areas. The development of autonomous driving only exposes more needs of software. These systems need high-performance computing and sensor integration.

Telematics & Connectivity is the fastest-growing category with a CAGR of 26.1% during the forecast period, due to the increased need in connected vehicle services and real-time exchange of various information. The consumers demand cars that are capable of navigation, remote control, the capacity to interconnect with applications, and cloud connectivity. 5G and V2X communication allows cars to be highly connected. Telematics are also needed in fleet management and smarter mobility platforms.

By End User

OEMs is the largest category with a market share of about 65% in 2025, due to direct participation of the vehicle manufacturers in the development of software-defined platforms. OEMs are the main adopters of most SDV technologies as these are incorporated when designing and manufacturing the vehicles. Auto manufacturers are spending a lot of money on proprietary code, operating systems, and centralized designs.

Mobility Service Providers is the fastest-growing category during the forecast period, due to the spread of shared mobility, robotaxis, and connected fleet services. These suppliers need cars that have sophisticated software control, remote surveillance, and real-time updates. The software-defined architecture can be used to have an efficient fleet management and predictive maintenance.

Regional Insights

North America

North America is the fastest-growing region in the software-defined vehicles market, driven by strong technological leadership in automotive software, artificial intelligence, and autonomous driving systems. There is a high density of technology firms, semiconductor manufactures, and electric vehicle manufacturers in the United States which are actively building centralized vehicle computing platforms and proprietary automotive operating systems. Rising investments in self-driving, connected vehicles, and over-the-air updates are enhancing the adoption of SDV. Foxconn committed USD 100 million to form MIH EV Design LLC, a joint venture created to develop electric vehicles based on the Mobility in Harmony (MIH) open platform, aimed at modular EV architecture, software-defined vehicle systems, and centralized vehicle computing technologies. The presence of government-assisted smart mobility, the vehicle safety rule, and the cybersecurity guidelines are also promoting the application of advanced software in cars. The large EV manufacturers and cloud service providers serve to enhance the growth of software-based vehicle architecture. The U.S. Department of Transportation Automated Driving Systems research funding allocated about USD 118 million to support testing tools, safety validation, and development of highly automated driving technologies. Rapid adoption is also boosted by high consumer demand for connected vehicles as well as premium vehicles.

Asia Pacific

Asia-Pacific is the largest region in the software-defined vehicles market, supported by its dominant position in global vehicle production, semiconductor manufacturing, and consumer electronics supply chains. China, Japan, South Korea, and India demand a large proportion of the global number of passenger cars and electric vehicles, leading to the large-scale adoption of software-defined platforms. China is putting a major investment on intelligent vehicles, autonomous driving, and EV ecosystems, which generates a high demand in centralized vehicle software. China created more than 300 government-backed investment funds with over USD 200 billion in assets to support high-tech sectors including autonomous vehicles, intelligent connected vehicles, EV platforms, and automotive software technologies under industrial policies such as Made in China 2025 and the national AI development plan. Cost-effective production, good component supply chains, and state subsidies of electric and connected vehicles are also favorable to the region. The Japanese government-supported collaboration between Toyota Motor Corporation and Nippon Telegraph and Telephone includes about ¥500 billion (~USD 3.3 billion) investment to develop an AI-based mobility platform for automated driving, driver-assistance systems, and connected vehicle software infrastructure. The demands of smart and connected cars are on the rise due to rapid urbanization and increase in disposable income. Local car companies are coming up with their own operating systems and software platforms to be used on the international scene.

