Asia Pacific Dental Implants Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Dental Crowns, Dentures, Dental Bridges, Abutments, Other), by Material (Titanium Implants, Zirconium Implants), by Facility Type (Hospitals and Clinics, Dental Laboratories, Other Segments), by Design (Fixed, Removable), by Region (China, India, Japan, Australia, Rest of Asia Pacific)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1332 | Industry : Healthcare | Available Format :

|

Page : 134 |

Asia Pacific Dental Implants Market Overview

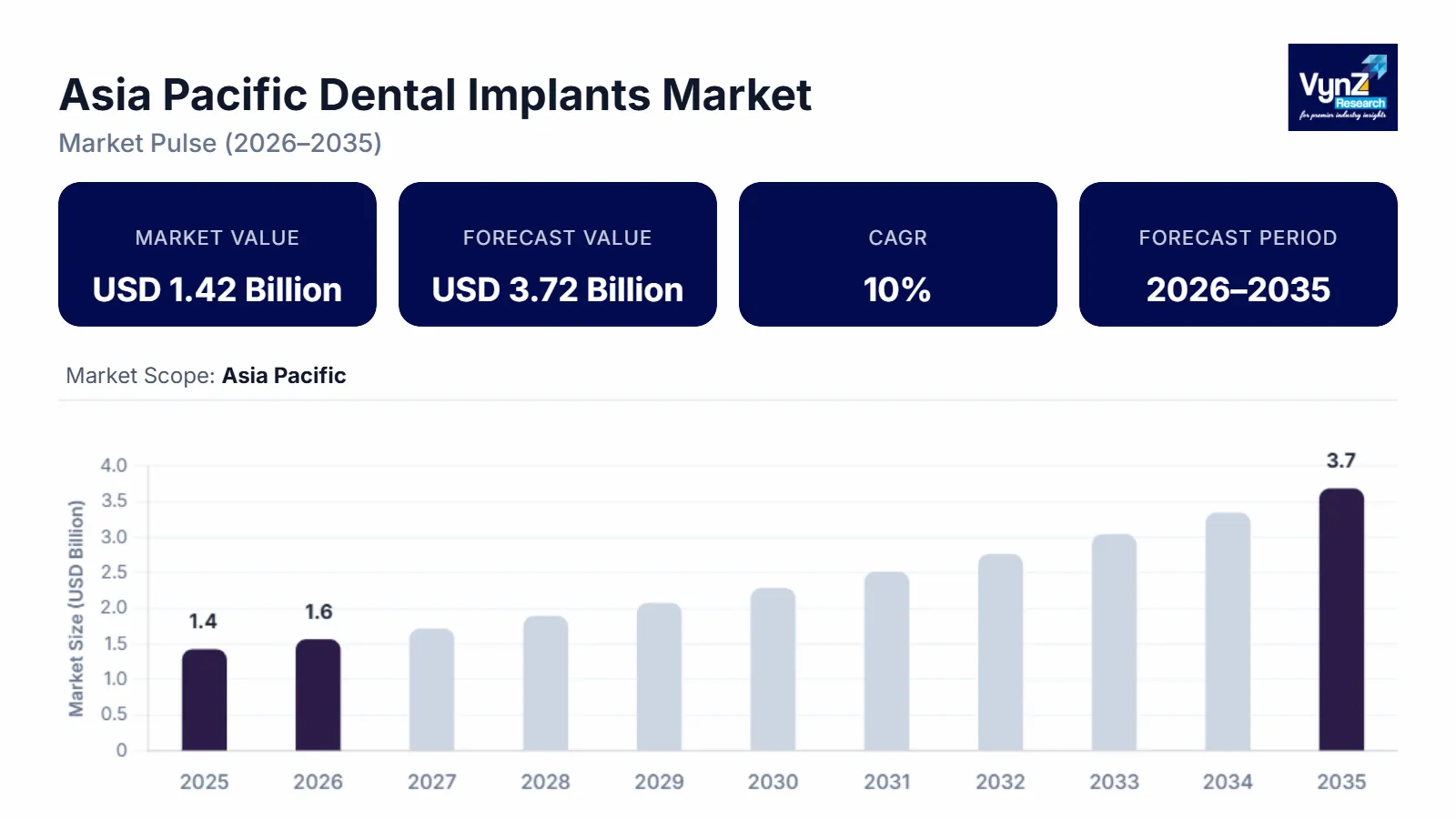

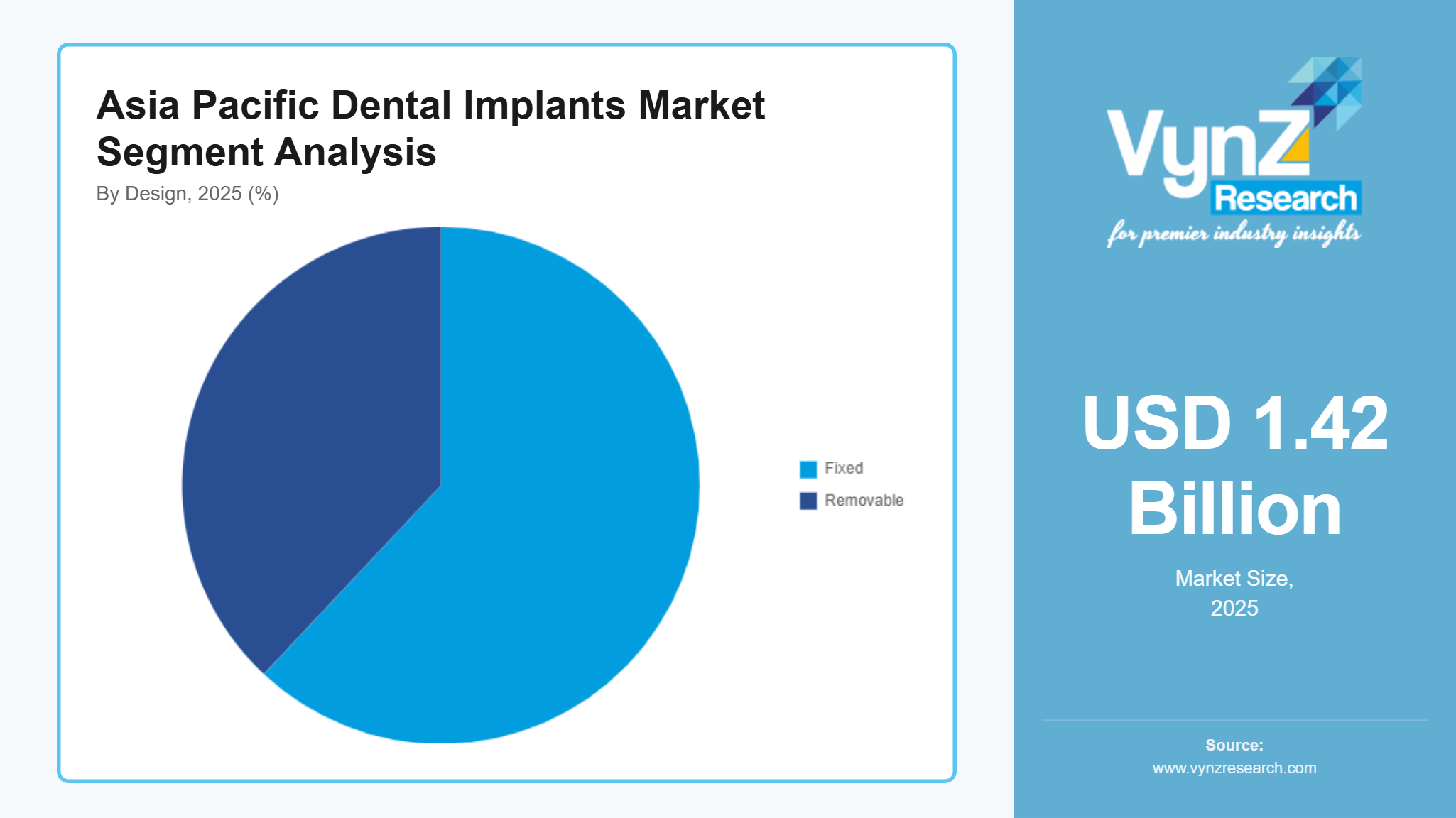

The Asia Pacific dental implants market which was valued at approximately USD 1.42 billion in 2025 and is estimated to rise further up to almost USD 1.58 billion in 2026, is projected to reach around USD 3.72 billion in 2035, expanding at a CAGR of about 10% during the forecast period from 2026 to 2035.

Market growth happens because the geriatric population increases and people prefer advanced restorative procedures. Also, digital implantology and minimally invasive techniques gain more usage and edentulism and periodontal disorders become common. Urban residents show growing interest in aesthetic dentistry and functional oral rehabilitation, which together with public healthcare investments lead to market growth in China, India and Japan.

The World Health Organization states that dental diseases impact most people in Asia Pacific because untreated dental caries and severe periodontal conditions cause tooth loss and permanent functional impairment. Regional public health organizations and health ministries have started to include oral health within their non communicable disease control programs, which has produced better public understanding and better disease detection. Government supported programs which promote preventive dental treatment, expand dental education and strengthen primary healthcare systems are improving public access to restorative dental services. The rising healthcare expenses and existing reimbursement models in particular countries are driving more hospitals to use implant procedures, which results in ongoing market growth throughout the region.

