Wastewater Treatment Plants Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Treatment Process (Primary Treatment, Secondary Treatment, Tertiary / Advanced Treatment), by Plant Type (Municipal Wastewater Treatment Plants, Industrial Wastewater Treatment Plants), by Technology (Biological Treatment, Chemical Treatment, Physical Treatment, Membrane Filtration Technology, Sludge Treatment & Management), by Capacity (Small Capacity Plants, Medium Capacity Plants, Large Capacity Plants), by Application (Residential / Municipal, Industrial), by End-Use Industry (Municipal Authorities, Industrial Facilities, Commercial Establishments)

| Status : Published | Published On : Feb, 2026 | Report Code : VRCH2127 | Industry : Chemicals & Materials | Available Format :

|

Page : 182 |

Wastewater Treatment Plants Market Overview

The wastewater treatment plants market which was valued at approximately USD 140.4 billion in 2025 and is estimated to reach around USD 155.6 billion in 2026, is projected to reach close to USD 308.2 billion by 2035, expanding at a CAGR of about 7.9% during the forecast period from 2026 to 2035.

This market is primarily driven by increasing urbanization and rapid industrialization, which are significantly raising the volume of municipal and industrial wastewater generated worldwide. Growing population levels and expanding cities are placing pressure on existing water infrastructure, necessitating the construction and modernization of treatment facilities. Stringent environmental regulations and government mandates aimed at reducing water pollution and protecting aquatic ecosystems are further accelerating investment in advanced treatment technologies. Rising concerns over water scarcity are encouraging wastewater recycling and reuse initiatives, especially in water-stressed regions. Industrial sectors such as chemicals, pharmaceuticals, food & beverages, and oil & gas are adopting on-site treatment solutions to comply with discharge standards. Additionally, public-private partnerships and infrastructure funding programs are supporting large-scale wastewater projects globally. Technological advancements in membrane filtration, biological treatment, and sludge management are improving efficiency and operational sustainability.

Waste Water Treatment Plants Market Dynamics

Market Trends

The increasing adoption of advanced treatment technologies is a major trend shaping the wastewater treatment plants market, as regulatory standards for effluent quality continue to become more stringent worldwide. Traditional primary and secondary treatment methods are often insufficient to remove emerging contaminants such as pharmaceuticals, microplastics, and heavy metals, driving demand for tertiary and advanced processes. Technologies such as membrane bioreactors (MBR), reverse osmosis (RO), ultraviolet (UV) disinfection, and advanced oxidation processes (AOP) are being widely implemented to enhance purification efficiency. A $500 million industrial wastewater recycling plant with annual capacity ~8,760,000 m³ is planned in Jubail Industrial City through a 30-year partnership among SATORP, Marafiq, Veolia and Lamar, aimed at large-scale wastewater reuse for industrial applications. These systems provide higher contaminant removal rates and improved water reuse potential. Industries with strict discharge norms, including pharmaceuticals and chemicals, are increasingly investing in advanced on-site treatment solutions. Additionally, municipalities are upgrading aging infrastructure to comply with environmental regulations and sustainability targets. As water scarcity intensifies globally, advanced treatment technologies are becoming essential for enabling safe water recycling and long-term resource management.

Growth Drivers

Rapid urbanization and population growth are major drivers of the wastewater treatment plants market, as expanding cities generate significantly higher volumes of municipal wastewater. As more people migrate to urban areas, demand for housing, sanitation, and water supply infrastructure increases, leading to greater pressure on existing treatment systems. Many developing regions are experiencing accelerated urban expansion, often outpacing the capacity of current wastewater facilities. This creates an urgent need for new treatment plants as well as the expansion and modernization of aging infrastructure. Higher population density also increases the risk of water pollution and public health concerns if wastewater is not properly treated. The NRCP has covered 57 rivers in 17 states at a total cost of ₹8,970 crore and has created about 2,945 MLD of sewage treatment capacity under earlier sanctioning and implementation. Earlier data also records that the NRCP had sanctioned projects worth around ₹5,870.54 crore, with central funds released of ₹2,510.63 crore, creating >2,500 MLD of capacity. Governments are therefore prioritizing investments in sewage networks and centralized treatment facilities to maintain environmental quality. Additionally, urban development projects often incorporate modern and energy-efficient treatment technologies to ensure long-term sustainability.