Europe

Europe represents a technologically advanced and regulation-driven market, characterized by strong automotive engineering and strict safety and environmental standards. Other countries, including Germany, France, and the United Kingdom, are working on the next-generation vehicle architectures that enable software-defined architecture and electric mobility and autonomous driving. A European smart mobility and transport modernization project worth about €535 million, including €179 million EU funding, supports connected vehicles, automated mobility, and digital transport technologies required for software-defined vehicles. The European car manufacturers are spending a lot of money on centralized computing system, cybersecurity systems, and operating systems of the vehicles to meet the tough rules. The high physical demand of the region towards electric vehicles heightens the necessity of software-based systems of battery management and energy optimization. Austria’s Federal Ministry invested about €65 million (2019–2022) in research programs related to automated driving, intelligent transport, and digital vehicle technologies, following earlier investments of about €20 million. These programs support development of advanced vehicle control systems, ADAS technologies, and automated mobility platforms. Privacy of data and cybersecurity laws are also going to promote the implementation of safe car software systems. Cooperation between auto makers, chip makers and software companies favours innovation.

Rest of the World

The Rest of the World, including Latin America, the Middle East, and Africa, is experiencing gradual growth in the software-defined vehicles market due to increasing adoption of connected vehicle technologies and modernization of automotive industries. The Brazil and Mexico are also growing their vehicle manufacturing and absorbing the newer electronics and software systems in new models. Software-defined vehicle platforms are getting new opportunities in the Middle East due to smart city projects, intelligent transport projects, and an investment in electric mobility. The Saudi Arabia NEOM smart mobility project investment, supported by government funding, included about USD 100 million investment in autonomous driving technology development to deploy self-driving vehicles and intelligent transport infrastructure in future smart cities. Connected vehicle technologies are slowly being adopted in African markets, with the infrastructural enhancement of telecom. Even though the region has weaknesses in terms of local software development, alliances with international automakers and technology vendors have been helping in the expansion of the markets. The increasing need in fleet management, mobility services, and digital transportation solutions will be a factor that will lead to growth in the long term.

Competitive Landscape / Company Insights

The software-defined vehicles market is moderately consolidated, characterized by the presence of global automotive manufacturers, semiconductor companies, cloud service providers, and automotive software developers. Major companies like Robert Bosch GmbH, Continental AG, Denso Corporation and ZF Friedrichshafen AG are at a good position because they have a lot of experience in terms of automotive electronics, control systems, and software platforms. Centralized computing architecture, advanced driver-assistance software, and integrated vehicle operating systems are the areas that these companies are focusing on to provide next-generation mobility. These players ensure that they have the competitive edge in the market through long-term relationships with automakers, heavy investments in R&D and international supply chains.

Such technology firms as NVIDIA Corporation, Qualcomm Incorporated, and Intel Corporation are essential in the creation of high-performance automotive processors, artificial intelligence platforms, and software frameworks needed when developing software-defined vehicles. Moreover, like BlackBerry Limited, Elektrobit Automotive GmbH and Aptiv PLC, other companies are already working on automotive operating systems, middleware and cybersecurity that allows over-the-air updates and connected car services. Car manufacturers such as Tesla, Inc., Bayerische Motoren Werke AG, and Mercedes-Benz Group AG are also designing their own software platforms to minimize reliance on suppliers and have a more comprehensive control over vehicle functions. One of the main tendencies in the market is the increasing cooperation of automakers, chip companies, and cloud providers to develop integrated vehicle software systems, and an increase in the number of investments in autonomous driving, electric vehicles, and digital services based on subscriptions to become more competitive in the long term.

Mini Profiles

Robert Bosch GmbH is a leading global automotive technology supplier providing advanced electronic control units, vehicle software platforms, and centralized computing solutions used in software-defined vehicles.

Continental AG is a major automotive electronics and software provider offering high-performance computing platforms, middleware, and advanced driver-assistance software for software-defined vehicle architecture.

Denso Corporation is a key automotive technology company specializing in vehicle electronics, sensors, and software platforms required for intelligent and software-defined vehicles. The company invests heavily in AI-based driving systems, advanced safety technologies, and vehicle control software to support future mobility solutions.

