Décor Paper Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Application (Continuous Pressure Laminates, Low-Pressure Laminates, High-Pressure Laminates), by Raw Materials (Fillers & Binders, Additives, Coating, Pulp, Others), by Product Type (Uni Paper, Edge Banding Paper, Base Paper for Foil Production, Absorbent Kraft Paper, Print Base Paper, Others), by Weight (Above 100 GSM, 81–100 GSM, 65–80 GSM, Less than 65 GSM), by Industry (Household Type, Commercial Type), by End User (Direct Printing, Store Fixture, Panelling, Wallcovering Laminates, Furniture and Cabinets, Wallpaper, Flooring), by Region (North America, Europe, Asia Pacific, Rest of the World)

| Status : Published | Published On : May, 2026 | Report Code : VRCG7056 | Industry : Consumer Goods | Available Format :

|

Page : 160 |

Décor Paper Market Overview

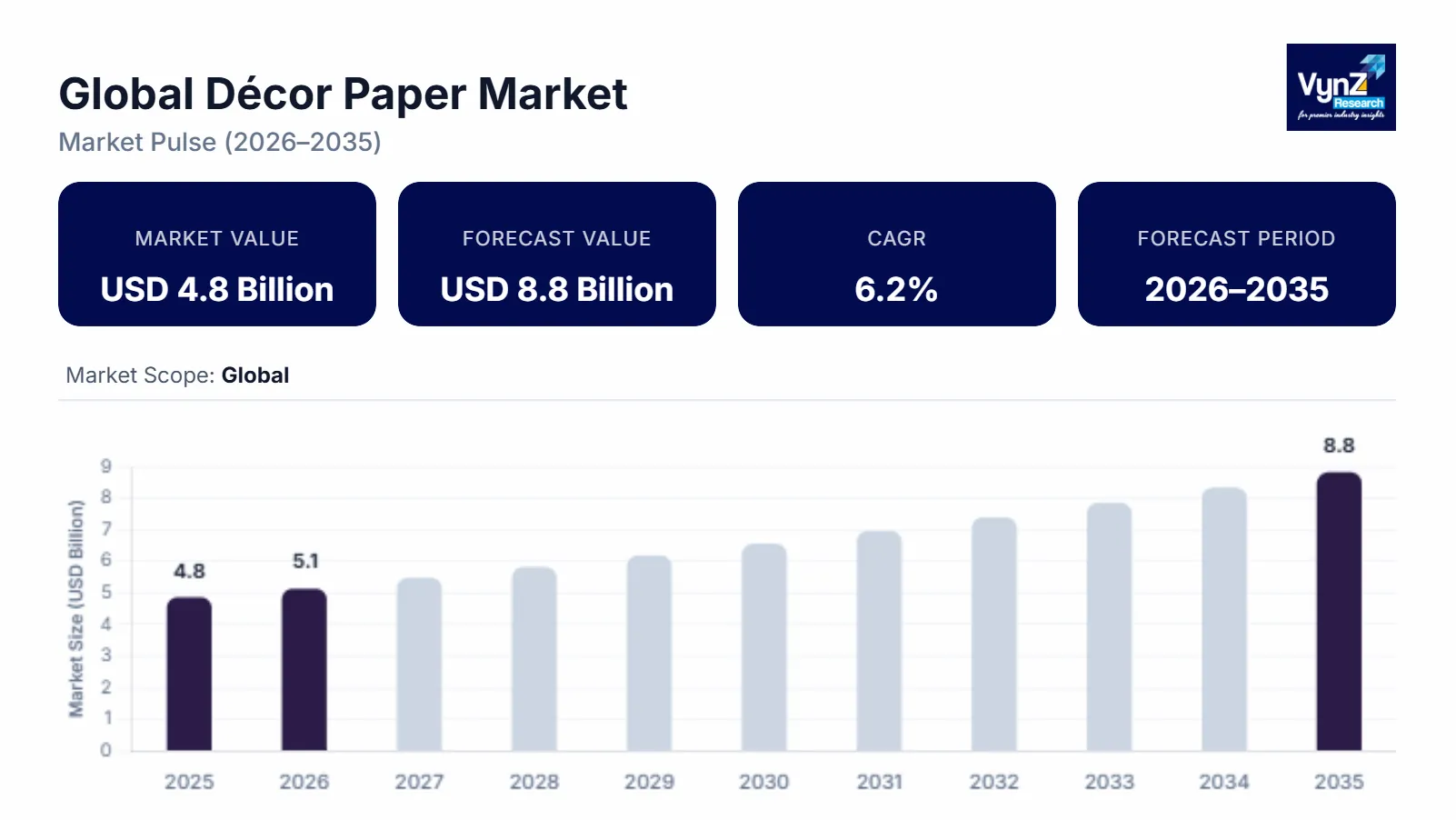

The global décor paper market which was valued at approximately USD 4.8 billion in 2025 and is estimated to rise further up to almost USD 5.11 billion by 2026, is projected to reach around USD 8.80 billion in 2035, expanding at a CAGR of about 6.2% during the forecast period 2026 to 2035.

The market is expanding fast because the demand for decorative laminates in furniture, paneling and modular interiors keeps going up and people are looking for sustainable surface materials. Urbanization, real estate growth, and an increasing adoption of digitally printed décor paper pushes the market in Asia Pacific, Europe, and North America, largely due to manufacturing strength and ongoing design modernization. At a government level, initiatives around sustainable forest management and circular economy practices are really shifting how material sourcing is being done in this décor paper sphere, which pushes companies toward certified feedstocks and lower emission production routes. Larger global frameworks for responsible forest usage, with sustainability guidelines, and green procurement rules are tightening the compliance bar for manufacturers. Expansion across Asia Pacific, Europe, and North America is being supported through industrial policy backing, infrastructure buildout, and steady demand for premium interior aesthetics, in general.

Global Décor Paper Market Dynamics

Market Trends

The design tastes changing, sustainability getting real attention and digital manufacturing being pulled in more directly point toward eco efficient and more highly customized surface solutions that match them but without the heavy footprint. One of the bigger shifts is a growing preference for sustainable and low emission decorative substrates showing how buyers are preferring environmentally responsible interior materials and certified raw sourcing. There’s also an emerging wave of