Membrane Bioreactor Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Membrane Type (Hollow Fiber, Flat Sheet, Multi-Tubular), by Configuration (Submerged MBR, Side-Stream MBR), by Application (Municipal Wastewater Treatment, Industrial Wastewater Treatment), by Flow Rate Capacity (Small Capacity, Medium Capacity, Large Capacity)

| Status : Published | Published On : Feb, 2026 | Report Code : VRCH2128 | Industry : Chemicals & Materials | Available Format :

|

Page : 182 |

Membrane Bioreactor Market Overview

The membrane bioreactor market which was valued at approximately USD 4.2 billion in 2025 and is estimated to reach around USD 4.7 billion in 2026, is projected to reach close to USD 10.7 billion by 2035, expanding at a CAGR of about 9.5% during the forecast period from 2026 to 2035.

This market is primarily driven by the rising need for advanced wastewater treatment solutions due to rapid urbanization, industrialization, and stricter environmental regulations. Increasing water scarcity is pushing municipalities and industries to adopt water reuse and recycling systems, where MBR technology offers high-quality effluent and compact plant design. Growing investments in municipal wastewater infrastructure, especially in emerging economies, are further supporting demand. Additionally, the ability of MBR systems to reduce sludge production and operating footprint compared to conventional treatment methods is accelerating adoption across industrial and residential sectors.

Membrane Bioreactor Market Dynamics

Market Trends

Advancements in membrane technology and digital integration are shaping the MBR market by making treatment systems more efficient, reliable, and cost-effective. Newer membrane materials with improved fouling resistance and longer lifespans help reduce maintenance needs and downtime, while innovations in energy-efficient designs lower overall operating costs. Similarly, digital tools such as automation, real-time monitoring, and smart control systems are being integrated into MBR plants to optimize performance, enable predictive maintenance, and improve process stability. Under Namami Gange Programme-II, the government committed ₹22,500 crore until 2026 for river cleanup and associated wastewater treatment works, including numerous sewage treatment plant (STP) projects — creating opportunities for advanced treatment technologies such as MBR to be deployed for higher-quality effluent and river pollution reduction.

Growth Drivers

Rising global water scarcity is a major growth driver for the Membrane Bioreactor (MBR) market, as increasing population, rapid urbanization, industrial expansion, and climate change continue to strain freshwater resources. The European Investment Bank committed €15 billion (about $17 billion) over 2025–2027 toward reducing water pollution, preventing wastage, and supporting innovative solutions in the water sector, including advanced treatment technologies that enable water reuse. According to the United Nations, nearly two-thirds of the global population could face water-stressed conditions in the coming decades, pushing governments and industries to prioritize wastewater recycling and reuse. MBR systems are highly suitable for water reuse applications because they produce high-quality treated effluent that can be safely reused for irrigation, industrial processes, and even potable reuse in advanced cases.

Market Restraints / Challenges

High initial capital investment is one of the major restraints in the Membrane Bioreactor (MBR) market, as the installation of MBR systems requires significant upfront expenditure compared to conventional wastewater treatment technologies. The cost of advanced membrane modules, aeration systems, control units, and civil infrastructure makes project implementation financially intensive, particularly for small municipalities and cost-sensitive industries. In addition, the need for skilled design, engineering, and integration further increases capital requirements. Although MBR systems offer long-term operational benefits such as better effluent quality and reduced footprint, the higher initial investment often delays adoption, especially in developing regions with limited infrastructure budgets.

Market Opportunities

Industrial wastewater treatment in emerging economies presents a significant growth opportunity for the Membrane Bioreactor (MBR) market, driven by rapid industrialization, urban expansion, and tightening environmental regulations. Countries across Asia-Pacific, Latin America, and parts of Africa are witnessing strong growth in sectors such as chemicals, pharmaceuticals, food & beverages, textiles, and power generation, all of which generate high volumes of complex effluents. Governments in these regions are increasingly enforcing stricter discharge norms and promoting zero-liquid-discharge (ZLD) practices to reduce environmental pollution and protect freshwater resources. MBR systems offer superior treatment efficiency, compact design, and high-quality effluent suitable for reuse, making them ideal for industrial applications where space constraints and water recovery are critical.

