Sports Nutrition Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Protein-focused nutrition products, Hydration & endurance products, Functional performance nutrition, Weight & lifestyle management nutrition), by Form (Powder-based, Liquid, Solid), by Distribution Channel (Offline, Online), by Ingredient Source (Animal-derived, Plant-derived, Blended formulations), by Application (Performance & recovery, Hydration & endurance, Weight & lifestyle management), by End User (Recreational fitness participants, Lifestyle-oriented consumers, Professional athletes)

| Status : Published | Published On : Feb, 2026 | Report Code : VRFB11038 | Industry : Food & Beverage | Available Format :

|

Page : 188 |

Sports Nutrition Market Overview

The sports nutrition market which was valued at approximately USD 28.50 billion in 2025 and is estimated to rise further up to almost USD 30.95 billion by 2026 is projected to reach around USD 65.03 billion by 2035 expanding at a CAGR of about 8.6% during the forecast period from 2026 to 2035.

Market expansion is supported by rising health awareness increasing participation in structured fitness activities and sustained demand for protein focused nutrition products. Expanding adoption among lifestyle consumers and recreational athletes continues to strengthen consumption patterns across North America, Europe, and Asia Pacific.

Growth momentum is reinforced by government backed nutrition and physical activity frameworks issued by institutions such as the World Health Organization, the Food and Agriculture Organization and National Public Health authorities. These programs emphasize balanced protein intake muscle health and regular physical activity to address lifestyle related disorders. Public investment in sports infrastructure community fitness initiatives and athlete development programs across North America, Europe, and Asia Pacific continues to support wider product uptake. Regulatory oversight related to food safety ingredient transparency and nutrition labeling compliance remains essential in sustaining consumer confidence and long-term market stability.

Sports Nutrition Market Dynamics

Market Trends

The industry is experiencing notable shifts driven by evolving consumer behavior and increasing alignment with preventive healthcare and wellness-oriented lifestyles. One of the key trends shaping the market is the rising preference for clean label and function specific formulations focusing on protein quality, micronutrient balance and digestive tolerance. This trend reflects growing awareness around long term health outcomes and regulatory backed dietary guidance encouraging balanced nutrient intake.

The increasing use of lifestyle-focused and customized nutrition plans that are backed by evidence-based dietary planning, exercise tracking, and digital health tools is another new trend. Government-backed nutrition frameworks from the Food and Agriculture Organization, the World Health Organization, and national health agencies place a strong emphasis on active living and individualized dietary adequacy, which continues to have an impact on product development and market positioning.

Growth Drivers

The growth of the market is largely supported by increasing public focus on physical activity fitness participation and structured exercise programs across urban and semi urban populations. Government led initiatives promoting physical activity and healthy diets under national non-communicable disease prevention strategies are generating sustained demand across multiple consumer segments.

Additionally, expanding investment in sports infrastructure, school level fitness programs and organized athletic development supported by ministries of health sports and education is accelerating market expansion.

Another key driver is rising consumer emphasis on performance recovery and nutritional compliance as individuals prioritize muscle health endurance and metabolic wellness. This has strengthened demand for protein supplements, functional beverages and recovery focused nutrition products throughout the forecast period.

Market Restraints / Challenges

Despite favorable growth prospects the sports nutrition market faces certain challenges that may limit expansion. Regulatory complexity related to ingredient approval health claims and labeling standards continues to affect product launches and market penetration particularly among smaller manufacturers and emerging brands. Government food safety authorities and public health agencies impose strict compliance requirements to ensure consumer protection which can increase development timelines and cost burdens.

Furthermore, price sensitivity among mass market consumers poses an additional challenge as dependence on high quality protein sources, imported raw materials and specialized processing technologies can elevate production costs. These factors may constrain affordability and limit adoption in price sensitive and developing consumer segments during periods of economic uncertainty.