digital printing technology getting adopted in décor uses, largely because precision printing systems have improved and the surfaces are easier to work with now. These changes are already steering product portfolios, pushing companies to build around customized textures, sharper visual appeal, and design solutions that fit together more smoothly, with evolving environmental compliance requirements and broader sustainable construction guidelines showing up in major economies.

Growth Drivers

The market keeps growing mainly because demand is expanding from furniture, interior design, and modular construction applications. This demand keeps feeding steady use in both residential and commercial project types. More money going into urban infrastructure, housing development, and commercial real estate is also speeding up expansion, especially in economies that are moving fast. There’s also a strong increasing interest in ecofriendly interior materials and end users seem to care about sustainability compliance, durability, and design flexibility at the same time. In addition, policy frameworks that promote green building benchmarks and responsible forestry management are helping substitution toward decorative paper-based solutions.

Market Restraints

Even with the outlook looking positive, there are still constraints that can slow things down. A big hurdle is the volatility in wood pulp and cellulose based raw material supply, which increases production costs and make profitability harder to predict. Environmental rules around forestry extraction and chemical usage in coating steps also add compliance pressure for manufacturers, especially where sustainability enforcement is strict. Several developing economies rely heavily on imported raw materials resulting in strained operations and cost swing disrupting supply chains.

Market Opportunities

There are openings in sustainable material innovation like development of bio-based resins, recyclable substrates, and low emission coating technologies that match the rising desire for interior solutions that meet environmental expectations. Firms that can deliver high performance and customizable decorative paper solutions should be in a good position to win business from furniture makers, interior designers, and modular construction groups. Another opportunity is the growth of digitally enabled décor printing solutions, where automation plus precision printing systems allow faster design cycles and better product differentiation allowing companies to iterate quickly instead of waiting. Also, more investments in urban development and green infrastructure initiatives across emerging economies are likely to boost adoption and support longer term revenue expansion through global value chains.

