Vehicle-to-Grid Technology Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Electric Vehicles (EVs), EV Charging Stations (Bidirectional Chargers), Smart Meters, Software & Energy Management Systems), by Technology Type (Unidirectional V2G (V1G / Smart Charging), Bidirectional V2G), by Vehicle Type (Battery Electric Vehicles (BEV), Plug-in Hybrid Electric Vehicles (PHEV), Fuel Cell Electric Vehicles (FCEV)), by Application (Peak Power Management, Frequency Regulation, Renewable Energy Integration, Backup Power Supply, Demand Response Services), by End User (Residential, Commercial, Industrial, Utilities / Grid Operators)

| Status : Published | Published On : Mar, 2026 | Report Code : VRAT9661 | Industry : Automotive & Transportation | Available Format :

|

Page : 195 |

Vehicle-to-Grid Technology Market Overview

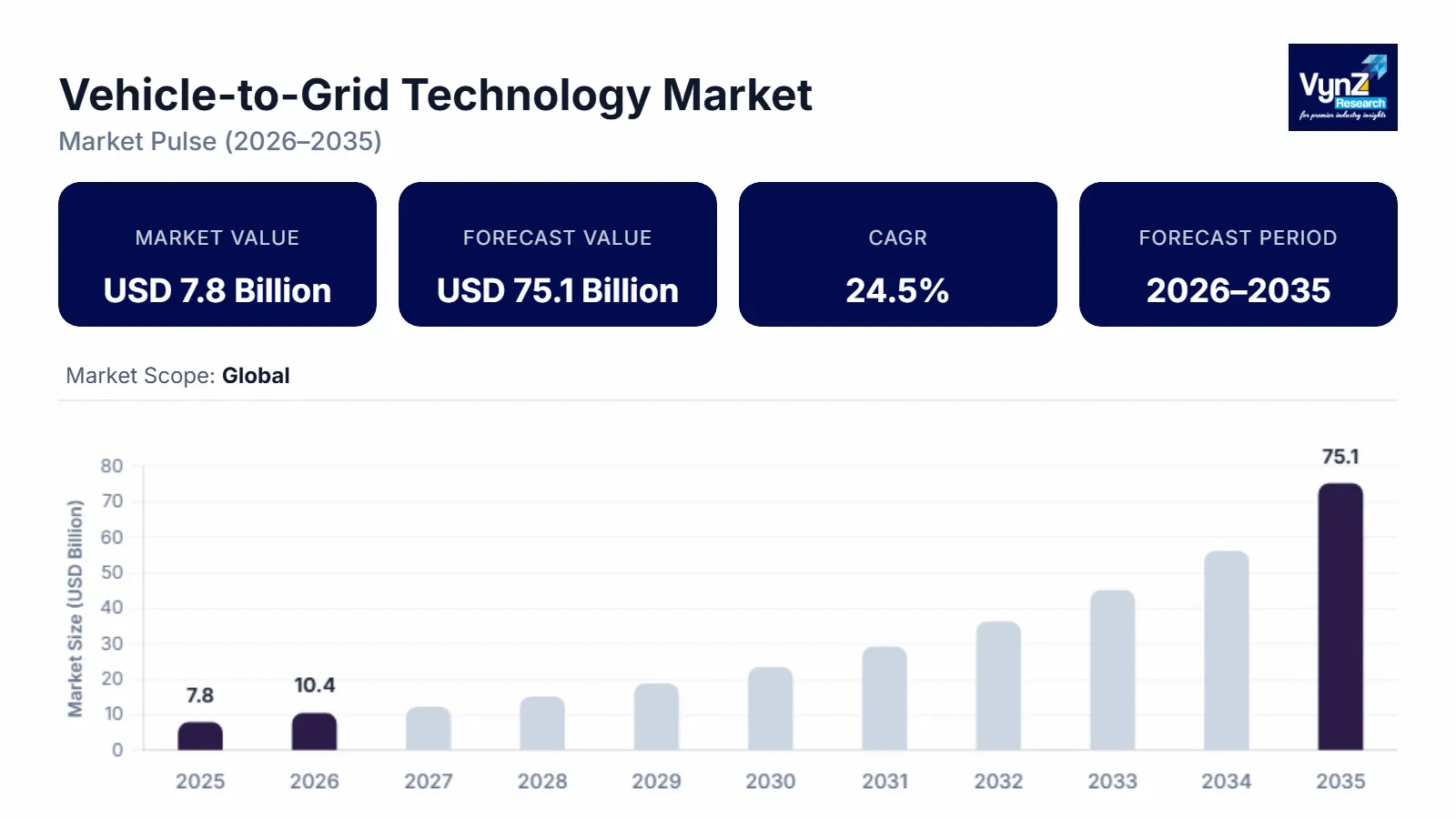

The vehicle-to-grid (V2G) technology market which was valued at approximately USD 7.8 billion in 2025 and is estimated to reach around USD 10.4 billion in 2026, is projected to reach close to USD 75.1 billion by 2035, expanding at a CAGR of about 24.5% during the forecast period from 2026 to 2035.

The market is driven by the rapid global shift toward electric vehicles (EVs) and the increasing need for efficient energy management systems. North American, European, and Asian-Pacific governments are encouraging the adoption of EVs by providing subsidies, tax credits, and catalyzing stringent emission limits, which is growing the number of electric vehicles that can be utilized to integrate V2G. Meanwhile, the increased adoption of renewable energy sources like solar and wind has caused a need of grid-balancing technologies, in which V2G technology will allow EV batteries to store surplus energy and release it back into the grid when the demand peaks. Smart grid infrastructure and grid bidirectional charging are being considered by utilities and grid operators to enhance grid stability as well as to minimize the use of fossil-fuel-powered peaker plants.

Moreover, increasing electricity demands, urbanization, and aspects of energy resilience are also fostering the use of distributed energy storage systems which further promotes the use of V2G. V2G partnerships between automakers and energy companies are also emerging to create V2G-enabled vehicles and charging networks, which are commercializing faster. Additionally, the potential of V2G technology to offer cost-saving benefits, energy trading, and a source of backup electricity to consumers and businesses is making it more economically appealing.

Vehicle-to-Grid Technology Market Dynamics

Market Trends

