Ready to Eat Food Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Ready Meals, Ready-to-Cook (RTC) Food, Instant Noodles & Pasta, Snacks & Savory Products, Soups, Frozen Food, Baked Products, Meat & Poultry Products, Others), by Category (Vegetarian, Non-Vegetarian, Vegan), by Packaging Type (Canned, Frozen Packs, Retort Pouches, Vacuum Packs, Trays & Bowls, Others), by Distribution Channel (Supermarkets & Hypermarkets, Convenience Stores, Online Retail / E-commerce, Specialty Stores, Others), by End User (Household / Residential Consumers, Food Service Industry, Institutional Buyers, Travel & Transportation Sector, Others)

| Status : Published | Published On : Feb, 2026 | Report Code : VRFB11040 | Industry : Food & Beverage | Available Format :

|

Page : 182 |

Ready to Eat Food Market Overview

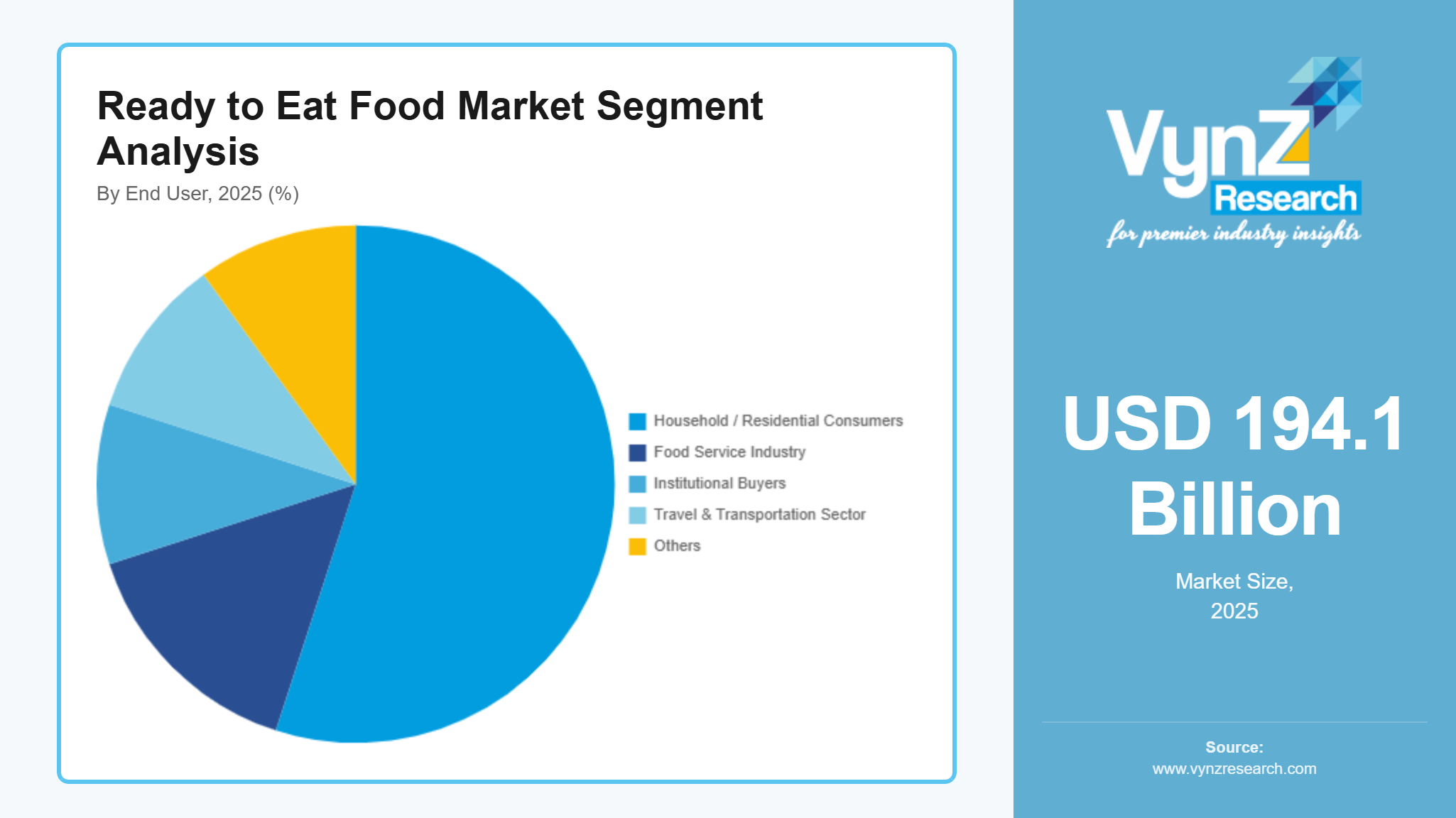

The ready to eat food market which was valued at approximately USD 194.1 billion in 2025 and is estimated to reach around USD 220.9 billion in 2026, is projected to reach close to USD 524.2 billion by 2035, expanding at a CAGR of about 10.1% during the forecast period from 2026 to 2035.

This market is primarily driven by rapid urbanization, changing lifestyles, and the growing need for convenience among working professionals and dual-income households. The rise in the number of women joining the work force and the time spent commuting has severely limited the amount of time to do house cooking, and the increased need of quick meal options. The increasing disposable income in the emerging market economies like India and China is also making consumers increase their spending on packaged and high-end ready meals. Besides, the growth of modern retail formats and electronic commerce platforms has enhanced product availability in both urban and semi urban regions. The sustained product innovation, like the healthier, organic, and plant-based ready-to-eat products is appealing to health-conscious consumers. Advancements in packaging technologies like the retort processing and vacuum sealing have increased shelf life and food safety which has helped in the further growth of the market. Major food companies are also contributing to consumer adoption in the world by aggressively promoting their products and having solid distribution channels.

Ready to Eat Food Market Dynamics

Market Trends

