Smart Grid Systems Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Hardware, Software, Services), by Solution (Advanced Metering Infrastructure (AMI), Grid Distribution Management, Grid Asset Management, Substation Automation, Demand Response Management, Energy Management Systems), by Technology (Wired Communication, Wireless Communication), by Application (Generation, Transmission, Distribution, Consumption), by End User (Residential, Commercial, Industrial, Utilities)

| Status : Published | Published On : Feb, 2026 | Report Code : VREP3065 | Industry : Energy & Power | Available Format :

|

Page : 183 |

Smart Grid Systems Market Overview

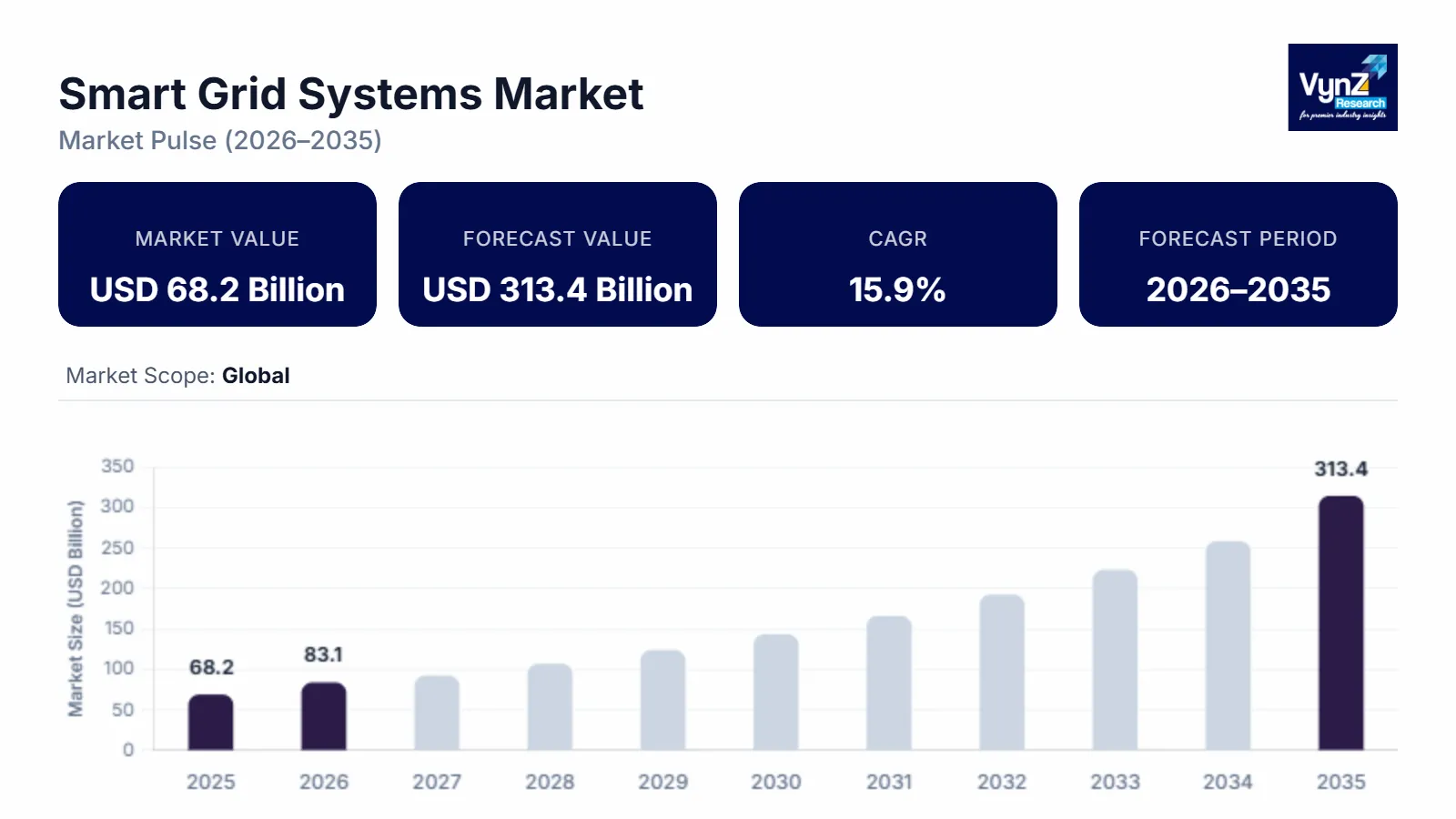

The smart grid systems market which was valued at approximately USD 68.2 billion in 2025 and is estimated to reach around USD 83.1 billion in 2026, is projected to reach close to USD 313.4 billion by 2035, expanding at a CAGR of about 15.9% during the forecast period from 2026 to 2035.

This market is primarily driven by the accelerating global transition toward cleaner and more efficient energy infrastructure. Governments and utilities worldwide are modernizing traditional power grids to accommodate renewable energy sources such as solar and wind, which are inherently variable and decentralized. Smart grid systems enable real-time monitoring, automated load balancing, and improved integration of distributed energy resources. As countries commit to decarbonization targets and net-zero emissions, utilities are investing heavily in digital grid technologies that enhance grid flexibility, reliability, and resilience, thereby driving sustained market growth. Another major growth driver is the rising electricity demand fueled by rapid urbanization, industrial expansion, and the electrification of transportation. The increasing adoption of electric vehicles, electric heating systems, and distributed energy generation has placed significant pressure on aging grid infrastructure.

Smart Grid Systems Market Dynamics

Market Trends