Market Restraints / Challenges

High capital and operational costs represent a significant challenge for the wastewater treatment plants market, as constructing and maintaining these facilities requires substantial financial investment. The initial setup involves expenses related to land acquisition, civil construction, advanced treatment equipment, pipeline networks, and automation systems. Modern plants incorporating membrane filtration, tertiary treatment, and energy recovery technologies further increase upfront costs. In addition to capital expenditure, operational costs such as electricity consumption, chemical usage, skilled labor, and routine maintenance remain consistently high. Energy-intensive processes like aeration and sludge treatment contribute significantly to ongoing expenses. Smaller municipalities and developing regions often struggle to secure sufficient funding for large-scale projects. As a result, despite long-term environmental benefits, the high financial burden can slow the adoption and expansion of advanced wastewater treatment infrastructure.

Market Opportunities

The expansion of water reuse and recycling projects represents a significant opportunity in the wastewater treatment plants market, driven by increasing global water scarcity and rising freshwater demand. Many regions are facing declining groundwater levels and unpredictable rainfall patterns, prompting governments to prioritize sustainable water management strategies. Advanced tertiary treatment technologies such as membrane filtration, reverse osmosis, and ultraviolet disinfection enable treated wastewater to be safely reused for irrigation, industrial processes, and even potable applications. Industries are increasingly adopting closed-loop water systems to reduce freshwater intake and comply with environmental regulations. The expansion of water reuse and recycling presents a significant opportunity in the wastewater treatment plants market, as global wastewater generation has reached nearly 359.4 billion cubic meters annually, while only 52% is effectively treated Municipalities are also investing in large-scale water recycling plants to secure alternative water sources for urban populations. Reuse initiatives help reduce pressure on natural water bodies while improving long-term water security.

Global Wastewater Treatment Plants Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 140.4 Billion |

|

Revenue Forecast in 2035 |

USD 308.2 Billion |

|

Growth Rate |

7.9% |

|

Segments Covered in the Report |

Treatment Process, Plant Type, Technology, Capacity, Application, End-Use Industry |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Veolia (France), SUEZ (France), Xylem Inc. (U.S.), IDE Technologies (Israel), Jacobs Solutions Inc. (U.S.), AECOM (U.S.), Doosan Heavy Industries & Construction (South Korea), Thermax Ltd. (India), Kurita Water Industries Ltd. (Japan), Mitsubishi Heavy Industries, Ltd. (Japan), Ecolab Inc. (U.S.), Aquatech International LLC (U.S.) |

|

Customization |

Available upon request |

Wastewater Treatment Plants Market Segmentation

By Treatment Process

Secondary Treatment is the largest category with a market share of about 50% in 2025, due to its widespread adoption in both municipal and industrial wastewater treatment facilities as a mandatory biological purification stage. Secondary processes such as activated sludge and sequencing batch reactors are essential for removing organic matter and suspended solids before discharge. These systems form the backbone of most conventional treatment plants worldwide. Regulatory frameworks typically require at least secondary-level treatment for effluent compliance, ensuring consistent demand. Their proven reliability, scalability, and cost-effectiveness make them the standard choice globally.

There Secondary Treatment further classified into followings

- Activated Sludge Process

- Trickling Filters

- Sequencing Batch Reactors (SBR)

Tertiary / Advanced Treatment is the fastest-growing category with a CAGR of 8.1% during the forecast period, due to increasing environmental regulations and rising water reuse initiatives. Technologies such as membrane bioreactors (MBR), reverse osmosis (RO), and UV disinfection are being adopted to remove emerging contaminants and enable safe water recycling. Growing industrial discharge standards and potable reuse projects are accelerating demand for advanced purification. These technologies support higher-quality effluent output suitable for reuse in agriculture and industry.

There Tertiary / Advanced Treatment further classified into followings

- Membrane Bioreactors (MBR)

- Reverse Osmosis (RO)

- UV Disinfection

- Advanced Oxidation Processes (AOP)

