Conformal Coating Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Material Type (Acrylic, Silicone, Epoxy, Polyurethane, Parylene, Fluoropolymer), by Application Method (Brush Coating, Spray Coating, Dip Coating, Selective Coating, Chemical Vapor Deposition (CVD)), by End-Use Industry (Consumer Electronics, Automotive, Aerospace & Defense, Industrial, Healthcare / Medical Devices, Telecommunications), by Curing Process (UV-Curable, Thermal Cure, Moisture Cure)

| Status : Published | Published On : Mar, 2026 | Report Code : VRCH2129 | Industry : Chemicals & Materials | Available Format :

|

Page : 190 |

Conformal Coating Market Overview

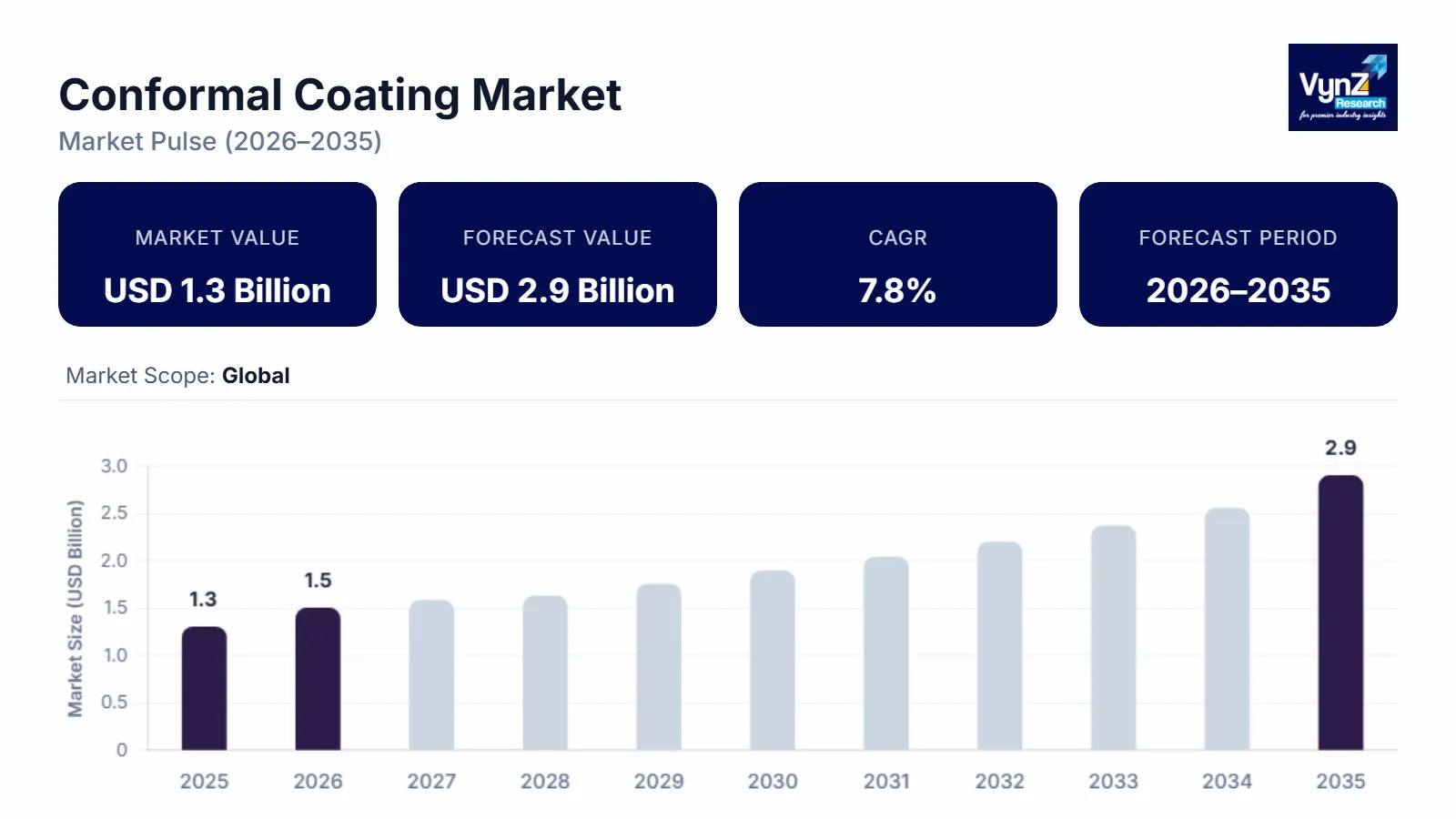

The conformal coating market which was valued at approximately USD 1.3 billion in 2025 and is estimated to reach around USD 1.5 billion in 2026, is projected to reach close to USD 2.9 billion by 2035, expanding at a CAGR of about 7.8% during the forecast period from 2026 to 2035.

The conformal coating market is primarily driven by the rapid growth of the electronics and semiconductor industries, where protection of printed circuit boards (PCBs) against moisture, dust, chemicals, and temperature fluctuations is essential for long-term reliability. The rising need of miniature and high-performance electronic appliances in car, consumer electronics, aerospace, and industrial applications is driving the use of sophisticated coating solutions to a faster rate. The growth of electric vehicles (EVs) and superior driver-assistance technologies (ADAS) also positively impact demand because these technologies demand increased environmental safety of vulnerable electronic components. Moreover, the introduction of the IoT and 5G networks is providing the demand of robust and miniaturized electronic parts, which favors the use of coating. High level of product safety and durability regulations in all industries also promote growth of the market. The introduction of UV-curing and silicone-based coating creates that enhance efficiency and shorten processing time is increasing in popularity due to the application of new technology. In addition, the increasing investments in the production of electronic in the Asia-Pacific region are enhancing capacity production, which further boosts the growth of the entire market.

Conformal Coating Market Dynamics

Market Trends

