Asia Pacific Drip Irrigation Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Emitters / Drippers, Drip Tubes / Laterals, Filters, Valves, Pressure Pumps, Controllers, Fittings and Accessories), by Crop Type (Field Crops, Fruits and Nuts, Vegetables, Plantation Crops, Greenhouse Crops), by Emitter Type (Inline Emitters, Online Emitters), by End User (Open Field Agriculture, Greenhouse Farming, Landscape and TurfTop of Form, Bottom of Form)

| Status : Published | Published On : Apr, 2026 | Report Code : VRFB11041 | Industry : Food & Beverage | Available Format :

|

Page : 135 |

Asia Pacific Drip Irrigation Market Overview

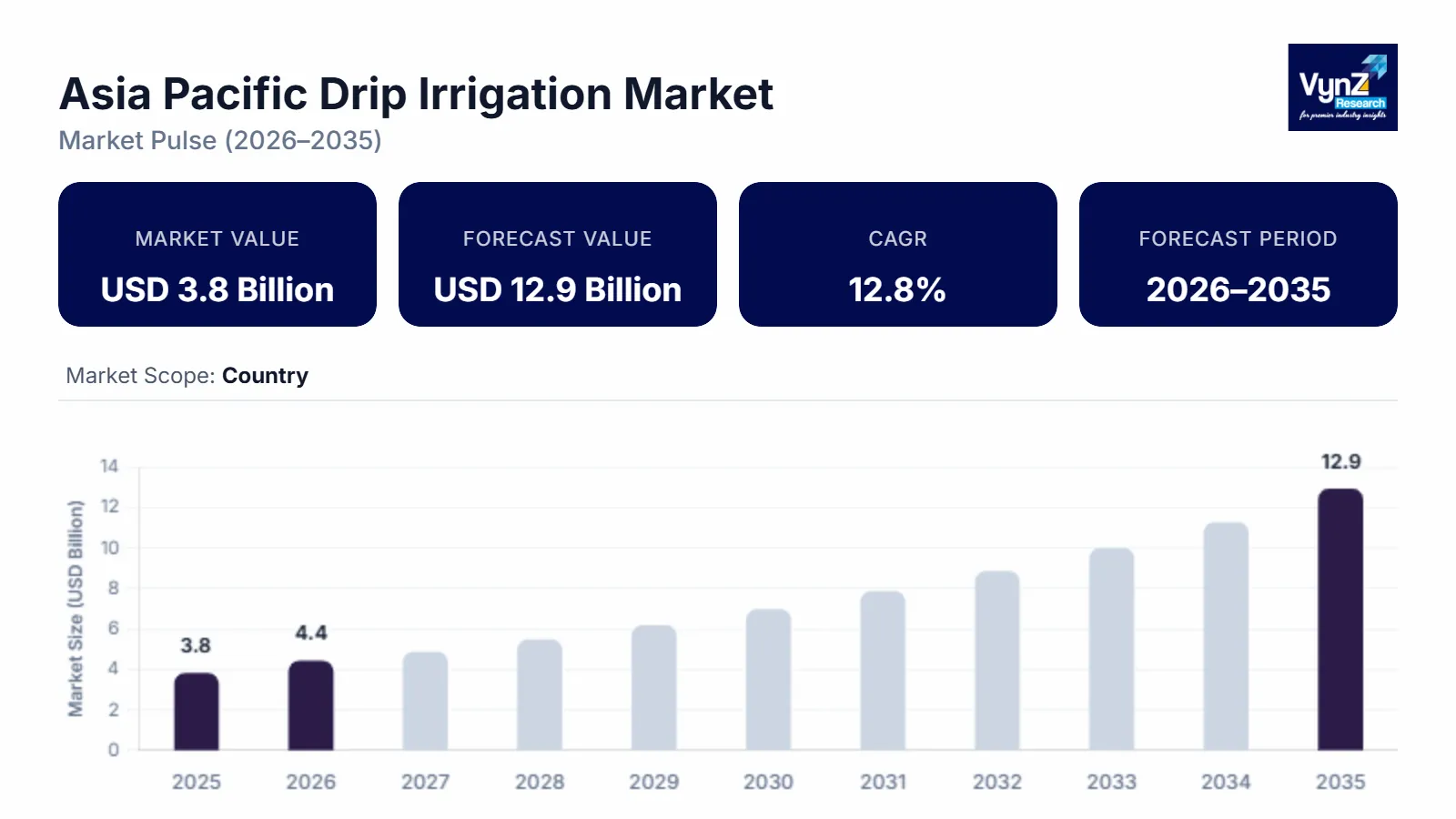

The Asia Pacific drip irrigation market which was valued at approximately USD 3.8 billion in 2025 and is estimated to rise further up to almost USD 4.4 billion by 2026, will reach a market size of USD 12.9 billion by 2035 with a CAGR of 12.8% during the period from 2026 to 2035.