By Plant Type

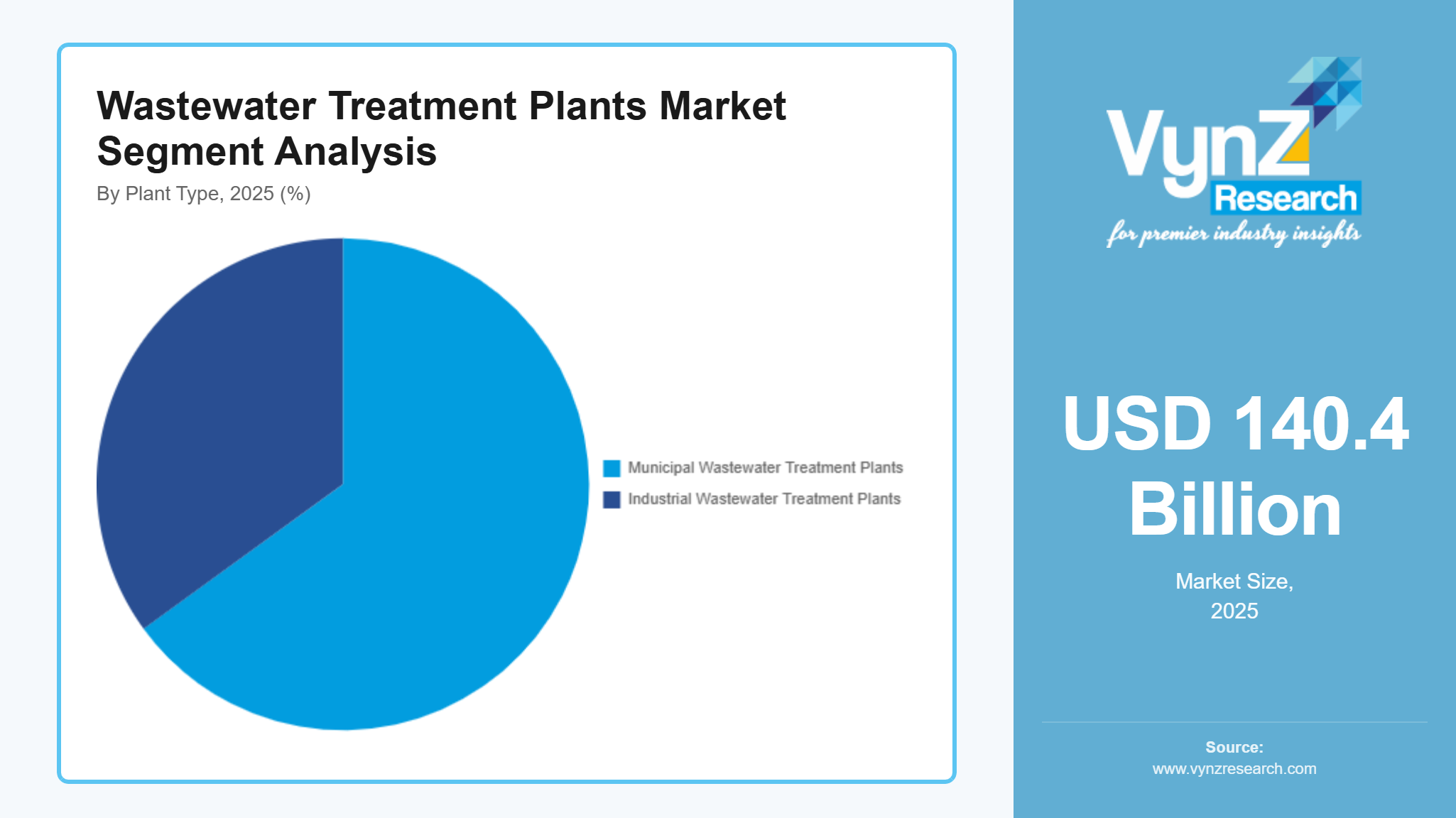

Municipal Wastewater Treatment Plants is the largest category with a market share of about 65% in 2025, due to expanding urban populations and the continuous generation of domestic sewage. Governments prioritize municipal wastewater infrastructure to protect public health and prevent environmental pollution. Large-scale centralized plants serve millions of residents, contributing significantly to overall market revenue. Urban development projects often include new sewage networks and treatment facilities. The consistent need for sanitation services ensures stable demand for municipal plants.

Industrial Wastewater Treatment Plants is the fastest-growing category with a CAGR of 8.5% during the forecast period, due to stricter industrial discharge norms and increasing manufacturing activities. Industries such as chemicals, pharmaceuticals, oil & gas, and food processing are investing in on-site treatment facilities. Compliance requirements and sustainability goals are pushing companies to upgrade and expand industrial wastewater systems. Rapid industrialization in emerging economies further supports strong growth in this segment.

By Technology

Biological Treatment is the largest category with a market share of about 40% in 2025, due to its effectiveness in removing organic pollutants through natural microbial processes. Activated sludge systems and aerobic treatment technologies are widely deployed across municipal and industrial plants. Biological methods are cost-effective and scalable, making them a preferred solution globally. Their long-standing operational reliability ensures continued dominance in the market.

