AI in Clinical Documentation Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Component (Software, Services), by Deployment Mode (Cloud Based, On Premises), by Technology (Natural Language Processing, Generative AI and Ambient Listening, Others), by End User (Hospitals and Healthcare Providers, Ambulatory Care Centers and Telehealth Providers, Pharmaceutical and Biotechnology Companies, Payers and Insurance Companies, Others), by Region (North America, Europe, Asia Pacific, Rest of the World)

| Status : Published | Published On : May, 2026 | Report Code : VRHC1339 | Industry : Healthcare | Available Format :

|

Page : 156 |

AI in Clinical Documentation Market Overview

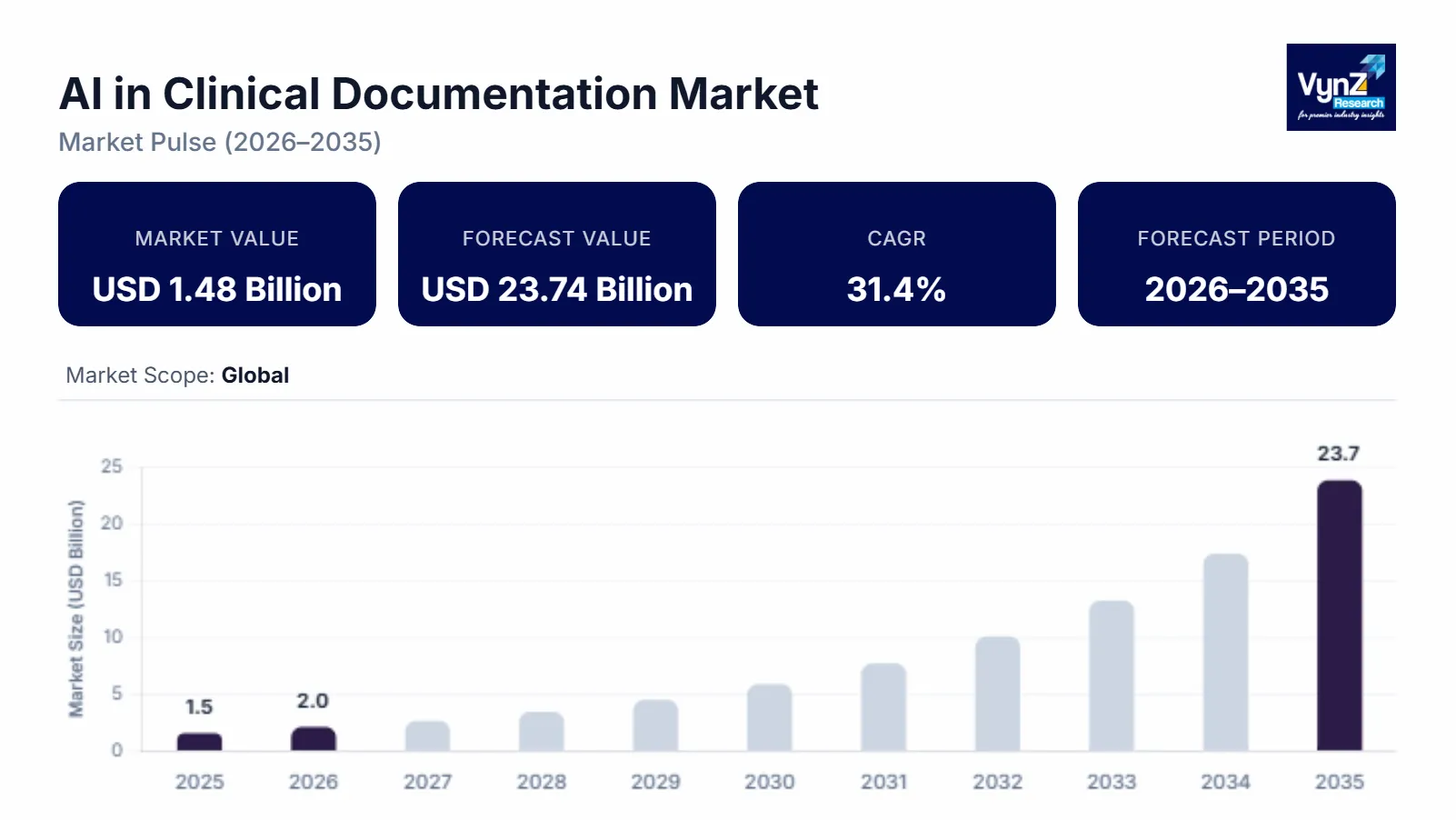

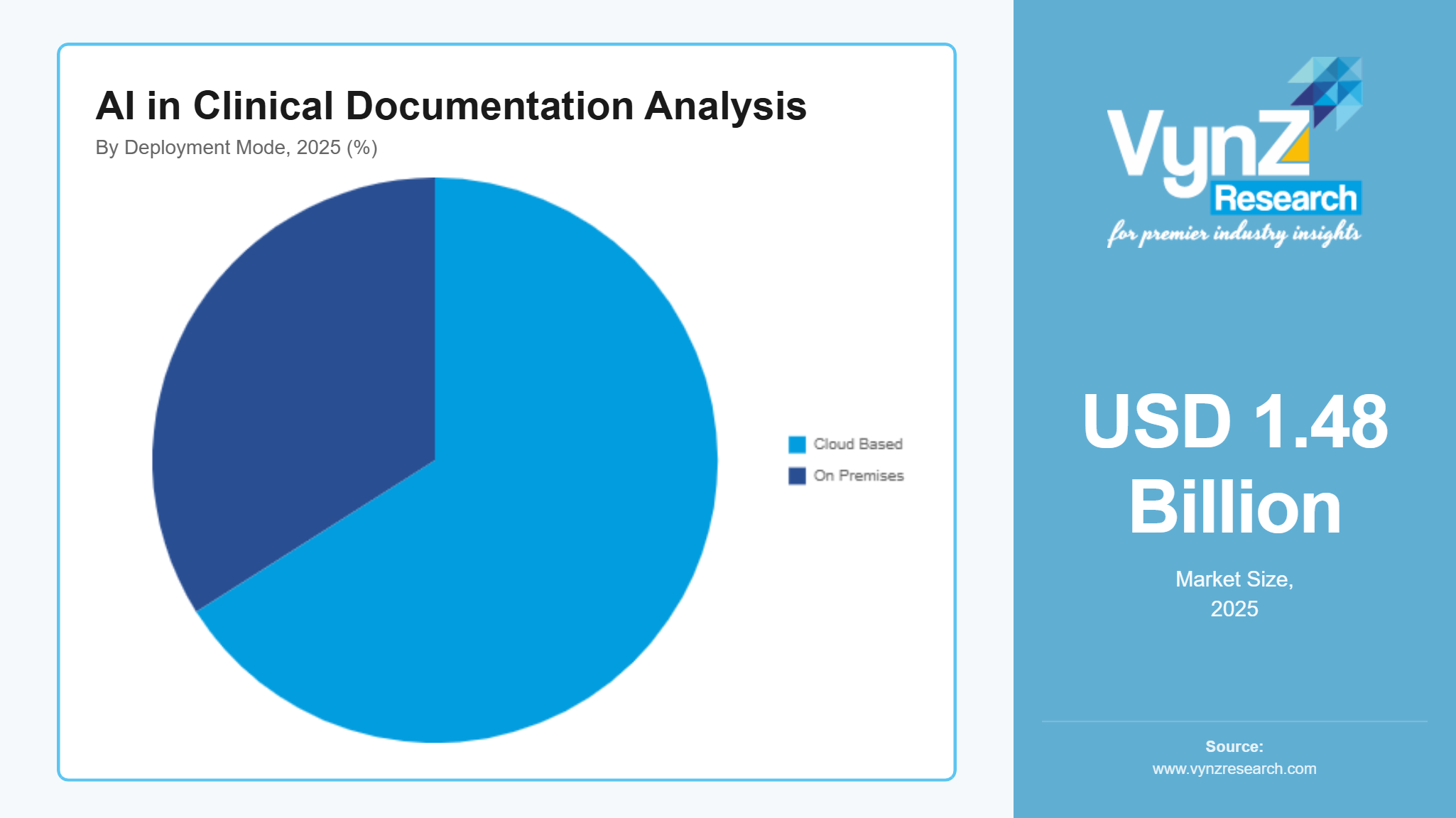

The AI in clinical documentation market which was valued at approximately USD 1.48 billion in 2025 and is estimated to rise further up to almost USD 2.03 billion in 2026, is projected to reach around USD 23.74 billion in 2035, expanding at a CAGR of about 31.4% during the forecast period from 2026 to 2035.