The development of plant-based and alternative protein meals is one of the significant trends defining the ready to eat food market. Growing consumerism regarding health, sustainability, and animal welfare is promoting a move towards vegetarian, vegan, and flexitarian diets. The perceived healthiness of many plant-based ready meals makes them more preferred by consumers since they contain less saturated fats and do not have any cholesterol. In Canada, government investment of nearly USD 110 million through the National Research Council’s Sustainable Protein Production Programme focuses on expanding processing capabilities for plant-based proteins and strengthening industry value chains, with initiatives linking agricultural crops to protein processing hubs. Meanwhile, bioenvironmental issues of livestock production such as greenhouse gases emissions and water consumption are fueling the need to seek sustainable protein sources. Food manufacturers are reacting by offering ready-made meals with soy, pea protein, lentils, and chickpeas among other foods that are of plant origin. Plant-based meals are becoming more attractive to the mainstream population because of innovations in taste, texture, and meat substitutes. Also, good advertisement campaigns and increased distribution at the supermarkets and online stores are enhancing the uptake around the world.

Growth Drivers

The increased disposable income is a key growth driver of the ready to eat food market because an increase in earnings allows consumers to buy more premium and convenient food. The growing populations of the middle classes in the emerging economies, including India, China and the Southeastern Asian nations, are increasingly adopting the packaged meals which save time and efforts. The consumers also have the capacity to indulge in foreign dishes, fancy ready-made meals, and fancier foods that are healthier and can be more expensive than home-cooked meals. Urban families, especially two-income families, are expanding their budgets on items that are convenient. The Government of India’s Production Linked Incentive (PLI) Scheme for Food Processing provides financial incentives (4–10% of incremental sales) to food manufacturers, including ready-to-eat/ready-to-cook foods, to boost production capacity and brand visibility, driving industry investments and scaling operations that benefit from rising consumption. Moreover, the growing per capita income promotes demand for branded and quality-assured food products and consolidates the organized retail sales. The requirement of convenience, variety and quality is also becoming a priority among the customers as the purchasing power increases, and this is boosting the ready to eat food market.