Asia Pacific Dental Implants Market Dynamics

Market Trends

The present-day market undergoes a fundamental change because the industry now uses digital systems to perform exact implant operations which medical professionals and patients throughout the area require. The market currently experiences its most significant transformation because medical professionals now prefer using CAD CAM systems for implant design and guided surgical procedures which deliver improved surgical accuracy and shorter chair time and better aesthetic results. The market today witnesses an emerging trend which sees 3D printing systems and digital imaging systems becoming one complete solution because technology evolves at a rapid pace and digital healthcare systems become more widely utilized. The World Health Organization reports that Asia Pacific oral health systems now focus on early diagnosis and methods which use minimal treatment to prevent dental issues while their clinics establish standard dental implant procedures which use advanced technology, these changes will transform how dental practices compete within the industry.

Growth Drivers

The market grows because rising oral disease and tooth loss problems create ongoing demand from both older people and city residents. The market now experiences rapid growth because emerging economies dedicate more funds for healthcare facilities and dental education programs. People now understand the importance of oral aesthetics and functional rehabilitation which drives higher product adoption among dental customers. The advanced implant systems market will maintain strong demand throughout the forecast period because patients now choose products that offer durable material performance and visually appealing results. The National Oral Health Program in India and public dental care expansion strategies in Japan and China help improve preventive and restorative care access, which creates sustained demand for dental services throughout the region.

Market Restraints / Challenges

The market needs to overcome multiple challenges which will restrict its future development. The middle-income and rural population struggles to access dental services because high procedural costs and limited insurance coverage make dental procedures too expensive. Manufacturers and healthcare providers face difficulties which arise from their need to use imported implant materials and advanced surgical equipment. Public health authorities report that developing regions experience treatment delays and scalability problems between World Health Organization assessment areas because their healthcare infrastructure lacks basic medical services and skilled dental professionals.

Market Opportunities

The market offers great potential to widen access for patients who need affordable digital implant solutions because the middle class increases in emerging economies which also experience higher health awareness. Businesses that provide budget-friendly dental implant systems with customization options will attract patients who seek affordable solutions and international dental tourism customers. The market now provides another major growth opportunity through its implementation of advanced digital systems and AI treatment planning, which hospitals now use to deliver better patient results with better efficiency. Government healthcare expansion programs and World Health Organization oral health awareness initiatives will make healthcare services more accessible while they build essential clinical infrastructure to foster market growth throughout the region.