Global Membrane Bioreactor Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.2 Billion |

|

Revenue Forecast in 2035 |

USD 10.7 Billion |

|

Growth Rate |

9.5% |

|

Segments Covered in the Report |

Membrane Type, System Configuration, Application, Flow Rate Capacity |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

SUEZ Water Technologies & Solutions, Veolia Water Technologies & Solutions, Kubota Corporation, Evoqua Water Technologies LLC, Toray Industries, Inc., Mitsubishi Chemical Aqua Solutions, Inc., Koch Membrane Systems, Inc., Pentair plc, Ovivo Inc., Xylem Inc., DuPont de Nemours, Inc., Alfa Laval AB |

|

Customization |

Available upon request |

Membrane Bioreactor Market Segmentation

By Membrane Type

Hollow Fiber is the largest category with a market share of about 55% in 2025, due to their high packing density, cost efficiency, and widespread adoption in municipal wastewater treatment plants. These membranes offer a larger surface area per unit volume, making them highly suitable for large-scale treatment facilities where space optimization and operational efficiency are critical.

Flat sheet membranes are the fastest-growing category during the forecast period, due to their superior mechanical strength, durability, and lower fouling tendency. These membranes are increasingly preferred in industrial wastewater treatment applications where effluent characteristics are more complex and solids concentration is higher. Their ease of maintenance and longer operational life make them attractive in sectors such as pharmaceuticals, chemicals, and food processing, contributing to their accelerated adoption rate.