Market Restraints / Challenges

Great competition and price sensitivity are major threats of ready to eat food market. The market is very fragmented with many international brands, regional manufacturers and own-label products that compete in the market. The result of this stiff competition is the aggressive pricing strategies, discounts, and promotional campaigns, which tend to squeeze the profit margins. In price-elastic markets, especially in the least developed economies, people are less loyal to a brand and focused more on the price of the product, therefore it is hard to scale up with premium products. Moreover, the availability of local competitors with low-cost variants increases the pressure on the price of the old brands. Competition is also further escalated with Supermarkets and retail chains offering their own brand of ready meals at competitive rates. Consequently, businesses are forced to constantly strike the right balance between cost-efficiency, quality, and innovations to ensure that they are profitable whilst being competitive.

Market Opportunities

The ready to eat food market is experiencing a lot of growth opportunities due to the technological advances in food processing. Retort processing, high-pressure processing (HPP) and new freezing methods are modern preservation methods aimed at increasing shelf life without compromising taste, texture, and nutritional value. These new technologies minimise the use of unnecessary preservatives and respond to market preferences of cleaner labels and more healthful products. Better automation and intelligent manufacturing are also boosting the efficiency and consistency of production which reduces the cost of operation in the long run. Also, aseptic, and vacuum packaging technologies enhance food safety and reduce chances of contamination during storage and transportation. The innovations in cold chain logistics also enable ready meals with a shorter shelf life to be distributed to more geographic areas.

Global Ready to Eat Food Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 194.1 Billion |

|

Revenue Forecast in 2035 |

USD 524.2 Billion |

|

Growth Rate |

10.1% |

|

Segments Covered in the Report |

Product Type, Category, Packaging Type, Distribution Channel, End User, Region |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Nestlé S.A., Unilever PLC, The Kraft Heinz Company, Conagra Brands, Inc., General Mills, Inc., Tyson Foods, Inc., Hormel Foods Corporation, McCain Foods Limited, The Campbell’s Company, ITC Limited, Ajinomoto Co., Inc., Dr. Oetker GmbH |

|

Customization |

Available upon request |

Ready to Eat Food Market Segmentation

By Product Type

Ready Meals is the largest category with a market share of about 25% in 2025, due to the high consumer demand towards whole and easy meals that need little preparation. Urbanization and two-earner families are favoring the demand of ready to serve full course meals. Extensive distribution in the supermarkets and online stores reinforces its supremacy. This is further enhanced by continuous innovation of flavor, healthier options, and premium offerings, which increases adoption. The networks of its distribution throughout North America, Europe, and Asia-Pacific make it leaders.

Frozen Food is the fastest-growing category with a CAGR of 10.4% during the forecast period, due to the improvement in the freezing and cold-chain technologies that preserve the taste and nutrients. Consumer acceptance is increasing due to growing needs in the shelf life and lowered food waste. Growth in the organized retail and freezer network in the new markets is increasing the penetration. The producers are launching vegan and fancy frozen foods to appeal to consumers. The convenience and the preservation of quality are still factors in enhancing rapid growth in this segment.

By Category

Non-Vegetarian is the largest category with a market share of about 50% in 2025, due to high global consumption of meat, poultry, and seafood-based ready meals. Strong protein demand and consumer preference for traditional meat-based cuisines support its dominance. Developed markets show high per capita meat consumption, reinforcing steady sales. Manufacturers continuously expand product portfolios with diversified meat options. Established supply chains and strong brand loyalty further sustain category leadership.

Vegan is the fastest-growing category with a CAGR of 10.5% during the forecast period, driven by increasing adoption of plant-based diets and sustainability concerns. Rising health awareness and demand for cholesterol-free meal options are encouraging consumers to shift toward vegan ready meals. Innovation in alternative protein sources such as soy, pea, and lentils is enhancing product appeal. Younger consumers and flexitarians are significantly contributing to segment expansion. Strong marketing and expanding retail presence are accelerating growth momentum.