Market expansion is mostly due healthcare digitalization, the rising tedium of administrative work across medical facilities and also the heightened need for workflow automation. More organizations are adopting generative AI and natural language processing tools to keep things moving. There is also growing interest in automated medical transcription, better electronic health record optimization and real time clinical documentation tools. This is happening together with continued investments in healthcare IT modernization and other digital health initiatives, often backed by public health authorities. So, the market keeps broadening in North America, Europe and Asia Pacific.

AI in Clinical Documentation Market Dynamics

Market Trends

The industry is showing noticeable changes in healthcare workflow automation getting pushed forward, voice enabled documentation becoming a norm, and AI assisted transcription tech getting more traction. A big trend is the wider adoption of generative AI to improve operational efficiency, documentation accuracy, and reducing time. Lots of healthcare providers are also starting to blend AI powered documentation tools directly with electronic health record systems, trying to boost clinical productivity while also supporting patient engagement.

Cloud-based clinical documentation platforms keep expanding due to digital health transformation plans and growing interoperability needs across healthcare. Companies are leaning harder into integrated analytics, real time transcription features, and more scalable healthcare automation solutions.

Growth Drivers

The market is being driven by more healthcare data being generated and also by the rising need for automated medical documentation in hospitals, clinics, and telehealth setups. Investments in healthcare IT infrastructure, electronic health records modernization, and the broader move toward digital healthcare systems are pushing the market forward on a global scale. Public healthcare agencies plus healthcare modernization programs are adopting AI-enabled documentation technologies to support operational efficiency and smoother clinical workflows.

There is a strong push to cut physician burnout and improve documentation accuracy resulting in AI adoption. When healthcare teams prioritize efficiency, compliance and less chaotic patient record management, demand for AI powered clinical documentation solutions is likely to stay solid across the forecast window.

Market Restraints / Challenges

Even with all those growth signs, the market still has issues that can slow expansion down. Regulatory complexity and healthcare data privacy concerns are affecting how easily implementations roll out across healthcare organizations, especially in developing or cost sensitive markets. Compliance is getting harder too, because healthcare data protection standards are evolving and AI governance frameworks add extra layers.

The need for advanced AI infrastructure and skilled healthcare IT professionals creates operational strain for solution providers. Implementation costs is high, integration with legacy healthcare systems is not easy and technical expertise is limited to restrict scalability. This can also delay deployment, particularly when budgets tighten and economic uncertainty is around.

Market Opportunities

AI assisted telehealth documentation and automated clinical workflow management offers opportunities for growth fueled by more digital healthcare adoption along with more demand for faster and more reliable patient record systems. Companies that build scalable and intelligent clinical documentation platforms are in a decent position to take advantage, especially as hospitals, outpatient facilities, and telemedicine providers look for workflow optimization solutions.

Another opportunity that stands out involves multilingual AI transcription combined with predictive healthcare analytics. More investment in digital health platforms and cloud-based healthcare technologies is opening doors for long term healthcare collaborations, and it also supports specialized service expansion. Progress in natural language processing, automation, and speech recognition is expected to keep improving documentation efficiency and healthcare data management in multiple regions, which could matter a lot for long term growth.

Global AI in Clinical Documentation Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.48 Billion |

|

Revenue Forecast in 2035 |

USD 23.74 Billion |

|

Growth Rate |

31.4% |

|

Segments Covered in the Report |

Component, Deployment Mode, Technology, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Abridge AI Inc., Amazon Web Services Inc., Augmedix, DeepScribe, Google Health, IBM, Microsoft Corporation, Oracle Corporation, Suki AI, 3M Health Information Systems |

|

Customization |

Available upon request |

AI in Clinical Documentation Market Segmentation

By Component

In 2025, the software solutions was the largest with roughly 62% of total revenue. This is because more hospitals and outpatient centers are rolling out AI powered transcription platforms, speech recognition systems and clinical workflow automation tools. Government supported healthcare digitalization programs and a broader push to integrate electronic health records keep strengthening uptake in many developed healthcare markets.