The adoption of AI, IoT, and Big Data analytics is emerging as one of the most transformative trends in the smart grid systems market. Smart grids rely on a vast network of interconnected sensors, smart meters, and intelligent devices that continuously collect real-time data across transmission, distribution, and consumption points. IoT technology enables seamless communication between these devices, allowing utilities to monitor grid performance, detect anomalies, and manage energy flows with greater precision. This interconnected infrastructure forms the foundation for data-driven decision-making within modern power networks. The U.S. Department of Energy (DOE) allocated $3 billion (FY 2022–2026) under the Grid Resilience and Innovation Partnerships (GRIP) program to modernize the electric grid. Artificial intelligence enhances this ecosystem by enabling predictive analytics and automated control. AI-powered algorithms analyze historical and real-time grid data to forecast demand patterns, predict equipment failures, and optimize load distribution. This helps utilities reduce downtime, prevent blackouts, and improve asset utilization.

Growth Drivers

The integration of renewable energy sources such as solar, wind, hydro, and distributed rooftop systems is a major growth driver of the smart grid systems market. Unlike conventional power plants, renewable energy generation is intermittent and decentralized, creating variability in voltage, frequency, and power flow across the grid. Smart grid technologies enable real-time monitoring, automated control, and bidirectional communication, which help utilities efficiently manage fluctuating renewable inputs. Advanced forecasting tools, energy storage integration, and demand response systems further support grid stability while maximizing renewable utilization. The Indian government recently raised the equity investment limit for Power Grid Corporation of India Ltd subsidiaries from ₹5,000 crore to ₹7,500 crore to better finance renewable evacuation infrastructure, helping integrate large solar and wind capacities into the national grid. As countries accelerate their clean energy transition targets and increase renewable capacity additions, the need for flexible and intelligent grid infrastructure continues to rise. Smart grids also facilitate the integration of distributed energy resources (DERs) at the consumer level, such as rooftop solar panels and microgrids. Consequently, the expansion of renewable energy installations globally is directly driving investments in smart grid modernization and digital grid management solutions.