Miniaturization of electronic components is a major trend shaping the conformal coating market, as modern devices are becoming smaller, lighter, and more functionally dense. Increased risk of short circuit, corrosion, and thermal stress is caused by the utilization of multi-component circuit boards (high-density PCB) that now occupy limited areas. In July 2025, KONIG announced the launch of the KP400 3D Digital Packaging Solution, an advanced conformal coating system designed to improve precision, speed, and material efficiency in electronic manufacturing. The KP400 system focuses on high-density electronics and supports improved protection performance for complex PCB assemblies. With the tightening of the component spacing, exposure to the moisture, dust or even the chemical can severely affect the performance and reliability. Conformal coatings offer a thin uniform protective coating that protects complex circuitry without affecting electrical performance. Increasing demand of miniature consumer electronics, wearable devices, medical equipments and sophisticated automotive systems are driving this trend up. As well, small-scale electronics employed in IoT and 5G infrastructure need to be made more durable in a variety of operating conditions. This has seen manufacturers invest in precise coating technologies that deliver effective coverage without compromising on product performance and our product life.

Growth Drivers

The conformal coating market is experiencing significant growth due to expansion in consumer electronics manufacturing because the world is constantly buying smart phones, laptops, tablets, gaming consoles and wearable devices. The growing volumes of production demand a greater level of protection of the printed circuit boards (PCBs) to achieve their durability and high reliability. Actnano, Inc. secured a $40 million investment from Anthelion Capital, which the company plans to use to expand its production capacity, technical service support, and global footprint for its Advanced nanoGUARD water- and environmental-resistant nanocoating technology used in protecting electronics. Protective coatings are often necessary because consumer devices are often subjected to moisture, dust, temperature fluctuations and unintentional spillage. With the continued thinness and smaller size of electronics, the probability of short circuits and corrosion is growing, further enhancing the use of conformal coating. India’s India Semiconductor Mission 2.0 with an estimated outlay of ₹1.25 lakh crore aims to build a domestic semiconductor and display ecosystem, including ATMP (Assembly, Testing, Marking & Packaging) units that rely on conformal coating processes as part of component protection. Moreover, the quick pace of product innovation compels the manufacturers to use modern state of the art coating technologies to accommodate high speed production. The emerging markets are also leading to increased consumption of electronics which increases production