By Packaging Type

Frozen Packs is the largest category with a market share of about 35% in 2025, because it has extended shelf life and food quality is maintained. These packs are commonly applied to ready meals, meat products, and snacks that need the store at a certain temperature. The developed cold-chain logistics in developed economies promote adoption in large numbers. Frozen packaging is desirable because it is efficient in stocking. The domination is also reinforced with continuous advances in technology of the freezers.

Retort Pouches is the fastest-growing category during the forecast period, owing to their light weight, portability, and affordability. These pouches allow shelf life that is long and does not require refrigeration so that they are suitable in the emerging markets. On-the-go consumption is gaining momentum because of the increasing demand. Manufacturers prefer retort pouches due to lower transportation expenses and better sustainability records. Advancement in the flexible packaging materials is further boosting the expansion of the segments.

By Distribution Channel

Supermarkets & Hypermarkets is the largest category with a market share of about 40% in 2025, driven by extensive product variety and strong consumer footfall. Organized retail provides greater visibility, promotional offers, and brand comparison opportunities. Consumers prefer one-stop shopping experiences for grocery purchases. Established retail chains across developed and emerging markets sustain high sales volumes. Strategic shelf placement and in-store marketing further strengthen dominance.

Online Retail / E-commerce is the fastest-growing category with a CAGR of 10.8% during the forecast period, fueled by increasing digital adoption and doorstep delivery convenience. Growth of quick-commerce and grocery apps is transforming purchasing behavior. Subscription-based meal models are gaining popularity among urban consumers. Attractive discounts and wider product accessibility enhance online penetration. Expanding internet access in emerging economies continues to accelerate growth.

By End User

Household / Residential is the largest category with a market share of about 55% in 2025, as the need to have convenient daily meals solutions will increase among working professionals and families. The number of urban consumers who adopt ready to eat dishes to save time on cooking is increasing. The increase in disposable income favors the increased expenditure on packaged meals. The strong household consumption is further enhanced by the wide retail accessibility. Segment dominance is maintained through changes in eating habits and the hectic lifestyles.

Food Service is the fastest-growing category during the forecast period, due to the increasing demand of hotels, airlines, corporate cafeterias, and quick-service restaurants. Ready meal components are standardized to cut down on time and labor expenses of preparing the food. Increase in travel and hospitality business is promoting bulk purchases. Institutional purchasers would want predictable quality and supply effectiveness. The trend of outsourcing food preparation is also increasing and boosting expansion in this segment.

Regional Insights

North America

North America is the largest regional market for the ready to eat food market, supported by high consumer purchasing power and strong demand for convenient meal solutions. United States and Canada boast a well-maintained packaged food and developed cold-chain infrastructure. The consumption is still driven by busy lives, increased workforce contribution, and increased preference of food that can be consumed on-the-go. Large food producers constantly launch high quality, organic, and health-conscious ready food products to cater to changing tastes. the U.S. Department of Agriculture’s Resilient Food Systems Infrastructure (RFSI) program has allocated about $400 million nationwide in federal funding to strengthen food processing, aggregation, and distribution infrastructure, including support for value-added and processing capacity that benefits ready-to-eat food production. Distribution is also enhanced by high presence of supermarkets, hypermarkets, and online grocery shops.

Additionally, USDA’s National Institute of Food and Agriculture (NIFA) invested $6.8 million in 2025 through the Agriculture and Food Research Initiative’s Novel Foods and Innovative Manufacturing grants to advance science, technology, and innovative food manufacturing and processing methods. Moreover, there is a growing need for clean-label and plant-based products that are reshaping innovation in products within the region.

Asia Pacific

Asia-Pacific is the fastest-growing region in the ready to eat food market, driven by rapid urbanization, rising disposable incomes, and expanding middle-class populations. There are major changes in the food consumption toward convenience-oriented food in countries like China, India, Japan, and South Korea. Modern retail chains and the development of e-commerce platforms are increasing the accessibility of products both in the urban and semi-urban settings. India Production Linked Incentive Scheme for Food Processing Industry (PLISFPI): a central scheme with an approved outlay of ₹10,900 crore (INR) for 2021–22 to 2026–27 that incentivizes investment in modern food manufacturing, scale-up of processing lines, and adoption of advanced technologies by ready-to-eat manufacturers. The demand of packaged meals is increasing due to changing lifestyles, and more working hours and nuclear families. The interest of governments in food processing industries and better cold storage facilities also contribute to the growth of the market. The increasing popularity of local taste and the low-cost product offering remain to stimulate the growth rates.

