Micro Nuclear Reactor Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Reactor Type (High Temperature Gas Cooled Reactors, Light Water Reactors, Molten Salt Reactors, Fast Neutron Reactors), by Power Output (Below 10 MW, 10 MW to 50 MW, Above 50 MW), by Application (Power Generation, Hydrogen Production, Industrial Process Heat, Desalination, District Heating), by Mobility (Stationary Micro Reactors, Mobile and Transportable Micro Reactors), by End User (Industrial, Defense and Military, Utilities, Mining, Remote Communities)

| Status : Published | Published On : May, 2026 | Report Code : VREP3070 | Industry : Energy & Power | Available Format :

|

Page : 143 |

Micro Nuclear Reactor Market Overview

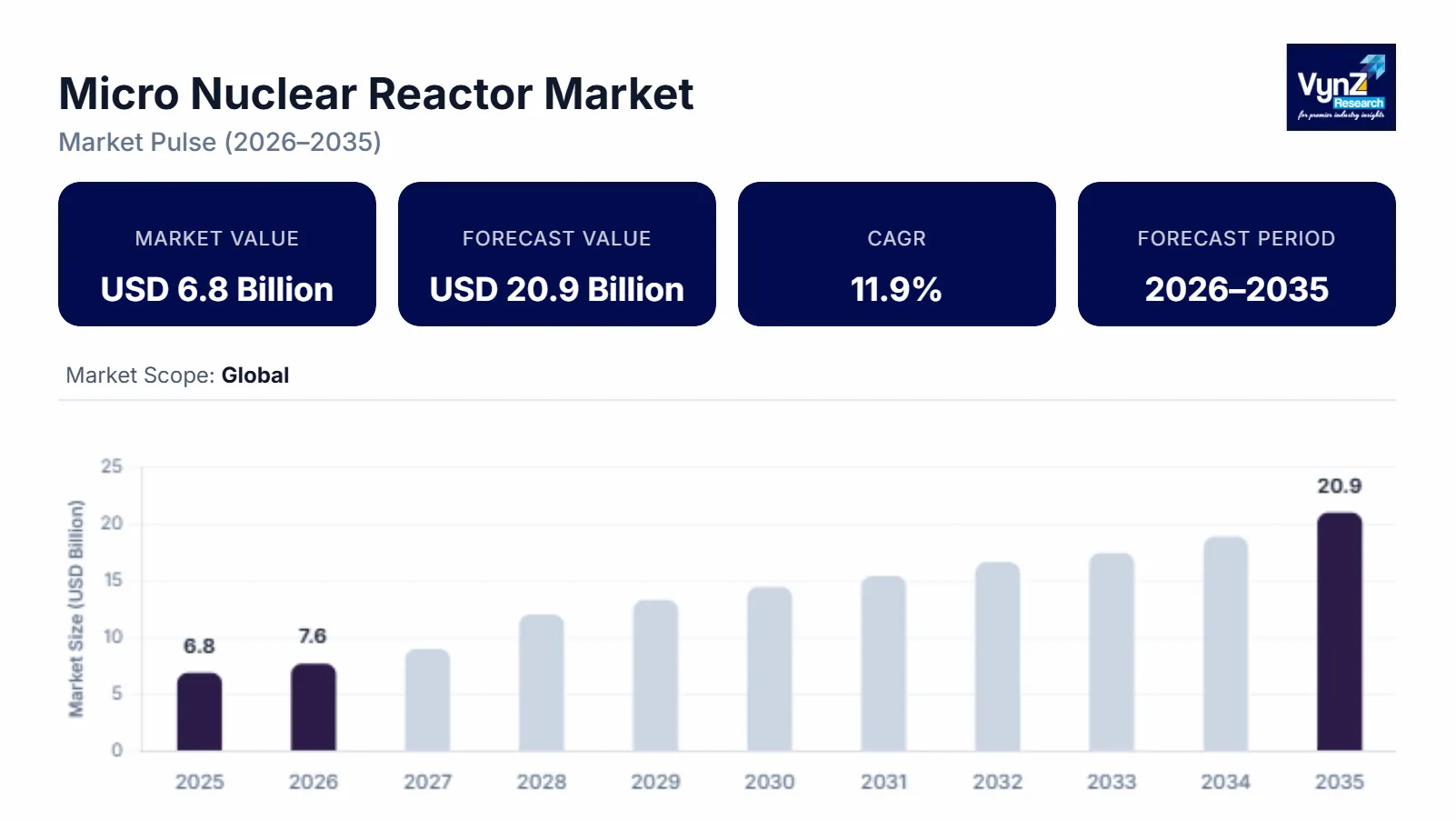

The Micro Nuclear Reactor market which was valued at approximately USD 6.8 billion in 2025 and is estimated to rise further up to almost USD 7.6 billion by 2026, is projected to reach around USD 20.9 billion in 2035, expanding at a CAGR of about 11.9% during the forecast period from 2026 to 2035.