The market growth will happen because of three factors: farmers face increasing water shortages, farmers are adopting more precise farming methods, and governments are providing financial support for micro irrigation systems and farmers are starting to use automated irrigation systems. The market growth in major regions including East Asia, South Asia and Southeast Asia is being driven by the need to improve crop yields and water efficiency, which is particularly important for countries facing water shortages like China, India and Australia who are also developing their agricultural systems.

The market momentum is sustained by government backed initiatives and institutional reports which confirm that agriculture consumes almost 70% of freshwater resources in Asia Pacific according to the Food and Agriculture Organization. The adoption of micro irrigation subsidy schemes and national water conservation missions and climate resilient agriculture programs as policy frameworks in India and China is driving increased farm adoption. The Asian Development Bank backed regional development programs provide funding for precision agriculture while establishing sustainable irrigation systems which results in lasting agricultural demand throughout the region.

Asia Pacific Drip Irrigation Market Dynamics

Market Trends

The industry experiences particular technological developments which customers employ to enhance water efficiency and water management techniques for agricultural fields because they want to use resources better and develop agricultural systems that can withstand climate change. The market experiences its most substantial transformation through precision irrigation technologies which people now prefer to use because they optimize water usage and energy efficiency and deliver nutrients according to specific crop requirements. The Food and Agriculture Organization establishes institutional frameworks with technical guidance to demonstrate that micro irrigation serves as an essential method which helps to solve water scarcity problems while increasing agricultural output throughout the entire region.

The current trend shows that farm workers are adopting smart irrigation systems which operate automatically because digital technology becomes more accessible and sensor technology enables remote monitoring. The product development process creates new requirements which push companies to develop integrated irrigation solutions that merge fertigation systems with real-time soil moisture monitoring and automated control units. Asian Development Bank funding for regional agricultural modernization programs establishes digital agriculture infrastructure which produces new competitive advantages through technology advancements and system integration and performance improvements for extensive farming businesses.

Growth Drivers

The market experiences growth through two primary forces which depend on electric power consumption and water supply reduction to create constant demand from agriculture and water-scarce areas. The market expands because increased agricultural infrastructure investments which include irrigation modernization, watershed development and sustainable farming programs. Government programs promote micro irrigation adoption through two main methods which include establishing subsidies and implementing irrigation efficiency missions thus creating increased demand from both smallholder and commercial farmers.

Agricultural productivity improvement and crop yield increase represent two critical drivers which enhance adoption rates. The demand for drip irrigation systems will continue strong throughout the forecast period because farmers and agribusiness enterprises now focus their resources on achieving cost efficiency through water conservation methods which generate more output per hectare of land. The World Bank shows through its published policy recommendations and water management frameworks that efficient irrigation technologies play a crucial role in raising food security levels and supporting sustainable agricultural practices which will lead to sustained market expansion throughout the entire region.

Market Restraints / Challenges

The market shows strong potential but its market development faces specific obstacles which will restrict its upcoming growth. The market faces obstacles which stem from high initial costs and affordable system access problems that specifically affect small farmers in developing countries. The market faces price-sensitive conditions because its essential components which include filtration units, tubing networks and automation equipment require high capital investment thus creating obstacles for market entry despite their proven efficiency advantages.

The manufacturers and end users face operational difficulties because they need to import components while several rural areas lack sufficient technical expertise. The system performance suffers from two main problems which emerge from insufficient after-sales service networks and the complicated maintenance processes which lead to decreased equipment longevity. The Food and Agriculture Organization reports together with its policy assessments show that two main obstacles which prevent precision irrigation technology expansion in emerging agricultural economies during financial or climatic crises are technical training shortages and infrastructure deficiencies.