Asia Pacific Dental Implants Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.42 Billion |

|

Revenue Forecast in 2035 |

USD 3.72 Billion |

|

Growth Rate |

10% |

|

Segments Covered in the Report |

By Type, By Facility, By Design, By Material |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, Australia, Rest of Asia Pacific |

|

Key Companies |

Anthogyr SAS, Bicon LLC, BioHorizons IPH Inc., DENTIS, DENTIUM Co. Ltd., DENTSPLY Sirona, Institut Straumann AG, KYOCERA Medical Corp., Leader Italy, Nobel Biocare Services AG, OSSTEM IMPLANT, T-Plus Implant Tech. Co., Zimmer Biomet Holdings Inc |

|

Customization |

Available upon request |

Asia Pacific Dental Implants Market Segmentation

By Type

The market in 2025 saw dental crowns as its largest revenue source which generated roughly 34% of total market earnings. The treatment method dominates dental practices because dentists perform it frequently while patients need both restorative and cosmetic procedures and dental clinics in cities are starting to use it more often. The World Health Organization reports that untreated dental caries have become a greater public health problem which increases the demand for crown restorations throughout the entire region. The segment expansion is supported by people in China and India learning about permanent oral rehabilitation and dental coverage programs expanding their dental insurance services.

The dental bridge market will experience continuous growth which will reach a CAGR of 9.1% between 2026 and 2035. The growth happens because middle income people find the treatment affordable and it works for them to replace multiple missing teeth. The market share of dentures remains high because older people can afford them and they will grow at a rate of 8.4% from current levels. The market for abutments and their components will grow fastest at about 10.2% because dental centers use advanced restorative methods which depend on precise implant connection systems.

By Material

Titanium implants made up the largest market share in 2025 when they generated approximately 57% of total revenue for that market. The product continues to lead the market because it offers better biocompatibility and long-lasting performance and it enables successful bone integration for all patient groups. The regulatory system requires organizations to meet safety and quality standards which helps hospitals to adopt the technology more widely. The rising number of dental training facilities and infrastructure development in Asia Pacific has increased the use of titanium-based systems.

Zirconium implants will experience the highest market growth because their CAGR will reach 10.5% between 2026 and 2035. Growth returns from people in urban areas with high income levels who want metal-free products that look better than standard options. Patients choose to undergo treatments which use the least invasive methods and focus on their needs according to the current trend. The segment development in advanced and developing markets will continue because dental services now offer premium options and ceramic material technology has improved.

By Design

The market for fixed implant solutions reached its highest revenue level in 2025 because it generated about 62% of total segment earnings. The treatment option becomes popular among doctors and patients because it provides long-lasting results which lead to higher satisfaction rates. The World Health Organization recommends that Asian governments establish oral health programs which should focus on creating effective treatments to improve fixed implant system usage. The increase in disposable income enables people to access better dental treatment services which leads to ongoing dental treatment needs.

According to estimates removably implantable solutions will become the fastest growing market segment which will achieve a 9.6% CAGR between 2026 and 2035. The elderly patients with complex dental issues can understand the treatment because it costs less and requires simple maintenance. The growing elderly population requires low-cost treatment options to drive everything in this segment. The market acceptance by patients has increased because healthcare design systems now offer better design choices and treatment systems provide better user experience.

By Facility

The 2025 market sector included hospitals and clinics as its biggest section because they generated about 68% of total market earnings. The market sector maintains its position because patient numbers increase and dental professionals become available and facilities introduce cutting-edge diagnostic and surgical systems. The World Health Organization approved oral health programs which work with primary and secondary healthcare improvement projects to strengthen dental implant procedure availability.

The dental laboratory market will grow at a 9.3% CAGR between 2026 and 2035 because more people want custom-made prosthetics while digital manufacturing methods like CAD CAM systems gain popularity. The growth of the market occurs because clinics and specific laboratories work together to deliver high-precision restorative treatments. Other facilities which include academic institutions and research centers help the market achieve higher growth rates and better training methods throughout the whole region.

