Modular Flooring Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Luxury Vinyl Tile, Ceramic, Rubber, Polyolefin), by Installation Technique (Interlocking, Loose Lay), by End Use (Residential, Commercial, Healthcare, Education, Retail)

| Status : Published | Published On : May, 2026 | Report Code : VRCH2131 | Industry : Chemicals & Materials | Available Format :

|

Page : 163 |

Modular Flooring Market Overview

The global modular flooring market which was valued at approximately USD 13.5 billion in 2025 and is estimated to rise further up to almost USD 14.4 billion in 2026, is projected to reach around USD 20.8 billion in 2035, expanding at a CAGR of about 4.5% during the forecast period from 2026 to 2035.

The market experiences growth because cities construct new infrastructure, people renovate their homes and business spaces, and customers choose affordable flooring options which require simple installation, while they also begin to use environmentally friendly and recyclable materials. The market expands due to increased demand for flooring solutions which provide high durability and require minimal upkeep in office spaces, retail locations and healthcare facilities, combined with ongoing funding for smart city projects and green building initiatives.

The industry receives government-backed institution support and policy-level interventions, which enable industry growth. The World Health Organization and other organizations report that healthcare facilities require hygienic indoor environments, which create an indirect need for flooring systems that can withstand heavy use and undergo quick cleaning. The construction and refurbishment activities throughout Asia Pacific, North America, and Europe proceed at an accelerated pace because national infrastructure pipelines and urban housing missions drive development, which leads to increased adoption of modular flooring solutions in both developed and emerging economies.

Modular Flooring Market Dynamics

Market Trends

The design trends of the industry and material development progress through sustainable development requirements and energy efficient performance standards. The market develops through the rising use of flooring materials that can be recycled and environmentally friendly properties which demonstrate a shift toward ecofriendly building methods. The United Nations Environment Program together with green building standards functions as a framework that helps manufacturers create modular flooring products which fulfill environmental standards by using materials that decrease carbon emissions.

The construction industry develops through the combination of advanced manufacturing methods with digital design systems which operate under technological progress and changing construction methods. The new market conditions prompt businesses to develop products that feature long-lasting capabilities and straightforward installation options while allowing customers to create personalized flooring solutions. The trend develops further through the increasing use of prefabricated building components and modular construction methods which receive backing from regional infrastructure development programs.

Growth Drivers

The global construction industry growth creates ongoing demand for modular flooring products which supports the market growth through its three main application areas of residential, commercial and institutional building projects. The market expansion receives a boost from rising investments in urban infrastructure, housing projects and commercial real estate development. The World Bank reports that emerging economies experience ongoing construction spending growth which drives demand for affordable and scalable flooring products.

The rising demand for hygienic and low maintenance building materials functions as a major factor that drives increased product adoption. The demand for resilient modular flooring systems will continue to grow during the entire forecast period because end users need products that offer durability together with safety and simple cleaning process. The World Health Organization Guidelines for healthcare and public infrastructure state that indoor hygiene standards should be improved, which helps critical environments establish better cleanliness practices.

Market Restraints / Challenges

The market has attractive growth prospects but the industry faces several obstacles which will restrict its future development. The market faces challenges from raw material price changes which primarily affect polymers and synthetic materials because they significantly reduce product margins for businesses located in price sensitive areas. Supply chain disruptions together with reliance on petroleum-based materials cause manufacturers to experience cost fluctuations which negatively influence their profits during economic downturns.

The product development process faces obstacles because manufacturers and suppliers need to fulfill environmental regulatory requirements which transform into operational obstacles. The rising production expenses and certification obligation problems stem from businesses who depend on imported raw materials together with changing sustainability regulations. The European Environment Agency and other official organizations publish environmental guidelines and reports which create greater compliance standards for businesses that need to fulfill environmental regulations, leading to longer product approval processes and reduced scalability in selected markets.

Market Opportunities

The market provides large growth possibilities through sustainable building solutions which gain momentum from the rising use of building materials that comply with environmental regulations. Companies offering recyclable, low emission, and modular flooring systems are well positioned to capture incremental demand from commercial developers and institutional buyers. Government supported green building programs and urban sustainability initiatives are further enabling this transition toward eco efficient materials.