Market Restraints / Challenges

Complex application and rework procedures represent a significant challenge in the conformal coating market due to the precision required during the coating process. The precise coverage of tightly packed and reduced-sized PCBs requires sophisticated equipment and operators making the operation much more intricate. Connectors and other vital parts are then selectively masked, which further increases the steps to be put in place thus making the process time consuming. In addition, inappropriate use can cause defects in coating like bubbles, irregular coating thickness or even incomplete coating, which can affect the reliability of the product. Refinishing coated boards is also not an easy task, because it needs complex solvents or mechanical processes to remove the protective layer without destroying components beneath. This makes them costly in terms of time and money in terms of maintenance and production. Such complexities in high-volume manufacturing environments may slack throughput and efficiency. Subsequently, manufacturers will be forced to invest in automation and quality control measures to reduce errors and provide uniform performance.

Market Opportunities

Growth in 5G infrastructure and IoT gadgets can build a huge growth potential in the conformal coating market as international connectivity develops at an alarming pace. Installation of 5G base stations, small cells, routers and network equipments demand very high reliable electronic assemblies that can be used in various environmental conditions. The systems tend to be subjected to moisture, changes in temperatures as well as external pollution, necessitating protective finishes that are durable. Meanwhile, the IoT devices have permeated smart homes, industrial automation, healthcare and smart cities, which are increasing the manufacture of smaller and sensitive electronic components. Under the CHIPS program, the U.S. Department of Commerce announced up to $300 million in funding for advanced semiconductor packaging research projects across states like Georgia, California, and Arizona. Since IoT devices are often remote operated or work under harsh conditions, long-term security is essential. Conformal coatings are used to avoid corrosion, short circuiting and performance losses to ensure stable connectivity and lifespan of the device. As the world continues to undergo digital transformation, with coating solutions becoming more demanded globally, the demand of sophisticated coating solutions is set to go up as time goes by.

Global Conformal Coating Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.3 Billion |

|

Revenue Forecast in 2035 |

USD 2.9 Billion |

|

Growth Rate |

7.8% |

|

Segments Covered in the Report |

Material Type, Application Method, End-Use Industry, Curing Process, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Henkel AG & Co. KGaA, Dow Inc., Shin-Etsu Chemical Co., Ltd., H.B. Fuller Company, Chase Corporation, Dymax Corporation, ALTANA AG (ELANTAS GmbH), MG Chemicals, Specialty Coating Systems, Inc., PPG Industries, Inc., Electrolube (MacDermid Alpha Electronics Solutions), KISCO Ltd. |

|

Customization |

Available upon request |

Conformal Coating Market Segmentation

By Material Type

Acrylic is the largest category with a market share of about 30% in 2025, because it is cost-effective, endures easily, and has properties of high moisture resistance. It finds a lot of applications in consumer electronics and industrial use due to its rapid dry-out period and easy rework nature. Acrylic coating is a sure environmental cover and does not affect electrical insulation quality. Their suitability to many applications methods also enhances their adoption. Their wide usage is supported by the high availability and well-established manufacturing infrastructure. The high-volume electronics production has ensured that it maintains its leading position in the world.

Parylene is the fastest-growing category during the forecast period, due to their high dielectric strength and consistent vapor-deposited coverage. It provides outstanding moisture resistance, chemical resistance and extreme temperature resistance and it is best suited to aerospace, medical and high-reliability electronics. Further miniaturization of components increases the needs in thin and highly conformal protective layers. Advanced automotive and defense electronics is growing, which promotes adoption. It can coat intricate geometries without pinholes thus increasing long-term reliability. Growing attention to high-quality electronics promotes high growth trend.