Market Opportunities

The market presents significant opportunities in expanding lifestyle and preventive nutrition adoption particularly driven by demographic shifts toward aging populations and rising incidence of lifestyle related health conditions. Companies offering scientifically validated and affordable nutrition solutions aligned with public dietary recommendations are well positioned to capture incremental demand from health-conscious consumers.

Another key opportunity lies in premium and specialized nutrition categories supported by government backed athlete development programs, military nutrition standards and clinical nutrition research initiatives. Rising investment in digital nutrition platforms, evidence-based formulation and traceable ingredient sourcing is creating pathways for higher margin offerings and long-term consumer engagement while enhancing trust and regulatory alignment across key markets.

Global Sports Nutrition Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 28.50 Billion |

|

Revenue Forecast in 2035 |

USD 65.03 Billion |

|

Growth Rate |

8.6% |

|

Segments Covered in the Report |

By Product Type, By Form, By Distribution Channel, By Ingredient Source, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, GCC Region, Other Regions |

|

Key Companies |

Abbott Laboratories Inc., Amway Corp., Atlantic Multipower, BPI Sports, BSN (Bio‑Engineered Supplements and Nutrition) Nutrabolt, Clif Bar & Company, Coca‑Cola Company, Nestlé S.A., PepsiCo Inc. |

|

Customization |

Available upon request |

Sports Nutrition Market Segmentation

By Product Type

Protein-focused nutrition products accounted for approximately 44% of total market revenue in 2025, representing the largest share due to high repeat consumption frequency strong brand penetration and broad relevance across strength training endurance and lifestyle fitness routines. This segment benefits from alignment with government backed dietary protein intake guidelines that emphasize muscle maintenance metabolic health and physical resilience. Its dominance is further reinforced by stable pricing structures and widespread availability across both offline and digital retail channels.

Other nutrition categories continue to contribute meaningfully to overall revenue, particularly hydration and endurance focused offerings which held an estimated 28% share in 2025, supported by usage during prolonged physical activity and sports participation.

Meanwhile, functional performance nutrition products are expected to register the fastest expansion with an estimated CAGR of 6.9% during the forecast period, driven by formulation innovation clean label positioning and increasing adoption of targeted nutrition solutions among fitness conscious consumers seeking measurable performance outcomes.

By Form

Powder-based products dominated the market in 2025 accounting for approximately 49% of total revenue, supported by cost efficiency longer shelf life and ease of portion control. This form is widely preferred among regular fitness participants and institutional buyers due to logistical advantages and compatibility with regulatory labeling standards enforced by food safety authorities. Its dominance is also supported by bulk purchasing behavior and consistent usage across training cycles.

Liquid formulations are emerging as the fastest growing category and are expected to expand at an estimated CAGR of 6.7% through 2035. Growth is driven by convenience-oriented consumption rising demand for ready to consume solutions and expanding urban lifestyles that favor portability.

Solid formats accounted for roughly 21% of market revenue in 2025, maintaining relevance in structured nutrition routines such as endurance events and controlled dietary supplementation. Government backed nutrition awareness programs emphasizing portion accuracy and safe consumption continue to support balanced growth across all forms.