The market growth is subject to the rising need for dependable off grid power generation, defense use and remote industrial energy demands. A stronger push toward low carbon electricity generation, deployment of compact modular reactor systems for mining work, military sites, and isolated communities, encourage industries to adopt these solutions across both developed and emerging economies. Growth is also fueled by rising investment in newer nuclear technologies and supportive clean energy transition policies as well as increasing demand for electricity for remote areas and energy intensive industries.

The International Atomic Energy Agency and the U.S. Department of Energy are speeding up pilot efforts and financing setups aimed at advanced micro reactor deployment to improve energy security and cut carbon emissions. There are ongoing government backed measures to decarbonization and more resilient energy infrastructure that push market expansion in big regions like the United States, Canada, and China.

Micro Nuclear Reactor Market Dynamics

Market Trends

The industry is seeing some notable shifts in advanced reactor deployment approaches, more decentralized electricity generation models, and cleaner energy purchasing behavior. The wider adoption of transportable and factory fabricated micro reactor systems indicate a movement away from rigid deployment toward operational flexibility, stronger energy security and lower carbon intensity. There is also a growing attention on compact reactors for defense installations, mining operations, and remote industrial sites which is reinforcing commercial traction across many developed economies. Another thing starting to show up is the use of advanced digital monitoring and passive safety features due to regulatory modernization and ongoing innovation in nuclear engineering. The International Atomic Energy Agency and the U.S. Nuclear Regulatory Commission point to pilot projects with autonomous operation capabilities and updated safety frameworks for next generation micro reactors.

Growth Drivers

The market growth is mostly driven by a rising global demand for dependable low carbon power generation, driving consistent interest across remote industrial facilities, defense related energy needs, and off grid communities. Bigger investments in advanced nuclear programs and more resilient energy infrastructure are accelerating expansion and government backed decarbonization initiatives in places like the United States and Canada are adding extra deployment momentum. The push for energy independence and long duration power steadiness is playing a key role in adoption by industrial operators and public sector agencies looking for energy efficiency, emissions cuts and uninterrupted electricity supply. Data and summaries from the U.S. Department of Energy and the International Energy Agency continue to describe advanced nuclear technologies as a meaningful ingredient in future clean energy transition roadmaps.

Market Restraints / Challenges

The market faces regulatory complexity and long approval timelines that slows down commercialization and limit the ability to enter the market, especially for companies that are newer or still developing nuclear tech. Different national nuclear licensing structures and strict safety compliance expectations are creating operational uncertainties for manufacturers and project teams in multiple regions. High upfront capital demands and reliance on specialized engineering know-how create operational bottlenecks for reactor producers and suppliers. Dependency on advanced fuel technologies, non-availability of a skilled nuclear workforce, and limited supply chain maturity affects costs and delay projects.

Market Opportunities

Real opportunities lie especially for remote and off grid power generation use cases where energy demand is rising at mining sites, military bases, and isolated settlements. Firms that provide modular, transportable, and high efficiency reactor solutions are in a good place to secure additional orders from industrial operators who want dependable low emission electricity in hard geographic conditions. Another opportunity is hybrid clean energy integration. Investments in hydrogen production, desalination, and industrial heat solutions are opening pathways for long term revenue streams and with better automation systems, digital reactor monitoring platforms, and newer fuel cycle technologies operational performance should improve and help customer buy-in. As per recent progress described by the International Atomic Energy Agency and the U.S. Department of Energy, public and private support for advanced reactor demonstration programs continues to grow worldwide, making the funding environment stronger.

Global Micro Nuclear Reactor Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.8 Billion |

|

Revenue Forecast in 2035 |

USD 20.9 Billion |

|

Growth Rate |

11.9% |

|

Segments Covered in the Report |

Reactor Type, Power Output, Application, Mobility, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, Rest of the World |

|

Key Companies |

BWX Technologies, General Atomics, Holtec International, Kairos Power, NuScale Power, Oklo, Rolls-Royce SMR, TerraPower, Ultra Safe Nuclear Corporation, Westinghouse Electric Company |

|

Customization |

Available upon request |

Micro Nuclear Reactor Market Segmentation

By Reactor Type

In 2025, high temperature gas cooled reactors took the lead in the market, making up about 48% of the overall revenue due to solid thermal efficiency, passive safety features and more deployments in remote industrial areas. Adoption is getting a boost from newer reactor programs from the U.S. Department of Energy and the International Atomic Energy Agency.