Market Opportunities

The market offers extensive growth potential for micro irrigation systems which agricultural areas yet to receive sufficient service can access through sustainable farming solutions and climate adaptation strategies. The companies which provide irrigation systems at an affordable price and with scalable capacity will benefit from the growing demand which smallholder farmers and emerging agribusinesses create. The government-supported irrigation programs and rural development initiatives enable farmers to access financing, training and infrastructure thus promoting system adoption throughout various agricultural landscapes.

The digital agriculture sector presents an opportunity which allows smart irrigation systems to develop through increased funding for sensor technology, automated systems and data-based farm management software. The Asian Development Bank development initiatives will enhance remote monitoring technologies which will boost system performance, increase water efficiency and improve farmer participation thus establishing technology-driven irrigation solutions as an essential growth driver for the regional market.

Asia Pacific Drip Irrigation Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.8 Billion |

|

Revenue Forecast in 2035 |

USD 12.9 Billion |

|

Growth Rate |

12.8% |

|

Segments Covered in the Report |

Component, Crop Type, Emitter Type, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Australia, Japan and Southeast Asia |

|

Key Companies |

Chinadrip Irrigation Equipment Co., Ltd., EPC Industries Limited, Hunter Industries, Irritec S.p.A., Jain Irrigation Systems Ltd., Lindsay Corporation, Mahindra EPC Irrigation Ltd., Netafim Limited, Rain Bird Corporation, Rivulis Irrigation Ltd., The Toro Company |

|

Customization |

Available upon request |

Asia Pacific Drip Irrigation Market Segmentation

By Component

The market in 2025 saw its most revenue from emitters and drippers which generated about 34% of total market earnings. Farmers need to control water output through this technology because it helps them maintain their irrigation systems for various crop types. The need for water conservation and consistent agricultural output has driven higher adoption rates in nations that deal with irrigation deficits. The Indian and Chinese governments back micro irrigation systems which create higher demand for emitters as they require efficient water distribution while minimizing agricultural waste according to their policy guidelines.

The most rapid growth will occur in filters and control systems which are expected to achieve 13.4% CAGR between 2026 and 2035. Automated irrigation systems require filtration and pressure regulation which drives market growth because these features maintain system performance and extend equipment lifespan. Farmers who use advanced system components are increasing their investment because of fertigation unit and digital controller adoption. The Food and Agriculture Organization supports agricultural efficiency frameworks which help farmers apply integrated irrigation systems to achieve better water productivity and reduced operational losses that drive segment growth.

By Crop Type

Field crops generated the highest revenue share in 2025 because they accounted for 41% of total segment sales. The Asia Pacific region continues to use drip irrigation for cotton, sugarcane and cereal crops because it enables better yield results which helps maintain their current market dominance. Farmers receive financial assistance through government irrigation subsidy programs and water conservation initiatives which enable them to switch from traditional flood irrigation methods to drip irrigation systems especially in regions with limited water resources. The current developments are enabling agricultural systems to implement large-scale projects which will maintain demand for this segment.

The fastest market growth between 2026 and 2035 will occur in the fruits and vegetable segment which will achieve 13.1% CAGR. The market grows due to higher demand for valuable crops and the emergence of export-focused horticulture and the requirement for precision irrigation to sustain crop quality. Commercial farmers prefer controlled irrigation because it helps them achieve better nutrient management and higher productivity. The Asian Development Bank supports development programs that focus on horticulture development and irrigation efficiency which will help emerging agricultural economies achieve segment growth.

By Emitter Type

Inline emitter systems held the largest market share in 2025 which generated about 58% of total system revenue. The system has become highly respected because farmers can easily set it up at low costs while using it for large-scale row crop and plantation farming operations. The system works because it delivers consistent water distribution while requiring less manual work, which has made it popular among developing countries. Farmers can use inline systems for agricultural modernization which the government supports because these systems help them achieve better irrigation efficiency through their scalable design.

The online emitter systems will achieve the fastest market growth between 2026 and 2035 with an expected CAGR of 12.6%. The system has flexible spacing and customization which makes it ideal for use in orchards and vineyards and uneven terrains. High-value crop producers want crop-specific irrigation solutions and precision farming practices which will lead to higher adoption rates among producers. The World Bank recommends efficient irrigation systems and sustainable agricultural practices which will help different farming systems to adopt these technologies.

