Hydrogen Storage Infrastructure Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Storage Type (Compressed Hydrogen Storage, Liquefied Hydrogen Storage, Solid-State Storage Systems), by Storage Form (Physical Storage Systems, Material-Based Storage Solutions), by Technology (Compression Systems, Liquefaction Systems, Adsorption-Based Systems, Cryogenic Pressurized Systems), by End User (Oil & Gas Companies, Utilities, Transportation Sector, Industrial Manufacturers, Energy Storage Operators)

| Status : Published | Published On : May, 2026 | Report Code : VREP3069 | Industry : Energy & Power | Available Format :

|

Page : 154 |

Hydrogen Storage Infrastructure Market Overview

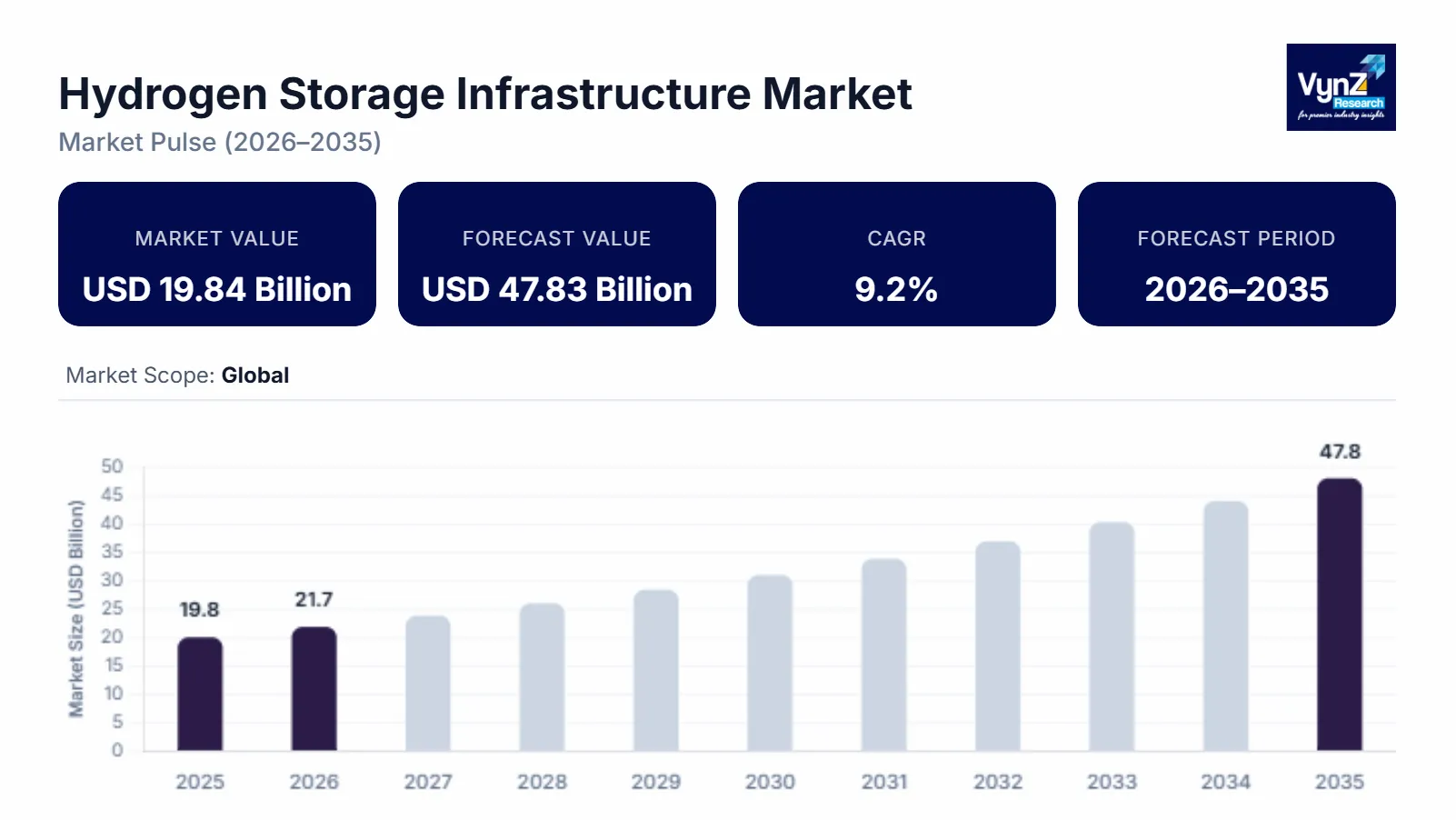

The global hydrogen storage infrastructure market, which was valued at approximately USD 19.84 billion in 2025 and is estimated to reach around USD 21.66 billion in 2026, is projected to reach approximately USD 47.83 billion by 2035, expanding at a CAGR of about 9.2% during the forecast period from 2026 to 2035.