ZF Friedrichshafen AG provides advanced automotive software, domain controllers, and high-performance computing platforms used in software-defined vehicle architecture. The company focuses on autonomous driving software, vehicle motion control systems, and integrated electronic architectures designed for next-generation electric and connected vehicles.

NVIDIA Corporation is a leading provider of artificial intelligence and high-performance computing processors used in autonomous driving and software-defined vehicle platforms. Its automotive computing solutions support real-time data processing, sensor fusion, and centralized vehicle control required for advanced driver-assistance and self-driving systems.

Key Players

- Robert Bosch GmbH

- Continental AG

- Denso Corporation

- ZF Friedrichshafen AG

- NVIDIA Corporation

- Qualcomm Incorporated

- Intel Corporation

- Aptiv PLC

- BlackBerry Limited

- Elektrobit Automotive GmbH

- Tesla, Inc.

- Bayerische Motoren Werke AG (BMW AG)

Recent Developments

January 2026 – NVIDIA Corporation announced the expansion of its automotive computing platform with new high-performance AI processors designed for software-defined vehicles, enabling improved autonomous driving capabilities, real-time data processing, and centralized vehicle computing architecture.

December 2025 – Qualcomm Incorporated introduced an upgraded Snapdragon automotive platform to support advanced driver-assistance systems, in-vehicle infotainment, and cloud-connected services, strengthening its position in software-defined vehicle and connected mobility ecosystems.

November 2025 – Robert Bosch GmbH revealed a new centralized vehicle computer architecture aimed at supporting software-defined vehicle platforms, allowing automakers to integrate multiple vehicle functions into a single high-performance processing unit.

October 2025 – Continental AG announced the development of a scalable software platform for electric and autonomous vehicles, designed to enable over-the-air updates, cybersecurity protection, and integration of advanced digital cockpit features.

September 2025 – Aptiv PLC launched a next-generation vehicle software platform focused on enabling centralized computing, improved connectivity, and faster software deployment for future electric and autonomous vehicles.

Global Software-Defined Vehicles Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Autonomous Vehicles

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Software Layer Insight and Forecast 2026 - 2035

- Operating System

- Middleware

- Application Software

Application Insight and Forecast 2026 - 2035

- ADAS & Autonomous Driving

- Infotainment Systems

- Telematics & Connectivity

- Powertrain Control

- Body Control & Comfort Systems

- Vehicle Management & Diagnostics

End User Insight and Forecast 2026 - 2035

- OEMs (Original Equipment Manufacturers)

- Fleet Operators

- Mobility Service Providers

Global Software-Defined Vehicles Market by Region

- North America

- By Vehicle Type

- By Component

- By Software Layer

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Vehicle Type

- By Component

- By Software Layer

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Vehicle Type

- By Component

- By Software Layer

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Vehicle Type

- By Component

- By Software Layer

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Software-Defined Vehicles Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Component

1.2.3. By

Software Layer

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger Vehicles

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Commercial Vehicles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Electric Vehicles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Autonomous Vehicles

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Hardware

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Software

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Services

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Software Layer

5.3.1. Operating System

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Middleware

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Application Software

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. ADAS & Autonomous Driving

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Infotainment Systems

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Telematics & Connectivity

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Powertrain Control

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Body Control & Comfort Systems

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Vehicle Management & Diagnostics

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. OEMs (Original Equipment Manufacturers)

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Fleet Operators

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Mobility Service Providers

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Component

6.3. By

Software Layer

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Component

7.3. By

Software Layer

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Component

8.3. By

Software Layer

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Component

9.3. By

Software Layer

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Robert Bosch GmbH

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Continental AG

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Denso Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

ZF Friedrichshafen AG

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

NVIDIA Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Qualcomm Incorporated

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Intel Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Aptiv PLC

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

BlackBerry Limited

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Elektrobit Automotive GmbH

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Tesla, Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Bayerische Motoren Werke AG (BMW AG)

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Software-Defined Vehicles Market