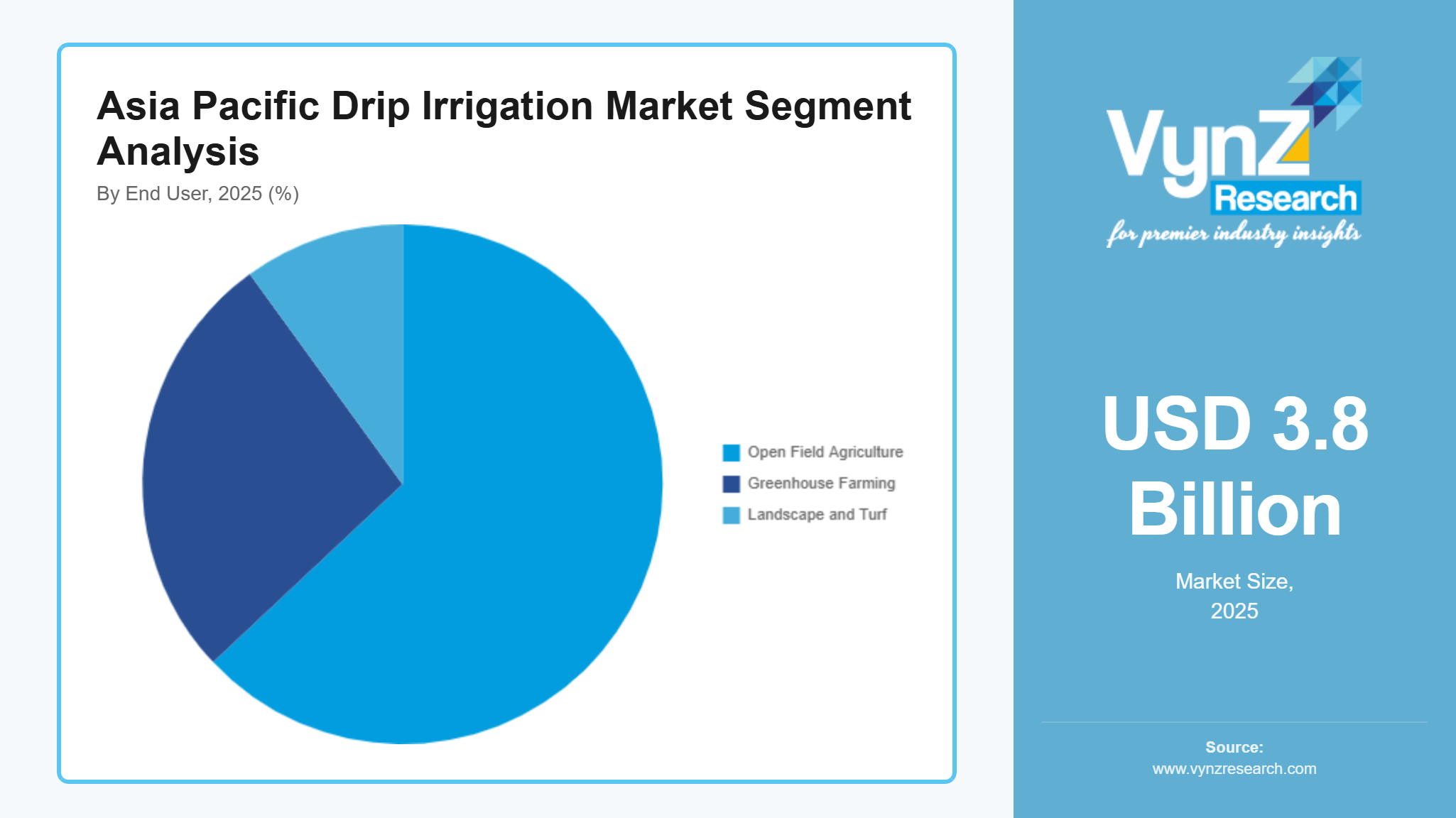

By End User

The open field agriculture segment held the largest market share in 2025 with a revenue contribution of 63% of total market earnings. The Asia Pacific region needs efficient irrigation systems for large-scale crop production because its vast agricultural land area supports extensive farming activities. Governments across this segment implement water conservation measures, irrigation efficiency programs and rural agricultural development initiatives which will enhance system adoption. The ongoing expansion of irrigation infrastructure together with subsidy-driven programs creates higher demand for modern irrigation systems among farmers who are transitioning to these systems.