Market expansion is driven by faster deployment of green hydrogen production projects and higher demand for large scale energy storage solutions. The International Energy Agency (IEA) hydrogen reports keep indicating that hydrogen adoption should accelerate inside industrial decarbonization programs which increases the demand for brand new infrastructure.

Government programs around net zero emissions and the broader move toward cleaner fuels are also pushing adoption forward in several big regions. Hydrogen mission programs, national fuel cell roadmaps and public financing toward electrolyzer installation and storage deployment helps speed up the overall infrastructure buildout. Policy backing from energy ministries and clean energy agencies is further making large scale investment decisions feel more realistic, especially for compression systems, liquefaction units, and underground hydrogen storage facilities.

Hydrogen Storage Infrastructure Market Dynamics

Market Trends

The market is seeing some noticeable shifts in both technology use and procurement behavior mainly in high pressure gaseous storage and cryogenic liquid hydrogen systems. Solid state storage ideas are shaping large scale underground hydrogen storage that match evolving preferences for long duration energy storage efficiency, safety, and overall cost optimization. The International Energy Agency (IEA) hydrogen outlook notes indicate at stronger hydrogen integration into power generation and industrial systems. Another emerging trend is digital monitoring and AI enabled storage system optimization pushed by technological innovation that align with hydrogen safety standards.

Growth Drivers

Market growth is mostly supported by rising green hydrogen production capacity that can meet large demand across industrial decarbonization, transport, and power generation. More investments in hydrogen hubs, electrolyzer deployment, and even pipeline infrastructure, government backed hydrogen mission programs and clean energy transition strategies are reinforcing large scale buildouts. Increasing demand for energy security and grid balancing pushes utilities, industrial users, and mobility operators to focus on low carbon compliance and long duration energy storage. It is further boosted by energy department initiatives and climate neutrality commitments.

Market Restraints / Challenges

The faces hurdles in expansion from the high capital intensity of storage systems like cryogenic tanks and underground caverns that hurt profitability and limit market penetration, especially for early-stage hydrogen economy projects and developing regions. Regulatory complexity around hydrogen transport and safety certification can stretch deployment timelines. Operational issues with specialized materials such as advanced composites and high-grade steel faced by manufacturers and suppliers cause significant constraints. Limited availability of a skilled hydrogen engineering workforce can create cost pressure, cause project delays, and reduce scalability.

Market Opportunities

The market does offer significant opportunities in large scale hydrogen storage hubs, largely because renewable energy penetration keeps rising and industrial decarbonization is still a major requirement. Companies that provide modular, scalable, and high-pressure storage solutions are in a better position to win incremental demand from utilities, refineries, steel manufacturers, and transport operators. Another opportunity is integrated hydrogen energy ecosystems, where investments are moving toward ammonia-based storage, liquid hydrogen export terminals, and smart hydrogen grids that are opening paths for better margins and longer-term contracts. Digital monitoring upgrades, automation, and AI driven energy optimization are also expected to improve operational efficiency, making commercial adoption easier.

Global Hydrogen Storage Infrastructure Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 19.84 Billion |

|

Revenue Forecast in 2035 |

USD 47.83 Billion |

|

Growth Rate |

9.2% |

|

Segments Covered in the Report |

Storage Type, Storage Form, Technology, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Air Liquide, Bloom Energy, Chart Industries, Engie, Linde plc, Nel ASA, Nikola Corporation, Plug Power, Siemens Energy, Thyssenkrupp Nucera |

|

Customization |

Available upon request |

Hydrogen Storage Infrastructure Market Segmentation

By Storage Type

Compressed hydrogen storage held the biggest share in 2025, around 48% of total revenue mainly due to broad rollout in industrial hydrogen use and transport fueling set ups along with lower upfront capital needs and safety standards that follow national hydrogen safety regulations and energy department guidelines.

Liquefied hydrogen storage is predicted to grow faster with an estimated CAGR of 23.6% from 2026 to 2035 due to higher demand for long distance hydrogen hauling and bigger export-import hydrogen supply chains. There are also strong investments in hydrogen liquefaction terminals and national clean energy export strategies, which is helping especially in energy exporting countries and industrial clusters that are focused on low carbon fuel distribution.

By Storage Form

Physical storage systems had the largest share in 2025, roughly 72%, because of heavy deployment of high-pressure tanks and cryogenic storage units across industrial hydrogen production sites and energy storage locations. Government backed hydrogen infrastructure plans, and safety certification rules from national energy agencies make physical storage technologies easier to scale, across utilities and industrial segments.