Molten salt reactors are expected to grow the quickest, with an estimated CAGR of 13.4% from 2026 to 2035 driven by higher research funding, better hopes for fuel efficiency, and an increased emphasis on flexible next generation nuclear systems.

By Power Output

For 2025, reactors in the 10 MW to 50 MW band accounted for the biggest share, roughly 46% of segment revenue due to operational flexibility, usefulness for industrial operations, and the ability to deliver decentralized power in a steadier way.

Reactors below 10 MW are projected to grow faster, with an estimated CAGR of 13.1% during 2026 to 2035 due to rising demand for transportable energy systems, defense energy resilience initiatives, and electrification needs in isolated communities.

By Application

Power generation applications held the largest share in 2025, at around 51% of revenue due to the increasing need for dependable low emission electricity across mining activities, industrial sites, and decentralized energy arrangements. Decarbonization plans from governments and clean energy transition roadmaps are further encouraging advanced reactor rollout.

Hydrogen production applications are expected to be the fastest growing, with an estimated CAGR of 13.7% from 2026 to 2035, fueled by investments into low carbon hydrogen infrastructure and industrial decarbonization programs.

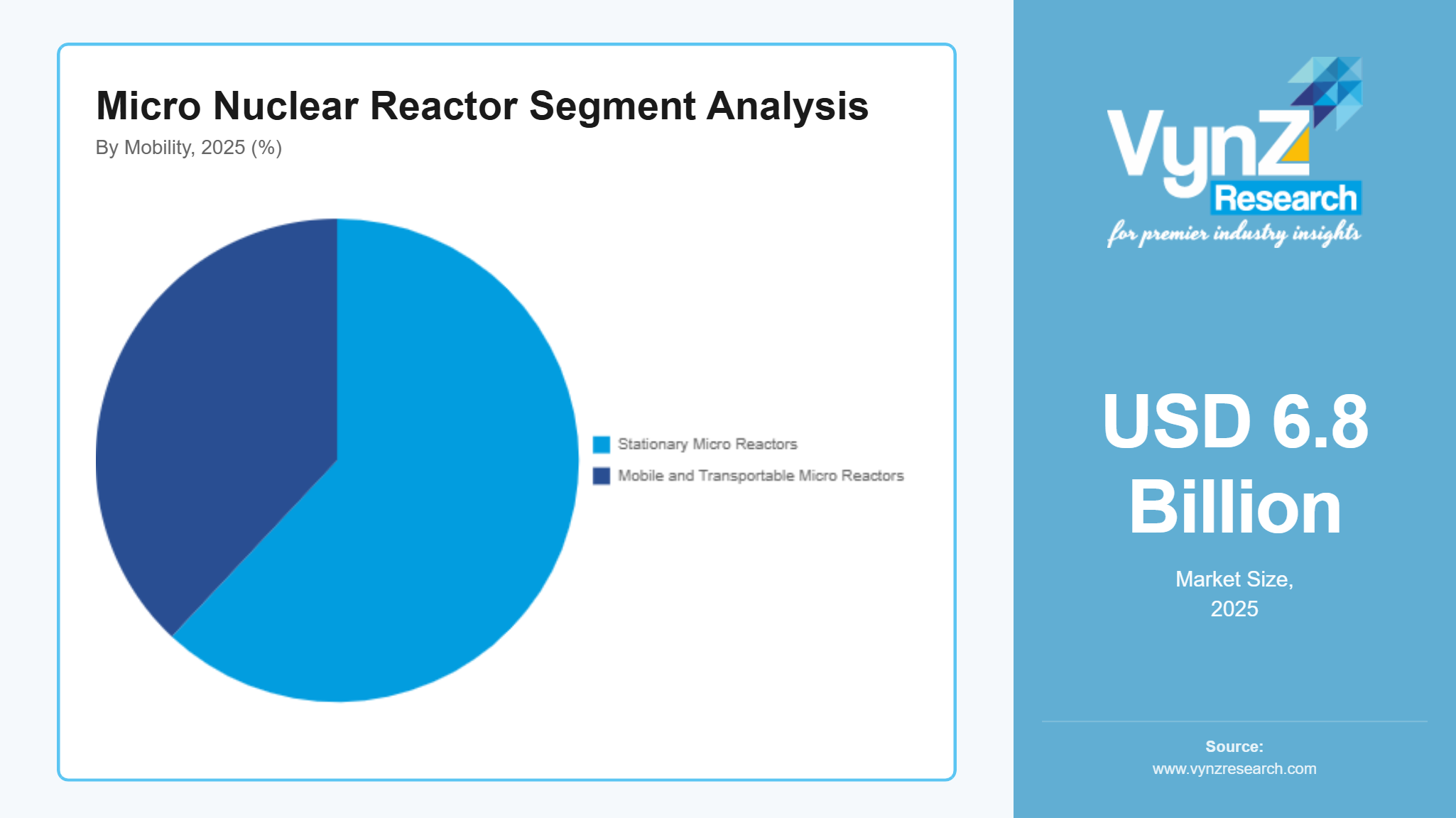

By Mobility

Stationary micro reactors were the biggest part of the market in 2025, contributing nearly 62% of total segment revenue driven by more deployments in industrial infrastructure, utility operations, and government backed resilient energy undertakings. Regulatory support for fixed advanced reactor installations keeps reinforcing that momentum.

Mobile and transportable micro reactors are anticipated to register the quickest growth, reaching an estimated CAGR of about 14.2% during 2026 to 2035, driven by military energy requirements, emergency deployment capabilities, and the growing demand for adaptable off grid electricity solutions.

By End User

Industrial users accounted for the largest segment in 2025, representing approximately 44% of total market revenue due to growing energy needs from mining, oil and gas, and heavy manufacturing operations in remote locations. Government supported clean energy transition initiatives, along with lower dependence on diesel generation, also strengthen industrial adoption.

Defense and military applications are forecast to grow at a CAGR of 13.6% during 2026 to 2035 supported by bigger investments in energy secure military infrastructure and the deployment of transportable reactor systems.

Regional Insights

North America

North America accounted for approximately 34% of the market in 2025, driven by strong investments in advanced nuclear technologies, defense energy programs, and resilient clean energy infrastructure. Strong demand from industrial and defense hubs across United States and Canada continues to support regional market growth. Government initiatives led by the U.S. Department of Energy, along with funding support for advanced reactor demonstration projects, are accelerating commercialization activities and deployment of compact reactor technologies.