The greenhouse farming and landscape applications market will achieve a 13.2% CAGR from 2026 until 2035. Controlled environment agriculture adoption is rising while the demand for high-quality produce and urban landscaping projects grows which creates market expansion. The adoption of irrigation automation and climate-controlled farming systems is driven by advances in both technologies. The Asian Development Bank has highlighted institutional support together with infrastructure investments which are driving advanced agricultural practices to expand which will create better growth opportunities for these end-use segments.

Regional Insights

China

China held approximately 28% of the Asia Pacific drip irrigation market during 2025 due to its extensive agricultural operations, rising water shortages in northern territories and government initiatives dedicated to enhancing irrigation systems. The agricultural market continues expanding through demand from major provinces which include Xinjiang, Henan and Shandong that cultivate high-value crops and operate in water-intensive agricultural areas. The commercial farms are adopting modern irrigation systems and water-saving technologies because the policy frameworks which support these technologies are promoting their use.

India

India will account for about 24% of the market according to predictions made for 2025. The market maintains its upward trajectory because of strong policy backing, rising micro irrigation system usage and increasing groundwater resource problems. The demand for agricultural products shows continuous growth because farmers are using more land for sugarcane and cotton and horticulture in Maharashtra and Gujarat and Tamil Nadu states.

Australia

Australia held an approximate 12% market share within the regional market during 2025 through its implementation of modern agricultural methods and its high level of precision irrigation technology usage and its growing commitment to water conservation in desert areas. The growth of the market depends on commercial farming operations which require efficient irrigation systems to utilize their restricted water resources especially in New South Wales and Victoria.

Japan and Southeast Asia

The market share for Japan and Southeast Asia was about 14% of the total market size during 2025. The regions experience growth because farmers adopt greenhouse farming methods and high-value crop demand rises and agricultural practices begin modernizing. The countries of Japan, Thailand, Vietnam and Indonesia observe steady adoption of drip irrigation systems for their horticulture and controlled environment agriculture.

Competitive Landscape / Company Insights

The market operates at a medium level of competition because both international and domestic companies work to develop new products and establish their market presence through pricing and product distribution methods. The companies are now directing their financial resources toward research and development activities which include digital irrigation technology and complete farming solution development to enhance their market competitiveness. The agricultural system of the region will protect its competitive advantages through innovative development activities which result from the implementation of water-saving systems and intelligent irrigation technologies that the Food and Agriculture Organization considers sustainable development standards.

Mini Profiles

Chinadrip Irrigation Equipment Co., Ltd. focuses on cost-effective drip irrigation systems and components, supported by strong manufacturing capabilities, domestic distribution networks, and competitive pricing strategies across large-scale agricultural regions in Asia Pacific.

EPC Industries Limited operates in the mass segment, emphasizing affordable micro irrigation solutions, efficient water management technologies, and extensive dealer networks to serve small and medium-scale farmers across India and neighboring markets.

Hunter Industries leverages advanced engineering expertise and global distribution reach to expand market presence, offering high-performance irrigation systems, controllers, and smart water management solutions tailored for agriculture and landscape applications.

Irritec S.p.A. focuses on precision irrigation products and sustainable water management systems, supported by international presence, strong brand recognition, and continuous innovation in environmentally efficient agricultural technologies.

Jain Irrigation Systems Ltd. operates in both mass and premium segments, emphasizing integrated irrigation solutions, agri-tech innovations, and strong global distribution supported by government-backed agricultural development initiatives.

Key Players

- Chinadrip Irrigation Equipment Co., Ltd.

- EPC Industries Limited

- Hunter Industries

- Irritec S.p.A.

- Jain Irrigation Systems Ltd.

- Lindsay Corporation

- Mahindra EPC Irrigation Ltd.

- Netafim Limited

- Rain Bird Corporation

- Rivulis Irrigation Ltd.

- The Toro Company

Recent Developments

In February 2026, Netafim was involved in discussions regarding a potential acquisition of a controlling stake by an international consortium, reflecting increasing consolidation in precision irrigation markets. The development highlights strategic interest in expanding digital agriculture capabilities and global irrigation infrastructure.

In 2025, Rain Bird Corporation strengthened its smart irrigation portfolio through the acquisition of Rachio, a company specializing in intelligent sprinkler controllers. This move enhances its digital irrigation capabilities and supports expansion into data-driven water management solutions.

In November 2025, Hunter Industries continued expanding its advanced irrigation product portfolio, focusing on high-efficiency controllers and system components designed for precision water management. The company emphasized professional distribution networks and integrated system solutions to strengthen its competitive positioning.