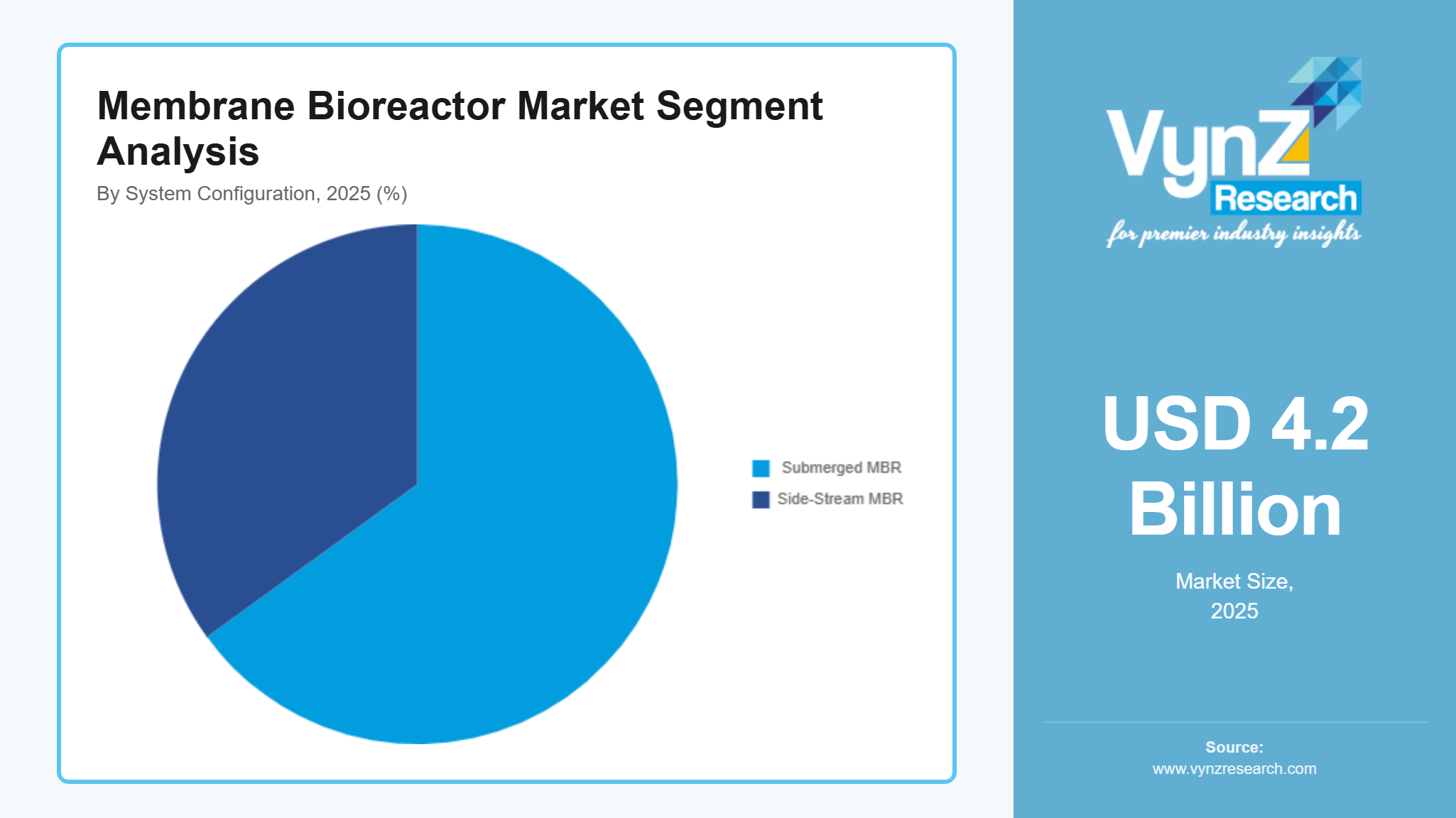

By System Configuration

Submerged MBR is estimated to account for approximately 65% of total market revenue in 2025. This is because they consume less energy compared to side-stream configurations and are widely deployed in municipal wastewater treatment facilities. Their simplified design, lower operating costs, and compatibility with large-capacity plants make them the preferred choice for urban sewage treatment projects worldwide.

Side-stream systems are experiencing the fastest growth rate at a CAGR of 9.6% in the coming years. This is due to their suitability for high-strength industrial wastewater. These systems offer better control over membrane cleaning and are capable of handling higher mixed liquor suspended solids (MLSS) concentrations. As industries adopt stricter discharge compliance measures and zero-liquid-discharge (ZLD) policies, demand for robust side-stream configurations is expected to increase.

By Application

Municipal wastewater treatment is the largest category, driven by large-scale public infrastructure investments, stricter environmental discharge standards, and increasing need for treated water reuse. Urban population growth and expansion of sewer networks continue to fuel demand for advanced treatment technologies in public utilities.

Industrial wastewater treatment is the fastest-growing category, due to tightening environmental regulations and rising adoption of water recycling in industrial operations. Sectors such as chemicals, pharmaceuticals, textiles, and food & beverages are increasingly implementing advanced treatment solutions to meet compliance standards and reduce freshwater consumption, thereby accelerating MBR adoption.

By Flow Rate Capacity

Large capacity MBR systems is the largest category with a market share of approx. 45% in 2025, this is due to extensive deployment in major municipal sewage treatment plants and industrial clusters. Rapid urbanization, population growth, and government-led infrastructure expansion programs are driving the installation of high-capacity treatment facilities. These systems are essential for handling large wastewater volumes in metropolitan cities and industrial zones.

Medium capacity systems are the fastest-growing category with a CAGR of 9.8% during the forecast period, this is supported by increasing adoption in mid-sized municipalities and expanding industrial facilities. Growing focus on decentralized wastewater treatment and water reuse projects in emerging economies is contributing to demand for medium-scale plants that balance operational efficiency and capital expenditure.

