U.S. Tyre Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Vehicle Type (Passenger Vehicles, Light Commercial Vehicles, Heavy Commercial Vehicles), by Demand Type (OEM, Replacement), by Rim Size (Less than 15 inches, 15 to 20 inches, Greater than 20 inches), by Distribution Channel (Offline, Online), by End Use (Passenger Mobility, Commercial Transportation)

| Status : Published | Published On : Apr, 2026 | Report Code : VRAT9672 | Industry : Automotive & Transportation | Available Format :

|

Page : 124 |

U.S. Tyre Market Overview

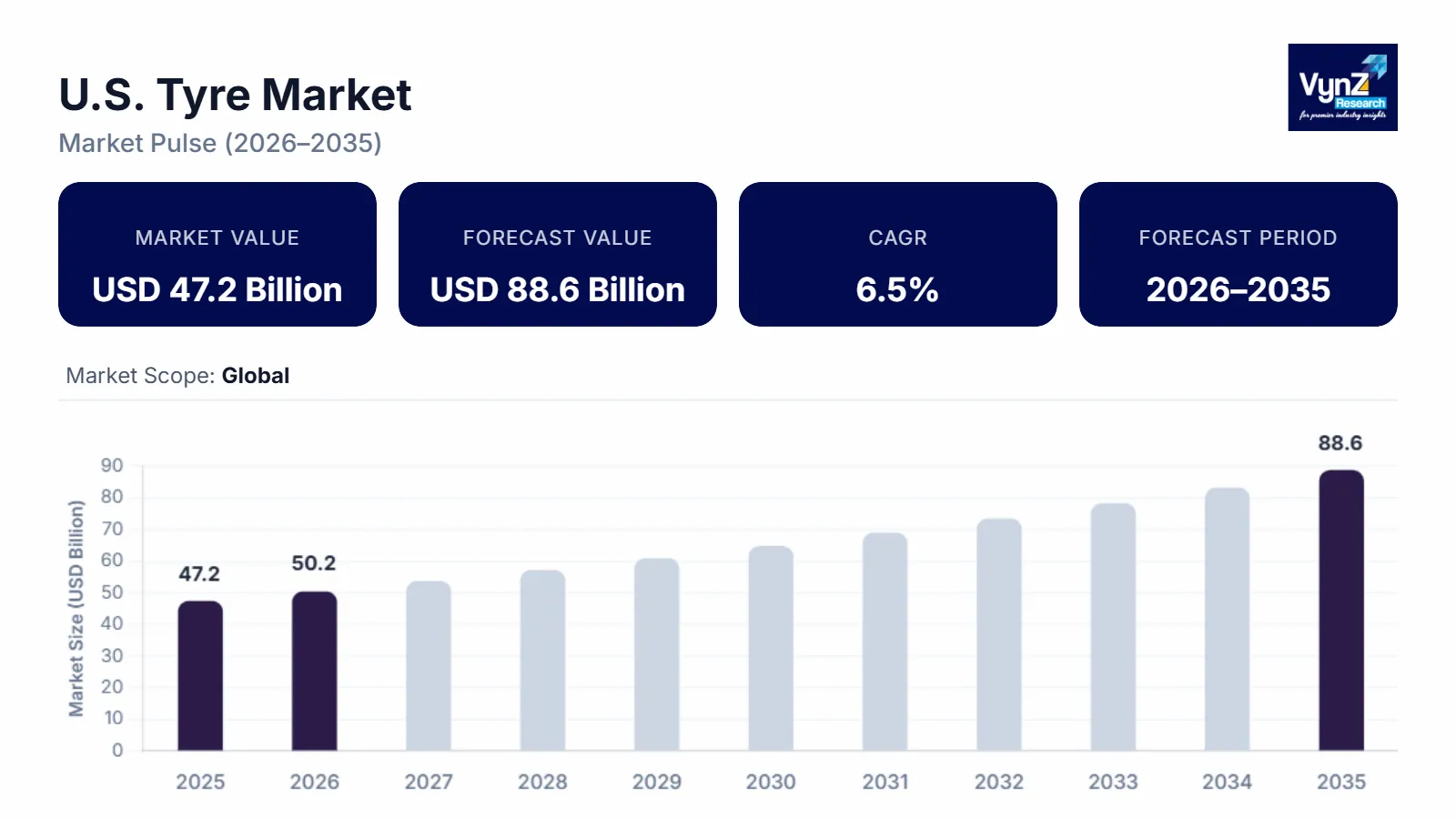

The U.S. tyre market which was valued at approximately USD 47.2 billion in 2025 and is estimated to rise further up to almost USD 50.6 billion by 2026, is projected to reach around USD 88.6 billion in 2035, expanding at a CAGR of about 6.5% during the forecast period from 2026 to 2035.

