Mining Drilling Tools Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Tool Type (Down-the-hole (DTH), Top hammer tools, Rotary drill bits, Others), by Mining Type (Surface mining, Underground mining), by Application (Production / blast-hole drilling, Mineral exploration, Grade control and development drilling), by End-Use Industry (Metal mining, Coal mining, Quarrying & aggregates)

| Status : Published | Published On : Apr, 2026 | Report Code : VREP3067 | Industry : Energy & Power | Available Format :

|

Page : 195 |

Mining Drilling Tools Market Overview

The mining drilling tools market which was valued at approximately USD 6.7 billion in 2025 and is estimated to reach around USD 7.2 billion in 2026, is projected to reach close to USD 12.2 billion by 2035, expanding at a CAGR of about 5.9% during the forecast period from 2026 to 2035.

The market is primarily driven by sustained demand for metals and minerals across infrastructure, manufacturing, and the energy transition, as both surface and underground operations rely on continuous drilling for exploration, grade control, development, and production blasting. Rising investment in copper and other critical minerals is increasing drilling intensity and pushing operators toward higher-performance consumables that can improve penetration rates and deliver consistent hole quality in harder and more abrasive formations. The adoption of automated and digitally enabled drilling is rapidly expanding the need for tooling that supports repeatable performance, reduced deviation, and data-driven optimization of cost-per-meter, particularly in large, high-utilization fleets.

In addition, the trend toward deeper and more complex ore bodies is increasing wear rates and downtime sensitivity, strengthening demand for premium bits, hammers, rods, and wear parts engineered for longer service life. Increasing focus on productivity, safety, and emissions reduction is also accelerating electrification, especially in underground mines supporting demand for durable consumables compatible with modern electric drill rigs and higher utilization cycles.

Mining Drilling Tools Market Dynamics

Market Trends

A key trend in mining drilling tools is tighter integration with automated and digitally enabled drilling. As surface and underground operations deploy autonomous or semi-autonomous rigs, tooling is increasingly specified alongside data-driven drilling optimization focused on consistent energy transfer, reduced deviation, improved hole quality, and repeatable outcomes across shifts and operators. Mines are also adopting structured tool management programs (standardized tool selection, measured performance tracking, and planned change-outs) to reduce non-productive time and stabilize cost-per-meter. In parallel, electrification is expanding particularly in underground mines driving demand for tools that can sustain high utilization rates while supporting lower-maintenance fleets and constrained operating environments. Sandvik AB’s €80 million DataDrive’31 program (2025–2031) is a strategic investment focused on advancing digitalization and automation in mining operations. The initiative is aimed at integrating data-driven technologies, AI, and real-time analytics into drilling equipment, enabling smarter and more autonomous drilling processes. Manufacturers continue to improve carbide grades, button geometries, heat treatment, and wear-resistant features to extend service life in abrasive formations, enabling higher penetration rates while reducing the frequency of bit changes and associated downtime.

Growth Drivers

Expanding mineral exploration and mine development activity is a major growth driver for mining drilling tools because exploration drilling, grade control, and production drilling directly translate into recurring demand for consumables (bits, rods/tubes, hammers, and related wear parts). While financing conditions have been volatile, global nonferrous exploration budgets remain substantial; for example, S&P Global Market Intelligence reported exploration budgets of about USD 12.5 billion in 2024. Beyond exploration, sustaining capital at producing mines supports ongoing replacement demand as drilling is a continuous part of drill-and-blast cycles and mine planning (including pre-split, buffer, and production drilling). Demand is further supported by the push for critical minerals especially copper, nickel, and lithium where harder rock conditions and deeper targets increase the need for premium tooling that improves penetration rates and tool life. In addition, larger mines increasingly use performance-based procurement and contractor frameworks that favor suppliers capable of providing consistent quality, reliable delivery, and on-site technical support.

Market Restraints / Challenges

High operating costs and performance variability across geology are key challenges in the mining drilling tools market. Tool wear rates can increase sharply in abrasive or high-strength rock, raising cost-per-meter and creating downtime for tool changes especially in deep or remote operations where logistics, inventory planning, and service access are complex. In addition, procurement teams often face a trade-off between lower-priced tools and premium tooling that offers longer life and higher penetration, making total cost of ownership analysis critical but sometimes difficult to standardize across sites and contractors. Market demand is also sensitive to commodity price cycles and mining capital expenditure, when prices fall, exploration and development programs are frequently deferred, reducing drilling activity and near-term tooling consumption. Volatility in raw material costs, as well as supply chain disruptions for specialty materials, can influence tool pricing and supplier margins and may lead to longer lead times in certain product categories.