Regional Insights

Asia Pacific

Asia-Pacific is expected to register the fastest growth in the MBR market due to rapid urbanization, expanding industrial activities, and increasing government investments in wastewater infrastructure. The government of Uttar Pradesh unveiled an ambitious plan to promote sustainable water management by reusing treated wastewater, with a goal of achieving 50% reuse by 2030 and 100% reuse by 2035. Countries such as China and India are significantly increasing sewage treatment capacity to address rising environmental concerns and water scarcity challenges. Growing enforcement of wastewater discharge norms, coupled with rising adoption of water reuse practices in both municipal and industrial sectors, is accelerating MBR deployment. China aims to add 15 million cubic meters per day of reclaimed water capacity by 2025 under the 14th Five-Year Plan, reflecting a substantial expansion in wastewater reuse infrastructure. The government also targets a recycled water utilization rate of over 25% in water-scarce prefecture-level cities by 2025 to conserve freshwater and increase reuse.

Europe

Europe is characterized by stringent environmental directives and strong sustainability policies promoting circular water economy practices. The European Investment Bank (EIB) has committed €15 billion (~US$17 billion) from 2025 to 2027 to support projects aimed at reducing water pollution, improving wastewater infrastructure, preventing water wastage, and promoting innovation in water technologies across the EU funding that creates opportunities for advanced treatment solutions such as membrane systems. The European Union’s wastewater treatment and reuse regulations encourage adoption of advanced membrane technologies. Countries such as Germany, France, and the UK are investing in upgrading treatment plants to meet stricter discharge norms. Industrial sustainability commitments further strengthen market demand.

North America

North America holds the largest share in the Membrane Bioreactor (MBR) market due to its highly developed wastewater treatment infrastructure, strict environmental regulations, and early adoption of advanced membrane technologies. The United States and Canada have established regulatory frameworks under agencies such as the Environmental Protection Agency (EPA), which mandate high effluent discharge standards and promote water reuse initiatives. The U.S. federal infrastructure package (Bipartisan Infrastructure Law / IIJA) directs billions into water infrastructure including $11.7 billion specifically for the Clean Water State Revolving Fund (CWSRF), plus additional IIJA/CWSRF appropriations for emerging contaminants and other water projects money that states use for wastewater treatment plant upgrades. Additionally, significant investments in upgrading aging municipal treatment facilities and industrial wastewater systems support sustained demand for advanced MBR solutions. The Government of Canada announced a federal investment of over CAD 369.57 million (about USD 258 million) through the Canada Housing Infrastructure Fund (CHIF) to improve water and wastewater infrastructure across the country.

Rest of the World

The Rest of the World region, comprising Latin America and the Middle East & Africa, is witnessing gradual expansion in wastewater treatment infrastructure driven by urban development, regulatory reforms, and rising water sustainability concerns. In Latin America, countries such as Brazil and Mexico are focusing on expanding municipal sewage treatment capacity and reducing untreated wastewater discharge, while industrial compliance standards are steadily improving despite existing infrastructure gaps. Meanwhile, the Middle East & Africa region is primarily influenced by acute water scarcity and the growing need for wastewater reuse in irrigation, industrial applications, and urban development. Governments across countries such as Saudi Arabia and the UAE are actively integrating wastewater recycling into national water security strategies.

Competitive Landscape / Company Insights

The Membrane Bioreactor (MBR) market is moderately fragmented in nature, characterized by the presence of several global technology providers along with numerous regional and local manufacturers. While a few multinational companies dominate large-scale municipal wastewater treatment projects, especially in developed regions, many mid-sized and specialized firms actively compete in industrial and decentralized treatment segments. The market structure is influenced by technological differentiation, pricing strategies, and project-based competition. Additionally, regional players in Asia-Pacific and Europe contribute significantly to overall supply, preventing high market concentration.

Mini Profiles

SUEZ Water Technologies & Solutions provides advanced water and wastewater treatment solutions, including membrane bioreactor (MBR) systems, serving municipal and industrial clients worldwide with sustainable and high-performance treatment technologies.

Veolia Water Technologies & Solutions delivers integrated water, wastewater, and reuse solutions, offering innovative membrane filtration and biological treatment systems that support environmental compliance and circular water management globally.

Kubota Corporation develops flat-sheet membrane bioreactor systems widely used in municipal and industrial wastewater treatment, known for compact design, high treatment efficiency, and long operational reliability.