Europe

Europe holds a significant position in the ready to eat food market due to strong demand for frozen meals and packaged convenience foods. Countries like the United Kingdom, Germany, and France have established stores and huge consumption of ready meals per capita. The issue of sustainability and health consciousness has motivated manufacturers to launch organic, plant-based, and clean-label products. The EU Funding Portal currently lists food-related grants worth approximately €12 million, aimed at supporting innovations in the food sector, including techniques, value-chain improvements, and market competitiveness which many ready meal producers can leverage. The quality of products and confident customer satisfaction is guaranteed by strict food safety and labeling regulations. There are also shifting market trends of increased use of recyclable packaging and energy efficient processing technologies. The constant innovation on the gourmet and international cuisine provides also contribute to regional demand.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, is witnessing steady growth in the ready to eat food market. The acceptance of packaged meals is rising with the increasing youth demographics and the exposure of the youth to the food patterns in the world. The African Development Bank (AfDB) is mobilizing approximately US$2.2 billion to establish Special Agro-Industrial Processing Zones across 28 states in Nigeria. Increased Supermarkets and convenience stores are enhancing product penetration. Despite price sensitivity being a major issue in certain markets, the picture is slowly improving as more people have disposable income and more people are joining the workforce which is boosting demand. The government effort to boost food processing and the growth of the retail sector will also boost the growth opportunities in the region.

Competitive Landscape / Company Insights

The ready to eat food market is fragmented in nature, with the presence of numerous global, regional, and local manufacturers competing across different product categories and price points. Large multinational food corporations have strong brand name, and distribution capabilities, yet the competitors in the region provide regional tastes, and cheaper options. The competitive intensity is further augmented by the market structure whereby the major retail chains could dominate the market with their brand of privately labeled products that have received significant shelf space.

The main competition among the companies is innovativeness of the products, differentiation of the packaging and growth in the healthy segment of the market with organic and plant-based meals. The common strategies to appeal to the changing consumer preferences include frequent new products and diversification of flavors. Good distribution networks in all the supermarkets, convenience stores, and e-commerce enable a firm to maintain market shares. Although big players enjoy economies of scale and highly developed processing capacities, smaller brands can compete by targeting the niche segmentation and regional customization of tastes.

Mini Profiles

Nestlé S.A. is a global food and beverage leader offering a wide portfolio of ready-to-eat meals, frozen foods, and prepared dishes through brands such as Maggi and Stouffer’s, focusing on product innovation, nutritional enhancement, and sustainable packaging solutions across international markets.

Unilever PLC operates in the convenient foods segment with a strong presence in ready meals, soups, and savory products, leveraging its global distribution network, brand strength, and continuous investment in plant-based and health-oriented meal solutions.

The Kraft Heinz Company provides a broad range of ready-to-eat and prepared food products, emphasizing convenience, flavor innovation, and strong retail partnerships, while expanding its portfolio with premium and clean-label offerings.

Conagra Brands, Inc. is a key player in frozen and shelf-stable ready meals, offering diverse products under well-established brands, supported by advanced food processing technologies and strong penetration across supermarkets and online channels.

General Mills, Inc. delivers convenient meal solutions including ready-to-serve and frozen food products, focusing on consumer-driven innovation, health-conscious formulations, and expanding e-commerce presence.

Key Players

- Nestlé S.A.

- Unilever PLC

- The Kraft Heinz Company

- Conagra Brands, Inc.

- General Mills, Inc.

- Tyson Foods, Inc.

- Hormel Foods Corporation

- McCain Foods Limited

- The Campbell’s Company

- ITC Limited

- Ajinomoto Co., Inc.