The integration of renewable energy with vehicle-to-grid (V2G) systems is a major trend driving the growth of the V2G technology market, as power grids increasingly rely on intermittent energy sources such as solar and wind. The production of renewable energy sources is usually unpredictable according to weather conditions, which makes it difficult to sustain the stability of the grid and balance the electricity supply and demand. The U.S. government launched a $25 billion loan program to support advanced vehicle technologies, including electric vehicles, battery systems, grid integration, and energy-efficient transportation projects. The V2G technology will make them electric vehicles which can be treated as distributed energy storage platforms where the surplus renewable energy produced at low-demand times can be stored in the EV batteries and released into the grid when the demand increases. This will enable utilities to minimize the wastage of energy and minimize the reliance on fossil-fuel-based backup power plants. To ensure harmonious incorporation of renewables into the V2G networks, governments and grid operators are investing in smart grid infrastructure and energy management systems. Moreover, V2G pilot projects are being combined with large scale renewable projects in Europe, the United States, China, and Japan to increase grid flexibility. The increased attention to decarbonization and carbon-neutral energy systems is also contributing to the increased use of V2G solutions associated with renewable power.

Growth Drivers

The rapid growth in electric vehicle adoption worldwide is one of the primary drivers of the Vehicle-to-Grid (V2G) technology market, as the increasing number of EVs creates a large network of mobile energy storage units that can support grid operations. The governments of key economic regions like the United States, China, Germany, Japan and India are encouraging the use of electric vehicles by subsidizing them, providing tax breaks and imposing stringent emission standards to cut down on carbon emission and reliance on fossil fuels. The Government of India launched the FAME (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) program with a budget of about ₹10,000 crore, providing subsidies for electric two-wheelers, cars, buses, and charging infrastructure. The possible capacity of connected batteries that can be enrolled in V2G programs also grows considerably as the EV sales continue to grow annually. This enables the utilities to store surplus electricity using EV batteries at low demand times and release it to the grid when the demand is high to enhance energy efficiency. There is also the development of vehicles with inbuilt bidirectional charging thus V2G compatible by the automakers. Moreover, EV ownership is becoming more feasible due to the growth of both state-owned and privately owned charging networks, which is driving the adoption further. Electrification of fleets in the public transport, logistics and corporate vehicles is also leading to availability of large battery capacity to the grid support.