In 2026, Jain Irrigation Systems strengthened its position in the micro irrigation sector through ongoing investments in technology-driven irrigation solutions and expansion of integrated agri-services. The company continues to focus on improving water-use efficiency and supporting sustainable farming practices across key markets.

In 2025, Rivulis Irrigation advanced its global expansion strategy by strengthening its presence across Asia Pacific and Europe through technology-driven irrigation solutions. The company continues to invest in precision irrigation systems and digital farming integration to enhance agricultural productivity.

Asia Pacific Drip Irrigation Market Coverage

Component Insight and Forecast 2026 - 2035

- Emitters / Drippers

- Drip Tubes / Laterals

- Filters

- Valves

- Pressure Pumps

- Controllers

- Fittings and Accessories

Crop Type Insight and Forecast 2026 - 2035

- Field Crops

- Fruits and Nuts

- Vegetables

- Plantation Crops

- Greenhouse Crops

Emitter Type Insight and Forecast 2026 - 2035

- Inline Emitters

- Online Emitters

End User Insight and Forecast 2026 - 2035

- Open Field Agriculture

- Greenhouse Farming

- Landscape and TurfTop of Form

- Bottom of Form

Asia Pacific Drip Irrigation Market by Region

- China

- By Component

- By Crop Type

- By Emitter Type

- By End User

- Japan

- By Component

- By Crop Type

- By Emitter Type

- By End User

- India

- By Component

- By Crop Type

- By Emitter Type

- By End User

- South Korea

- By Component

- By Crop Type

- By Emitter Type

- By End User

- Vietnam

- By Component

- By Crop Type

- By Emitter Type

- By End User

- Thailand

- By Component

- By Crop Type

- By Emitter Type

- By End User

- Malaysia

- By Component

- By Crop Type

- By Emitter Type

- By End User

- Rest of Asia-Pacific

- By Component

- By Crop Type

- By Emitter Type

- By End User

Table of Contents for Asia Pacific Drip Irrigation Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Crop Type

1.2.3. By

Emitter Type

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia Market Estimate and Forecast

4.1. Asia Market Overview

4.2. Asia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Emitters / Drippers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Drip Tubes / Laterals

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Filters

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Valves

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Pressure Pumps

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Controllers

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Fittings and Accessories

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.2. By Crop Type

5.2.1. Field Crops

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Fruits and Nuts

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Vegetables

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Plantation Crops

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Greenhouse Crops

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Emitter Type

5.3.1. Inline Emitters

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Online Emitters

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Open Field Agriculture

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Greenhouse Farming

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Landscape and TurfTop of Form

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Bottom of Form

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Component

6.2. By

Crop Type

6.3. By

Emitter Type

6.4. By

End User

7. Japan Market Estimate and Forecast

7.1. By

Component

7.2. By

Crop Type

7.3. By

Emitter Type

7.4. By

End User

8. India Market Estimate and Forecast

8.1. By

Component

8.2. By

Crop Type

8.3. By

Emitter Type

8.4. By

End User

9. South Korea Market Estimate and Forecast

9.1. By

Component

9.2. By

Crop Type

9.3. By

Emitter Type

9.4. By

End User

10. Vietnam Market Estimate and Forecast

10.1. By

Component

10.2. By

Crop Type

10.3. By

Emitter Type

10.4. By

End User

11. Thailand Market Estimate and Forecast

11.1. By

Component

11.2. By

Crop Type

11.3. By

Emitter Type

11.4. By

End User

12. Malaysia Market Estimate and Forecast

12.1. By

Component

12.2. By

Crop Type

12.3. By

Emitter Type

12.4. By

End User

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Component

13.2. By

Crop Type

13.3. By

Emitter Type

13.4. By

End User

14. Company Profiles

14.1.

Chinadrip Irrigation Equipment Co., Ltd.

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

EPC Industries Limited

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Hunter Industries

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

Irritec S.p.A.

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

Jain Irrigation Systems Ltd.

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Lindsay Corporation

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Mahindra EPC Irrigation Ltd.

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Netafim Limited

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Rain Bird Corporation

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Rivulis Irrigation Ltd.

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

14.11.

The Toro Company

14.11.1.

Snapshot

14.11.2.

Overview

14.11.3.

Offerings

14.11.4.

Financial

Insight

14.11.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia Pacific Drip Irrigation Market