Market Opportunities

Growing adoption of automated drilling, digital mine operations, and electrified equipment creates strong opportunities for drilling tool manufacturers and service providers. Mines are increasingly looking for tooling systems that can deliver predictable penetration rates, support repeatable hole quality, and enable proactive maintenance planning through performance tracking and condition monitoring. This is expanding demand for premium consumables, tool-life optimization programs, and integrated tools and service offerings, particularly in large surface mines and mechanized underground operations where even small productivity gains translate into material value. Governments and mining companies are actively driving mineral exploration and mine development through targeted initiatives and long-term programs. In India, mining investment proposals worth ₹56,414 crore highlight strong policy and institutional support for exploration activities. Opportunities also exist in customizing tooling to site-specific rock conditions, improving button and bit designs for harder formations, and offering local regrinding and repair services where applicable to extend usable life. As operators target lower emissions and better worker safety, electrification especially underground supports demand for high-durability tooling that sustains higher utilization with fewer unplanned stoppages, while supplier-managed inventory models and on-site technical support can further strengthen customer retention.

Global Mining Drilling Tools Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.7 Billion |

|

Revenue Forecast in 2035 |

USD 12.2 Billion |

|

Growth Rate |

5.9% |

|

Segments Covered in the Report |

Tool Type, Drilling Method, Mining Type, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

|

Key Companies |

Sandvik, Epiroc, Boart Longyear, Caterpillar, Komatsu, FLSmidth, Furukawa Rock Drill, Robbins (Epiroc), Normet, Mincon Group |

|

Customization |

Available upon request |

Mining Drilling Tools Market Segmentation

By Type

Down-the-hole (DTH) tools are the largest category with a market share of about 40% in 2025, as DTH hammers and bits are widely used for high-volume blast-hole drilling in surface mines where consistent penetration, hole straightness, and repeatable fragmentation outcomes are critical. DTH systems place the hammer directly behind the bit, enabling efficient energy transfer in hard rock and supporting high utilization in open-pit fleets, which drives recurring demand for bits, hammers, and wear components.

Top hammer tools are the fastest-growing category with a CAGR of 6.2% during the forecast period, driven by fleet modernization and increasing adoption of automated drilling in bench drilling, development drilling, and production drilling across a broad range of hole diameters. As mines standardize drilling KPIs and target lower cost-per-meter, demand is rising for optimized top hammer tool strings (bits, rods, couplings, shank adapters) that deliver consistent hole quality, reduced deviation, and longer service life through improved carbide grades and wear-resistant designs.

By System Type

Surface mining is the larger category with a market share of about 60% in 2025, as open-pit operations require continuous, high-meterage blast-hole and pre-split drilling to sustain production, which drives high recurring consumption of bits, hammers, rods, and related wear parts. The typically higher utilization of surface drill fleets and larger hole diameters also increase replacement frequency, supporting a sizeable aftermarket for drilling consumables.

Underground mining is the faster-growing category with a CAGR of 6.5% during the forecast period, supported by deeper mining, rising mechanization, and growing deployment of automated and battery-electric drill rigs in hard-rock operations. Underground environments place a premium on reliable hole accuracy and longer tool life to reduce time-consuming change-outs, which is increasing demand for premium consumables and supplier-led tool management programs that improve drilling consistency and reduce non-productive time.

By Application

Production and blast-hole drilling is the largest category with a market share of about 55% in 2025, as operating mines perform drilling continuously to support drill-and-blast cycles and maintain output, resulting in steady replacement demand for DTH consumables, rotary bits, drill rods, shank adapters, and related wear parts. Tooling is selected based on rock hardness, abrasion, and hole diameter, and mines increasingly prioritize hole quality and deviation control because these factors influence blasting outcomes, wall stability, and downstream loading and hauling efficiency.