The growing urban centers and intelligent infrastructure systems create demand for building system automation which drives the market for modular building systems and prefabrication facilities. Customer interaction will improve while project delivery time will decrease because businesses will develop automated manufacturing systems together with digital design platforms and installation methods. The Asian Development Bank supports public infrastructure strategies which create more opportunities for developing markets to experience long-term growth in the market.

Global Modular Flooring Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 13.5 Billion |

|

Revenue Forecast in 2035 |

USD 20.8 Billion |

|

Growth Rate |

4.5% |

|

Segments Covered in the Report |

Product Type, Installation Technique, End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Armstrong Flooring, Inc., Beaulieu International Group, CFL Holding Limited, Forbo Holding AG, Gerflor Group, Interface, Inc., James Halstead plc, Mannington Mills, Inc., Mohawk Industries, Inc., Shaw Industries Group, Inc., Tarkett |

|

Customization |

Available upon request |

Modular Flooring Market Segmentation

By Product Type

In 2025, luxury vinyl tile achieved the highest market share with 46% total revenue because its products offered superior durability, moisture protection and simple installation methods. The widespread use of sustainable construction materials in offices, retail spaces and healthcare centers derives from building regulations and indoor environmental standards which the United Nations Environment Program establishes to promote environmentally friendly building practices.

The market will experience highest growth through rubber and polyolefin products which will achieve a compound annual growth rate of 5.2% between 2026 and 2035. The market expansion occurs because institutional and industrial sectors now demand materials which can withstand heavy impact while remaining recyclable. Organizations that create regulations for sustainable infrastructure development have specific requirements which driving organizations must meet before their solutions can be adopted in high-traffic spaces.