Evoqua Water Technologies LLC supplies advanced water and wastewater treatment systems, including membrane-based technologies, supporting municipal utilities and industrial facilities with reliable, compliant, and resource-efficient solutions.

Toray Industries, Inc. manufactures high-performance membrane materials and filtration systems, providing advanced separation technologies for municipal and industrial wastewater treatment applications worldwide.

Key Players

- SUEZ Water Technologies & Solutions

- Veolia Water Technologies & Solutions

- Kubota Corporation

- Evoqua Water Technologies LLC

- Toray Industries, Inc.

- Mitsubishi Chemical Aqua Solutions, Inc.

- Koch Membrane Systems, Inc.

- Pentair plc

- Ovivo Inc.

- Xylem Inc.

- DuPont de Nemours, Inc.

- Alfa Laval AB

Recent Developments

June 2024, SUEZ signed an agreement with VINCI Construction Grands Projects and the Serbian government to build a major wastewater treatment plant in Belgrade, aimed at improving effluent quality and protecting the Danube and Sava rivers, reflecting strategic expansion of its municipal wastewater infrastructure footprint.

May 2025, Veolia Water Technologies & Solutions announced $750 million worth of new flagship contracts across water technologies focused on energy and semiconductor markets, showcasing its leadership in advanced treatment projects and reinforcing its strategic positioning in wastewater and related solutions globally.

November 2025, Xylem partnered with Veolia to deploy AI-optimized membrane bioreactors with real-time IoT analytics across over 500 municipal wastewater plants worldwide, achieving significant operational efficiencies and energy savings — an example of digital transformation in advanced water treatment.

Global Membrane Bioreactor Market Coverage

Membrane Type Insight and Forecast 2026 - 2035

- Hollow Fiber

- Flat Sheet

- Multi-Tubular

Configuration Insight and Forecast 2026 - 2035

- Submerged MBR

- Side-Stream MBR

Application Insight and Forecast 2026 - 2035

- Municipal Wastewater Treatment

- Industrial Wastewater Treatment

Flow Rate Capacity Insight and Forecast 2026 - 2035

- Small Capacity

- Medium Capacity

- Large Capacity

Global Membrane Bioreactor Market by Region

- North America

- By Membrane Type

- By Configuration

- By Application

- By Flow Rate Capacity

- By Country - U.S., Canada, Mexico

- Europe

- By Membrane Type

- By Configuration

- By Application

- By Flow Rate Capacity

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Membrane Type

- By Configuration

- By Application

- By Flow Rate Capacity

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Membrane Type

- By Configuration

- By Application

- By Flow Rate Capacity

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Membrane Bioreactor Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Membrane Type

1.2.2. By

Configuration

1.2.3. By

Application

1.2.4. By

Flow Rate Capacity

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Membrane Type

5.1.1. Hollow Fiber

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Flat Sheet

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Multi-Tubular

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Configuration

5.2.1. Submerged MBR

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Side-Stream MBR

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Municipal Wastewater Treatment

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Industrial Wastewater Treatment

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Flow Rate Capacity

5.4.1. Small Capacity

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Medium Capacity

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Large Capacity

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Membrane Type

6.2. By

Configuration

6.3. By

Application

6.4. By

Flow Rate Capacity

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Membrane Type

7.2. By

Configuration

7.3. By

Application

7.4. By

Flow Rate Capacity

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Membrane Type

8.2. By

Configuration

8.3. By

Application

8.4. By

Flow Rate Capacity

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Membrane Type

9.2. By

Configuration

9.3. By

Application

9.4. By

Flow Rate Capacity

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

SUEZ Water Technologies & Solutions

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Veolia Water Technologies & Solutions

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Kubota Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Evoqua Water Technologies LLC

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Toray Industries, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Mitsubishi Chemical Aqua Solutions, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Koch Membrane Systems, Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Pentair plc

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Ovivo Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Xylem Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

DuPont de Nemours, Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Alfa Laval AB

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Membrane Bioreactor Market