Market Restraints / Challenges

Limited standardization and interoperability issues represent a significant challenge for the Vehicle-to-Grid (V2G) technology market, as the lack of uniform technical standards makes it difficult for different vehicles, chargers, and grid systems to communicate effectively. Different protocols and software platforms are commonly employed by various automakers, charging equipment vendors, and utility providers and may lead to compatibility issues during the integration of V2G solutions. The large scale implementation of V2G infrastructure is complicated and expensive without universally accepted international standards to communicate in both directions in grid charging, grid communication, and energy management systems. The lack of regular regulation rules also makes interoperable systems development slow in most areas. The utilities might be unwilling to invest in V2G projects, in the case where the technology is not capable of easily integrating with the existing grid networks. Moreover, consumers and fleet operators can experience uncertainty concerning the future levels of compatibility of their vehicles with future charging infrastructure. Organizations in the industry and governments are trying to set standard standards but slowly. V2G technology will not achieve widespread commercial use until there is better interoperability, and this means that it will continue to be implemented only in pilot projects and in a few markets.

Market Opportunities

The growing deployment of renewable energy power projects is creating significant opportunities for the Vehicle-to-Grid (V2G) technology market, as the increasing share of solar, wind, and other clean energy sources requires advanced energy storage and grid balancing solutions. Under the Green Energy Corridor project, the government approved a project cost of about ₹12,031 crore, including central financial assistance of about ₹3,970 crore, to build transmission networks that can evacuate renewable power from solar and wind projects and integrate it into the national grid. The generation of renewable energy is also variable in nature since solar energy requires the presence of sunlight and wind power requires the weather conditions, thus making it unstable at times to power. V2G technology can overcome this issue because it enables electric cars to store surplus renewable electricity during the high production process and release it into the grid when the demand is high. The need to generate renewable sources on a large scale has seen governments all over the world spending heavily to ensure carbon neutrality and dependence on fossil fuels, therefore increasing the demand of flexible storage systems such as V2G. The V2G is also being considered by the utilities as a less expensive option to the construction of new stationary battery storage facilities. Moreover, the developers of renewable energy projects, along with the smart grid technologies, are promoting bidirectional charging infrastructure. Pilot programs are being initiated in countries worldwide in Europe, North America, China, Japan, and India, that combine EV fleets with renewable power systems.

Global Vehicle-to-Grid Technology Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 7.8 Billion |

|

Revenue Forecast in 2035 |

USD 75.1 Billion |

|

Growth Rate |

24.5% |

|

Segments Covered in the Report |

Component, Technology Type, Vehicle Type, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Nissan Motor Co., Ltd., Nuvve Holding Corp., Enel X S.r.l., ABB Ltd., Siemens AG, Schneider Electric SE, Bayerische Motoren Werke AG (BMW Group), Ford Motor Company, Mitsubishi Motors Corporation, Toyota Motor Corporation, Honda Motor Co., Ltd., Hitachi, Ltd. |

|

Customization |

Available upon request |

Vehicle-to-Grid Technology Market Segmentation

By Component

Electric Vehicles (EVs) is the largest category with a market share of about 40% in 2025, due to the increasing global adoption of electric vehicles which serve as the primary energy storage units in Vehicle-to-Grid systems. The growing number of EVs provides a large, distributed battery network that can supply power back to the grid when required. Governments are supporting EV adoption through incentives and emission regulations, which directly increases the installed base of V2G-capable vehicles. Automakers are also introducing models with bidirectional charging capability, further strengthening the dominance of this segment.

Software & Energy Management Systems is the fastest-growing category with a CAGR of 24.7% during the forecast period, due to the rising need for advanced grid communication, monitoring, and control platforms. V2G networks require intelligent software to manage energy flow between vehicles, charging stations, and utilities. The expansion of smart grids and digital energy platforms is increasing demand for sophisticated management systems. Utilities and technology providers are investing heavily in AI-based and cloud-based energy control solutions, accelerating growth in this segment.

By Technology Type

Bidirectional V2G Technology is the largest category with a market share of about 65% in 2025, due to its ability to both draw electricity from the grid and return stored power back when demand rises. This two-way energy flow provides higher efficiency and better grid support compared to unidirectional charging. Utilities prefer bidirectional systems for peak load management and renewable energy balancing. Increasing deployment of smart grids and advanced chargers is further strengthening the dominance of bidirectional V2G technology.

