US TIC Market for Consumer Goods & Retail Industry Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In house testing services, Outsourced testing services), by Service Type (Testing services, Inspection services, Certification services), by Industry Vertical (Consumer goods, Retail, Food and beverage, Electronics, Household products)

| Status : Published | Published On : Apr, 2026 | Report Code : VRCG7055 | Industry : Consumer Goods | Available Format :

|

Page : 123 |

US TIC Market for Consumer Goods & Retail Industry Overview

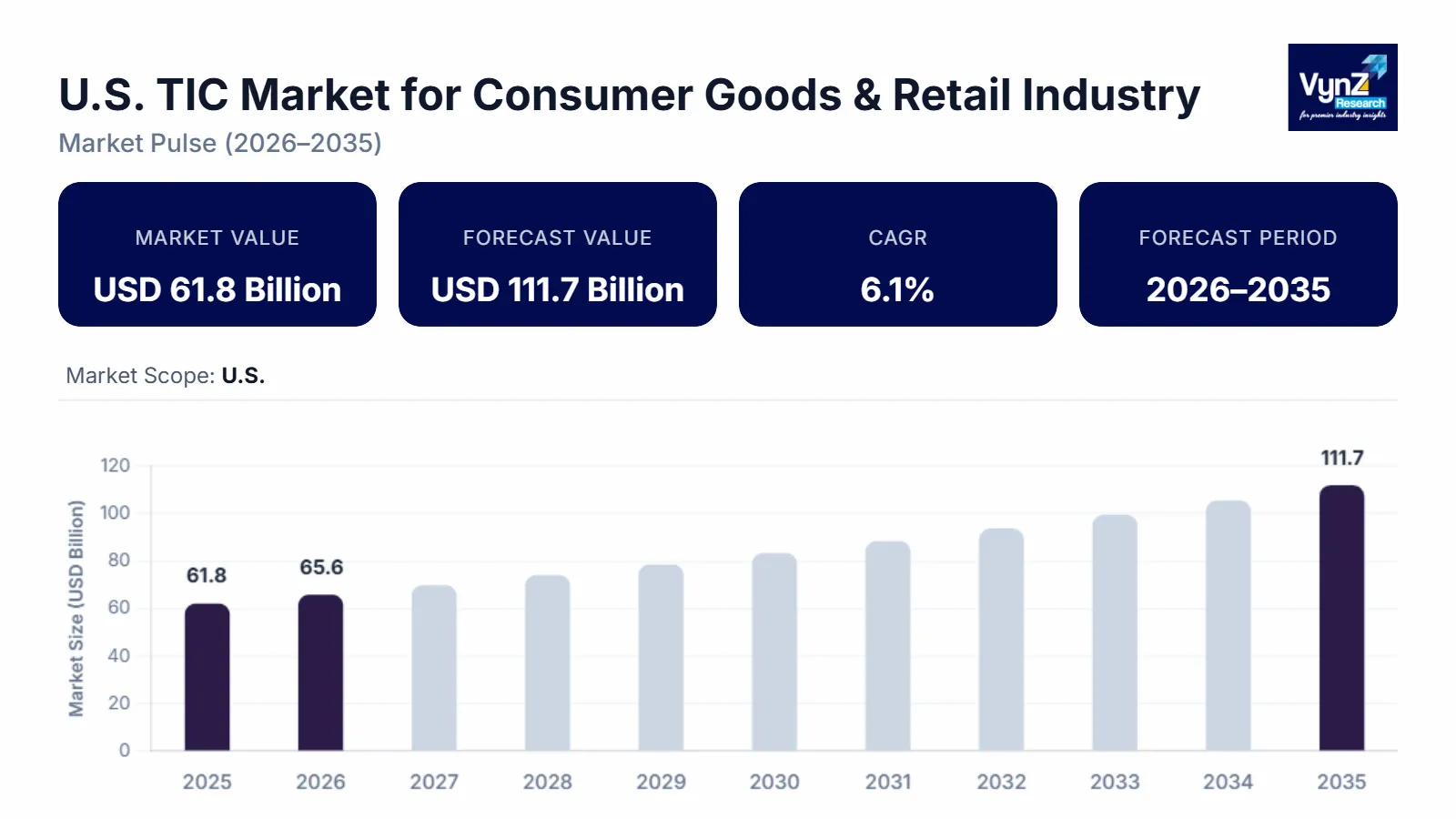

The U.S. TIC market for consumer goods and retail industry which was valued at approximately USD 61.8 billion in 2025 and is estimated to rise further up to almost USD 65.5 billion by 2026, is projected to reach around USD 111.7 billion in 2035, expanding at a CAGR of about 6.1% during the forecast period from 2026 to 2035.