Global Décor Paper Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.8 Billion |

|

Revenue Forecast in 2035 |

USD 8.8 Billion |

|

Growth Rate |

6.2% |

|

Segments Covered in the Report |

Application, Raw Materials, Product Type, Weight, Industry, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Chiyoda Corporation, Felix Schoeller Group, ImPress Surfaces GmbH, KÄMMERER Paper GmbH, KJ Specialty Paper Co., Ltd., Neenah Paper and Packaging, Onyx Papers, Pudumjee Paper Products, Schattdecor, Stora Enso, Ved Cellulose Paper |

|

Customization |

Available upon request |

Global Décor Paper Market Segmentation

By Application

Continuous pressure laminates held the largest share in 2025, about 42% of total revenue, mostly because they’re used all over furniture surfaces, interior panels, and modular construction stuff where durability and visual steadiness really matter. The government backed infrastructure push and housing expansion programs in developing economies keeps the demand stable for this category. Meanwhile low-pressure laminates are expected to grow the quickest, with a CAGR around 6.8%, linked to cost effectiveness, a lighter framework and wider use in residential interior settings where affordability and layout flexibility are crucial. More investment in city housing projects and sustainable construction materials also makes this segment keep expanding across key regions.

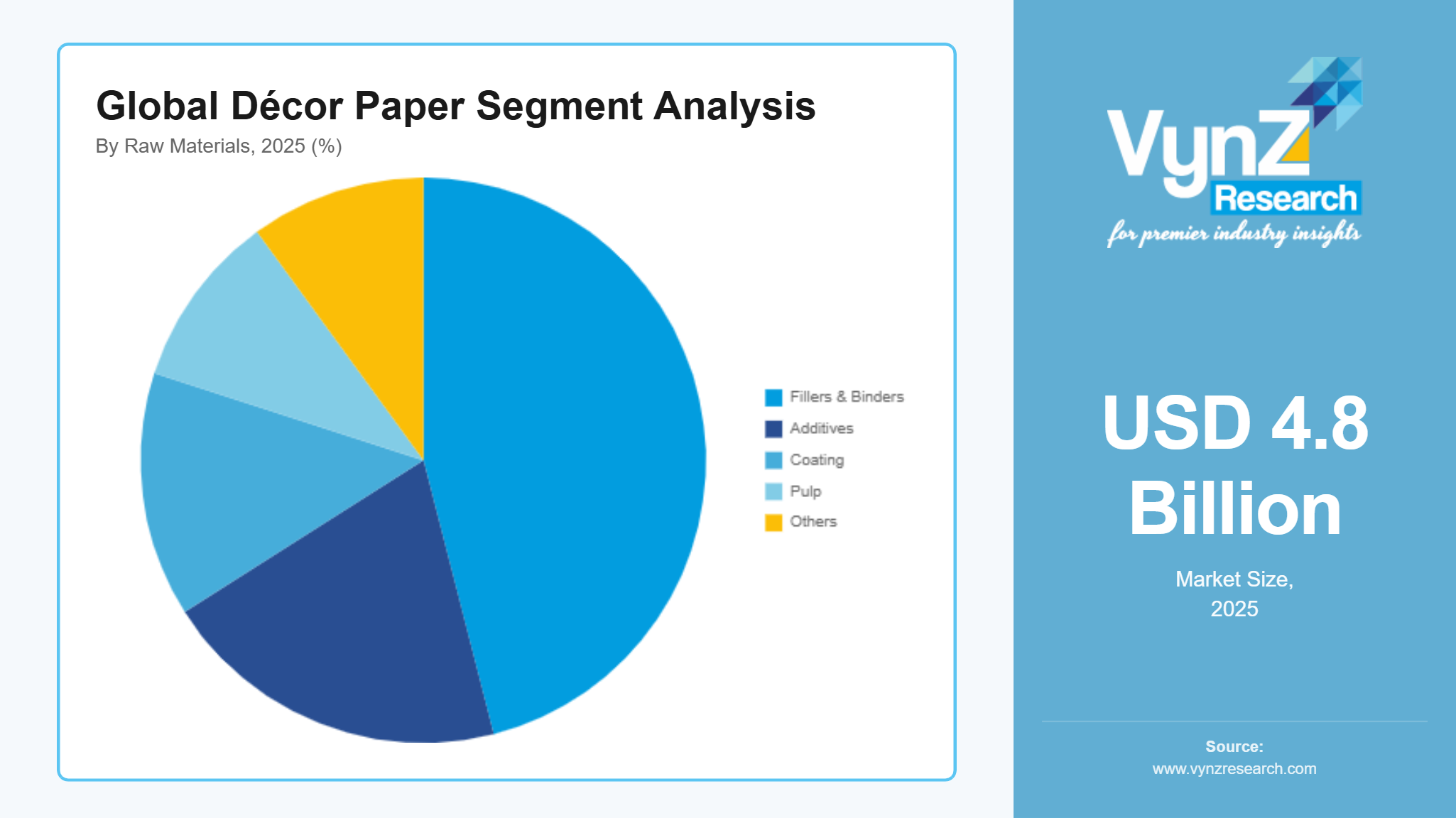

By Raw Materials

Pulp based materials were the dominant group in 2025, with roughly a 46% share, mainly due to strong availability, solid structural strength, and how often pulp gets blended into décor paper production steps. The sustainability rules that promote verified forestry sources and responsible pulp sourcing, and global environmental compliance programs are really helping keep long term demand steadier. For coatings, it is projected to be the fastest moving part, CAGR about 7.1% supported by the growing need for better surface toughness, moisture resistance, and improved print friendliness for decorative uses. Rising funding in advanced coating methods and ecofriendly chemical formulations is encouraging manufacturers across industrial production units.

By Product Type

Base paper for foil production held the largest market share in 2025, about 38% of total revenue due to extensive use in laminated furniture surfaces and interior design work that needs strong bonding and reliable durability. More furniture manufacturing activity and ongoing urban interior development projects keep supporting demand consistency in this space. Print base paper is expected to see the fastest growth, at a CAGR of 7.3%, due to the rising adoption of digitally printed décor options, customization trends, and improvements in high resolution printing. Government supported efforts that promote sustainable interior materials and modern building practices are also speeding up how deep this segment penetrates.

By End User