The market grows because people need to replace tyres after they reach the end of their useful life while light commercial and passenger vehicle production increases. Also, people start using advanced tire systems that include low rolling resistance and all-season performance features. People in need of transportation for personal use and freight delivery will increase their consumption because e-commerce business growth supports this trend. The United States tyre industry benefits from both ongoing regulations and infrastructure improvements that receive funding from government-supported body.

The United States Department of Transportation together with the Federal Highway Administration has released data showing that highway development and road maintenance funding has resulted in higher vehicle traffic which causes more tire replacement need. The National Highway Traffic Safety Administration issues safety regulations which include tire performance standards and fuel efficiency requirements that promote manufacturers to create new advanced products. The industrial sector together with logistics growth in California, Texas, and New York will create sustained market development through their combination of two factors.

U.S. Tyre Market Dynamics

Market Trends

The industry is undergoing major transformations because people now prefer products that deliver efficiency and benefit the environment through their sustainable characteristics. The market experiences its most significant change through the rising popularity of fuel-efficient tires which have low rolling resistance because people now want to achieve better fuel efficiency and meet environmental standards. The National Highway Traffic Safety Administration and the Environmental Protection Agency established regulatory frameworks to which manufacturers must respond by creating new tire materials and designs that increase vehicle efficiency while ensuring safety standards are upheld.

The use of smart tire technologies now emerges as a new market trend which results from the development of digital monitoring systems and connected vehicle technology. Transportation safety programs supported by the government demonstrate how tire pressure monitoring systems contribute to safer roads and better vehicle performance. The company needs to change its product development process because these market developments lead to new product requirements which now require real time performance tracking and predictive maintenance features and enhanced product durability to compete with competitors.

Growth Drivers

The market expands because more active vehicles exist which create steady demand for both passenger and commercial vehicles. The market shows faster growth because transportation infrastructure development and logistics network development continue to increase. The United States Department of Transportation and Federal Highway Administration report that current highway modernization projects and freight mobility programs will result in higher road usage which will lead to increased tire wear and replacement needs throughout the nation.

The growth of e commerce and freight transportation services plays a vital role in increasing adoption rates of these services. The demand for tires that provide both strength and extended mileage will stay strong throughout the forecast period because logistics operators and fleet owners now require tires that deliver both operational efficiency and cost savings. The industrial and commercial transportation sectors maintain their demand levels because government programs that improve supply chains and freight efficiency continue to run.

Market Restraints / Challenges

The market maintains its growth potential but it encounters several obstacles which restrict its market expansion potential. The price changes of raw materials especially natural rubber and synthetic compounds create profitability problems which prevent price sensitive segments from entering the market. The United States Department of Agriculture reports that natural rubber supply experiences fluctuations because of both climate changes and international trade dependencies which create manufacturing cost risks.

Manufacturers and suppliers face operational difficulties because they must comply with both regulatory requirements and environmental protection standards. The use of imported raw materials together with global supply chains creates situations that result in both increased costs and delayed deliveries especially when geopolitical or economic conditions become unstable. Environmental Protection Agency regulations increase production expenses for manufacturers which results in lower market performance during uncertain economic times.

Market Opportunities

The market provides substantial opportunities for companies that create environmentally friendly tire solutions which achieve high performance standards because governmental regulations now emphasize emission reduction and environmental sustainability. Environmentally conscious consumers will choose advanced tire technologies which show improved durability and fuel efficiency, so companies that provide these solutions will meet their increasing demand. The manufacturing process and tire materials which reduce environmental impact through government supported clean transportation initiatives and sustainability frameworks will become the new standard in tire production.