Market Restraints / Challenges

Cybersecurity risks and data privacy concerns represent a significant challenge for the smart grid systems market due to the increasing digitalization and interconnected nature of modern power infrastructure. Smart grids rely on advanced communication networks, IoT-enabled sensors, smart meters, and cloud-based analytics platforms, all of which expand the potential attack surface for cyber threats. Unauthorized access, data breaches, malware attacks, and ransomware incidents can disrupt grid operations, compromise sensitive consumer data, and even cause large-scale power outages. As smart grids collect real-time consumption data from households and industries, concerns regarding the misuse or leakage of personal and operational information are rising. Utilities must invest heavily in encryption technologies, intrusion detection systems, and continuous network monitoring to safeguard infrastructure. However, implementing robust cybersecurity frameworks increases operational costs and system complexity. Consequently, ensuring secure and resilient grid operations remains a critical barrier to widespread smart grid adoption.

Market Opportunities

The rapid expansion of electric vehicle (EV) charging infrastructure presents a significant growth opportunity for the smart grid systems market. Global EV adoption accelerates due to decarbonization goals and supportive government incentives, electricity demand patterns are becoming more dynamic and complex. Large-scale deployment of public and private charging stations increases peak load pressures on existing grid networks. Smart grid technologies enable load balancing, real-time monitoring, and intelligent demand response to manage EV charging without overloading distribution systems. Vehicle-to-grid (V2G) capabilities further enhance grid flexibility by allowing EVs to supply stored energy back to the grid during peak demand periods. Under the PM E-Drive framework, Karnataka is planning to establish ~1,500 high-capacity EV charging stations across key locations such as highways and logistics hubs, supported by central subsidies that cover 80-100 % of upfront infrastructure costs including transformers and transmission upgrades. Additionally, integration of renewable energy with EV charging infrastructure requires advanced grid coordination and energy management systems. Consequently, the rising penetration of EVs is creating strong demand for digital, automated, and resilient smart grid solutions.

Global Smart Grid Systems Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 68.2 Billion |

|

Revenue Forecast in 2035 |

USD 313.4 Billion |

|

Growth Rate |

15.9% |

|

Segments Covered in the Report |

Component, Solution, Technology, Application, End User, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, Rest of the World |

|

Key Companies |

Siemens AG, General Electric Company, ABB Ltd, Schneider Electric SE, Itron, Inc., Honeywell International Inc., Oracle Corporation, Landis+Gyr Group AG, Eaton Corporation plc, Cisco Systems, Inc. |

|

Customization |

Available upon request |

Smart Grid Systems Market Segmentation

By Component

Hardware is the largest category with a market share of about 45% in 2025, as it forms the physical backbone of smart grid infrastructure including smart meters, sensors, transformers, substations, and communication devices. Utilities across developed and emerging economies are heavily investing in grid modernization projects that require large-scale deployment of advanced metering infrastructure and substation automation equipment. Hardware installations account for a significant portion of capital expenditure during grid upgrades. Additionally, expanding renewable energy integration and EV charging infrastructure further increases demand for intelligent grid hardware. Since physical infrastructure deployment is the first step toward digital grid transformation, hardware continues to dominate overall spending.

Software is the fastest-growing category with a CAGR of 16.1% during the forecast period, driven by increasing demand for real-time analytics, grid optimization, AI-based forecasting, and energy management platforms. Utilities are shifting toward data-driven decision-making, requiring advanced grid management software and cloud-based control systems. The rise of distributed energy resources and demand response programs also increases reliance on intelligent software platforms. As grids become more digital and interconnected, software solutions enabling automation, predictive maintenance, and cybersecurity are witnessing accelerated adoption.

By Solution

Advanced Metering Infrastructure (AMI) is the largest category with a market share of about 35% in 2025, as smart meter rollouts are central to smart grid deployment worldwide. Governments and utilities are prioritizing smart meter installations to enhance billing accuracy, demand response capability, and real-time consumption monitoring. Large-scale national smart meter programs across North America, Europe, and Asia-Pacific are significantly contributing to this dominance. AMI also acts as the foundation for further smart grid applications, strengthening its leadership position.

