Europe Drip Irrigation Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Emitters/Drippers, Drip Tubes/Drip Lines, Filters, Valves, Pressure Pumps, Controllers and Sensors, Fittings & Accessories), by Application (Surface Drip Irrigation, Subsurface Drip Irrigation), by Crop Type (Field Crops, Orchard Crops & Vineyards, Vegetable Crops, Turf & Ornamentals, Plantation Crops)

| Status : Published | Published On : Mar, 2026 | Report Code : VRFB11040 | Industry : Food & Beverage | Available Format :

|

Page : 147 |

Europe Drip Irrigation Market Overview

The European Drip Irrigation Market, which was valued at approximately USD 2.2 billion in 2025 and is estimated to reach around 3.2 billion in 2026, is projected to reach close to USD 9.5 billion by 2035, expanding at a CAGR of about 15.1% during the forecast period from 2026 to 2035.

The continent's agricultural sector needs to adopt precision delivery technologies due to depleting groundwater resources and frequent severe droughts. The market expansion relies on the enforcement of strict environmental protection regulations and the substantial increase in agricultural labor expenses combined with rising use of autonomous systems.

The transition to micro-irrigation has become an essential requirement for commercial farming operations in Spain, Italy, and Germany, which represent the main regions of this trend. According to the European Commission, farming accounts for roughly 59% of all water abstraction in the region, which recently triggered the launch of the water resilience initiative in June 2025. The government-supported framework accelerates market adoption through its provision of substantial capital subsidies which the updated common agricultural policy delivers, thus reducing financial risks for small-to-medium scale farmers during their transitional phase.

Europe Drip Irrigation Market Dynamics

Market Trends

The market shows increasing technological changes which lead to different methods of acquiring resources between various farming operations and rapid growth for Internet of Things (IoT) sensors because farmers now prefer micro-irrigation systems which provide better operational efficiency through digital resource management. This new method enables automatic water distribution through actual soil moisture monitoring and localized climate assessment. The need for pressure-compensated and anti-clogging emitters has been increasing because new environmental standards require organizations to meet particular environmental requirements. The European Commission defines the water resilience strategy which began in June 2025 as a program that requires water services to adopt digital technologies for loss reduction because manufacturers must now include smart diagnostic tools into their standard drip lines to meet local regulatory needs.

Growth Drivers

The market expands because Mediterranean farmers require more water resources which creates continuous demand for this irrigation technology. The market expansion receives additional support from increased funding for smart agricultural systems and greenhouse upgrades because farmers now prioritize stable crop yields. The European Union modernized common agricultural policy (CAP) system plays a vital role in increasing technology adoption throughout Europe. European businesses need precision systems to control their expenses while achieving European green deal compliance, so they will keep purchasing these products during the entire prediction period. The European Investment Bank reports that more than €15 billion has been dedicated to water-smart agricultural changes, which aim to decrease water loss during transportation. The institutional support enables financial resources to flow continuously toward major farming improvements throughout Spain and Italy, which face water shortages because of climate change.

Market Restraints / Challenges

The market shows positive growth opportunities, but certain factors will prevent its development. High upfront capital expenditure, such as the initial costs for filtration units and automation hardware, continues to affect profitability and market penetration, particularly among price-sensitive smallholder farmers. The lack of skilled workers who understand system design and pressure management systems creates difficulties for production operations. The need for skilled workers to handle complicated setups and maintain delicate sensor equipment results in expenses which reduce operation capacity during economic downturns. The European Environment Agency reports that fragmented groundwater licensing and the complexity of transboundary water regulations frequently slow down the approval process for new irrigation projects. The combination of regulatory requirements and the potential for emitter damage from recycled water high mineral content functions as a major obstacle which prevents quick and complete micro-irrigation system implementation.