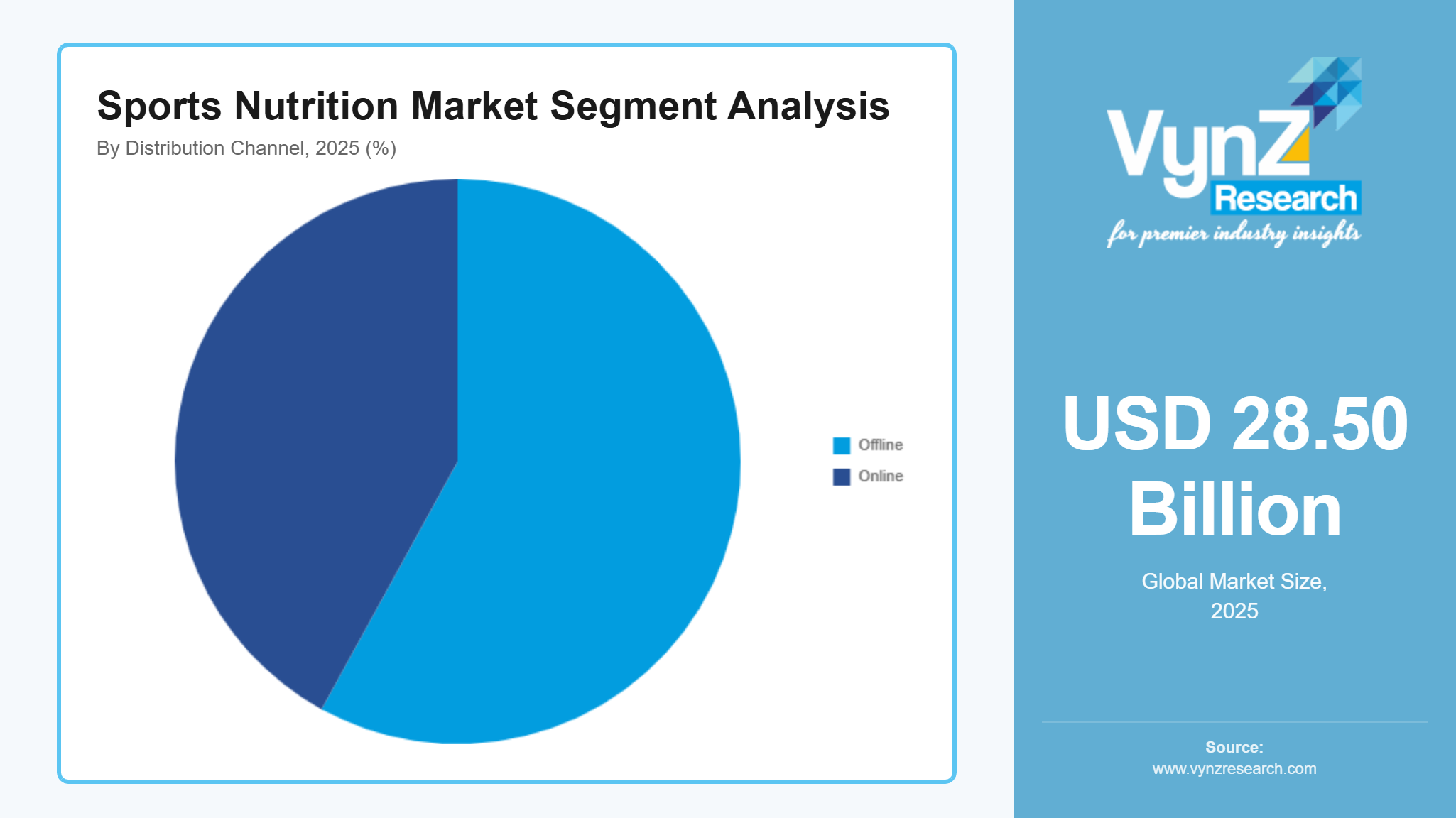

By Distribution Channel

Offline channels accounted for approximately 58% of total sales in 2025, maintaining dominance due to consumer reliance on in store validation professional recommendations and immediate product availability. Specialty nutrition stores pharmacies and fitness centers benefit from regulatory oversight-controlled storage environments and direct consumer engagement which reinforces trust particularly among first time buyers and older demographics.

Online distribution is witnessing accelerated growth and is projected to register a CAGR of about 7.4%, the fastest among all channel categories. Expansion is supported by increasing digital penetration improved last mile logistics and transparent pricing structures. Integration of digital platforms with physical retail networks is further enhancing consumer reach and enabling subscription-based purchasing models. Government initiatives supporting digital commerce consumer protection and data security frameworks are strengthening confidence in online nutrition purchasing contributing to sustained channel level expansion.

Animal derived ingredients accounted for approximately 52% of total market revenue in 2025, supported by established consumption patterns, strong amino acid profiles and long-standing acceptance among professional and recreational athletes. This segment benefits from extensive scientific validation and regulatory clarity around safety and nutritional efficacy.