Unidirectional V2G (Smart Charging) Technology is the fastest-growing category with a CAGR of 24.8% during the forecast period, due to its lower cost and easier implementation compared to fully bidirectional systems. Many regions are adopting smart charging as an initial step toward full V2G deployment. It allows utilities to control charging time and reduce peak demand without complex infrastructure. Developing countries and early-stage EV markets are increasingly adopting this technology, supporting rapid growth.

By Vehicle Type

Battery Electric Vehicles (BEV) is the largest category with a market share of about 70% in 2025, due to the higher battery capacity and full electric architecture that makes BEVs more suitable for V2G applications. Governments worldwide are strongly promoting BEVs to reduce emissions, which is increasing their share in the EV fleet. BEVs can store more energy compared to hybrid vehicles, making them ideal for grid support. Automakers are also focusing on BEV platforms with built-in bidirectional charging compatibility.

Plug-in Hybrid Electric Vehicles (PHEV) is the fastest-growing category with a CAGR of 24.9% during the forecast period, due to their flexibility of operating on both electric power and fuel, which encourages adoption in regions where charging infrastructure is still developing. PHEVs provide an entry point for V2G participation while reducing range anxiety for users. Increasing consumer acceptance and government incentives for hybrid vehicles are supporting growth in this segment.

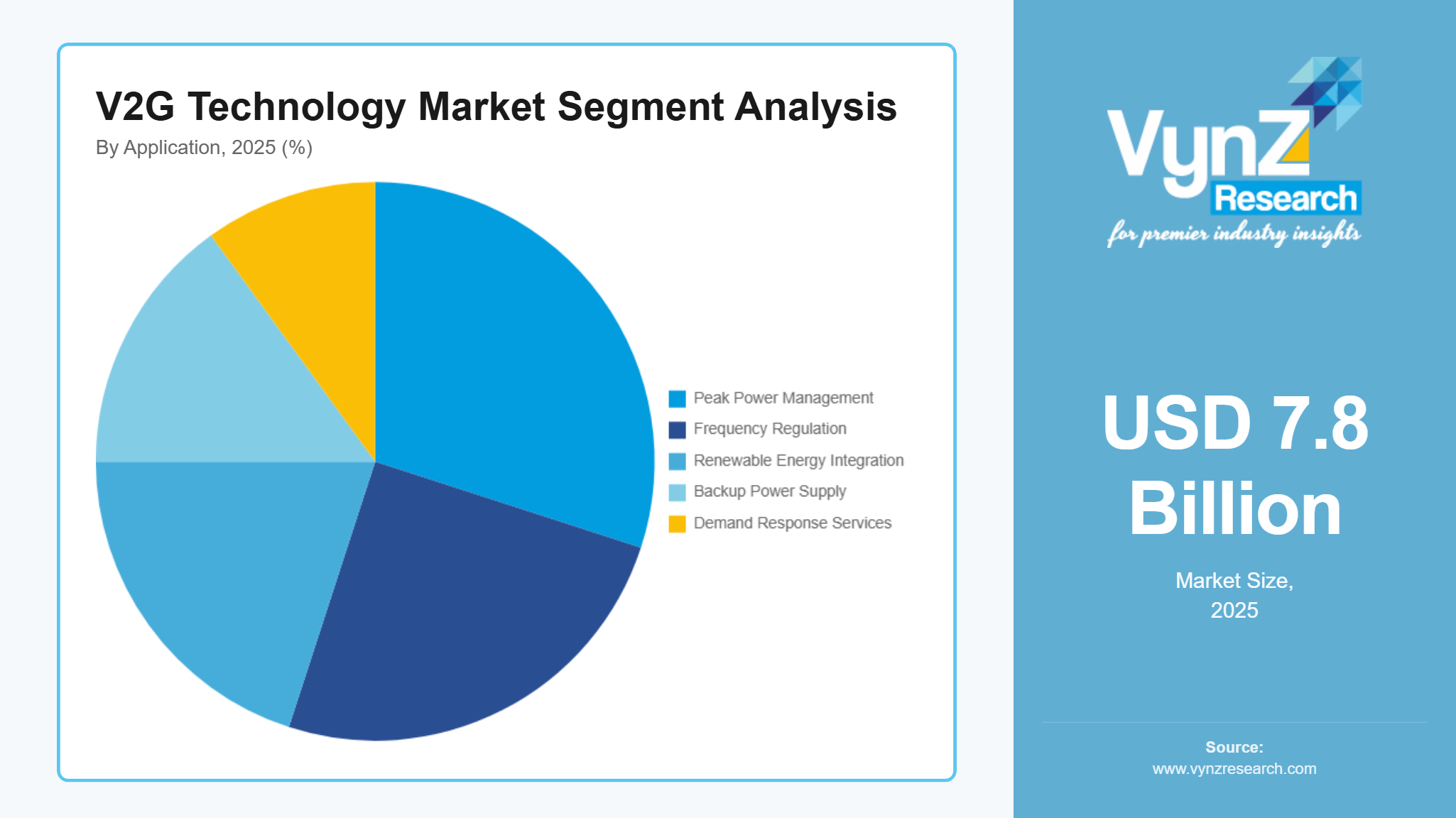

By Application

Peak Power Management is the largest category with a market share of about 30% in 2025, due to the increasing need for balancing electricity demand during high-consumption periods. Utilities use V2G-enabled vehicles as distributed storage to supply power back to the grid during peak hours, reducing pressure on power plants. Rising electricity demand in urban areas is increasing the importance of peak load control. This makes peak power management the most widely used application of V2G technology.

Renewable Energy Integration is the fastest-growing category during the forecast period, due to the rapid expansion of solar and wind power projects worldwide. Renewable energy generation is variable, creating the need for flexible storage solutions such as V2G. Electric vehicles can store excess renewable power and release it when generation drops. Governments focusing on decarbonization and clean energy targets are accelerating the growth of this application.

By End User

Utilities / Grid Operators is the largest category with a market share of about 40% in 2025, due to the direct role of utilities in managing electricity distribution and maintaining grid stability. V2G technology helps utilities reduce peak load, improve reliability, and integrate renewable energy sources. Many V2G pilot projects are led by power companies and grid operators. Investments in smart grid infrastructure are further increasing utility adoption of V2G systems.