Market Opportunities

High market potential exists for precision-fertigation and automated nutrient delivery systems, which will benefit from technological progress in wireless connectivity. Companies that provide modular and high-performance solutions will benefit from the increasing demand which horticultural and viticultural groups need to reduce their operational expenses. The market for biodegradable drip lines will create another significant opportunity because the demand for eco-friendly materials will increase, which will lead to higher profit margins. Cloud-based decision support tool development will enable customers to interact better with businesses because farmers will receive concrete information which increases conversion rates. The European Commission states that irrigation providers should create systems which work with reclaimed water sources because the new water reuse regulation will now give them this opportunity. The manufacturing process of advanced filtration and chemical-resistant irrigation components will create new sources of income through the manufacturing process because these manufacturers will need to adapt to circular water economy operations.

Europe Drip Irrigation Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.2 Billion |

|

Revenue Forecast in 2035 |

USD 9.5 Billion |

|

Growth Rate |

15.1% |

|

Segments Covered in the Report |

By Component, By Application, By Crop Type |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Western Europe, Southern Europe, Northern Europe, Eastern Europe |

|

Key Companies |

AZUD, Hunter Industries, Irritec S.p.A., Jain Irrigation Systems Ltd., Metzer Group, Netafim, Novagric, Rain Bird Corporation, Rivulis, The Toro Company |

|

Customization |

Available upon request |

Europe Drip Irrigation Market Segmentation

By Component

The drip tube and drip line segment dominated the market in 2025 by generating approximately 30% of total regional revenue through its usage in large-scale field crops and its frequent replacement in high-salinity agricultural areas. The segment's dominance is reinforced by the persistent need for durable, UV-resistant lateral lines that can withstand the intense solar radiation of Mediterranean farming clusters.

The period from now until 2035 will see controllers and sensors achieve the fastest growth according to projections with their market volume expected to grow at a compound annual growth rate of approximately 14%. The fast growth of Internet of Things (IoT) node deployment together with rising demand for data-based moisture management to handle drought cycles drives this acceleration in technology adoption.

Commercial vineyards and orchards now utilize high adoption rates of these tools which allow for water application reductions of up to 30% when compared to traditional timer-based scheduling methods. The European Commission's 2025 Water Resilience Strategy identifies irrigation infrastructure digitalization as its main goal while smart controller market access for mid-sized enterprises improves through capital subsidies which lower market entry costs.