By Application Method

Spray Coating is the largest category with a market share of about 30% in 2025, due to its flexibility, cost-effectiveness and ability to produce at large scale production. It enables fast coverage of complicated PCB assemblies and is commonly used in the production of consumer electronics. The approach promotes both manual and automated operations, enhancing the flexibility of operations. The fact that it is easy to fit within the already available production lines also contributes to its popularity. The market share of the product is reinforced by high throughput and comparatively low capital investment. The wide applicability in any industry upholds its top position.

Selective Coating is the fastest-growing category with a CAGR of 8.1% during the forecast period, due to the rising demand in precision and less material wasted. It allows precise application to PCB regions without a masking effect enhancing efficiency. Integration of automation increases consistency and repeatability in the manufacturing of high volumes. The increasing trends of miniaturization need specific coating solutions, which makes its use gain momentum. Manufacturers are emphasizing on the enhancement of productivity and minimization of operational errors. This change of smart manufacturing helps in quick development.

By End-Use Industry

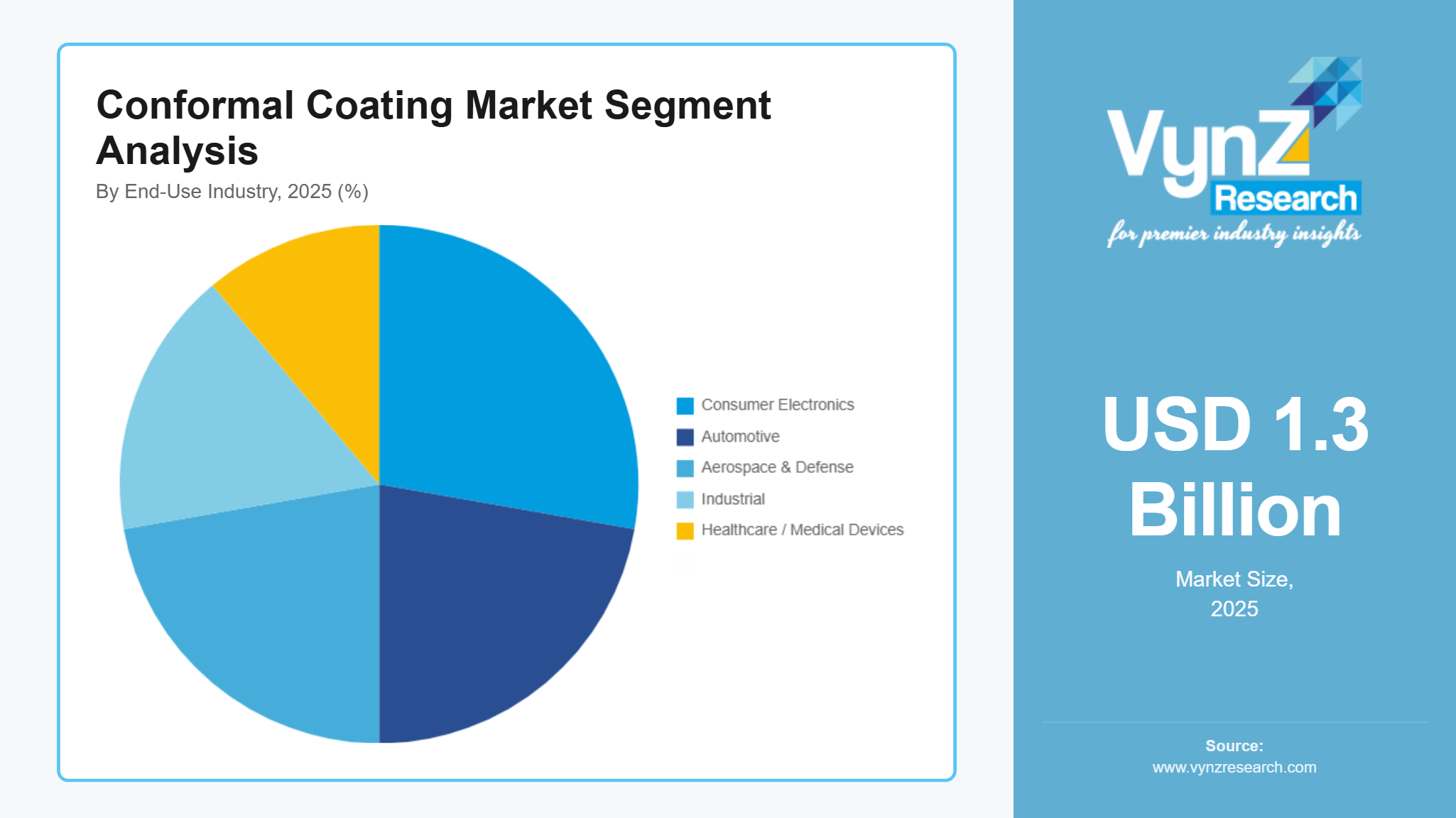

Consumer electronics is the largest category with a market share of about 25% in 2025, owing to the colossal production of smartphones, laptops, tablets and wearable devices all over the world. Continuous protection of PCB is due to high product turnover and innovation cycles. The size reduction in electronics makes it more susceptible to moisture and corrosion, which enhances the use of coating. The high concentration of the manufacturing centers in the Asia-Pacific promotes mass consumption. The increasing number of middle classes and the increasing digitalization also increase demand. Maintaining its dominance is done through large distribution networks.

Automotive is the fastest-growing category with a CAGR of 7.9% during the forecast period, driven by the fast growth of the electric vehicles and the advanced driver-assistance systems. The growth of electronic content in each vehicle may largely increase the requirement of PCB protection. The components should be able to tolerate vibration, heat, and adverse weather conditions. Additional coating needs are generated in EV battery management systems and power electronics. The vehicle safety is increased because of the regulatory concern on the quality of the vehicles. Smart mobility is technologically advanced, and this aspect drives robust growth.