Animal derived ingredients accounted for approximately 52% of total market revenue in 2025, supported by established consumption patterns, strong amino acid profiles and long-standing acceptance among professional and recreational athletes. This segment benefits from extensive scientific validation and regulatory clarity around safety and nutritional efficacy.

Plant derived formulations are gaining traction and are expected to grow at an estimated CAGR of 6.8%, driven by rising interest in sustainable nutrition lactose free alternatives and ethical consumption trends. Growth is further supported by government backed dietary diversification guidance and increasing inclusion of plant protein in public nutrition recommendations.

Blended formulations held around 18% share in 2025, offering balance between functionality and dietary inclusivity. Ongoing innovation in ingredient processing and labeling transparency continues to influence source-based purchasing decisions.

By Application

Performance and recovery-oriented applications accounted for approximately 46% of total market demand in 2025, reflecting high usage intensity among fitness enthusiasts and structured training participants. These applications benefit from strong alignment with government backed physical activity guidelines that emphasize post exercise recovery and injury prevention.

Hydration and endurance focused applications represented an estimated 27% share, supported by organized sports participation and outdoor activity trends.

Weight and lifestyle management applications are expected to register the fastest growth with an estimated CAGR of 6.5%, driven by preventive healthcare adoption and rising focus on metabolic wellness. Public health programs promoting active lifestyles and balanced energy intake continue to reinforce demand across application categories contributing to diversified and resilient market expansion.

By End User

Recreational fitness participants accounted for approximately 48% of total market revenue in 2025, making this the largest end use group due to expanding gym memberships, urban fitness culture and rising awareness around daily protein intake. This segment benefits significantly from public investment in community fitness infrastructure and national physical activity promotion programs.

Lifestyle oriented consumers are expected to witness the fastest growth registering an estimated CAGR of 6.6% during the forecast period. Growth is driven by preventive health adoption, aging yet active populations and alignment with government backed wellness and nutrition education initiatives.

Professional athletes accounted for roughly 19% of market revenue, supported by institutional procurement, standardized performance nutrition protocols and elite sports development programs. Together, these end use groups provide a stable and diversified demand base for long-term market growth.

Regional Insights

North America

North America accounted for approximately 29% of the market in 2025, driven by high health awareness, strong fitness culture, and widespread gym membership penetration. Major cities including New York, Los Angeles, and Chicago continue to generate strong demand for protein supplements, sports drinks, and functional nutrition products. Government-backed initiatives, such as the U.S. Department of Health and Human Services physical activity guidelines and the Dietary Guidelines for Americans, encourage preventive health measures and balanced nutrient intake, further supporting regional market growth. Expansion of specialty retail outlets, pharmacies, and online nutrition platforms is enhancing accessibility, driving sustained revenue growth with an estimated CAGR of 6.1% through 2035.

Europe

Europe represented approximately 25% of the market in 2025, with growth supported by increasing participation in structured fitness programs and rising adoption of clean label and plant-based nutrition products. Urban centers such as London, Berlin, and Paris are key consumption hubs, benefiting from government nutrition campaigns and national dietary guidelines issued across EU member states. Public health authorities encourage protein and micronutrient intake among active populations, while regulatory frameworks ensure product quality and labeling transparency. Online retail and e-commerce channels are rapidly expanding, facilitating wider distribution and faster product penetration. The segment is expected to grow at an estimated CAGR of 6.4% during the forecast period.

Asia Pacific

Asia Pacific accounted for roughly 24% of the market in 2025, driven by urbanization, rising disposable incomes, and increasing consumer awareness regarding fitness and preventive health. Countries including China, India, Japan, and Australia are witnessing growing demand for protein powders, performance nutrition, and ready-to-drink supplements. Government-backed initiatives, such as China’s Healthy China 2030 program, India’s Fit India Movement, and public dietary guidance frameworks, are promoting active lifestyles and balanced nutrition, supporting adoption among both recreational and lifestyle consumers. Expansion of organized fitness centers and digital nutrition platforms in metropolitan areas is further enhancing regional market revenue. The region is projected to grow at an estimated CAGR of 6.7% through 2035.