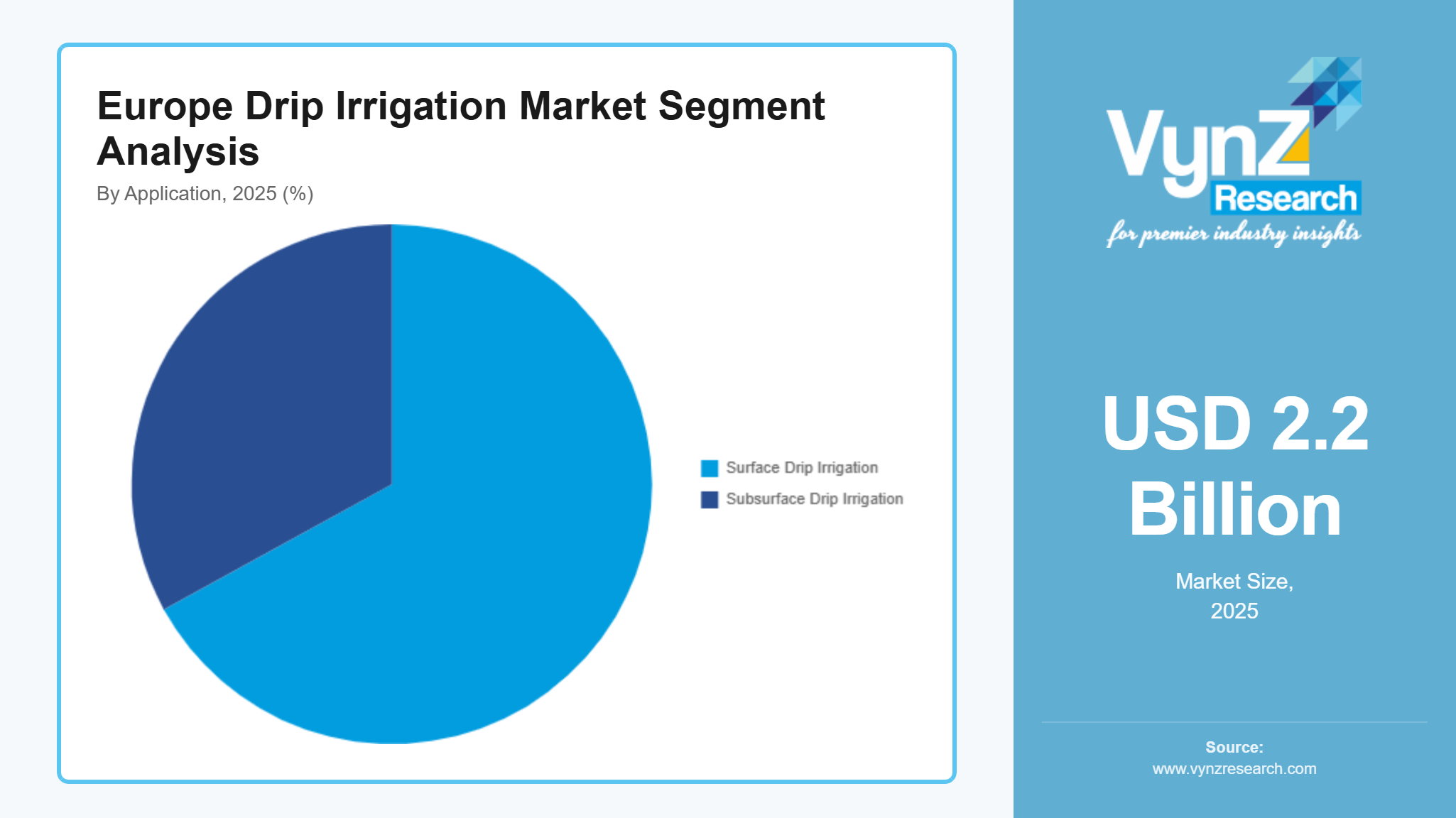

By Application

The surface drip irrigation system maintained its market leadership position through 2025 by securing 67% of market share because buyers preferred its easy installation and simple maintenance and lower upfront costs. The segment specifically focuses on growing seasonal vegetables and row crops because those crops require equipment to be relocated or rearranged. French and German traditional farming operations continue to prefer the system because emitter visibility enables them to conduct immediate troubleshooting and mechanical validation of their equipment.

The subsurface drip irrigation market now represents its fastest-growing segment which will expand at a 11.6% CAGR throughout 2035 because water-scarce regions such as Spain and Italy require maximum water-use efficiency. The buried line system provides a strategic benefit for permanent crops because it stops weed growth while eliminating evaporative losses between crop rows. The market for subsurface systems continues to develop because root-resistant emitters and automated flushing systems now reduce possibilities of system blockage which used to impede system growth. The European Environment Agency mandates that agricultural water extraction must decrease by 10% by 2030 to achieve resilience targets which drives the shift toward subsurface solutions in high-value horticulture clusters.

By Crop Type

Field crops held the largest market share through 2025 because maize, cotton and sugar beet producers use drip systems instead of overhead sprayers to maximize their resource productivity. The dominance of these crops exists because farmers dedicate extensive arable land to these staples while wide-spacing drip solutions that support broad-acre applications have become available. The agricultural industry in the region depends on field crops as its main volume driver because their yield stability matches the unpredictable climate conditions.

Orchard crops and vineyards will expand faster because the global demand for premium European wine and stone fruits keeps growing. The segment will experience a 10.2% CAGR through 2035 because it offers higher margins while fertigation requires precise nutrient delivery to maintain correct fruit quality and size balance. Mediterranean basin vineyards serve strategic purposes leading to this category becoming the main area where high-performance pressure-compensated emitters get used. Spain achieves operational water efficiency above 90% in both greenhouse and vineyard operations which now serves as a guideline for specialized drip systems that drive agricultural policy changes throughout Europe.