Mineral exploration is the fastest-growing category during the forecast period, driven by continued exploration and reserve replacement programs for copper, gold, lithium, and other critical minerals. Exploration drilling requires specialized consumables to support core recovery, sample quality, and drilling efficiency particularly in deeper targets and harder formations while remote project locations increase the value of durable tooling, reliable supply, and local technical support to minimize downtime during drilling campaigns.

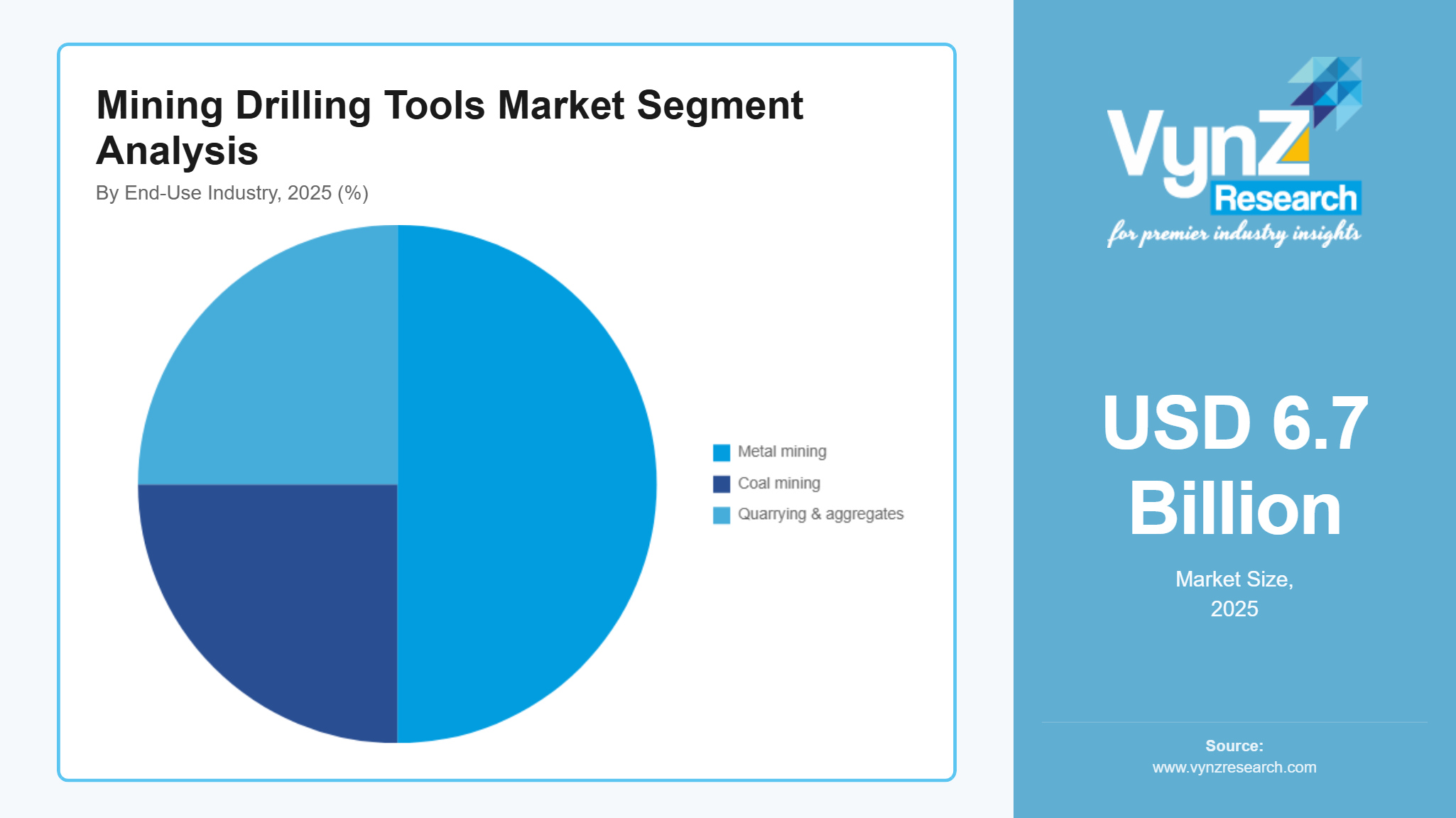

By End-Use Industry

Metal mining is the largest category with a market share of about 50% in 2025, as hard-rock operations for copper, iron ore, gold, nickel, and other base metals typically run large drilling fleets across both surface and underground sites and require continuous consumable replacement to maintain production schedules. The prevalence of hard and abrasive formations in many metal mines increases wear rates, supporting demand for premium tools and service programs focused on lowering total cost of ownership.