Regional Insights

China

The market in 2025 showed China as the major market with its 29% share, which increased because of urban development, a growing middle class and more people wanted cosmetic and dental restoration treatments. The major cities of Beijing, Shanghai and Shenzhen provide many dental treatments through their private clinics and specialty clinics. The World Health Organization reports that many people still have dental problems which remain untreated, so they should get long-lasting dental restorations. The regional market performance gets stronger from government programs which modernize healthcare and increase dental care access in public healthcare systems.

India

The Indian market share for 2025 will reach about 18% because people now understand oral health better and dental tourism continues to grow and patients can access advanced dental treatments more easily. Major implant procedure centers in India have established themselves in Mumbai, Delhi and Bengaluru. The National Oral Health Program receives government support to create preventive dental care and build dental treatment facilities according to World Health Organization guidelines. The market expands through dental treatment options at low costs and the rising number of organized dental care providers who serve urban and semi-urban areas.

Japan

The Japanese market will reach 16% in 2025 because of its aging demographic and people needing precise dental restoration services. The progress of Tokyo and Osaka to become the top cities for clinical adoption shows their advanced healthcare infrastructure and their skilled healthcare workers. The government healthcare system establishes standards for treatment procedures which help build trust between doctors and patients. WHO aligned public health knowledge demonstrates that elderly people require oral care, which creates demand for long-lasting dental implant solutions.

Australia

The Australian market reached 9% in 2025 because people spent more on healthcare and their insurance plans provided complete coverage and they became more informed about dental health practices. The central areas of Sydney and Melbourne serve as the main locations for dental procedures and dental specialized clinics. The government dental policies together with global WHO recommendations create a framework which helps people receive dental exams and dental treatment right away. Digital dentistry technology adoption leads to better clinical results and matches regional growth.

Rest of Asia Pacific

The market in 2025 showed that the Rest of Asia Pacific region which includes South Korea, Thailand, Indonesia and Malaysia held an 8% market share. The region develops through better healthcare systems, increased medical tourism and growing awareness about dental aesthetic needs. The government programs which expand healthcare access and develop oral health programs according to World Health Organization standards help hospitals adopt dental implant procedures. The market distribution across the region remains balanced because other smaller economies in the area which were not specifically mentioned take up the remaining market share.

Competitive Landscape / Company Insights

The market is moderately competitive, because established global manufacturers and emerging regional players spend their resources on product development and cost reduction and market expansion activities. Companies are investing more money into research and development, digital dentistry solutions and precision manufacturing which will help them improve their market position. The World Health Organization and regional health authorities have established regulatory frameworks and quality standards which encourage organizations to follow rules while developing new solutions. The dental clinics and laboratories which dental companies work with, help their business operations by improving their market presence and brand recognition.

Mini Profiles

Anthogyr SAS focuses on precision dental implant systems and prosthetic solutions, supported by strong clinical expertise, established distribution networks, and integration within a globally recognized implantology ecosystem.

Bicon LLC operates in niche segments, emphasizing short implant design, simplified surgical protocols, and long-term clinical stability, catering to specialized practitioners seeking minimally invasive and cost-efficient solutions.

DENTSPLY Sirona operates in premium segments, emphasizing advanced digital dentistry solutions, integrated workflows, and high-performance implant systems, supported by strong brand recognition and global distribution capabilities.

Institut Straumann AG leverages strategic partnerships, innovation in biomaterials, and digital dentistry platforms to expand market presence, supported by extensive research capabilities and strong penetration across developed and emerging markets.

Zimmer Biomet Holdings Inc. focuses on comprehensive implant solutions and surgical technologies, supported by broad product portfolios, global distribution strength, and continuous investment in research driven orthopedic and dental innovations.

Key Players

- Anthogyr SAS

- Bicon LLC

- BioHorizons IPH Inc.

- DENTIS

- DENTIUM Co. Ltd.