Market expansion throughout the world occurs because businesses need to follow more regulations, supply chains become more complicated and product quality verification processes become more critical. Digital testing and certification solutions also gain popularity among users. The United States, Canada and Mexico experience market growth because consumers require safe products which meet current retail standards of compliance and safety.

The market expansion process receives additional support from the regulatory framework and standardization efforts which government and international organizations implement. The World Health Organization and U.S. Consumer Product Safety Commission established frameworks which create essential testing requirements for all consumer goods because they require protection of product safety and established quality standards and need risk control. The U.S. Food and Drug Administration together with trade compliance programs work to enhance inspection processes by implementing new certification requirements. The United States market is experiencing increased acceptance of TIC services because government organizations spend more money on QI-based infrastructure and e commerce and border trade monitoring systems have expanded.

US TIC Market for Consumer Goods & Retail Industry Dynamics

Market Trends

The sector experiences significant technological changes, new compliance systems and different purchasing methods throughout retail supply chains. Digital inspection systems and automation technology together with data driven certification services, serve as major market transformation because they enable businesses to achieve efficient operations and trace their products and reduce costs. The U.S. Consumer Product Safety Commission developed safety monitoring systems through its regulatory guidance to create urgent product monitoring requirements, which resulted in increased adoption of modern TIC technologies.

Testing and certification procedures now operate according to environmental compliance standards and sustainability standards because of new regulations and corporate responsibility growth, which led to this trend. The World Health Organization and environmental safety directives establish frameworks that promote the use of safer materials, which manufacturers need to follow through operational assessment of their products. The market developments create new service options, which lead companies to pursue complete compliance solutions, digital documentation platforms and verification services that provide additional value, thus changing the market competition structure.

Growth Drivers

The market achieves its expansion through increasing regulatory enforcement and product safety compliance needs, which create permanent demand in retail, e-commerce, and manufacturing sector. The market growth accelerates due to new investments into supply chain network development, international trade system development, and quality control system implementation. Government compliance frameworks established by U.S. Food and Drug Administration need testing and certification processes, which create more demand for TIC services.

The e-commerce industry and omnichannel retail sector both experience growth, which boosts their acceptance of products. Enterprises experience continuous demand for testing and inspection services because they need to maintain product authenticity, safety and regulatory compliance. Public safety regulations and international trade standards create a stable demand for digital compliance tools and traceability systems, which drive long-term growth in the industry.

Market Restraints / Challenges

The market maintains strong growth potential, yet it encounters several obstacles that will restrict its market development. Regulatory requirements together with changing compliance requirements create operational challenges for small and medium enterprises by reducing their market access. U.S. Consumer Product Safety Commission requirements for government compliance reports and safety requirements mandate enterprises to provide more testing and certification evidence, which results in higher processing costs.

Third party inspection systems together with global supply chain dependence create operational issues that make service delivery more complicated. Organizations that rely on imported testing equipment, skilled personnel and external laboratories face both cost challenges and delays in delivering services, which results in negative market effects during times of economic fluctuation. International regulatory standards, which countries apply differently, create difficulties that companies need to navigate when they work on cross-border certification.

Market Opportunities

The market provides major prospects through the digital transformation process, which enables testing and certification operations to become fully automated. Retailers and brand owners will seek integrated technology solutions, which provide them operational efficiency, better product visibility and digital systems. The government-backed programs, which focus on digitizing product safety and modernizing trade compliance, provide additional growth opportunities.

The testing and certification services for sustainability create a business chance because more companies invest in products that respect environmental regulations and ethical sourcing standards. The development of AI-based inspection systems, remote auditing technologies and digital certification platforms will improve operational efficiency and client engagement. The World Health Organization supports regulatory alignment, which promotes the use of TIC solutions that meet both standard and high-performance requirements in the United States market.