The premium tire segment and high technology tire segment present a major opportunity for the industry because investment in smart vehicle solutions will create profitable business relationships with long term customers. The company will gain better customer interaction and improved operational performance through its implementation of digital monitoring systems, automated manufacturing processes and data-driven fleet management systems. The combination of transportation modernization programs and safety initiatives will create market growth opportunities that enhance market positions for businesses.

U.S. Tyre Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 47.2 Billion |

|

Revenue Forecast in 2035 |

USD 88.6 Billion |

|

Growth Rate |

6.5% |

|

Segments Covered in the Report |

Vehicle Type, Demand Type, Rim Size, Distribution Channel, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

West, South, Midwest, Northeast |

|

Key Companies |

Bridgestone Corporation, Continental AG, Cooper Tire & Rubber Company, Goodyear Tire & Rubber Company, Hankook Tire & Technology Co., Ltd., Michelin Group, Nokian Tyres plc, Pirelli & C. S.p.A., Sumitomo Rubber Industries, Ltd., Yokohama Rubber Company |

|

Customization |

Available upon request |

U.S. Tyre Market Segmentation

By Vehicle Type

Passenger vehicles accounted for the largest share of the market in 2025, which produced roughly 62% of total revenue. The vehicle population combined with ownership rates and replacement cycles which people follow through their daily commuting and personal mobility determines this dominant market position. Federal Highway Administration data shows that registered passenger vehicles have been increasing which leads to constant tyre demand throughout their lifespan. The consumption patterns of urban areas and private vehicle usage have experienced growth, particularly in states with high population density and urban areas.

Light commercial vehicles will experience the highest growth rates as they have an expected compound annual growth rate of 6.9% which will occur between 2026 and 2035. The industry progresses through its delivery system improvements which enhance last mile delivery operations, logistics services and e commerce distribution network expansion. Government programs which support transportation facilities and freight efficiency have raised commercial fleet operations which results in more vehicle wear. Heavy commercial vehicle operations maintain their market presence because industrial freight and infrastructure development projects require these vehicles, which scientists calculate will grow by 6.2% during long distance hauling.

By Demand Type

Replacement demand accounted for the largest share of the market in 2025, representing approximately 74% of total revenue. The continuous tyre wear and tear together with shorter replacement cycles and the large number of vehicles currently operating in the market make this segment the dominant force in the industry. The National Highway Traffic Safety Administration states that safety regulations about tyre performance and maintenance practices lead to drivers replacing their tyres at the appropriate time, which results in ongoing demand. Regional climate conditions and seasonal changes create different replacement needs for various vehicle types across the entire automotive industry.

OEM demand will experience a faster growth rate because the market will expand at an estimated CAGR of 6.7% during the forecast period. Vehicle production and assembly operations in the United States are expanding, which leads to growth in this market sector. Domestic automotive production receives a boost from industrial policies and manufacturing incentives, which results in increased OEM tyre installations. The OEM market segment will expand at a stable pace of 6.3% because new vehicles include fuel-efficient tyres and performance-based tyre technologies.

By Rim Size

The mid-range rim size category accounted for the largest share in 2025, contributing approximately 48% of total segment revenue. The widespread usage of this product throughout passenger vehicles and light commercial fleets establishes its market dominance because standardization creates purchasing advantages through cost efficiency. Government transportation data shows that a majority of vehicles fall within this category, which ensures ongoing demand for the product. The product maintains its market leadership because it offers affordable pricing and compatibility with various vehicle types.

The fastest growing market for tyres will be larger rim size tyres, which will experience a CAGR of 6.8% between 2026 and 2035. The market for premium vehicles and SUVs and performance-oriented automobiles continues to expand because more customers demand these types of vehicles. Rising consumer preference for enhanced driving experience and vehicle aesthetics is contributing to higher adoption. The market for smaller rim sizes maintains steady demand because entry level vehicles and cost sensitive customers support their growth at a rate of 5.9%.