Quarrying and aggregates are the fastest-growing category during the forecast period, supported by sustained construction demand and infrastructure investment that increase output requirements for crushed stone, cement raw materials, and industrial minerals. Quarry operators are increasingly adopting modern drill rigs and standardized drilling practices, which is raising demand for tooling that delivers high penetration rates, consistent hole geometry, and longer service life to minimize downtime and improve blasting efficiency.

Regional Insights

North America

North America accounted for approximately 30% of the market in 2025, driven by large-scale mining operations, strong exploration activity, and steady replacement demand from high-utilization drill fleets across the United States and Canada. Strong demand from major mining regions in Nevada, Arizona, Ontario, and Quebec continues to support market growth. According to the Government of Canada, critical mineral development programs and exploration incentives, including multi-billion-dollar investments under national critical minerals strategies, are supporting drilling and mine expansion activities across the region.

Government initiatives, combined with rising adoption of automated drilling systems and productivity-focused mining operations, are encouraging investments in premium drilling consumables and supplier-led tool management services.

Asia-Pacific

Asia Pacific accounted for approximately 27% of the market in 2025, supported by rising mining production, expanding exploration activities, and increasing investments in mechanized drilling across China, India, and Australia. Increasing adoption across iron ore, coal, copper, lithium, and gold mining operations is driving consistent demand for drilling consumables and rock tools. According to the Government of India, the National Critical Mineral Mission launched in 2025 includes investments of over ₹16,000 crore to strengthen mineral exploration and mining infrastructure development.

Government support, along with rising demand for critical minerals and ongoing mine modernization programs, is accelerating adoption of high-performance drilling tools designed to improve penetration rates, drilling accuracy, and operational efficiency.

Europe

Europe accounted for approximately 16% of the market in 2025, driven by quarrying operations, underground mining activity, and increasing focus on operational efficiency and sustainable mining practices. Demand remains strong across Sweden, Finland, Germany, and other industrial mining regions. According to the European Union’s Critical Raw Materials Act, investments exceeding €10 billion are planned to strengthen domestic mining, mineral processing, and recycling capacity across Europe.

Growth in Europe is supported by modernization of mining fleets, increasing use of data-driven drilling technologies, and strong demand for premium consumables that reduce downtime and improve drilling performance in hard-rock applications.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, accounted for approximately 8% of the market in 2025, supported by expanding mining and quarrying activities across copper, gold, lithium, and iron ore projects. Countries such as Chile, Peru, Brazil, South Africa, and Saudi Arabia continue to invest in mining infrastructure and fleet modernization, supporting demand for drilling consumables and rock tools.

Increasing exploration spending, infrastructure development, and modernization of drilling operations are expected to create long-term opportunities across these regions. Collectively, the above-mentioned regional markets account for nearly 81% of the global mining drilling tools market, while the remaining share is distributed among smaller developing markets worldwide.

Competitive Landscape / Company Insights

The mining drilling tools market is moderately consolidated in nature, reflecting a balanced mix of large global players and numerous regional and local manufacturers. Major companies dominate the high-end segment by offering advanced, technology-driven drilling solutions, strong service networks, and integrated offerings that combine tools with maintenance and performance monitoring. Their ability to invest in innovation and provide customized solutions gives them a competitive edge, especially in large-scale and mechanized mining operations. Similarly, the market remains partially fragmented due to the presence of smaller players that cater to cost-sensitive segments, particularly in standard consumables such as drill bits, rods, and accessories. These companies often compete on pricing, local availability, and quick service support, making them relevant in emerging and price-conscious markets. Additionally, regional suppliers play a key role in meeting site-specific requirements and maintaining close customer relationships.

Mini Profiles

Sandvik AB is a major supplier of rock tools and drilling consumables used in surface and underground mining, including top hammer and DTH tooling systems.

Epiroc AB provides rock excavation and drilling solutions for surface and underground mining, including drilling consumables and rock tools designed to improve productivity, safety, and operational consistency.