US TIC Market for Consumer Goods & Retail Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 61.8 Billion |

|

Revenue Forecast in 2035 |

USD 111.7 Billion |

|

Growth Rate |

6.1% |

|

Segments Covered in the Report |

Sourcing Type, Service Type, Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

West, South, Northeast, Midwest |

|

Key Companies |

Intertek Group plc, SGS SA, Bureau Veritas, Eurofins Scientific, TUV Rheinland, TUV Nord Group, TUV SUD, Applus+, DNV, UL Solutions |

|

Customization |

Available upon request |

US TIC Market for Consumer Goods & Retail Industry Segmentation

By Sourcing Type

The market which operates through internal testing services managed to achieve its highest market share during 2025 when it used 56% of the market because companies used their internal testing systems to meet strict compliance demands while large retail businesses needed reliable testing solutions and they needed to monitor product quality for their high-volume inventory. The U.S. Consumer Product Safety Commission establishes mandatory safety verification requirements which operate as both safety testing procedures and product testing procedures which need to verify all consumer products.

The testing services growth rate will reach 6.4% CAGR because supply chains become more complicated and companies need to reduce operational costs and they start using specialized third-party TIC providers. Retail and consumer goods manufacturers increase their outsourcing activities because global sourcing networks require them to establish compliance standards which should adapt to their growing business operations.

By Service Type

The market gained its highest share of 48% in 2025 through testing services because consumer goods and retail products required safety validation, product performance evaluation and chemical compliance testing. The U.S. Food and Drug Administration enforce rigorous product testing requirements which all regulated products must follow to meet compliance standards.

The inspection services growth rate will reach 6.2% CAGR in the forecast period from 2026 to 2035because retail distribution networks need to establish supply chain transparency and monitor product quality and verify product details in real time. Certification services maintained a market share of 20% because international trade compliance requirements and global retail ecosystems started to standardize product quality benchmarks.

By Industry Vertical

The consumer goods segment achieved the highest market share when it reached 38% during 2025 because companies could sell their products through various channels while meeting safety standards required for mass market items. The World Health Organization establishes regulatory frameworks which create more stringent requirements for safety and quality compliance in this product category.

The retail segment will experience the highest growth rate of 6.5% in the forecast period because e-commerce platforms and omnichannel retail systems and product authentication needs are all growing rapidly. Electronics maintained a market share of 19% while household products managed to capture 15% of the market because both markets are experiencing rising product complexity and safety concerns and consumers want products with better quality.

Regional Insights

West

The West United States accounted for approximately 34% of the market in 2025 driven by strong presence of large-scale retail chains advanced manufacturing ecosystems and high concentration of technology enabled supply chain operations. States such as California and Washington play a central role due to their dense consumer markets and stringent product safety enforcement environment. The U.S. Consumer Product Safety Commission continues to enhance its regulatory oversight which establishes stricter compliance requirements that drive ongoing demand for testing and certification solutions. The region experiences market expansion through two main factors which include increasing e-commerce logistics hub development and rising cross border trade activities that happen at West Coast ports.

South

The South United States held approximately 29% market share in 2025 supported by rapid industrial expansion, growing retail distribution networks and increasing consumer goods manufacturing activity in states such as Texas, Florida and Georgia. Strong population growth and urbanization trends are driving higher consumption of packaged goods and retail products which results in increased demand for TIC services. Government supported trade and safety frameworks together with compliance standards that match U.S. Food and Drug Administration requirements are establishing better quality assurance standards for regional food and beverage and consumer product categories.

Northeast

The Northeast United States accounted for approximately 21% of the market share in 2025 driven by high retail density, established consumer markets and strong presence of corporate headquarters and compliance centers. The retail ecosystems of New York, Massachusetts and Pennsylvania face strict regulatory standards which result in significant contributions from those states. The demand for testing and inspection and certification services rises because of high product turnover rates which are associated with premium consumer demand patterns. The regional TIC landscape benefits from better operational efficiency through organizations that adopt digital compliance systems and structured safety monitoring frameworks.

Midwest

The Midwest United States accounted for approximately 16% of the market share in 2025 supported by strong manufacturing activity, logistics infrastructure and industrial distribution networks across states such as Illinois, Ohio and Michigan. The region plays a key role in consumer goods production and supply chain operations which creates ongoing demand for quality assurance and compliance services. The expansion of warehousing hubs together with transportation network development results in stronger inspection and certification requirements. The government industrial safety regulations and quality monitoring standards create a stable market environment which results in consistent market growth throughout the region.