By Distribution Channel

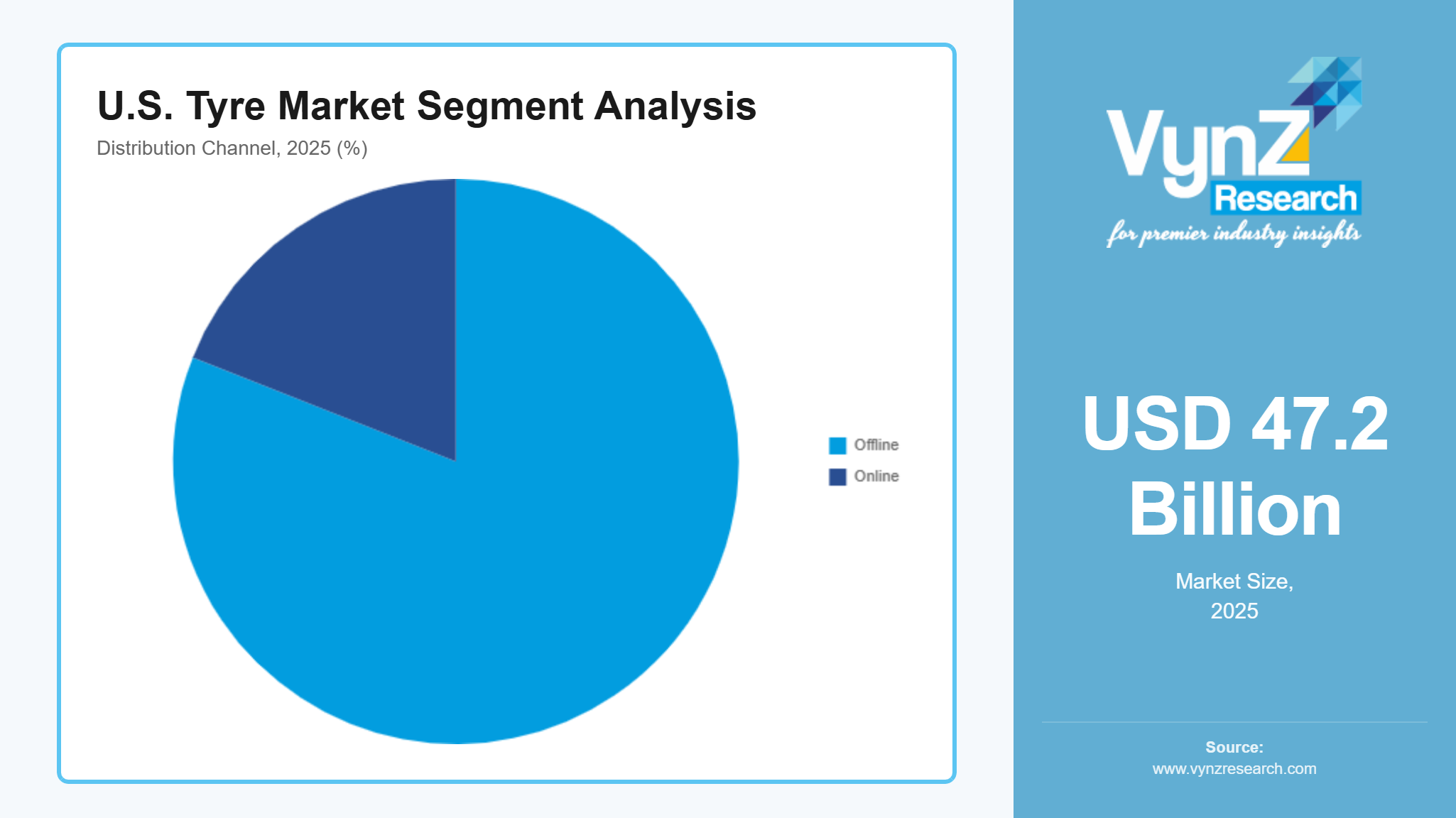

Offline distribution channels accounted for the majority share in 2025, representing approximately 81% of total market revenue. Consumers prefer to examine products physically, which includes installation services and after-sales support, which keeps the market leader position for this segment. Retail outlets, authorized dealerships, and service centers continue to play a critical role in product validation and customer trust. The existing vehicle safety and maintenance regulations expect professional installation to be performed, which drives demand for offline channel development.

Online distribution is witnessing rapid expansion, with an estimated CAGR of 7.1% during the forecast period. The market for e commerce platforms grows because more people use digital services and logistics systems become better and pricing information becomes accessible to users. Customers can now order products online and have them installed offline, which improves their convenience and access to these services. Government programs which support digital commerce and supply chain updates have led to market expansion for this segment because urban customers are adopting the segment at a steady rate.