Membrane Filtration Technology is the fastest-growing category during the forecast period, due to its superior contaminant removal efficiency and suitability for water reuse applications. Membrane-based systems such as ultrafiltration and reverse osmosis provide high-quality effluent output. Industries and municipalities seeking advanced purification and zero-liquid discharge solutions are increasingly adopting membrane technologies.

By Capacity

Large Capacity Plants is the largest category with a market share of about 45% in 2025, due to their deployment in major metropolitan areas and industrial clusters. Large plants treat massive volumes of wastewater daily, generating higher project values and infrastructure spending. Governments often invest heavily in centralized large-scale treatment facilities to serve dense populations. These projects involve significant engineering, construction, and technology procurement costs, reinforcing their dominant revenue share.

Small Capacity Plants is the fastest-growing category during the forecast period, due to increasing adoption of decentralized treatment solutions in rural and remote areas. Modular and compact systems are being deployed for residential complexes, small industries, and off-grid communities. Growing demand for localized wastewater management and faster installation timelines supports this segment’s rapid expansion.

By Application

Residential / Municipal Application is the largest category with a market share of about 60% in 2025, due to continuous sewage generation from urban households and public infrastructure. Municipal authorities are mandated to treat domestic wastewater before discharge into natural water bodies. Population growth and city expansion sustain consistent demand. Public health priorities further reinforce investment in residential wastewater treatment systems.

Industrial Application is the fastest-growing category with a CAGR of 8.5% during the forecast period, due to increasing industrial water consumption and strict compliance requirements. Industries are implementing advanced treatment systems to reduce environmental impact and enable water recycling. Sustainability initiatives and corporate ESG commitments further accelerate industrial wastewater infrastructure expansion.

There Industrial Application further classified into followings

- Chemicals & Petrochemicals

- Food & Beverages

- Pharmaceuticals

- Oil & Gas

- Power Generation

- Textiles

- Others

By End-Use Industry

Municipal Authorities is the largest category with a market share of about 65% in 2025, due to the fundamental responsibility of governments to manage public sanitation and wastewater infrastructure for urban and rural populations. Municipal bodies operate large-scale centralized wastewater treatment plants that process sewage generated from residential, commercial, and public facilities. Rapid urbanization and expanding city boundaries are continuously increasing municipal wastewater volumes, necessitating ongoing investments in new treatment facilities and upgrades of aging infrastructure. Governments allocate substantial public funding and often implement long-term infrastructure development programs to ensure environmental protection and compliance with discharge standards.

Industrial Facilities is the fastest-growing category with a CAGR of 8.2% during the forecast period, due to increasing industrialization and stricter regulatory enforcement on industrial effluent discharge. Industries such as chemicals, pharmaceuticals, food & beverages, textiles, oil & gas, mining, and power generation generate complex and high-strength wastewater that requires specialized treatment solutions. Regulatory agencies are tightening compliance norms, compelling industries to invest in advanced on-site treatment plants and zero-liquid discharge systems. Growing ESG commitments and the need to avoid environmental penalties continue to drive strong growth momentum in the industrial facilities segment.

Regional Insights

North America

North America is the largest regional market with a share of 30% in 2025 for wastewater treatment plants, supported by well-established water infrastructure and strict environmental regulations. The United States leads the region with extensive municipal wastewater networks and continuous investment in upgrading aging treatment facilities. Federal infrastructure funding programs and state-level environmental mandates are driving modernization projects, including nutrient removal and advanced tertiary treatment integration. The Pure Water Southern California project alone is valued at approximately $8 billion and is supported by $99.2 million in federal funding, forming part of a broader $450 million allocation for large water recycling projects under the Bipartisan Infrastructure Law. Additionally, the U.S. government has committed $8.3 billion over five years for water infrastructure development, significantly accelerating advanced wastewater recycling and potable reuse adoption across the region. Industrial sectors such as chemicals, pharmaceuticals, food processing, and energy also contribute significantly to demand for on-site wastewater treatment systems. Strong regulatory enforcement by environmental agencies ensures consistent compliance-driven investments.