Material based hydrogen storage is projected to grow faster, with an estimated CAGR of 24.1% during 2026 to 2035, supported by improvements in metal hydrides and chemical storage materials. More spending in next generation hydrogen carriers and research programs led by national laboratories and clean energy agencies is promoting commercialization and use cases in mobility and distributed energy systems.

By Technology

Compression systems got the largest market share in 2025, about 45%, due to common deployment in hydrogen refueling stations and industrial gas applications for its infrastructure, cost efficiency and compatibility with hydrogen safety regulations released by national energy ministries and environmental agencies.

Liquefaction systems are expected to post the fastest growth, with a CAGR of 25.2% from 2026 to 2035, driven by a rising need for high density hydrogen storage and longer-range energy transport approaches. Government backed hydrogen export projects plus big renewable hydrogen production investments are also accelerating how quickly liquefaction infrastructure gets rolled out across major energy transition economies.

By End User

Oil & gas companies accounted for the largest share in 2025, around 34%, supported by deep integration of hydrogen into refining processes and decarbonization of existing industrial operations. National hydrogen blending policies and industrial transition programs keep reinforcing adoption inside older energy value chains.

Utilities and energy storage operators are expected to grow at the fastest pace, with an estimated CAGR of 26.3% during 2026 to 2035, driven by increasing renewable energy and grid balancing needs. Government backed clean energy transition programs, plus large-scale hydrogen hub developments, are speeding up adoption of hydrogen storage systems for seasonal energy storage and grid stability uses across North America, Europe, and Asia Pacific.

Regional Insights

North America

North America accounted for approximately 37% of the hydrogen storage infrastructure market in 2025, driven by strong hydrogen hub development programs, large scale industrial decarbonization initiatives, and rapid investment in clean fuel infrastructure across the United States and Canada. Key industrial clusters in Texas, California, and Alberta continue to support large scale deployment of hydrogen storage systems linked to refining, power generation, and mobility applications. Government initiatives such as the U.S. Department of Energy hydrogen hub program and national clean hydrogen strategies are encouraging investments in compression, liquefaction, and underground storage systems. Expansion of private sector partnerships and tax credit driven clean hydrogen production incentives is further strengthening regional market growth.

Europe

Europe accounted for approximately 32% of the hydrogen storage infrastructure market in 2025, supported by aggressive decarbonization targets, strong renewable energy penetration, and large-scale hydrogen infrastructure investments across Germany, France, the United Kingdom, and the Netherlands. The European Union hydrogen strategy and REPowerEU framework are accelerating deployment of hydrogen valleys, storage terminals, and cross-border hydrogen transport networks. Increasing industrial demand for green hydrogen in steel, chemicals, and refining sectors is driving consistent storage infrastructure expansion. Public funding from national energy ministries and EU climate programs is further reinforcing adoption of advanced storage technologies, including liquefaction and underground hydrogen storage systems.

Asia Pacific

Asia Pacific accounted for approximately 28% of the hydrogen storage infrastructure market in 2025, driven by rapid industrialization, expanding renewable energy capacity, and large-scale hydrogen economy initiatives across China, Japan, South Korea, and India. Government led hydrogen mission programs and national energy transition roadmaps are accelerating investments in hydrogen production, storage, and distribution infrastructure. Strong demand from industrial manufacturing hubs and growing adoption of fuel cell mobility systems are further supporting market expansion. National ministries of energy and public clean fuel programs are encouraging development of hydrogen refueling stations and large-scale storage facilities integrated with renewable energy systems.

Rest of the World

Rest of the world including the Middle East, Latin America, and Africa accounted for approximately 3% of the hydrogen storage infrastructure market in 2025, driven by emerging hydrogen export projects, renewable energy integration initiatives, and early-stage clean fuel adoption programs. Countries such as Saudi Arabia, the United Arab Emirates, and Brazil are investing in large scale hydrogen production and export infrastructure supported by national diversification strategies and clean energy transition plans. Government backed sovereign energy programs and international climate cooperation frameworks are encouraging pilot scale hydrogen storage projects.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global engineering firms, energy majors, and emerging clean hydrogen specialists focusing on storage system innovation, cost reduction, and large-scale infrastructure deployment. Companies are increasingly investing in R&D, advanced materials, and digital monitoring capabilities to strengthen their market position. Government backed hydrogen strategies and national energy transition roadmaps supported by agencies such as the International Energy Agency (IEA) and national energy ministries are encouraging large scale investment. Strategic partnerships, project financing initiatives, and integrated hydrogen value chain development are further intensifying competition across global markets.