Asia Pacific

Asia Pacific accounted for approximately 28% of the market in 2025 and is witnessing steady growth due to expanding industrial activity, rising electricity demand, and strong government support for clean energy diversification. Increasing adoption across strategic industrial sectors and remote infrastructure projects is driving consistent demand for advanced reactor technologies across China, India, and Japan. Government backed nuclear energy development programs and investments in low emission energy infrastructure are further supporting regional expansion.

Europe

Europe accounted for approximately 18% of the market in 2025, supported by increasing decarbonization targets, modernization of energy infrastructure, and rising investments in next generation nuclear technologies. Countries including United Kingdom and France are strengthening advanced nuclear deployment strategies to support energy transition goals and improve electricity supply stability. Government climate frameworks and clean energy policies are further creating long term opportunities for market participants.

Rest of the World

The Rest of the World accounted for approximately 20% of the market in 2025, driven by gradual investments in energy diversification, remote electrification projects, and industrial infrastructure modernization. Emerging economies across the Middle East, Latin America, and parts of Africa are witnessing increasing interest in advanced nuclear technologies to strengthen energy security and support long term clean energy transition goals. Government backed infrastructure development initiatives and increasing industrial energy demand are further encouraging adoption of compact reactor systems across developing regions.

Competitive Landscape / Company Insights

The market is moderately competitive with the presence of global nuclear technology developers and engineering companies focusing on advanced reactor innovation, strategic partnerships, and geographic expansion. Companies are increasingly investing in research and development, fuel efficiency technologies, and autonomous safety systems to strengthen their market position. Government backed funding initiatives led by the U.S. Department of Energy and support from the International Atomic Energy Agency are further encouraging commercialization of advanced micro reactor technologies across defense, industrial, and remote energy applications.

Mini Profiles

BWX Technologies focuses on advanced nuclear reactor systems and defense energy solutions, supported by strong government partnerships, engineering expertise, and long-term strategic infrastructure projects.

General Atomics operates in niche advanced nuclear technology segments, emphasizing reactor innovation, operational efficiency, and integrated energy systems for industrial and defense applications.