By End Use

The passenger mobility segment accounted for the largest share in 2025, contributing approximately 58% of total market revenue. The segment exists because people own many vehicles while cities keep growing and they need to commute to work daily. The governments who invest in infrastructure and urban development programs create better road systems which lead to more vehicle usage and tyre replacements. The strong demand for passenger vehicles in urban and suburban areas persists because these factors maintain their market presence in both regions.

The commercial transportation segment is expected to register the fastest growth, with an estimated CAGR of 6.9% during the forecast period from 2026 to 2035. Logistics services and freight transportation and industrial supply chain operations will keep growing, which drives market expansion. Government-backed projects for freight mobility and infrastructure modernization lead to better fleet operations because they improve operational performance. The commercial users of tyre products require durable and high-performance solutions, which results in sustainable market growth for these companies.

Regional Insights

West

The West Coast contributed nearly 29% of the market in 2025 because California, Washington and Oregon have high vehicle ownership rates and their cities are densely populated and their logistics operations are strong. Cities like Los Angeles, San Francisco and Seattle create ongoing demand through their daily commuting needs and business transportation requirements. The California Department of Transportation and the Federal Highway Administration report that highways see heavy traffic and trucks move freight which causes tyres to need replacement more often.

South

The Southern region holds about 24% of the 2025 market while its market size keeps on expanding because Texas, Florida and Georgia continue to develop their industrial base and population and infrastructure projects. Logistics and construction and passenger mobility now make up the core demand segments that keep growing. The Texas Department of Transportation and federal infrastructure programs report that freight volumes are rising which allows commercial fleets to use their tyres continuously.

Midwest

The Midwest region held 18% of the market in 2025 because its states Michigan, Ohio and Illinois have strong automotive manufacturing and agricultural transportation needs. The region expands because its industrial sector is growing while supply chains operate and freight travel routes between important logistics hubs. The United States Department of Transportation shows that the region serves as a key center for moving goods between states and distributing products.

Northeast

The Northeast region holds approximately 12% of the 2025 market because New York, Massachusetts and Pennsylvania have dense urban areas and established transportation systems and residents frequently travel to work. New York and Boston maintain their high vehicle demand because their traffic congestion and road congestion create a constant need for vehicle services. The government backed programs that maintain infrastructure together with urban mobility projects create better road conditions which lead to increased tyre usage. The remaining share of the market is covered by other smaller regions and territories not included above, ensuring the overall regional distribution remains balanced and comprehensive.

Competitive Landscape / Company Insights

The market has a moderate level of competition because global tyre manufacturers from established companies and domestic tyre manufacturers who use product development, pricing methods and regional market growth strategies compete in the industry. Companies use research and development spending together with their development of new material technologies and digital manufacturing systems to build competitive advantages in their markets. The National Highway Traffic Safety Administration and Environmental Protection Agency regulatory standards drive manufacturers to enhance product safety features and fuel efficiency which creates more competition between premium products and mid-range products.

Mini Profiles

Bridgestone Corporation focuses on advanced tyre manufacturing and mobility solutions, supported by strong global distribution networks, established brand recognition, and continuous investment in sustainable and high performance product development.

Continental AG operates in premium segments, emphasizing performance engineering, safety technologies, and intelligent mobility solutions, with a strong focus on innovation, digital integration, and advanced tyre design capabilities.

Goodyear Tire & Rubber Company leverages extensive manufacturing capabilities and strategic partnerships to expand market presence, supported by a strong replacement market footprint and continuous advancements in smart tyre technologies.

Michelin Group focuses on high performance and sustainable tyre solutions, supported by strong research and development capabilities, premium brand positioning, and extensive global distribution across automotive and specialty segments.

Yokohama Rubber Company operates in both premium and mid-range segments, emphasizing product innovation, motorsport driven performance, and cost-efficient manufacturing supported by expanding international market presence.

Key Players

- Bridgestone Corporation

- Continental AG

- Cooper Tire & Rubber Company

- Goodyear Tire & Rubber Company

- Hankook Tire & Technology Co., Ltd.

- Michelin Group

- Nokian Tyres plc

- Pirelli & C. S.p.A.