Boart Longyear Group Ltd. is a well-known provider of drilling services and drilling products for mineral exploration and production, with a strong presence in diamond drilling consumables and tooling used in exploration and resource definition programs.

Caterpillar Inc. participates in the broader mining drilling ecosystem through its mining equipment platforms, technology solutions, and aftermarket services that support drilling and blasting value chains at mine sites.

Komatsu Ltd. provides mining equipment and technology solutions for surface and underground operations and supports drilling-related productivity initiatives through integrated mine planning, fleet management, and lifecycle services.

Key Players

- Sandvik AB

- Epiroc AB

- Boart Longyear Group Ltd.

- Caterpillar Inc.

- Komatsu Ltd.

- FLSmidth & Co. A/S

- Furukawa Rock Drill Co., Ltd.

- Mincon Group plc

- Robit Plc

- Rockmore International, Inc.

- Center Rock, Inc.

Recent Developments

In February 2025, Sandvik AB announced it will showcase several new rock tools and drilling solutions at Bauma 2025, including updates to top hammer tool systems and a new DTH hammer and bit family, alongside parts and service offerings aimed at improving drilling productivity and sustainability.

In February 2025, Epiroc AB introduced the Epiroc DTH 5 hammers range, positioned to increase drilling versatility, penetration performance, and service life for drilling contractors and mining-related drilling applications.

In December 2025, Boart Longyear Group Ltd announced the release of its Stingray diamond bit for downhole motor (DHM) and full-face drilling, designed to improve penetration rates and extend bit life in challenging ground conditions for exploration drilling programs.

In April 2025, Epiroc AB inaugurated an expanded manufacturing facility in Hyderabad, India, to increase capacity for rock drilling tools (including rotary and DTH drilling tools) and rock reinforcement products, supporting growing demand in mining and infrastructure markets.

In March 2026, Komatsu Ltd expanded its mining equipment and drilling technology portfolio with new automation-focused drilling solutions aimed at improving drilling precision, productivity, and consumable life in surface mining operations.

Global Mining Drilling Tools Market Coverage

Tool Type Insight and Forecast 2026 - 2035

- Down-the-hole (DTH)

- Top hammer tools

- Rotary drill bits

- Others

Mining Type Insight and Forecast 2026 - 2035

- Surface mining

- Underground mining

Application Insight and Forecast 2026 - 2035

- Production / blast-hole drilling

- Mineral exploration

- Grade control and development drilling

End-Use Industry Insight and Forecast 2026 - 2035

- Metal mining

- Coal mining

- Quarrying & aggregates

Global Mining Drilling Tools Market by Region

- North America

- By Tool Type

- By Mining Type

- By Application

- By End-Use Industry

- By Country - U.S., Canada, Mexico

- Europe

- By Tool Type

- By Mining Type

- By Application

- By End-Use Industry

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Tool Type

- By Mining Type

- By Application

- By End-Use Industry

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Tool Type

- By Mining Type

- By Application

- By End-Use Industry

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Mining Drilling Tools Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Tool Type

1.2.2. By

Mining Type

1.2.3. By

Application

1.2.4. By

End-Use Industry

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Tool Type

5.1.1. Down-the-hole (DTH)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Top hammer tools

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Rotary drill bits

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Others

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Mining Type

5.2.1. Surface mining

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Underground mining

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Production / blast-hole drilling

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Mineral exploration

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Grade control and development drilling

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End-Use Industry

5.4.1. Metal mining

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Coal mining

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Quarrying & aggregates

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Tool Type

6.2. By

Mining Type

6.3. By

Application

6.4. By

End-Use Industry

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Tool Type

7.2. By

Mining Type

7.3. By

Application

7.4. By

End-Use Industry

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Tool Type

8.2. By

Mining Type

8.3. By

Application

8.4. By

End-Use Industry

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Tool Type

9.2. By

Mining Type

9.3. By

Application

9.4. By

End-Use Industry

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Sandvik AB

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Epiroc AB

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Boart Longyear Group Ltd.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Caterpillar Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Komatsu Ltd.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

FLSmidth & Co. A/S

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Furukawa Rock Drill Co., Ltd.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Mincon Group plc

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Robit Plc

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Rockmore International, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Center Rock, Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Mining Drilling Tools Market