Holtec International leverages strategic partnerships and advanced reactor engineering capabilities to expand market presence, supported by growing investments in modular clean energy infrastructure projects.

Kairos Power focuses on next generation molten salt reactor technologies, supported by research driven development strategies and increasing government backed advanced nuclear demonstration programs.

NuScale Power operates in small modular reactor segments, emphasizing scalable reactor technologies, regulatory compliance, and long-term deployment opportunities across utility and industrial markets.

Key Players

- BWX Technologies

- General Atomics

- Holtec International

- Kairos Power

- NuScale

- Power

- Oklo

- Rolls-Royce SMR

- TerraPower

- Ultra Safe Nuclear Corporation

- Westinghouse Electric Company

Recent Developments

In September 2025, Oklo announced groundbreaking activities for its Aurora-INL fast reactor project at Idaho National Laboratory under the U.S. Department of Energy Reactor Pilot Program. The company also accelerated development of private fuel recycling capabilities to support advanced reactor commercialization.

In April 2026, Rolls-Royce SMR signed a contract with Great British Energy – Nuclear to support deployment of the United Kingdom’s first small modular reactor projects. The company also secured major government backed financial support to strengthen domestic reactor manufacturing and clean energy infrastructure development.

In April 2026, TerraPower officially commenced construction of the Natrium advanced nuclear power plant in Wyoming following approval from the U.S. Nuclear Regulatory Commission. The project represents one of the first utility scale advanced nuclear reactor developments in the United States.

In November 2025, Ultra Safe Nuclear Corporation continued expansion of advanced micro modular reactor development programs focused on remote industrial and defense energy applications. The company increased collaboration activities related to high temperature gas cooled reactor commercialization and resilient clean energy deployment initiatives.

In December 2025, Westinghouse Electric Company expanded strategic activities related to next generation small modular reactor technologies and advanced nuclear fuel development programs. The company also strengthened international partnerships supporting clean energy transition and long term nuclear infrastructure modernization projects.

Global Micro Nuclear Reactor Market Coverage

Reactor Type Insight and Forecast 2026 - 2035

- High Temperature Gas Cooled Reactors

- Light Water Reactors

- Molten Salt Reactors

- Fast Neutron Reactors

Power Output Insight and Forecast 2026 - 2035

- Below 10 MW

- 10 MW to 50 MW

- Above 50 MW

Application Insight and Forecast 2026 - 2035

- Power Generation

- Hydrogen Production

- Industrial Process Heat

- Desalination

- District Heating

Mobility Insight and Forecast 2026 - 2035

- Stationary Micro Reactors

- Mobile and Transportable Micro Reactors

End User Insight and Forecast 2026 - 2035

- Industrial

- Defense and Military

- Utilities

- Mining

- Remote Communities

Global Micro Nuclear Reactor Market by Region

- North America

- By Reactor Type

- By Power Output

- By Application

- By Mobility

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Reactor Type

- By Power Output

- By Application

- By Mobility

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Reactor Type

- By Power Output

- By Application

- By Mobility

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Reactor Type

- By Power Output

- By Application

- By Mobility

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Micro Nuclear Reactor Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Reactor Type

1.2.2. By

Power Output

1.2.3. By

Application

1.2.4. By

Mobility

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Reactor Type

5.1.1. High Temperature Gas Cooled Reactors

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Light Water Reactors

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Molten Salt Reactors

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Fast Neutron Reactors

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Power Output

5.2.1. Below 10 MW

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. 10 MW to 50 MW

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Above 50 MW

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Power Generation

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Hydrogen Production

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Industrial Process Heat

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Desalination

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. District Heating

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By Mobility

5.4.1. Stationary Micro Reactors

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Mobile and Transportable Micro Reactors

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Industrial

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Defense and Military

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Utilities

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Mining

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Remote Communities

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Reactor Type

6.2. By

Power Output

6.3. By

Application

6.4. By

Mobility

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Reactor Type

7.2. By

Power Output

7.3. By

Application

7.4. By

Mobility

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Reactor Type

8.2. By

Power Output

8.3. By

Application

8.4. By

Mobility

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Reactor Type

9.2. By

Power Output

9.3. By

Application

9.4. By

Mobility

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

BWX Technologies

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

General Atomics

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Holtec International

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Kairos Power

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

NuScale Power

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Oklo

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Rolls-Royce SMR

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

TerraPower

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Ultra Safe Nuclear Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Westinghouse Electric Company

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Micro Nuclear Reactor Market