Mini Profiles

Air Liquide focuses on industrial hydrogen production and storage infrastructure solutions, supported by strong global distribution networks and established brand recognition across energy, refining, and clean hydrogen ecosystems worldwide.

Bloom Energy operates in premium hydrogen and fuel cell segments, emphasizing high efficiency power generation systems and integrated energy solutions designed for decentralized industrial and commercial applications with strong performance focus.

Chart Industries leverages cryogenic engineering expertise and strategic partnerships to expand market presence, delivering hydrogen liquefaction, compression, and storage equipment across global energy and industrial gas infrastructure markets.

Engie focuses on renewable hydrogen production and storage infrastructure development, supported by strong global energy project capabilities and cost-efficient integrated energy transition solutions across utilities and industrial sectors.

Linde plc operates in large scale industrial gas and hydrogen infrastructure markets, emphasizing advanced storage technologies, global supply chain strength, and high-performance hydrogen delivery systems across multiple end use industries.

Key Players

- Air Liquide

- Bloom Energy

- Chart Industries

- Engie

- Linde plc

- Nel ASA

- Nikola Corporation

- Plug Power

- Siemens Energy

- Thyssenkrupp Nucera

Recent Developments

In February 2025, Air Liquide advanced its hydrogen infrastructure strategy by expanding low-carbon hydrogen production projects across Europe. The initiative focuses on large-scale electrolyzer deployment and strengthening cross-border hydrogen supply networks to support industrial decarbonization and energy transition goals.

In February 2025, Bloom Energy expanded its hydrogen-linked clean power ecosystem through new partnerships focused on carbon capture and low-emission energy systems for data centers. The development strengthens its role in supplying hydrogen-enabled fuel cell solutions for high-energy digital infrastructure.

In April 2025, Fluxys continued scaling its hydrogen infrastructure projects across Europe by advancing hydrogen transmission network development and CO₂/hydrogen corridor integration. The company is strengthening its role in enabling cross-border hydrogen transport systems supporting industrial decarbonization.

In 2025, ITM Power expanded its electrolyzer manufacturing and hydrogen production capabilities through its Sheffield-based facilities. The development supports rising demand for PEM-based hydrogen systems used in large-scale storage and power-to-X applications across global energy markets.

In August 2025, Linde plc strengthened its global hydrogen infrastructure footprint through continued investments in hydrogen production, storage, and distribution systems across industrial clusters. The expansion reinforces its leadership in large-scale industrial gas networks supporting clean hydrogen adoption.

Global Hydrogen Storage Infrastructure Market Coverage

Storage Type Insight and Forecast 2026 - 2035

- Compressed Hydrogen Storage

- Liquefied Hydrogen Storage

- Solid-State Storage Systems

Storage Form Insight and Forecast 2026 - 2035

- Physical Storage Systems

- Material-Based Storage Solutions

Technology Insight and Forecast 2026 - 2035

- Compression Systems

- Liquefaction Systems

- Adsorption-Based Systems

- Cryogenic Pressurized Systems

End User Insight and Forecast 2026 - 2035

- Oil & Gas Companies

- Utilities

- Transportation Sector

- Industrial Manufacturers

- Energy Storage Operators

Global Hydrogen Storage Infrastructure Market by Region

- North America

- By Storage Type

- By Storage Form

- By Technology

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Storage Type

- By Storage Form

- By Technology

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Storage Type

- By Storage Form

- By Technology

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Storage Type

- By Storage Form

- By Technology

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Hydrogen Storage Infrastructure Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Storage Type

1.2.2. By

Storage Form

1.2.3. By

Technology

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Storage Type

5.1.1. Compressed Hydrogen Storage

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Liquefied Hydrogen Storage

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Solid-State Storage Systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Storage Form

5.2.1. Physical Storage Systems

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Material-Based Storage Solutions

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Compression Systems

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Liquefaction Systems

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Adsorption-Based Systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Cryogenic Pressurized Systems

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Oil & Gas Companies

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Utilities

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Transportation Sector

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Industrial Manufacturers

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Energy Storage Operators

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Storage Type

6.2. By

Storage Form

6.3. By

Technology

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Storage Type

7.2. By

Storage Form

7.3. By

Technology

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Storage Type

8.2. By

Storage Form

8.3. By

Technology

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Storage Type

9.2. By

Storage Form

9.3. By

Technology

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Air Liquide

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bloom Energy

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Chart Industries

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Engie

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Linde plc

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Nel ASA

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Nikola Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Plug Power

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Siemens Energy

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Thyssenkrupp Nucera

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Hydrogen Storage Infrastructure Market