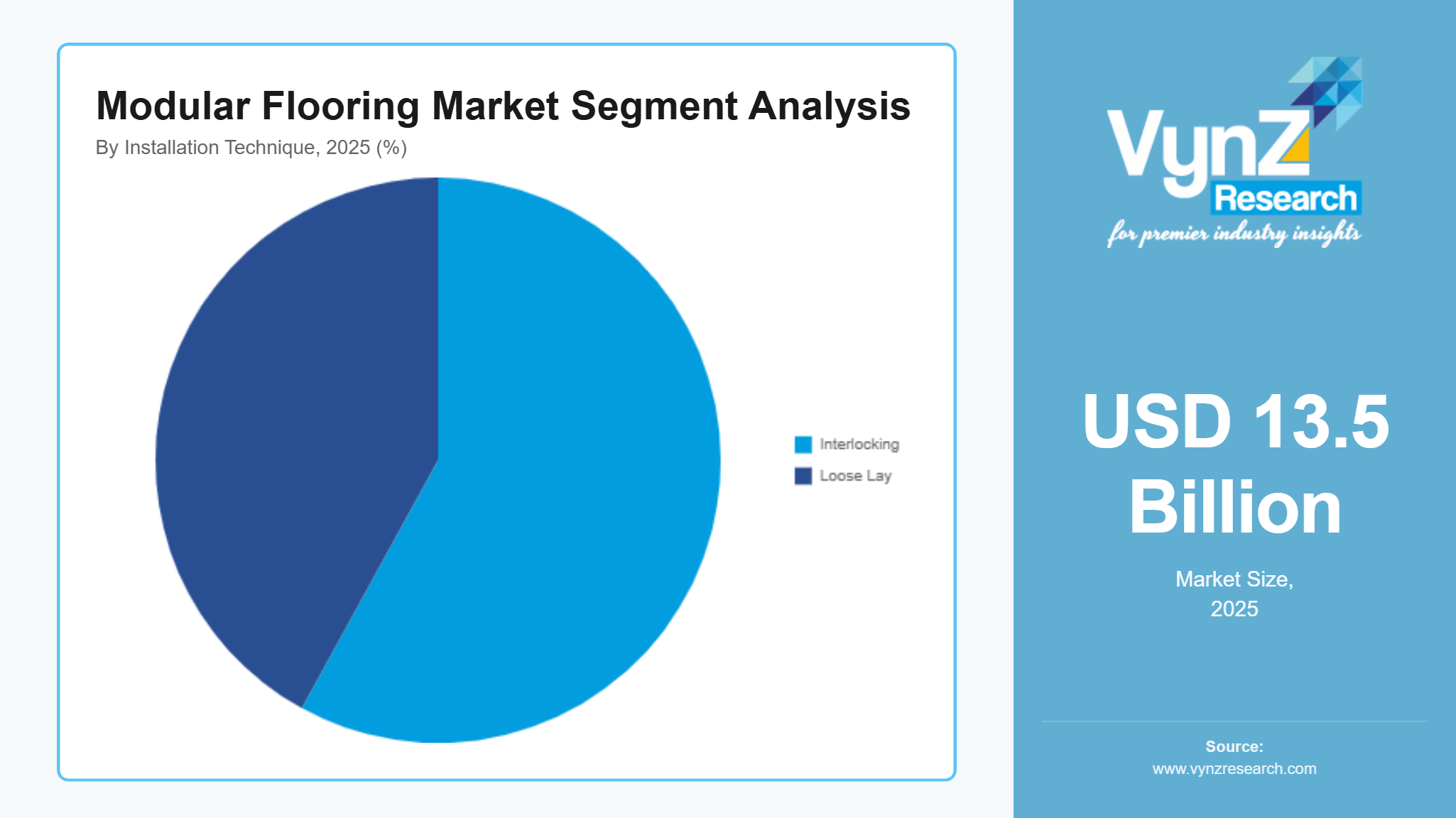

By Installation Technique

Interlocking systems held the majority share in 2025, accounting for approximately 58% of revenue, as buyers continue to prioritize ease of installation, reduced labor dependency, and faster project completion timelines. The adoption of these technologies gains support through construction efficiency guidelines which come from infrastructure development programs that emerge from developing countries.

The market for loose lay systems shows stronger development prospects with its projected compound annual growth rate of 5.4% until 2023. Businesses now prefer flexible flooring systems which they can reuse across their commercial and temporary installations. The industry adopts modular construction combined with cost efficiency solutions while companies use adhesive free technology to boost their operational productivity and decrease their installation duration.

By End Use

The commercial segment accounted for the highest revenue share in 2025, representing approximately 41% of the market, supported by rapid urbanization, expansion of office spaces, and increasing investment in retail infrastructure. The demand for long-lasting and expandable flooring products in commercial spaces receives support from government financed infrastructure projects and urban development programs which operate in critical economic regions.

The healthcare and education sectors will grow at the highest rate because they project a compound annual growth rate of 5.3% throughout the upcoming forecasting period. The market grows because hospitals, clinics and institutional infrastructure areas receive more funding while hygiene and safety regulations become increasingly important. The World Health Organization guidelines which promote clean and safe indoor environments help to drive demand for antimicrobial flooring solutions that require easy maintenance because of their cleanliness requirements.

Regional Insights

North America

North America accounted for approximately 32% of the market in 2025 because construction projects and renovation work increased and commercial and institutional facilities started using advanced building materials. The major urban centers of New York, Los Angeles and Toronto sustain demand through their construction of new office space, retail stores and healthcare facilities. The United States Environmental Protection Agency issues guidelines and sustainability frameworks which establish standards for low emission materials and recyclable materials and these standards provide a basis for using modular flooring solutions which comply with green building standards.

Europe

The market in Europe will reach 26% by 2025 due to strict environmental regulations which exist together with established construction standards and rising refurbishment needs in both residential and commercial buildings. The office healthcare and educational sectors in Germany, the UK France and Italy are currently experiencing constant demand for modular flooring products. The European Environment Agency leads environmental compliance policies which establish guidelines for using sustainable materials and energy efficient building practices that will drive market growth over time.

Asia Pacific

The Asia Pacific region holds 22% of the market share in 2025 because China, India and Japan experience rapid urban growth and their infrastructure projects, residential and commercial development activities expand. Shanghai, Mumbai and Tokyo function as primary centers for real estate investment and infrastructure development activities in their respective regions. The Asian Development Bank financially supports urban development initiatives which include reports that show increasing investment in smart cities and urban infrastructure development and these developments create a need for scalable and cost-efficient flooring solutions.

Rest of the World

The market share of Latin America, the Middle East and Africa constitutes 20% of global market share in 2025. Infrastructure development together with urban development projects and the gradual adoption of modern construction materials drive growth in these regions. The commercial and institutional construction sectors in Brazil, the UAE and South Africa are currently experiencing better construction activity. The World Bank development programs create a framework for infrastructure and urban expansion which will lead to market growth.