Demand Response Management is the fastest-growing category during the forecast period, driven by rising peak load pressures and increasing renewable energy penetration. Utilities are adopting demand-side management programs to balance grid loads efficiently and reduce infrastructure stress. With growing electricity consumption from EVs and electrified heating systems, demand response platforms are gaining importance. The ability to dynamically adjust power consumption in real time is fueling rapid growth in this segment.

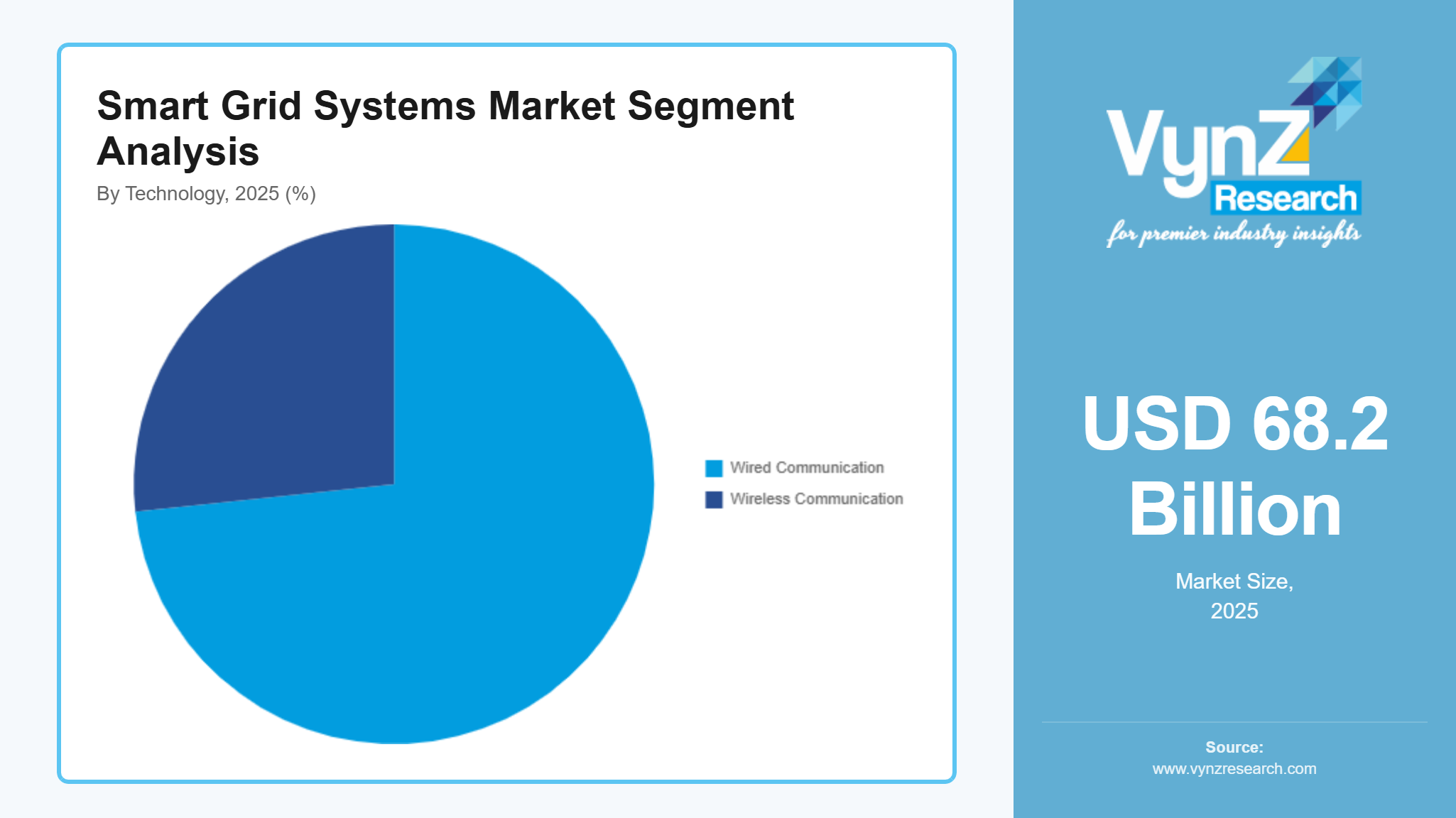

By Technology

Wireless Communication is the largest category with a market share of about 55% in 2025, as utilities increasingly prefer flexible and cost-efficient communication networks for smart meters and distributed assets. Wireless technologies such as RF mesh, cellular networks, and IoT-based connectivity reduce installation complexity compared to wired systems. Their scalability and suitability for remote areas further strengthen adoption. As grid assets expand geographically, wireless communication continues to dominate smart grid connectivity solutions.

Wireless Communication is the fastest-growing category with a CAGR of 16.4% during the forecast period, supported by rapid deployment of IoT devices and 5G-enabled grid connectivity. The transition toward decentralized energy systems requires agile and scalable communication frameworks. Advancements in secure wireless protocols and private LTE networks are accelerating adoption. These advantages position wireless technology as the primary growth engine within grid communication infrastructure.

By Application

Distribution is the largest category with a market share of about 40% in 2025, as distribution networks face the highest operational complexity due to integration of rooftop solar, EV charging stations, and distributed energy resources. Utilities prioritize distribution automation, voltage regulation, and outage management systems to enhance reliability. Since most customer-level grid interactions occur at the distribution stage, investments are heavily concentrated in this segment.

Consumption is the fastest-growing category with a CAGR of 16.7% during the forecast period, driven by smart homes, smart buildings, and prosumer energy participation. Real-time energy monitoring, dynamic pricing, and demand-side optimization are expanding rapidly at the consumer level. The growth of behind-the-meter storage and energy management systems is accelerating digitalization at the consumption stage.