Asia Pacific

Asia-Pacific is the fastest-growing region in the wastewater treatment plants market, driven by rapid urbanization, population growth, and expanding industrial activities. Countries such as China, India, Indonesia, and Vietnam are witnessing significant increases in wastewater generation due to urban expansion and manufacturing growth. Governments are investing heavily in new sewage treatment plants and upgrading existing infrastructure to reduce water pollution and improve sanitation coverage. Namami Gange Programme (National Mission for Clean Ganga) was originally approved with a budget outlay of ₹20,000 crore (~US$2.72 billion) from its launch in 2014 up to 2021. It was subsequently extended to March 2026 with further allocations; total budgetary allocation from FY 2014-15 to FY 2025-26 is ₹26,824.86 crore including ₹3,400 crore for FY 2025-26. As of late 2025, a total of 513 projects under the Namami Gange Programme have been sanctioned at a combined cost of ₹42,019 crore, with most projects focusing on sewage infrastructure and river pollution abatement. Water scarcity concerns are also encouraging wastewater recycling and reuse initiatives across the region. Industrial compliance requirements are becoming stricter, prompting higher adoption of advanced treatment technologies. Strong economic growth and infrastructure development programs continue to accelerate wastewater treatment investments in Asia-Pacific.

Europe

Europe maintains a strong presence in the wastewater treatment plants market due to stringent environmental regulations and a strong focus on sustainability. The European Union enforces comprehensive wastewater discharge standards that require continuous upgrades and adoption of advanced treatment processes. Countries such as France have announced plans to develop nearly 1,000 water reuse projects by 2027 as part of national water resilience strategies. These developments are supported through public funding mechanisms and EU-backed investment frameworks, driving deployment of advanced tertiary treatment and water recycling infrastructure across member states. Aging infrastructure modernization and circular economy initiatives further support market demand. Public awareness and regulatory enforcement ensure consistent investment in wastewater management systems.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is experiencing steady growth in wastewater treatment infrastructure development. In Latin America, Brazil and Mexico are expanding treatment capacity to improve sanitation coverage and reduce environmental pollution. The Middle East, particularly Saudi Arabia and the UAE, is investing in wastewater reuse projects to address water scarcity challenges. In Africa, countries such as South Africa are gradually strengthening wastewater infrastructure with support from public-private partnerships and international funding. Although infrastructure maturity varies, rising urbanization and environmental awareness are expected to accelerate market growth across these regions.

Competitive Landscape / Company Insights

The wastewater treatment market is moderately consolidated, led by large multinational engineering and environmental services firms that combine strong EPC (engineering, procurement, construction) capabilities with long-term O&M and concession models, while specialist technology providers compete on advanced process know-how. Major players such as Veolia and SUEZ dominate through broad service portfolios that span municipal concessions, industrial on-site plants, and integrated resource-recovery projects, giving them scale advantages in financing, global project delivery, and regulatory navigation. Technology and equipment leaders like Xylem Inc. and IDE Technologies differentiate by selling high-performance membranes, advanced RO/MBR packages, and modular treatment skids that appeal to both fast-track municipal projects and industrial clients with complex effluents.

Large AEC and infrastructure firms such as Jacobs Solutions Inc. and AECOM compete for big public and PPP contracts by bundling design, financing support, and lifecycle management, which raises barriers for smaller regional contractors. Heavy-equipment and process OEMs like Doosan Heavy Industries & Construction and specialist chemical/process suppliers capture value through proprietary process licensing, aftermarket spares, and performance guarantees. Niche innovators and start-ups focused on sludge-to-energy, nutrient recovery, and low-footprint MBR/EO (electrochemical/advanced oxidation) technologies are increasingly attractive partners for pilots, though their commercial scale-up is often accelerated via alliances with the larger players.

Mini Profiles

Veolia (France) is a global leader in water and wastewater solutions, providing integrated treatment systems, resource recovery technologies, and long-term operational services for municipal and industrial clients worldwide.

SUEZ (France) offers comprehensive wastewater treatment equipment and services, including membrane systems, biological treatment solutions, and turnkey plant design, with a strong global footprint across developed and emerging markets.

Xylem Inc. (United States) develops advanced water infrastructure technologies such as pumps, membranes, sensors, and automation platforms that optimize wastewater treatment performance and energy efficiency.

IDE Technologies (Israel) specializes in large-scale desalination and industrial wastewater treatment projects, integrating membrane technologies and advanced process engineering for high-efficiency treatment solutions.

Jacobs Solutions Inc. (United States) provides engineering, procurement, and construction (EPC) services for complex wastewater infrastructure projects, including planning, design, and long-term operations support.

Key Players

- Veolia

- SUEZ

- Xylem Inc.

- IDE Technologies

- Jacobs Solutions Inc.