- Sumitomo Rubber Industries, Ltd.

- Yokohama Rubber Company

Recent Developments

In February, 2026, Pirelli & C. S.p.A. expanded its portfolio of high-performance tyres with advanced sensor enabled solutions designed for premium and luxury vehicles. The development focuses on improving real time monitoring and enhancing driving safety and efficiency across connected mobility platforms.

In March, 2026, Hankook Tire & Technology Co., Ltd. announced the expansion of its electric vehicle tyre lineup with products optimized for durability and energy efficiency. This initiative supports increasing EV penetration and strengthens its presence in the North American market.

In January, 2026, Yokohama Rubber Company introduced new sustainable tyre compounds incorporating a higher proportion of renewable materials. The development aligns with environmental regulations and supports long term carbon neutrality targets across its global operations.

In April, 2026, Nokian Tyres plc expanded its manufacturing capacity in North America to enhance supply chain resilience and reduce delivery timelines. This move is aimed at strengthening regional market presence and meeting rising demand for all season and winter tyres.

In May, 2026, Cooper Tyre & Rubber Company focused on expanding its distribution network through strategic partnerships with regional dealers and service providers. The initiative enhances market accessibility and supports growth in the replacement tyre segment across the United States.

U.S. Tyre Market Coverage

Vehicle Type Insight and Forecast 2026 - 2035

- Passenger Vehicles

- Light Commercial Vehicles

- Heavy Commercial Vehicles

Demand Type Insight and Forecast 2026 - 2035

- OEM

- Replacement

Rim Size Insight and Forecast 2026 - 2035

- Less than 15 inches

- 15 to 20 inches

- Greater than 20 inches

Distribution Channel Insight and Forecast 2026 - 2035

- Offline

- Online

End Use Insight and Forecast 2026 - 2035

- Passenger Mobility

- Commercial Transportation

U.S. Tyre Market by Region

- West

- By Vehicle Type

- By Demand Type

- By Rim Size

- By Distribution Channel

- By End Use

- South

- By Vehicle Type

- By Demand Type

- By Rim Size

- By Distribution Channel

- By End Use

- Midwest

- By Vehicle Type

- By Demand Type

- By Rim Size

- By Distribution Channel

- By End Use

- Northeast

- By Vehicle Type

- By Demand Type

- By Rim Size

- By Distribution Channel

- By End Use

Table of Contents for U.S. Tyre Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Vehicle Type

1.2.2. By

Demand Type

1.2.3. By

Rim Size

1.2.4. By

Distribution Channel

1.2.5. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. U.S. Market Estimate and Forecast

4.1. U.S. Market Overview

4.2. U.S. Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Vehicle Type

5.1.1. Passenger Vehicles

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Light Commercial Vehicles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Heavy Commercial Vehicles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Demand Type

5.2.1. OEM

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Replacement

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Rim Size

5.3.1. Less than 15 inches

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. 15 to 20 inches

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Greater than 20 inches

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Distribution Channel

5.4.1. Offline

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Online

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By End Use

5.5.1. Passenger Mobility

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial Transportation

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

6. West Market Estimate and Forecast

6.1. By

Vehicle Type

6.2. By

Demand Type

6.3. By

Rim Size

6.4. By

Distribution Channel

6.5. By

End Use

7. South Market Estimate and Forecast

7.1. By

Vehicle Type

7.2. By

Demand Type

7.3. By

Rim Size

7.4. By

Distribution Channel

7.5. By

End Use

8. Midwest Market Estimate and Forecast

8.1. By

Vehicle Type

8.2. By

Demand Type

8.3. By

Rim Size

8.4. By

Distribution Channel

8.5. By

End Use

9. Northeast Market Estimate and Forecast

9.1. By

Vehicle Type

9.2. By

Demand Type

9.3. By

Rim Size

9.4. By

Distribution Channel

9.5. By

End Use

10. Company Profiles

10.1.

Bridgestone Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Continental AG

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Cooper Tire & Rubber Company

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Goodyear Tire & Rubber Company

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Hankook Tire & Technology Co., Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Michelin Group

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Nokian Tyres plc

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Pirelli & C. S.p.A.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Sumitomo Rubber Industries, Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Yokohama Rubber Company

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

U.S. Tyre Market