Regional Insights

Southern Europe

The market in Southern Europe which includes Spain, Italy, Greece, Portugal, Cyprus and Malta held the largest share of about 56.5% in 2025. The Mediterranean basin depends on intensive horticulture and viticulture for its existence which creates a situation where more than 60% of all freshwater resources are used for irrigation. The European Commission Water Resilience Strategy for 2025 designates this area as the primary site to implement Water Efficiency First requirements which enable safe conversion to precise driplines through extensive financial support. Spanish and Italian national resilience plans will generate more than €12 billion in public and private funding by 2035 to protect their valuable exports from long-term hydrological challenges.

Western Europe

The market in Western Europe which includes Germany, France, United Kingdom, Netherlands and Belgium possessed a market share of about 25% in 2025. Automated precision systems are being adopted in this area because unpredictable summer heatwaves have changed the requirements for commercial viability. The French Ministry of Agriculture states that the 2025 water management decrees will fund smart irrigation controllers which achieve a 20% decrease in water abstraction. The Netherlands has developed a greenhouse sector which creates demand for closed-loop high-efficiency drip systems that operate in protected cultivation areas while achieving resource circularity.

Eastern Europe

Russia, Poland, Romania and Ukraine, which together held 12.5% of the market in 2025 is designated as a region with strong potential for economic development. The region expands through modernization projects which transform outdated infrastructure into climate-resilient field crop systems. The European Environment Agency EEA reports that Polish and Romanian farmers focus on food security and large-scale commercial farming which fuels their adoption of automated lateral-move and drip systems. The area will experience ongoing investment activities until 2035 as farmers work to maintain their essential grain and oilseed yields during changing precipitation conditions.

Northern Europe

Northern Europe includes Sweden, Denmark and Finland which together held 6% of the market in 2025. The cluster used to depend less on intensive irrigation but now its members use more irrigation because of flash droughts and their need for better production of high-efficiency specialty crops in controlled environments. The 2026 Nordic Agricultural Policy Framework states that precision water management must improve environmental performance while reducing soil nutrient loss from berry and vegetable farming operations. The market in this region develops through high-value applications which use advanced technology to create specialized products that meet the area's strict sustainability requirements.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, and the major players globally continue to invest heavily in R&D which results in the development of anti, clogging emitters and solar, powered systems, thus, consolidating their market standing against the local players. The European Commission points out that the latest agricultural technology initiatives highlight the use of "smart" hardware to comply with the Green Deal water, saving targets, which has led to the strategic mergers aimed at strengthening the regional supply chain resilience.

Mini Profiles

AZUD focuses on high-performance agricultural technology, emphasizing anti-clogging emitter performance and sustainable water-use culture to drive profitability for growers across more than 100 countries.

Hunter Industries leverages strategic partnerships and a robust global manufacturing footprint to expand its market presence within the residential, commercial, and professional agricultural irrigation and landscape sectors.

Irritec specializes in smart precision irrigation solutions, emphasizing the optimization of water resources through highly technological extrusion and injection molding processes for greenhouses and large-scale field crops.

Netafim leverages digital farming platforms and 60 years of innovation to expand its global presence, focusing on end-to-end precision irrigation solutions that address water scarcity for millions of farmers.

Rain Bird operates in the premium irrigation segment, emphasizing water conservation and "The Intelligent Use of Water" through a diverse portfolio of rotors, valves, and smart control technologies globally.