Competitive Landscape / Company Insights

The modular flooring market has a competitive landscape that includes international and domestic businesses which compete through their product development efforts, their pricing methods and their expansion into new regions. Companies today invest their resources to develop sustainable materials, advanced manufacturing technologies and branding initiatives which help them build a successful market position. The environmental standards established through United Nations Environment Program and national construction policies promote green building programs which help developing low emission recyclable flooring solutions and create competitive advantages for businesses through expanded market access.

Mini Profiles

Armstrong Flooring, Inc. focuses on resilient flooring solutions, including vinyl tiles and modular systems, supported by strong distribution networks, brand recognition in North America, and cost-efficient manufacturing capabilities across commercial applications.

Beaulieu International Group operates in mass and premium flooring segments, emphasizing product diversity, performance efficiency, and sustainable materials, supported by global manufacturing presence and strong positioning across residential and commercial construction markets.

CFL Holding Limited leverages large scale manufacturing, private label partnerships, and global supply chain capabilities to expand market presence, offering cost competitive modular flooring solutions across residential, retail, and institutional applications.

Forbo Holding AG focuses on high performance modular flooring solutions, supported by innovation in sustainable materials, strong European distribution networks, and established brand recognition across commercial, healthcare, and industrial end use sectors.

Gerflor Group operates in specialized and performance driven segments, emphasizing durability, safety compliance, and eco friendly flooring systems, supported by strong presence in healthcare, education, and sports infrastructure markets globally.

Key Players

- Armstrong Flooring, Inc.

- Beaulieu International Group

- CFL Holding Limited

- Forbo Holding AG

- Gerflor Group

- Interface, Inc.

- James Halstead plc

- Mannington Mills, Inc.

- Mohawk Industries, Inc.

- Shaw Industries Group, Inc.

- Tarkett

Recent Developments

In March 2026, Mohawk Industries, Inc. expanded its operational footprint in Europe to strengthen supply chain efficiency and regional distribution capabilities. This development supports increasing demand for modular flooring solutions across commercial and residential applications.

In January 2026, Shaw Industries Group, Inc. launched its EcoWorx Resilient flooring, a PVC free and recyclable product line designed to enhance sustainability in modular flooring applications. The launch reflects growing industry focus on environmentally compliant materials.

In January 2026, Tarkett introduced an expanded iQ Optima vinyl flooring range, enhancing durability and design flexibility for commercial environments. The development strengthens its product portfolio aligned with high performance modular flooring demand.

In February 2026, Interface, Inc. introduced new design driven carpet tile and luxury vinyl tile collections, focusing on aesthetics and performance optimization. These product innovations support evolving workplace and commercial interior requirements.

In March 2026, Beaulieu International Group enhanced its digital platforms to improve customer access to sustainable flooring solutions. This initiative supports increasing adoption of eco friendly modular flooring products across global markets.

Global Modular Flooring Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Luxury Vinyl Tile

- Ceramic

- Rubber

- Polyolefin

Installation Technique Insight and Forecast 2026 - 2035

- Interlocking

- Loose Lay

End Use Insight and Forecast 2026 - 2035

- Residential

- Commercial

- Healthcare

- Education

- Retail

Global Modular Flooring Market by Region

- North America

- By Product Type

- By Installation Technique

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Installation Technique

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Installation Technique

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Installation Technique

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Modular Flooring Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Installation Technique

1.2.3. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Luxury Vinyl Tile

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Ceramic

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Rubber

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Polyolefin

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Installation Technique

5.2.1. Interlocking

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Loose Lay

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By End Use

5.3.1. Residential

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Commercial

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Healthcare

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Education

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Retail

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Installation Technique

6.3. By

End Use

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Installation Technique

7.3. By

End Use

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Installation Technique

8.3. By

End Use

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Installation Technique

9.3. By

End Use

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Armstrong Flooring, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Beaulieu International Group

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

CFL Holding Limited

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Forbo Holding AG

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Gerflor Group

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Interface, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

James Halstead plc

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Mannington Mills, Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Mohawk Industries, Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Shaw Industries Group, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Modular Flooring Market