Furniture and cabinets took the largest share in 2025, around 44% of total revenue, driven by solid residential construction momentum, rising demand for homes in urban areas, and a stronger customer pull toward good looking durable interior furniture. Housing development schemes from governments, and smart city infrastructure initiatives, keep consumption fairly steady here. Wallcovering laminates are forecast to grow fastest, with a CAGR of 6.9%, powered by renovation activity, stronger take up of premium interior design, and increasing need for decorative surface tailoring in both commercial and residential areas. As real estate refurbishment cycles keep rolling, and sustainable interior upgrades become more common, long term growth stays supported across global markets.

Regional Insights

North America

North America accounted for approximately 29% of the market in 2025, driven by strong demand from the furniture manufacturing sector, modular interior development, and high adoption of engineered wood and laminate based surface solutions. Major industrial and urban hubs such as the United States metropolitan regions continue to support consistent consumption due to advanced interior design standards and strong remodeling activity. Government backed initiatives supporting sustainable building materials, along with environmental compliance frameworks issued by agencies such as the U.S. Environmental Protection Agency (EPA), are encouraging the use of low emission decorative materials in construction and furnishing applications. Increasing investments in smart housing infrastructure and digital printing-based décor solutions are further strengthening regional market performance across commercial and residential applications.

Europe

Europe accounted for approximately 22% of the global décor paper market in 2025, supported by mature construction ecosystems, strong furniture export industries, and stringent sustainability regulations governing material sourcing and production processes. Countries such as Germany, Italy, France, and the United Kingdom serve as key consumption hubs due to their well-established interior design and furniture manufacturing sectors. Regulatory frameworks aligned with European environmental directives and sustainable forestry management policies are significantly influencing the shift toward certified and ecofriendly decorative paper materials. Increasing renovation activities in residential and commercial infrastructure, combined with rising demand for premium interior aesthetics, is further contributing to stable market expansion across the region.

Asia Pacific

Asia Pacific held approximately 27% of the global décor paper market in 2025, driven by rapid urbanization, large scale residential construction, and expanding furniture manufacturing industries in China, India, Japan, and Southeast Asia. Major cities such as Shanghai, Mumbai, Tokyo, and Jakarta are witnessing strong demand for decorative laminates and surface finishing materials due to rising housing development and commercial infrastructure expansion. Government supported initiatives promoting affordable housing, smart city development, and sustainable construction practices are further strengthening material adoption. The region is also benefiting from increasing investments in manufacturing capabilities and growing penetration of digitally printed décor solutions, enhancing customization and design efficiency across industrial applications.