By Curing Process

Thermal Cure is the largest category with a market share of about 40% in 2025, since they are still popular in the conventional production of electronics. It provides good adhesiveness, strength, and a variety of coating materials. It has established curing infrastructure in manufacturing facilities that helps to enhance its dominance. Thermal curing offers good mechanical and chemical protection. It is especially in the industrial and automotive use. Its leading share is sustained by long-term familiarity in the industry.

UV-Curable is the fastest-growing category during the forecast period, due to the shorter processing time and higher production efficiency. It saves a lot of time in curing as opposed to the traditional ways. The reduced energy consumption and throughput is helpful to manufacturers. The UV technology also facilitates ecologically friendly formulations that exhibit less VOC emissions. Electronics manufacturing is increasingly becoming automated, which enhances its usage. The increased emphasis on cost optimization and sustainability enhances the rapid growth.

Regional Insights

North America

North America holds a significant share in the conformal coating market, supported by strong presence of advanced electronics, aerospace, and automotive manufacturing industries. Canada and the United States are established in the production of PCB and high uptake of technology in protective coating to ensure high reliability levels. Regional demand is being enhanced by increasing investments in electric vehicles, defense electronics and 5G infrastructure. Its location is advantageous with developed automation in coating processes and excellent R&D. The CHIPS and Science Act is a major federal investment to strengthen U.S. semiconductor research, manufacturing, and packaging infrastructure with roughly $280 billion in funding, including $39 billion in direct subsidies for chip manufacturing and $11 billion for semiconductor R&D. Growth has been driven through better emphasis on innovation by high-performance and UV-curable coating. Tough environmental and health policies promote the use of compliant materials which have low VOC. Moreover, the increase in demand of the durable medical and industrial electronics also continues to support stable regional growth.