Commercial is the fastest-growing category during the forecast period, due to the rapid electrification of commercial fleets such as buses, delivery vehicles, and corporate transport. Fleet operators can use V2G to reduce energy costs and generate additional revenue by supplying power to the grid. Businesses are also adopting V2G to support sustainability goals and energy management strategies. Increasing deployment of fleet charging hubs is accelerating growth in this segment.

Regional Insights

North America

North America is the largest regional market for vehicle-to-grid (V2G) technology, supported by strong electric vehicle adoption, advanced smart grid infrastructure, and favorable government policies promoting clean energy integration. The United States leads the region with multiple V2G pilot projects led by utilities, automakers, and research institutions focused on grid balancing and renewable energy storage. Federal and state-level incentives for electric vehicles, along with investments under clean energy and infrastructure programs, are accelerating the deployment of bidirectional charging systems. Canada is also investing in smart grid modernization and EV charging networks to support future V2G applications. The U.S. government launched the $1.32 billion Charging and Fueling Infrastructure Grant Program to expand EV charging networks, supporting grid integration and the development of Vehicle-to-Grid (V2G) technology. The presence of major technology providers, automotive companies, and energy utilities enables faster commercialization of V2G solutions. In addition, growing renewable energy capacity in wind and solar energy is increasing the need for flexible storage systems, strengthening regional demand. Strong regulatory support and early adoption of advanced energy management technologies continue to maintain North America’s leadership in the V2G market.

Asia Pacific

Asia-Pacific is the fastest-growing region in the vehicle-to-grid (V2G) technology market, driven by rapid electric vehicle adoption, expanding renewable energy projects, and large-scale investments in smart grid infrastructure. Countries such as China, Japan, South Korea, and India are aggressively promoting EV adoption through subsidies, production incentives, and emission reduction targets. China leads in EV production and charging infrastructure, creating a strong foundation for V2G deployment. Japan has been an early adopter of V2G technology, with several commercial and residential pilot programs integrating EVs with power grids. India is also investing in smart grid development and renewable energy expansion, which is expected to create future opportunities for V2G integration. India is targeting large-scale renewable deployment, with plans requiring over US$190–215 billion in renewable generation and additional investments in transmission and storage infrastructure to reach its long-term clean-energy capacity goals. The expansion of solar, wind, and hybrid power projects is expected to create strong demand for distributed energy storage solutions, including vehicle-to-grid technology. Rapid urbanization and rising electricity demand across the region are increasing the need for grid stability solutions. Government initiatives supporting clean energy transition and energy storage technologies continue to accelerate V2G market growth in Asia-Pacific.