Rest of the World

The rest of the world, including Latin America, Middle East, and Africa, accounted for approximately 22% of the global décor paper market in 2025, with growth driven by gradual urbanization, infrastructure modernization, and increasing awareness of interior design solutions. Countries such as Brazil, Mexico, South Africa, and the United Arab Emirates are witnessing rising adoption of decorative laminates in residential and commercial construction projects. Government initiatives supporting housing development, trade expansion, and infrastructure investment are contributing to improved accessibility of décor paper products in these regions.

Competitive Landscape / Company Insights

The market is moderately competitive, with the presence of established international and regional manufacturers focusing on product innovation, sustainable material development, and expansion across high growth construction and furniture value chains. Companies are increasingly investing in advanced coating technologies, digital printing capabilities, and ecofriendly raw material sourcing to strengthen market positioning and compliance with global sustainability frameworks supported by environmental and forestry governance standards. Rising demand from furniture, interior design, and modular construction sectors is intensifying competition, while strategic partnerships, capacity expansion, and technology integration are further shaping competitive dynamics across developed and emerging markets.

Mini Profiles

Chiyoda Corporation focuses on engineered décor paper solutions and advanced surface materials, supported by strong industrial integration and cost-efficient production capabilities across diversified global supply chains.

Felix Schoeller Group operates in premium decorative paper segments, emphasizing high quality surface design, customization, and sustainable material innovation for furniture and interior applications across international markets.

ImPress Surfaces GmbH leverages advanced digital printing technologies and strong design capabilities to expand market presence in high end décor paper applications across Europe and export regions.

KÄMMERER Paper GmbH focuses on specialty decorative and technical paper solutions, supported by strong manufacturing expertise and consistent supply reliability for industrial laminate and surface applications.

KJ Specialty Paper Co. Ltd. operates in mass and mid-range décor paper segments, emphasizing cost efficiency, scalable production, and strong regional distribution networks across Asia Pacific markets.

Key Players

- Chiyoda Corporation

- Felix Schoeller Group

- ImPress Surfaces GmbH

- KÄMMERER Paper GmbH

- KJ Specialty Paper Co., Ltd.

- Neenah Paper and Packaging

- Onyx Papers

- Pudumjee Paper Products

- Schattdecor

- Stora Enso

- Ved Cellulose Paper

Recent Developments

In August 2025, Neenah Paper and Packaging expanded its décor paper production capabilities to strengthen supply for interior and laminate applications. The initiative focused on improving operational efficiency and meeting rising demand from furniture and construction sectors.

In May 2026, Onyx Papers enhanced its distribution network across key industrial regions to improve market penetration in decorative paper segments. The company also strengthened its product positioning in cost efficient and mid-range interior material solutions.

In November 2025, Pudumjee Paper Products upgraded its ecofriendly coating technologies to support sustainable décor paper manufacturing. The development aimed at improving surface durability and aligning with increasing demand for environmentally compliant interior materials.

In January 2026, Schattdecor expanded its digital printing and surface design capabilities to enhance customization in décor paper applications. The expansion supported stronger product differentiation in premium furniture and interior design markets.

In March 2025, Stora Enso invested in advanced sustainable pulp processing technologies to support high quality décor paper production. The move strengthened its focus on renewable raw materials and long-term environmental compliance in packaging and interior applications.

Global Décor Paper Market Coverage

Application Insight and Forecast 2026 - 2035

- Continuous Pressure Laminates

- Low-Pressure Laminates

- High-Pressure Laminates

Raw Materials Insight and Forecast 2026 - 2035

- Fillers & Binders

- Additives

- Coating

- Pulp

- Others

Product Type Insight and Forecast 2026 - 2035

- Uni Paper

- Edge Banding Paper

- Base Paper for Foil Production

- Absorbent Kraft Paper

- Print Base Paper

- Others

Weight Insight and Forecast 2026 - 2035

- Above 100 GSM

- 81–100 GSM

- 65–80 GSM

- Less than 65 GSM

Industry Insight and Forecast 2026 - 2035

- Household Type

- Commercial Type

End User Insight and Forecast 2026 - 2035

- Direct Printing

- Store Fixture

- Panelling

- Wallcovering Laminates

- Furniture and Cabinets

- Wallpaper

- Flooring

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Rest of the World

Global Décor Paper Market by Region

- North America

- By Application

- By Raw Materials

- By Product Type

- By Weight

- By Industry

- By End User

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Application

- By Raw Materials

- By Product Type

- By Weight

- By Industry

- By End User

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Application

- By Raw Materials

- By Product Type

- By Weight

- By Industry

- By End User

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Application

- By Raw Materials

- By Product Type

- By Weight

- By Industry

- By End User

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Décor Paper Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Application