By End User

Utilities is the largest category with a market share of about 35% in 2025, as they are the primary investors and operators of grid infrastructure modernization projects. Government-backed funding programs and regulatory mandates largely target utility-scale deployments. Utilities manage large-scale transmission and distribution systems, making them central to smart grid adoption.

Industrial is the fastest-growing category during the forecast period, driven by rising demand for energy efficiency, load optimization, and on-site renewable integration. Industrial facilities are adopting smart grid solutions to reduce operational costs and enhance energy reliability. As industries move toward decarbonization and electrification, digital energy management systems are witnessing strong growth.

Regional Insights

North America

North America is the largest regional market for the Smart Grid Systems Market, supported by highly advanced power infrastructure and significant investments in grid modernization initiatives. The United States leads the region with large-scale deployment of advanced metering infrastructure (AMI), digital substations, and grid automation technologies. Strong federal and state-level funding programs aimed at enhancing grid resilience and integrating renewable energy sources further drive market growth. The U.S. Department of Energy (DOE) has allocated approximately $10.5 billion under the Grid Resilience and Innovation Partnerships (GRIP) Program as part of the Bipartisan Infrastructure Law to strengthen and modernize the nation’s electric grid. The rapid expansion of electric vehicle charging networks is increasing the need for intelligent load management systems. Utilities are heavily investing in AI-driven analytics and cybersecurity solutions to secure increasingly digital grid networks. Canada is also advancing smart grid pilot projects focused on clean energy integration and rural grid reliability. Canada is also investing USD 100 million in its Smart Grid Program to support deployment of smart grid technologies and integrated systems. Regulatory emphasis on energy efficiency and carbon reduction continues to accelerate adoption of advanced grid technologies across the region.