Europe

Europe holds a significant share in the vehicle-to-grid (V2G) technology market due to strict carbon reduction targets, strong renewable energy penetration, and well-developed electric vehicle policies. The European Union is actively promoting smart energy systems and grid flexibility to support the transition toward a low-carbon economy. Countries such as the United Kingdom, Germany, France, and the Netherlands are running large-scale V2G demonstration projects involving utilities, automotive manufacturers, and research organizations. High adoption of wind and solar power in Europe has increased the need for energy storage and demand response solutions, making V2G an attractive option. Government incentives for EV purchases and charging infrastructure are further supporting the expansion of V2G-compatible vehicles. In addition, strong regulatory frameworks and collaboration between public and private sectors are accelerating technology standardization. Europe’s focus on sustainability and energy efficiency continues to drive steady growth in the V2G market.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is witnessing gradual growth in the vehicle-to-grid (V2G) technology market as electric vehicle adoption and renewable energy investments increase. In Latin America, countries such as Brazil and Mexico are expanding EV charging infrastructure and exploring smart grid technologies to improve energy reliability. The Middle East is investing in renewable energy projects, particularly solar power, which is creating future opportunities for V2G integration to manage power fluctuations. Countries like the United Arab Emirates and Saudi Arabia are also focusing on sustainable mobility and advanced energy systems as part of long-term diversification plans. In Africa, V2G adoption is still at an early stage, but increasing electrification programs and international funding for clean energy projects are expected to support future growth. Although infrastructure development is uneven across these regions, rising interest in energy storage, grid stability, and decarbonization is expected to drive steady market expansion.

Competitive Landscape / Company Insights

The Vehicle-to-Grid (V2G) technology market is moderately fragmented, with participation from automotive manufacturers, energy utilities, charging infrastructure providers, and software companies, all contributing to the development of bidirectional charging and smart grid integration solutions. Major automotive companies, including Nissan Motor Co., Ltd., Bay-mobilische Motoren Werke AG (BMW Group) and Ford Motor Company, are already working on V2G-accommodating electric vehicles and are relying on their large EV bases to support the widespread implementation of grid-integrated battery systems. Such businesses are interested in incorporating the capability of two-way charging in the direct vehicle platforms, which will enable EVs to serve as distributed energy storage devices.

Energy and power management firms like Nuvve Holding Corp., Enel X S.r.l. and ABB Ltd. are also important as they offer V2G platforms, grid services software and bidirectional charging systems that facilitate communication between vehicles and electricity systems. They can help utilities to integrate EV batteries into power grids effectively because of their knowledge on energy management systems, grid balancing and demand response solutions. The competition among the charging infrastructure providers such as Siemens AG and Schneider Electric SE takes the form of the smart charging stations, grid automation systems, and digital energy management platforms that facilitate the implementation of V2G at a large scale in commercial, residential, and utility uses.

Mini Profiles

Nissan Motor Co., Ltd. is a pioneer in Vehicle-to-Grid technology, developing bidirectional charging-enabled electric vehicles and participating in multiple global V2G pilot projects that integrate EV batteries with smart grid systems.

Nuvve Holding Corp. provides advanced V2G platforms and aggregation software that enables electric vehicles to store energy and return it to the grid, supporting demand response, grid stabilization, and renewable energy integration.

Enel X S.r.l. offers smart charging infrastructure and energy management solutions, focusing on V2G-enabled networks that allow utilities and fleet operators to optimize electricity usage and participate in energy trading programs.

ABB Ltd. develops bidirectional EV chargers, grid automation technologies, and digital energy management systems that support large-scale deployment of Vehicle-to-Grid infrastructure across commercial and utility applications.