Asia Pacific

Asia-Pacific is the largest and fastest-growing region in the conformal coating market, driven by large-scale electronics manufacturing in countries such as China, Japan, South Korea, and India. The area is a manufacturing center of consumer electronics and semiconductor which generates enormous demand in PCB protection solutions. Asia-Pacific is projected to require approximately 17,720 new passenger and freighter aircraft, driven by population growth and rising air travel demand. Cargo traffic in the region is expected to grow at around 3.7% annually, leading to a doubling of air freight volumes by 2040. The increasing disposable incomes and rapid urbanization is increasing the degree of electronics consumption in the emerging economies. Increase in the production of electric vehicles and telecommunication infrastructure continues to propagate growth. The supply chains are enhanced by government programs that favor the local production of electronics. The Government of India approved projects worth over ₹5,500 crore (~USD ~660 million) under the Electronics Manufacturing Component Scheme (ECMS), aimed at boosting domestic production of printed circuit boards and high-value components that underpin electronics assembly — a sector that drives demand for conformal coatings. Production capacity is increased with cost-effective labor and powerful component ecosystems. The active development of the region is driven by the active use of technologies and export-driven

Europe

Europe represents a technologically advanced and quality-focused market, characterized by strong automotive, aerospace, and industrial automation sectors. Germany, France, and the United Kingdom are the countries that focus on the electronic components’ high reliability standards. Increasing demand in silicone and parylene coating is evident in the automotive electronics and defence business in the region. Green coating formulations are being adopted due to the sustainability efforts and environmental compliance policies. Further manufacturing technology and automation system embarkation assist accuracy in the coating application. New demand opportunities are being generated by growth in electric mobility and renewable energy systems. Also, there are robust R&D investments that are promoting high-performance material innovation.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is witnessing gradual growth in the Conformal Coating Market. Regional demand is being aided by growing industrialization and growth in the number of electronics assembly processes. Brazil and Mexico are some of the countries in Latin America that are boosting the production of automotive and industrial electronics. In the Middle East, telecom infrastructure and smart city projects are being pursued, which increases the requirements of PCB protection. African markets are slowly turning to consumer of electronics with the urbanization and digitalization. The manufacturing capability is improving with foreign investments and modernization programs even though the problem of infrastructure and technical expertise gaps is still experienced in some regions. The rising telecommunications and industrial industries are likely to sustain the growth of the region in the long term.

Competitive Landscape / Company Insights

The conformal coating market is moderately consolidated, characterized by the presence of global specialty chemical manufacturers alongside regional coating solution providers and niche technology firms. Major player firms like Henkel AG & Co. KGaA, H.B. Fuller Company and Chase Corporation stand at a good position due to diversified product lines which comprise acrylic, silicone, polyurethane and UV-curable coating. These players are using the large distribution channels, technical service capabilities, and long-term association with the electronics manufacturers to reinforce their presence in the market.

Large material science firms like Dow Inc. and Shin-Etsu Chemical Co., Ltd. have a major role in conformal coatings based on silicone especially in high-temperature and automotive applications. At the same time, Electrolube (MacDermid Alpha Electronics Solutions) and Dymax Corporation are also interested in high performance and UV-curable technologies, with their application being precision electronics and automated manufacturing problems. The increasing trend is the investment of companies in more eco-friendly, low-VOC formulations and automation-compatible coating systems to fulfill the regulatory requirements and efficiency needs.

Mini Profiles

Henkel AG & Co. KGaA is a leading global provider of specialty adhesives and electronic materials, including a wide portfolio of conformal coatings under its advanced materials division. The company offers acrylic, silicone, and UV-curable coatings designed for automotive, consumer electronics, and industrial applications.

Dow Inc. is a major materials science company with strong expertise in silicone-based conformal coatings for high-performance electronics. Its products are widely used in automotive electronics, power modules, and industrial control systems due to superior thermal stability and moisture resistance

Shin-Etsu Chemical Co., Ltd. is a prominent supplier of silicone materials, including advanced conformal coatings for automotive, telecommunications, and semiconductor applications. The company is recognized for high-purity and high-reliability silicone technologies that enhance long-term PCB protection.

Chase Corporation specializes in protective materials and conformal coating solutions tailored for printed circuit boards and electronic assemblies. The company offers acrylic, urethane, and silicone coatings designed for industrial, aerospace, and defense applications.

Key Players

- Henkel AG & Co. KGaA

- H.B. Fuller Company

- Dow Inc.

- Shin-Etsu Chemical Co., Ltd.