For services, growth is projected to move the quickest from 2026 to 2035, with an estimated CAGR around 32.6%, due to stronger demand for implementation assistance, AI model tailoring, cloud migration, and healthcare workflow enhancement services.

By Deployment Mode

Cloud based deployment held the largest share in 2025, contributing approximately 66% of segment revenue due to lower infrastructure costs, better scalability, and more organizations adopting remote documentation setups. More healthcare organizations are using cloud integrated clinical documentation systems, mainly to gain operational flexibility and faster access to real time patient records.

On premises deployment is expected to grow steadily at an estimated CAGR of 28.9% during the forecast window. Growth is supported by ongoing worries around patient data privacy, cybersecurity, and staying compliant with healthcare data protection rules.

By Technology

Natural language processing technologies held the largest market share in 2025, about 39% of segment revenue, supported by demand for automated medical transcription, more intelligent clinical documentation, and AI assisted physician note creation systems. Meanwhile, electronic health records integration work, plus healthcare workflow automation programs are continuing to support growth in hospitals and specialty clinics.

Generative AI combined with listening technologies is forecasted to grow the fastest, with an estimated CAGR of 34.1% between 2026 and 2035. This is driven by the expanding use of real time physician documentation tools, voice enabled clinical assistants, and automated patient interaction platforms.

By End User

Hospitals and healthcare providers accounted for the largest segment in 2025, representing around 58% of total market revenue due to rising patient volumes, a heavier administrative documentation workload, and growing investments in AI enabled healthcare workflow systems. Government backed healthcare modernization initiatives, plus broader electronic health record adoption, are continuing to reinforce segment growth across major healthcare markets.

Ambulatory care centers and telehealth providers are expected to see the fastest growth over the forecast period, with an estimated CAGR of 31.8%. Growth is driven by higher demand for remote healthcare delivery, streamlined patient documentation systems and AI powered transcription platforms.

Regional Insights

North America

North America accounted for roughly 33% of the market in 2025 due to advanced healthcare IT infrastructure, higher healthcare expenditure and fast adoption of AI enabled clinical workflow systems. There is strong demand from major healthcare hubs like New York, Boston, and Toronto and government supported healthcare digitalization programs, mixed with growing investments in electronic health records modernization and telehealth infrastructure are making hospitals and healthcare networks more willing to deploy AI powered clinical documentation solutions.

Europe

Europe represented close to 24% of the market in 2025 because healthcare digital transformation initiatives keep increasing, regulatory backing supports healthcare data interoperability and more hospitals plus specialty clinics are adopting AI assisted transcription technologies. Germany, the UK, and France continue investing in healthcare automation and clinical workflow optimization platforms enabling long-term market expansion.

Asia Pacific

Asia Pacific made up around 20% of the market in 2025 and it is expected to see the fastest growth through the forecast period due to expanding healthcare infrastructure, rising healthcare IT spending and stronger adoption of cloud-based healthcare technologies across China, India, Japan, and South Korea. Government backed healthcare modernization programs, telemedicine expansion, and a bigger focus on healthcare accessibility keep opening long term doors for AI enabled clinical documentation providers.

Rest of the World

The rest of the world, including Latin America, the Middle East, and Africa, contributed about 23% of the market in 2025. Growth in these areas is due to gradual healthcare infrastructure modernization, better digital health awareness and wider adoption of AI assisted healthcare technologies in emerging economies. Government supported healthcare development initiatives along with rising investments in healthcare IT systems are also helping strengthen market opportunities in underserved healthcare sectors.

Competitive Landscape / Company Insights

The market is highly competitive with the presence of global healthcare IT providers, AI software developers and cloud technology companies focusing on product innovation, platform integration, and geographic expansion. Companies are increasingly investing in artificial intelligence research, speech recognition technologies and healthcare automation capabilities to strengthen market position. Government supported healthcare digitalization initiatives and regulatory frameworks promoting secure healthcare data management are further encouraging adoption of AI enabled clinical documentation solutions across hospitals, clinics, and telehealth platforms globally.

Mini Profiles

Abridge AI Inc. focuses on AI powered medical transcription and clinical documentation automation solutions, supported by growing healthcare partnerships, advanced speech recognition capabilities, and expanding adoption across hospital and telehealth networks.