- Dr. Oetker GmbH

Recent Developments

January 2026 – Nestlé S.A. announced the expansion of its ready meal production capacity in Asia-Pacific, focusing on fortified and plant-based ready-to-eat offerings to meet rising urban demand and health-conscious consumer preferences.

December 2025 – The Kraft Heinz Company introduced a new line of premium frozen ready meals featuring clean-label ingredients and globally inspired flavors, targeting busy working professionals and expanding its presence in the convenience food segment.

October 2025 – Conagra Brands, Inc. launched a range of high-protein and low-calorie ready-to-eat bowls under its healthy lifestyle portfolio, aiming to strengthen its position in the growing health-focused convenience food category.

August 2025 – ITC Limited expanded its ready-to-eat manufacturing facility in India to increase production capacity and enhance distribution across Tier II and Tier III cities, supporting rising domestic demand for packaged meals.

June 2025 – General Mills, Inc. unveiled new sustainable packaging initiatives for its frozen and shelf-stable ready meal products, incorporating recyclable materials and improved portion control designs to reduce food waste and environmental impact.

Global Ready to Eat Food Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Ready Meals

- Ready-to-Cook (RTC) Food

- Instant Noodles & Pasta

- Snacks & Savory Products

- Soups

- Frozen Food

- Baked Products

- Meat & Poultry Products

- Others

Category Insight and Forecast 2026 - 2035

- Vegetarian

- Non-Vegetarian

- Vegan

Packaging Type Insight and Forecast 2026 - 2035

- Canned

- Frozen Packs

- Retort Pouches

- Vacuum Packs

- Trays & Bowls

- Others

Distribution Channel Insight and Forecast 2026 - 2035

- Supermarkets & Hypermarkets

- Convenience Stores

- Online Retail / E-commerce

- Specialty Stores

- Others

End User Insight and Forecast 2026 - 2035

- Household / Residential Consumers

- Food Service Industry

- Institutional Buyers

- Travel & Transportation Sector

- Others

Global Ready to Eat Food Market by Region

- North America

- By Product Type

- By Category

- By Packaging Type

- By Distribution Channel

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Category

- By Packaging Type

- By Distribution Channel

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Category

- By Packaging Type

- By Distribution Channel

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Category

- By Packaging Type

- By Distribution Channel

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Ready to Eat Food Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Category

1.2.3. By

Packaging Type

1.2.4. By

Distribution Channel

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Ready Meals

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Ready-to-Cook (RTC) Food

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Instant Noodles & Pasta

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Snacks & Savory Products

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Soups

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Frozen Food

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Baked Products

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Meat & Poultry Products

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.1.9. Others

5.1.9.1. Market Definition

5.1.9.2. Market Estimation and Forecast to 2035

5.2. By Category

5.2.1. Vegetarian

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Non-Vegetarian

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Vegan

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Packaging Type

5.3.1. Canned

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Frozen Packs

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Retort Pouches

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Vacuum Packs

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Trays & Bowls

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Others

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Distribution Channel

5.4.1. Supermarkets & Hypermarkets

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Convenience Stores

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Online Retail / E-commerce

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Specialty Stores

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Others

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Household / Residential Consumers

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Food Service Industry

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Institutional Buyers

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Travel & Transportation Sector

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Others

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Category

6.3. By

Packaging Type

6.4. By

Distribution Channel

6.5. By

End User

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Category

7.3. By

Packaging Type

7.4. By

Distribution Channel

7.5. By

End User

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Category

8.3. By

Packaging Type

8.4. By

Distribution Channel

8.5. By

End User

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Category

9.3. By

Packaging Type

9.4. By

Distribution Channel

9.5. By

End User

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Nestlé S.A.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Unilever PLC

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

The Kraft Heinz Company

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Conagra Brands, Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

General Mills, Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Tyson Foods, Inc.

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Hormel Foods Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

McCain Foods Limited

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

The Campbell’s Company

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

ITC Limited

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Ajinomoto Co., Inc.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Dr. Oetker GmbH

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Ready to Eat Food Market