Key Players

- AZUD (Spain)

- Hunter Industries (USA/Europe)

- Irritec S.p.A. (Italy)

- Jain Irrigation Systems Ltd. (India/Europe)

- Metzer Group (Israel/Europe)

- Netafim (Orbia Precision Agriculture)

- Novagric (Spain)

- Rain Bird Corporation (USA/Europe)

- Rivulis (Singapore/Europe)

- The Toro Company (USA/Europe)

Recent Developments

In February 2026, Rain Bird Corporation has partnered with Spectrum Technologies and Watertronics, expanding the company's portfolio of soil data and pump monitoring solutions for golf course superintendents. This collaborations will help golf courses benefit from a broader range of agronomic insights to give choice and greater flexibility in how superintendents monitor course conditions and make irrigation decisions.

In February 2026, The Dosing 5G product line from Netafim was unveiled with the goal of improving fertigation management with AI-powered automation and remote monitoring features. FertiKit™ 5G, FertiOne™ 5G, NetaJet™ 5G, and NetaFlex™ 5G are all part of the Dosing 5G package which assist growers who manage protected cropping systems, open fields, and orchards.

In July 2025, The Irritec Group has announced that it has acquired the majority of Agrifim de Colombia, a company with over 45 years of expertise that was a pioneer in the introduction of drip irrigation technology in Colombia. This acquisition strengthens its presence in Latin America and reaffirms its commitment to the development of sustainable and efficient agriculture.

Europe Drip Irrigation Market Coverage

Component Insight and Forecast 2026 - 2035

- Emitters/Drippers

- Drip Tubes/Drip Lines

- Filters

- Valves

- Pressure Pumps

- Controllers and Sensors

- Fittings & Accessories

Application Insight and Forecast 2026 - 2035

- Surface Drip Irrigation

- Subsurface Drip Irrigation

Crop Type Insight and Forecast 2026 - 2035

- Field Crops

- Orchard Crops & Vineyards

- Vegetable Crops

- Turf & Ornamentals

- Plantation Crops

Europe Drip Irrigation Market by Region

- Germany

- By Component

- By Application

- By Crop Type

- U.K.

- By Component

- By Application

- By Crop Type

- France

- By Component

- By Application

- By Crop Type

- Italy

- By Component

- By Application

- By Crop Type

- Spain

- By Component

- By Application

- By Crop Type

- Russia

- By Component

- By Application

- By Crop Type

- Rest of Europe

- By Component

- By Application

- By Crop Type

Table of Contents for Europe Drip Irrigation Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Application

1.2.3. By

Crop Type

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Emitters/Drippers

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Drip Tubes/Drip Lines

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Filters

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Valves

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Pressure Pumps

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Controllers and Sensors

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Fittings & Accessories

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Surface Drip Irrigation

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Subsurface Drip Irrigation

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Crop Type

5.3.1. Field Crops

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Orchard Crops & Vineyards

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Vegetable Crops

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Turf & Ornamentals

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Plantation Crops

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Component

6.2. By

Application

6.3. By

Crop Type

7. U.K. Market Estimate and Forecast

7.1. By

Component

7.2. By

Application

7.3. By

Crop Type

8. France Market Estimate and Forecast

8.1. By

Component

8.2. By

Application

8.3. By

Crop Type

9. Italy Market Estimate and Forecast

9.1. By

Component

9.2. By

Application

9.3. By

Crop Type

10. Spain Market Estimate and Forecast

10.1. By

Component

10.2. By

Application

10.3. By

Crop Type

11. Russia Market Estimate and Forecast

11.1. By

Component

11.2. By

Application

11.3. By

Crop Type

12. Rest of Europe Market Estimate and Forecast

12.1. By

Component

12.2. By

Application

12.3. By

Crop Type

13. Company Profiles

13.1.

AZUD (Spain)

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Hunter Industries (USA/Europe)

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Irritec S.p.A. (Italy)

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Jain Irrigation Systems Ltd. (India/Europe)

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Metzer Group (Israel/Europe)

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Netafim (Orbia Precision Agriculture)

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Novagric (Spain)

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Rain Bird Corporation (USA/Europe)

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Rivulis (Singapore/Europe)

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

The Toro Company (USA/Europe)

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Drip Irrigation Market