Amazon Web Services Inc. operates in enterprise healthcare cloud and AI infrastructure segments, emphasizing scalable computing performance, secure healthcare data management, and integrated artificial intelligence capabilities for healthcare organizations.

DeepScribe leverages AI driven ambient clinical documentation technologies, physician workflow automation, and expanding digital healthcare collaborations to strengthen market presence across outpatient care and telemedicine environments.

Google Health focuses on AI enabled healthcare analytics, clinical workflow optimization, and intelligent documentation platforms, supported by strong digital ecosystem integration, cloud infrastructure strength, and continuous healthcare AI innovation.

IBM operates in healthcare AI and enterprise automation segments, emphasizing advanced analytics, hybrid cloud deployment, and intelligent clinical documentation capabilities for hospitals, healthcare providers, and research institutions.

Key Players

- Abridge AI, Inc.

- Amazon Web Services, Inc.

- Augmedix

- DeepScribe

- Google Health

- IBM

- Microsoft Corporation

- Oracle Corporation

- Suki AI, Inc.

- 3M Health Information Systems

Recent Developments

In January 2026, Suki AI Inc. expanded its ambient AI assistant capabilities through deeper electronic health record integration for clinical documentation workflows. The company strengthened automated physician note generation and voice enabled healthcare workflow support across hospital networks.

In February 2026, Oracle Corporation introduced advanced order creation capabilities within Oracle Health Clinical AI Agent to improve clinical documentation efficiency. The company expanded ambient AI functionality to reduce physician administrative workload and strengthen automated healthcare workflows.

In March 2025, Microsoft Corporation launched Dragon Copilot, an AI powered healthcare assistant designed for automated clinical documentation and workflow optimization. The platform integrated ambient listening, natural language processing, and generative AI technologies to improve physician productivity and patient interaction efficiency.

In February 2025, Augmedix expanded AI driven ambient documentation solutions across healthcare provider networks to improve medical transcription efficiency and workflow automation. The company increased focus on real time clinical note generation and AI enabled physician support capabilities.

In March 2025, 3M Health Information Systems strengthened its AI enabled clinical documentation technologies through expanded generative AI and speech recognition integration. The company focused on improving healthcare documentation accuracy and electronic health record workflow optimization across healthcare systems.

Global AI in Clinical Documentation Market Coverage

Component Insight and Forecast 2026 - 2035

- Software

- Services

Deployment Mode Insight and Forecast 2026 - 2035

- Cloud Based

- On Premises

Technology Insight and Forecast 2026 - 2035

- Natural Language Processing

- Generative AI and Ambient Listening

- Others

End User Insight and Forecast 2026 - 2035

- Hospitals and Healthcare Providers

- Ambulatory Care Centers and Telehealth Providers

- Pharmaceutical and Biotechnology Companies

- Payers and Insurance Companies

- Others

Region Insight and Forecast 2026 - 2035

- North America

- Europe

- Asia Pacific

- Rest of the World

Global AI in Clinical Documentation Market by Region

- North America

- By Component

- By Deployment Mode

- By Technology

- By End User

- By Region

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Deployment Mode

- By Technology

- By End User

- By Region

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Deployment Mode

- By Technology

- By End User

- By Region

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Deployment Mode

- By Technology

- By End User

- By Region

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AI in Clinical Documentation Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Deployment Mode

1.2.3. By

Technology

1.2.4. By

End User

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Software

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Services

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Deployment Mode

5.2.1. Cloud Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. On Premises

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Natural Language Processing

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Generative AI and Ambient Listening

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Others

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals and Healthcare Providers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Ambulatory Care Centers and Telehealth Providers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Pharmaceutical and Biotechnology Companies

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Payers and Insurance Companies

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Others

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. North America

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Europe

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Asia Pacific

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Rest of the World

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Deployment Mode

6.3. By

Technology

6.4. By

End User

6.5. By

Region

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Deployment Mode

7.3. By

Technology

7.4. By

End User

7.5. By

Region

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Deployment Mode

8.3. By

Technology

8.4. By

End User

8.5. By

Region

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Deployment Mode

9.3. By

Technology

9.4. By

End User

9.5. By

Region

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Abridge AI, Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services, Inc.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Augmedix

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

DeepScribe

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Google Health

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

IBM

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Microsoft Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Oracle Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Suki AI, Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

3M Health Information Systems

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AI in Clinical Documentation Market