- Chase Corporation

- Dymax Corporation

- Electrolube (MacDermid Alpha Electronics Solutions)

- MG Chemicals

- ALTANA AG (ELANTAS GmbH)

- KISCO Ltd.

- Specialty Coating Systems, Inc.

- PPG Industries, Inc.

Recent Developments

January 2026 – Henkel AG & Co. KGaA announced the expansion of its advanced electronic materials portfolio with new UV-curable conformal coatings designed for high-density automotive and EV power electronics applications, focusing on faster curing cycles and improved thermal resistance.

December 2025 – Dow Inc. introduced a next-generation silicone-based conformal coating formulated for enhanced moisture resistance and long-term durability in 5G infrastructure and industrial control systems, strengthening its high-performance materials segment.

October 2025 – Shin-Etsu Chemical Co., Ltd. expanded its production capacity for specialty silicone conformal coatings in Asia-Pacific to support rising demand from semiconductor and automotive electronics manufacturers.

August 2025 – Dymax Corporation launched an advanced light-curable conformal coating compatible with automated selective dispensing systems, aimed at improving manufacturing efficiency and reducing material waste in high-volume PCB assembly lines.

June 2025 – Chase Corporation announced the development of a low-VOC, environmentally compliant acrylic conformal coating targeting aerospace and defense applications, aligning with evolving global environmental and safety regulations.

Global Conformal Coating Market Coverage

Material Type Insight and Forecast 2026 - 2035

- Acrylic

- Silicone

- Epoxy

- Polyurethane

- Parylene

- Fluoropolymer

Application Method Insight and Forecast 2026 - 2035

- Brush Coating

- Spray Coating

- Dip Coating

- Selective Coating

- Chemical Vapor Deposition (CVD)

End-Use Industry Insight and Forecast 2026 - 2035

- Consumer Electronics

- Automotive

- Aerospace & Defense

- Industrial

- Healthcare / Medical Devices

- Telecommunications

Curing Process Insight and Forecast 2026 - 2035

- UV-Curable

- Thermal Cure

- Moisture Cure

Global Conformal Coating Market by Region

- North America

- By Material Type

- By Application Method

- By End-Use Industry

- By Curing Process

- By Country - U.S., Canada, Mexico

- Europe

- By Material Type

- By Application Method

- By End-Use Industry

- By Curing Process

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Material Type

- By Application Method

- By End-Use Industry

- By Curing Process

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Material Type

- By Application Method

- By End-Use Industry

- By Curing Process

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Conformal Coating Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Material Type

1.2.2. By

Application Method

1.2.3. By

End-Use Industry

1.2.4. By

Curing Process

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Material Type

5.1.1. Acrylic

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Silicone

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Epoxy

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Polyurethane

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Parylene

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Fluoropolymer

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Application Method

5.2.1. Brush Coating

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Spray Coating

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Dip Coating

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Selective Coating

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Chemical Vapor Deposition (CVD)

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By End-Use Industry

5.3.1. Consumer Electronics

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Automotive

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Aerospace & Defense

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Industrial

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Healthcare / Medical Devices

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Telecommunications

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Curing Process

5.4.1. UV-Curable

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Thermal Cure

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Moisture Cure

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Material Type

6.2. By

Application Method

6.3. By

End-Use Industry

6.4. By

Curing Process

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Material Type

7.2. By

Application Method

7.3. By

End-Use Industry

7.4. By

Curing Process

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Material Type

8.2. By

Application Method

8.3. By

End-Use Industry

8.4. By

Curing Process

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Material Type

9.2. By

Application Method

9.3. By

End-Use Industry

9.4. By

Curing Process

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Henkel AG & Co. KGaA

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

H.B. Fuller Company

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Dow Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Shin-Etsu Chemical Co., Ltd.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Chase Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Dymax Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Electrolube (MacDermid Alpha Electronics Solutions)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

MG Chemicals

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

ALTANA AG (ELANTAS GmbH)

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

KISCO Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Specialty Coating Systems, Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

PPG Industries, Inc.

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Conformal Coating Market