Asia-Pacific

Asia-Pacific is the fastest-growing region in the Smart Grid Systems Market due to rapid urbanization, rising electricity demand, and strong government-backed digital infrastructure programs. Countries such as China, India, Japan, and South Korea are investing heavily in smart meter rollouts and grid automation projects. Australia’s government-backed Clean Energy Finance Corporation (CEFC) has committed over USD 33 billion to clean energy investments, including grid upgrades that support renewable energy integration and storage solutions critical for smart grid operations. China leads in ultra-high voltage transmission deployment and renewable energy integration, requiring advanced monitoring and balancing systems. India is implementing nationwide smart metering initiatives to reduce transmission losses and improve billing efficiency. Expanding industrialization and smart city development programs are further boosting grid modernization efforts. The rapid adoption of rooftop solar systems and distributed energy resources is increasing demand for advanced distribution management solutions. Supportive regulatory frameworks and strong economic growth continue to drive large-scale smart grid investments across the region.

Europe

Europe holds a significant share in the Smart Grid Systems Market, driven by strict decarbonization targets and renewable energy mandates. The region emphasizes grid flexibility and cross-border electricity interconnections to support its energy transition goals. Countries such as Germany, France, and the United Kingdom are expanding smart meter installations and digital substation projects. The European Commission’s Digitalisation of the Energy System Action Plan anticipates around EUR 584 billion (~USD 633 billion) investment in the electricity grid by 2030, of which approximately EUR 170 billion (~USD 184 billion) is earmarked specifically for grid digitalisation including smart meters, automated grid technologies, and advanced communication systems to support renewables. High penetration of wind and solar energy requires advanced forecasting, storage integration, and demand response systems. The European Union’s climate neutrality objectives are encouraging utilities to adopt energy-efficient and automated grid technologies. Strong regulatory standards around emissions reduction and sustainability further support digital grid investments. The UK energy regulator fast-tracked £4 billion (~USD 5.2 billion) of electricity grid investments to accelerate infrastructure upgrades necessary for renewable integration and clean energy targets, indirectly supporting smart grid systems as part of overall network modernization efforts. Integration of electric mobility and electrified heating systems is also accelerating modernization of transmission and distribution networks.

Rest of the World

The rest of the world, including Latin America and the Middle East & Africa, is witnessing steady growth in smart grid deployment. In Latin America, countries such as Brazil and Mexico are modernizing distribution networks to reduce technical losses and improve service reliability. Increasing renewable energy projects across the region are creating demand for grid automation and monitoring systems. In the Middle East, nations such as the UAE and Saudi Arabia are investing in smart grid infrastructure as part of smart city and economic diversification initiatives. African countries, including South Africa, are gradually upgrading grid systems with support from international funding and public-private partnerships. Although infrastructure development levels vary, rising electricity demand and renewable integration efforts are driving consistent market expansion across these regions.

Competitive Landscape / Company Insights

The smart grid systems market is consolidated in nature, particularly in advanced grid automation, transmission management systems, and large-scale utility software platforms, where a limited number of multinational technology providers hold significant market influence. Smart grid deployment requires substantial capital investment, deep technical expertise, cybersecurity capabilities, and long-term utility partnerships, which creates high entry barriers for new players. Major energy technology companies, power equipment manufacturers, and digital solution providers dominate large utility contracts, especially in developed markets.

Competition is primarily centered on technological innovation, system integration capabilities, and the ability to deliver end-to-end solutions combining hardware, software, and services. Strategic collaborations with governments and utilities further strengthen the position of established firms. Although regional players and niche software providers are emerging, large-scale projects are generally awarded to financially strong and technologically mature companies. This structure sustains moderate-to-high market concentration while maintaining competitive intensity among leading global participants.

Mini Profiles

Siemens AG is a global leader in smart grid automation, digital substations, and grid management software, providing end-to-end solutions for transmission and distribution networks. The company supports utilities worldwide with advanced grid analytics, renewable integration technologies, and cybersecurity-enabled digital energy platforms, playing a major role in large-scale grid modernization projects.