Competitive Landscape / Company Insights

The market demonstrates a competitive environment which ranges from moderate to strong competition because global and regional companies operate their business through service innovation, digital compliance capabilities and their retail supply chain expansion into new markets. Companies are making more investments in digital testing platforms, automation technologies and advanced inspection systems to achieve operational efficiency and regulatory compliance. The U.S. Consumer Product Safety Commission and U.S. Food and Drug Administration compliance standards create regulatory frameworks which impose stricter quality assurance requirements and certification obligations that increase competition among businesses.

Mini Profiles

Applus+ focuses on testing, inspection, and certification services, supported by strong engineering expertise and diversified global operations, enabling consistent compliance solutions across automotive, energy, and industrial consumer goods markets.

Bureau Veritas operates in premium compliance and certification segments, emphasizing quality assurance, sustainability standards, and regulatory alignment, with strong global network presence across retail, manufacturing, and consumer product industries.

Eurofins Scientific leverages advanced laboratory testing capabilities and strong scientific infrastructure to expand market presence, delivering high precision analytical services across food, pharmaceuticals, and consumer goods safety testing segments.

Intertek Group plc focuses on assurance, testing, inspection, and certification solutions, supported by strong global brand recognition and integrated digital quality platforms, strengthening compliance across retail and supply chain ecosystems.

SGS SA operates in diversified TIC segments, emphasizing performance, safety, and sustainability testing services, with extensive international network strength enabling broad coverage across consumer goods and industrial regulatory compliance markets.

Key Players

- Applus+

- Bureau Veritas

- DNV

- Eurofins Scientific

- Intertek Group plc

- SGS SA

- TUV Nord Group

- TUV Rheinland

- TUV SUD

- UL Solutions

Recent Developments

In April, 2026, Intertek Group plc initiated a strategic review aimed at optimizing its business structure to enhance growth and shareholder value. The company also expanded its digital product passport and real-time compliance solutions portfolio, strengthening its position in global testing and certification services.

In March, 2026, SGS SA advanced its long-term incentive and governance framework to strengthen leadership alignment across global TIC operations. The company continued focusing on sustainability-linked performance metrics, reinforcing its certification and compliance leadership across consumer and industrial markets.

In January, 2026, Bureau Veritas completed multiple portfolio optimization initiatives, including strategic acquisitions and divestments to strengthen its consumer products and compliance services segment. The company also expanded its sustainability and digital assurance capabilities to support evolving regulatory requirements across global supply chains.

In December, 2025, Eurofins Scientific expanded its laboratory testing network across food, pharmaceuticals, and consumer goods sectors to enhance global analytical capacity. The company strengthened its regulatory testing services portfolio to support increasing demand for safety and quality compliance in international markets.

In December, 2025, Intertek Group plc expanded its global testing and calibration infrastructure through new laboratories focused on consumer goods and industrial safety testing. The company also strengthened its certification capabilities under evolving international machinery and safety regulations, improving compliance efficiency across sectors.

Market Coverage

By Sourcing Type

In house testing services

Outsourced testing services

By Service Type

Testing services

Inspection services

Certification services

By Industry Vertical

Consumer goods

Retail

Food and beverage

Electronics

Household products

US TIC Market for Consumer Goods & Retail Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- In house testing services

- Outsourced testing services

Service Type Insight and Forecast 2026 - 2035

- Testing services

- Inspection services

- Certification services

Industry Vertical Insight and Forecast 2026 - 2035

- Consumer goods

- Retail

- Food and beverage

- Electronics

- Household products

US TIC Market for Consumer Goods & Retail Industry by Region

- West

- By Sourcing Type

- By Service Type

- By Industry Vertical

- South

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Northeast

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Midwest

- By Sourcing Type

- By Service Type

- By Industry Vertical

Table of Contents for US TIC Market for Consumer Goods & Retail Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. US Market Estimate and Forecast

4.1. US Market Overview

4.2. US Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. In house testing services

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Outsourced testing services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing services

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection services

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification services

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Consumer goods

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Retail

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Food and beverage

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Electronics

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Household products

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. West Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

7. South Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

8. Northeast Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

9. Midwest Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

10. Company Profiles

10.1.

Applus+

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bureau Veritas

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

DNV

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Eurofins Scientific

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intertek Group plc

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

SGS SA

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

TUV Nord Group

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

TUV Rheinland

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TUV SUD

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

UL Solutions

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

US TIC Market for Consumer Goods & Retail Industry