Siemens AG provides smart grid platforms, EV charging systems, and power management software that enable integration of electric vehicles with modern electricity networks for improved grid stability and efficiency.

Key Players

- Nissan Motor Co., Ltd.

- Nuvve Holding Corp.

- Enel X S.r.l.

- ABB Ltd.

- Siemens AG

- Schneider Electric SE

- Bayerische Motoren Werke AG (BMW Group)

- Ford Motor Company

- Mitsubishi Motors Corporation

- Honda Motor Co., Ltd.

- Toyota Motor Corporation

- Hitachi, Ltd.

Recent Developments

January 2026 – Nuvve Holding Corp. announced the expansion of its Vehicle-to-Grid platform in partnership with multiple U.S. utility providers to support large-scale EV fleet integration for grid stabilization and demand response services.

December 2025 – Nissan Motor Co., Ltd. introduced an upgraded bidirectional charging system for its electric vehicle lineup, enabling improved Vehicle-to-Grid compatibility and enhanced energy sharing between vehicles and power networks.

October 2025 – Enel X S.r.l. launched a new smart charging and V2G management platform designed to help commercial fleet operators optimize energy usage and participate in electricity market trading programs.

September 2025 – ABB Ltd. unveiled a next-generation bidirectional DC fast charger that supports Vehicle-to-Grid applications, allowing electric vehicles to store renewable energy and supply power back to the grid during peak demand.

July 2025 – Siemens AG announced a collaboration with European grid operators to deploy smart grid software integrated with V2G-enabled charging stations, aimed at improving renewable energy balancing across urban power networks.

May 2025 – Ford Motor Company expanded its vehicle-to-home and vehicle-to-grid capabilities in new electric truck models, allowing users to supply stored battery power to homes, buildings, and utility grids during outages or peak load periods.

Global Vehicle-to-Grid Technology Market Coverage

Component Insight and Forecast 2026 - 2035

- Electric Vehicles (EVs)

- EV Charging Stations (Bidirectional Chargers)

- Smart Meters

- Software & Energy Management Systems

Technology Type Insight and Forecast 2026 - 2035

- Unidirectional V2G (V1G / Smart Charging)

- Bidirectional V2G

Vehicle Type Insight and Forecast 2026 - 2035

- Battery Electric Vehicles (BEV)

- Plug-in Hybrid Electric Vehicles (PHEV)

- Fuel Cell Electric Vehicles (FCEV)

Application Insight and Forecast 2026 - 2035

- Peak Power Management

- Frequency Regulation

- Renewable Energy Integration

- Backup Power Supply

- Demand Response Services

End User Insight and Forecast 2026 - 2035

- Residential

- Commercial

- Industrial

- Utilities / Grid Operators

Global Vehicle-to-Grid Technology Market by Region

- North America

- By Component

- By Technology Type

- By Vehicle Type

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Technology Type

- By Vehicle Type

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Technology Type

- By Vehicle Type

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Technology Type

- By Vehicle Type

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Vehicle-to-Grid Technology Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Technology Type

1.2.3. By

Vehicle Type

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Electric Vehicles (EVs)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. EV Charging Stations (Bidirectional Chargers)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Smart Meters

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Software & Energy Management Systems

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Technology Type

5.2.1. Unidirectional V2G (V1G / Smart Charging)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Bidirectional V2G

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Vehicle Type

5.3.1. Battery Electric Vehicles (BEV)

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Plug-in Hybrid Electric Vehicles (PHEV)

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Fuel Cell Electric Vehicles (FCEV)

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Peak Power Management

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Frequency Regulation

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Renewable Energy Integration

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Backup Power Supply

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Demand Response Services

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Residential

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Utilities / Grid Operators

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Technology Type

6.3. By

Vehicle Type

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Technology Type

7.3. By

Vehicle Type

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Technology Type

8.3. By

Vehicle Type

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Technology Type

9.3. By

Vehicle Type

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Nissan Motor Co., Ltd.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Nuvve Holding Corp.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Enel X S.r.l.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

ABB Ltd.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Siemens AG

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Schneider Electric SE

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Bayerische Motoren Werke AG (BMW Group)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Ford Motor Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Mitsubishi Motors Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Honda Motor Co., Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Toyota Motor Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Hitachi, Ltd.

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Vehicle-to-Grid Technology Market