GCC Region

The GCC region accounted for approximately 10% of the market in 2025, with growth supported by rising health awareness, government investment in sports infrastructure, and increasing gym memberships in countries such as Saudi Arabia, the UAE, and Qatar. National health campaigns emphasize fitness and proper nutrition, while high disposable incomes encourage adoption of premium protein and performance nutrition products. Online retail platforms are increasingly complementing traditional specialty nutrition stores, providing consumers with broader access to imported and locally manufactured products. Market expansion in the region is projected at a CAGR of 6.5% over the forecast period.

Other Regions

Other regions, including Latin America, Africa, and smaller APAC markets, collectively contributed approximately 10% of the global market in 2025, driven by urbanization, rising health awareness, and small-scale government initiatives promoting active lifestyles. Adoption is slower compared with North America, Europe, Asia Pacific, and GCC due to lower per capita income and limited structured fitness programs. The remaining 2% of the market is accounted for by minor regions that represent strategic long-term opportunities as public health campaigns and retail infrastructure continue to expand.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional players focusing on product innovation, brand differentiation, and geographic expansion. Companies are increasingly investing in research and development, clean label formulations, and digital marketing capabilities to strengthen their market position. Adoption is supported by government-backed initiatives, including national physical activity programs, dietary guidelines, and public health campaigns promoting protein intake and active lifestyles. These frameworks encourage vendors to expand distribution, improve product safety, and capture long-term consumer loyalty across North America, Europe, and Asia Pacific.

Mini Profiles

Abbott Laboratories Inc. focuses on clinical and sports nutrition products, supported by global brand recognition, extensive distribution networks, and research-driven formulations, enabling broad adoption among athletes, fitness enthusiasts, and healthcare consumers worldwide.

BPI Sports operates in niche and premium segments, emphasizing innovative protein blends, performance supplements, and functional ingredients, leveraging targeted marketing, athlete endorsements, and e-commerce channels to strengthen consumer engagement and market visibility.

Cellucor / Nutrabolt leverages digital reach and strategic partnerships to expand market presence, offering high-performance pre-workout, protein, and recovery supplements, emphasizing taste, quality, and product innovation for fitness-conscious consumers.

Glanbia plc provides mass-market and premium sports nutrition solutions, supported by global manufacturing facilities, strategic acquisitions, and brand equity, delivering whey proteins, functional foods, and performance-focused supplements to athletes worldwide.

Herbalife Nutrition Ltd. operates in mass and premium segments, emphasizing weight management, protein shakes, and performance nutrition, supported by strong direct-selling networks, digital platforms, and global health and wellness campaigns.

Key Players

- Abbott Laboratories Inc.

- Amway Corp.

- Atlantic Multipower UK

- BPI Sports

- BSN (Bio-Engineered Supplements and Nutrition)

- Nutrabolt

- Clif Bar & Company

- Coca-Cola Company

- Nestlé S.A.

- PepsiCo Inc.

Recent Developments

February 2026 - Amway shall invest $12 million in India over the next few years, that shows its strong commitment to growing its presence in the nation. The company can manage costs wisely, understand how the market responds, and expand gradually, by rolling out the investment in phases. Beyond that, this is a long-term strategy to strengthen its market presence and support its network of distributors, positioning India as an important part of Amway’s global growth story.

February 2026 - The Coca-Cola Company, alongside its strategic bottling partner Coca-Cola HBC Ireland and Northern Ireland, has announced a new soft drinks partnership with the Irish Football Association and the Northern Ireland Football League. The partnership will bring supporters together to champion both national and domestic teams across Northern Ireland through activations and activities, celebrating the country’s passion for football and the spirit of sport.