General Electric Company operates through its Grid Solutions business, delivering advanced transmission equipment, grid software, and automation systems. The company focuses on integrating renewable energy, enhancing grid reliability, and deploying digital monitoring technologies that support utilities in improving operational efficiency and resilience.

ABB Ltd provides smart grid technologies including substation automation, distribution management systems, and grid-edge solutions. Its portfolio supports renewable integration, microgrid development, and intelligent asset management, helping utilities enhance reliability and reduce transmission losses.

Schneider Electric SE offers comprehensive smart grid and energy management solutions, combining hardware, software, and analytics platforms. The company emphasizes grid digitization, demand response systems, and sustainable energy infrastructure to enable efficient and resilient electricity networks.

Itron, Inc. specializes in advanced metering infrastructure (AMI), grid edge intelligence, and utility data analytics. Its smart meters and communication platforms enable real-time monitoring, demand management, and distributed energy resource integration for utilities globally.

Key Players

- Siemens AG

- General Electric Company

- ABB Ltd

- Schneider Electric SE

- International Business Machines Corporation

- Cisco Systems, Inc.

- Itron, Inc.

- Oracle Corporation

- Honeywell International Inc.

- Eaton Corporation plc

- Landis+Gyr Group AG

- Wipro Limited

Recent Developments

January 2026 – Siemens AG announced the expansion of its digital grid portfolio with new AI-enabled grid management software designed to enhance renewable energy integration and improve real-time network resilience for utility operators.

December 2025 – Schneider Electric SE launched an advanced distribution management platform integrating AI-based load forecasting and cybersecurity layers to strengthen smart grid reliability across large-scale utility networks.

December 2025 – ABB signed an agreement to acquire Netcontrol, a Finland-based provider of grid automation solutions, to enhance its digital grid portfolio as utilities face increasing pressure from rising energy demand and renewable energy integration globally.

June 2025 – Honeywell International Inc. introduced an upgraded cybersecurity suite specifically designed for smart grid infrastructure, enabling utilities to detect, prevent, and respond to cyber threats targeting connected grid assets.

Global Smart Grid Systems Market Coverage

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Solution Insight and Forecast 2026 - 2035

- Advanced Metering Infrastructure (AMI)

- Grid Distribution Management

- Grid Asset Management

- Substation Automation

- Demand Response Management

- Energy Management Systems

Technology Insight and Forecast 2026 - 2035

- Wired Communication

- Wireless Communication

Application Insight and Forecast 2026 - 2035

- Generation

- Transmission

- Distribution

- Consumption

End User Insight and Forecast 2026 - 2035

- Residential

- Commercial

- Industrial

- Utilities

Global Smart Grid Systems Market by Region

- North America

- By Component

- By Solution

- By Technology

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Solution

- By Technology

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Solution

- By Technology

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Solution

- By Technology

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Smart Grid Systems Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Solution

1.2.3. By

Technology

1.2.4. By

Application

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Solution

5.2.1. Advanced Metering Infrastructure (AMI)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Grid Distribution Management

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Grid Asset Management

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Substation Automation

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Demand Response Management

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Energy Management Systems

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Wired Communication

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Wireless Communication

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Application

5.4.1. Generation

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Transmission

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Distribution

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Consumption

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Residential

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Commercial

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Industrial

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Utilities

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Solution

6.3. By

Technology

6.4. By

Application

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Solution

7.3. By

Technology

7.4. By

Application

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Solution

8.3. By

Technology

8.4. By

Application

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Solution

9.3. By

Technology

9.4. By

Application

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Siemens AG

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

General Electric Company

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

ABB Ltd

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Schneider Electric SE

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

International Business Machines Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Cisco Systems, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Itron, Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Oracle Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Honeywell International Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Eaton Corporation plc

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Landis+Gyr Group AG

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Wipro Limited

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Smart Grid Systems Market