- AECOM

- Doosan Heavy Industries & Construction

- Thermax Ltd.

- Kurita Water Industries Ltd.

- Mitsubishi Heavy Industries, Ltd.

- Ecolab Inc.

- Aquatech International LLC

Recent Developments

January 2026 – Veolia announced a strategic partnership with multiple U.S. municipalities to upgrade aging wastewater treatment plants with advanced membrane bioreactor (MBR) systems, enhancing effluent quality and water reuse capabilities.

December 2025 – SUEZ unveiled a new low-energy nutrient recovery process aimed at reducing operational costs and increasing phosphorus extraction from wastewater, supporting circular economy goals.

October 2025 – Xylem Inc. launched an AI-enabled wastewater plant optimization suite that integrates real-time sensor data with predictive analytics to lower energy consumption and improve plant reliability.

August 2025 – Jacobs Solutions Inc. secured a major EPC contract to design and build a tertiary treatment facility in Southeast Asia that incorporates advanced oxidation processes for potable reuse.

June 2025 – IDE Technologies announced expansion of its membrane manufacturing capacity in the Middle East to supply large-scale desalination and wastewater reuse projects tied to regional water security programs.

Global Wastewater Treatment Plants Market Coverage

Treatment Process Insight and Forecast 2026 - 2035

- Primary Treatment

- Secondary Treatment

- Tertiary / Advanced Treatment

Plant Type Insight and Forecast 2026 - 2035

- Municipal Wastewater Treatment Plants

- Industrial Wastewater Treatment Plants

Technology Insight and Forecast 2026 - 2035

- Biological Treatment

- Chemical Treatment

- Physical Treatment

- Membrane Filtration Technology

- Sludge Treatment & Management

Capacity Insight and Forecast 2026 - 2035

- Small Capacity Plants

- Medium Capacity Plants

- Large Capacity Plants

Application Insight and Forecast 2026 - 2035

- Residential / Municipal

- Industrial

End-Use Industry Insight and Forecast 2026 - 2035

- Municipal Authorities

- Industrial Facilities

- Commercial Establishments

Global Wastewater Treatment Plants Market by Region

- North America

- By Treatment Process

- By Plant Type

- By Technology

- By Capacity

- By Application

- By End-Use Industry

- By Country - U.S., Canada, Mexico

- Europe

- By Treatment Process

- By Plant Type

- By Technology

- By Capacity

- By Application

- By End-Use Industry

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Treatment Process

- By Plant Type

- By Technology

- By Capacity

- By Application

- By End-Use Industry

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Treatment Process

- By Plant Type

- By Technology

- By Capacity

- By Application

- By End-Use Industry

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Wastewater Treatment Plants Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Treatment Process

1.2.2. By

Plant Type

1.2.3. By

Technology

1.2.4. By

Capacity

1.2.5. By

Application

1.2.6. By

End-Use Industry

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Treatment Process

5.1.1. Primary Treatment

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Secondary Treatment

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Tertiary / Advanced Treatment

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Plant Type

5.2.1. Municipal Wastewater Treatment Plants

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Industrial Wastewater Treatment Plants

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Biological Treatment

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Chemical Treatment

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Physical Treatment

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Membrane Filtration Technology

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Sludge Treatment & Management

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Capacity

5.4.1. Small Capacity Plants

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Medium Capacity Plants

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Large Capacity Plants

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Residential / Municipal

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Industrial

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.6. By End-Use Industry

5.6.1. Municipal Authorities

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Industrial Facilities

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Commercial Establishments

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Treatment Process

6.2. By

Plant Type

6.3. By

Technology

6.4. By

Capacity

6.5. By

Application

6.6. By

End-Use Industry

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Treatment Process

7.2. By

Plant Type

7.3. By

Technology

7.4. By

Capacity

7.5. By

Application

7.6. By

End-Use Industry

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Treatment Process

8.2. By

Plant Type

8.3. By

Technology

8.4. By

Capacity

8.5. By

Application

8.6. By

End-Use Industry

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Treatment Process

9.2. By

Plant Type

9.3. By

Technology

9.4. By

Capacity

9.5. By

Application

9.6. By

End-Use Industry

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Veolia

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

SUEZ

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Xylem Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

IDE Technologies

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Jacobs Solutions Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

AECOM

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Doosan Heavy Industries & Construction

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Thermax Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Kurita Water Industries Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Mitsubishi Heavy Industries, Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Ecolab Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Aquatech International LLC

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Wastewater Treatment Plants Market