November 2025 - Abbott and Exact Sciences has acquired Exact Sciences to lead in fast-growing cancer diagnostics segments, serving millions more people. This partnership shall allow Exact Sciences's shareholders to receive $105 per common share, representing a total equity value of approximately $21 billion. These businesses will increase access to life-altering diagnostics, spur innovation, and assist more people in identifying and treating cancer in its early stages.

Global Sports Nutrition Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Protein-focused nutrition products

- Hydration & endurance products

- Functional performance nutrition

- Weight & lifestyle management nutrition

Form Insight and Forecast 2026 - 2035

- Powder-based

- Liquid

- Solid

Distribution Channel Insight and Forecast 2026 - 2035

- Offline

- Online

Ingredient Source Insight and Forecast 2026 - 2035

- Animal-derived

- Plant-derived

- Blended formulations

Application Insight and Forecast 2026 - 2035

- Performance & recovery

- Hydration & endurance

- Weight & lifestyle management

End User Insight and Forecast 2026 - 2035

- Recreational fitness participants

- Lifestyle-oriented consumers

- Professional athletes

Global Sports Nutrition Market by Region

- North America

- By Product Type

- By Form

- By Distribution Channel

- By Ingredient Source

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Form

- By Distribution Channel

- By Ingredient Source

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Form

- By Distribution Channel

- By Ingredient Source

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Form

- By Distribution Channel

- By Ingredient Source

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Sports Nutrition Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Form

1.2.3. By

Distribution Channel

1.2.4. By

Ingredient Source

1.2.5. By

Application

1.2.6. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Protein-focused nutrition products

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hydration & endurance products

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Functional performance nutrition

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Weight & lifestyle management nutrition

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Form

5.2.1. Powder-based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Liquid

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Solid

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Offline

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Online

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Ingredient Source

5.4.1. Animal-derived

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Plant-derived

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Blended formulations

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Performance & recovery

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Hydration & endurance

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Weight & lifestyle management

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.6. By End User

5.6.1. Recreational fitness participants

5.6.1.1. Market Definition

5.6.1.2. Market Estimation and Forecast to 2035

5.6.2. Lifestyle-oriented consumers

5.6.2.1. Market Definition

5.6.2.2. Market Estimation and Forecast to 2035

5.6.3. Professional athletes

5.6.3.1. Market Definition

5.6.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Form

6.3. By

Distribution Channel

6.4. By

Ingredient Source

6.5. By

Application

6.6. By

End User

6.6.1.

U.S. Market Estimate and Forecast

6.6.2.

Canada Market Estimate and Forecast

6.6.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Form

7.3. By

Distribution Channel

7.4. By

Ingredient Source

7.5. By

Application

7.6. By

End User

7.6.1.

Germany Market Estimate and Forecast

7.6.2.

France Market Estimate and Forecast

7.6.3.

U.K. Market Estimate and Forecast

7.6.4.

Italy Market Estimate and Forecast

7.6.5.

Spain Market Estimate and Forecast

7.6.6.

Russia Market Estimate and Forecast

7.6.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Form

8.3. By

Distribution Channel

8.4. By

Ingredient Source

8.5. By

Application

8.6. By

End User

8.6.1.

China Market Estimate and Forecast

8.6.2.

Japan Market Estimate and Forecast

8.6.3.

India Market Estimate and Forecast

8.6.4.

South Korea Market Estimate and Forecast

8.6.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Form

9.3. By

Distribution Channel

9.4. By

Ingredient Source

9.5. By

Application

9.6. By

End User

9.6.1.

Brazil Market Estimate and Forecast

9.6.2.

Saudi Arabia Market Estimate and Forecast

9.6.3.

South Africa Market Estimate and Forecast

9.6.4.

U.A.E. Market Estimate and Forecast

9.6.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Abbott Laboratories Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amway Corp.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Atlantic Multipower UK

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

BPI Sports

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

BSN (Bio?Engineered Supplements and Nutrition)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Nutrabolt

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Clif Bar & Company

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Coca?Cola Company

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nestlé S.A.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

PepsiCo Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Sports Nutrition Market