1.2.2. By

Raw Materials

1.2.3. By

Product Type

1.2.4. By

Weight

1.2.5. By

Industry

1.2.6. By

End User

1.2.7. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Application

5.1.1. Continuous Pressure Laminates

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Low-Pressure Laminates

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. High-Pressure Laminates

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Raw Materials

5.2.1. Fillers & Binders

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Additives

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Coating

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Pulp

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Others

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Product Type

5.3.1. Uni Paper

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Edge Banding Paper

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Base Paper for Foil Production

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Absorbent Kraft Paper

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Print Base Paper

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Others

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Weight

5.4.1. Above 100 GSM

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. 81–100 GSM

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. 65–80 GSM

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Less than 65 GSM

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Industry

5.5.1. Household Type

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial Type

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. Direct Printing

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Store Fixture

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Panelling

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

5.6.4. Wallcovering Laminates

5.6.4.1. Market Definition

5.6.4.2. Market Estimation and Forecast to 2035

5.6.5. Furniture and Cabinets

5.6.5.1. Market Definition

5.6.5.2. Market Estimation and Forecast to 2035

5.6.6. Wallpaper

5.6.6.1. Market Definition

5.6.6.2. Market Estimation and Forecast to 2035

5.6.7. Flooring

5.6.7.1. Market Definition

5.6.7.2. Market Estimation and Forecast to 2035

5.7. By Region

5.7.1. North America

5.7.1.1. Market Definition

5.7.1.2. Market Estimation and Forecast to 2035

5.7.2. Europe

5.7.2.1. Market Definition

5.7.2.2. Market Estimation and Forecast to 2035

5.7.3. Asia Pacific

5.7.3.1. Market Definition

5.7.3.2. Market Estimation and Forecast to 2035

5.7.4. Rest of the World

5.7.4.1. Market Definition

5.7.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Application

6.2. By

Raw Materials

6.3. By

Product Type

6.4. By

Weight

6.5. By

Industry

6.6. By

End User

6.7. By

Region

6.7.1.

U.S. Market Estimate and Forecast

6.7.2.

Canada Market Estimate and Forecast

6.7.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Application

7.2. By

Raw Materials

7.3. By

Product Type

7.4. By

Weight

7.5. By

Industry

7.6. By

End User

7.7. By

Region

7.7.1.

Germany Market Estimate and Forecast

7.7.2.

France Market Estimate and Forecast

7.7.3.

U.K. Market Estimate and Forecast

7.7.4.

Italy Market Estimate and Forecast

7.7.5.

Spain Market Estimate and Forecast

7.7.6.

Russia Market Estimate and Forecast

7.7.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Application

8.2. By

Raw Materials

8.3. By

Product Type

8.4. By

Weight

8.5. By

Industry

8.6. By

End User

8.7. By

Region

8.7.1.

China Market Estimate and Forecast

8.7.2.

Japan Market Estimate and Forecast

8.7.3.

India Market Estimate and Forecast

8.7.4.

South Korea Market Estimate and Forecast

8.7.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Application

9.2. By

Raw Materials

9.3. By

Product Type

9.4. By

Weight

9.5. By

Industry

9.6. By

End User

9.7. By

Region

9.7.1.

Brazil Market Estimate and Forecast

9.7.2.

Saudi Arabia Market Estimate and Forecast

9.7.3.

South Africa Market Estimate and Forecast

9.7.4.

U.A.E. Market Estimate and Forecast

9.7.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Chiyoda Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Felix Schoeller Group

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

ImPress Surfaces GmbH

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

KÄMMERER Paper GmbH

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

KJ Specialty Paper Co., Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Neenah Paper and Packaging

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Onyx Papers

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Pudumjee Paper Products

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Schattdecor

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Stora Enso

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Ved Cellulose Paper

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Décor Paper Market