- DENTSPLY Sirona

- Institut Straumann AG

- KYOCERA Medical Corp.

- Leader Italy

- Nobel Biocare Services AG

- OSSTEM IMPLANT

- T-Plus Implant Tech. Co.

- Zimmer Biomet Holdings Inc

Recent Developments

In October 2025, Institut Straumann AG reported an 8.3% increase in quarterly sales, driven by strong performance across Asia Pacific and North America, reflecting sustained demand for implant solutions. In February 2026, the company projected continued high single digit growth, supported by strategic flexibility amid procurement changes in China and expansion of digital service platforms.

In January 2025, DENTSPLY Sirona strengthened its market position through continued investments in digital dentistry platforms and integrated treatment workflows, enhancing clinical efficiency and product adoption. In 2026, the company expanded its focus on innovation driven implant solutions, aligning with growing demand for precision guided procedures and advanced restorative technologies.

In 2025, Zimmer Biomet continued to expand its dental implant portfolio with a focus on diversified implant designs tailored to varying bone structures and clinical needs. In 2026, the company emphasized precision driven solutions and surgical innovation, supporting improved treatment outcomes and broader adoption across specialized dental practices.

In 2025, OSSTEM IMPLANT strengthened its global footprint through strategic expansion initiatives and increased focus on cost competitive implant systems targeting emerging markets. In 2026, the company continued to enhance product accessibility and technological capabilities, supporting wider adoption across Asia Pacific and price sensitive regions.

In August 2025, Nobel Biocare Services AG advanced its product development strategies, focusing on premium implant solutions and digital integration to improve procedural accuracy and patient outcomes. In 2026, the company continued to expand its global distribution and clinical training programs, reinforcing its position in high value implant segments.

Asia Pacific Dental Implants Market Coverage

Type Insight and Forecast 2026 - 2035

- Dental Crowns

- Dentures

- Dental Bridges

- Abutments

- Other

Material Insight and Forecast 2026 - 2035

- Titanium Implants

- Zirconium Implants

Facility Type Insight and Forecast 2026 - 2035

- Hospitals and Clinics

- Dental Laboratories

- Other Segments

Design Insight and Forecast 2026 - 2035

- Fixed

- Removable

Region Insight and Forecast 2026 - 2035

- China

- India

- Japan

- Australia

- Rest of Asia Pacific

Asia Pacific Dental Implants Market by Region

- China

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- Japan

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- India

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- South Korea

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- Vietnam

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- Thailand

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- Malaysia

- By Type

- By Material

- By Facility Type

- By Design

- By Region

- Rest of Asia-Pacific

- By Type

- By Material

- By Facility Type

- By Design

- By Region

Table of Contents for Asia Pacific Dental Implants Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Material

1.2.3. By

Facility Type

1.2.4. By

Design

1.2.5. By

Region

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia Market Estimate and Forecast

4.1. Asia Market Overview

4.2. Asia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Dental Crowns

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Dentures

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Dental Bridges

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Abutments

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Other

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Material

5.2.1. Titanium Implants

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Zirconium Implants

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Facility Type

5.3.1. Hospitals and Clinics

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Dental Laboratories

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Other Segments

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By Design

5.4.1. Fixed

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Removable

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By Region

5.5.1. China

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. India

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Japan

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Australia

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Rest of Asia Pacific

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Type

6.2. By

Material

6.3. By

Facility Type

6.4. By

Design

6.5. By

Region

7. Japan Market Estimate and Forecast

7.1. By

Type

7.2. By

Material

7.3. By

Facility Type

7.4. By

Design

7.5. By

Region

8. India Market Estimate and Forecast

8.1. By

Type

8.2. By

Material

8.3. By

Facility Type

8.4. By

Design

8.5. By

Region

9. South Korea Market Estimate and Forecast

9.1. By

Type

9.2. By

Material

9.3. By

Facility Type

9.4. By

Design

9.5. By

Region

10. Vietnam Market Estimate and Forecast

10.1. By

Type

10.2. By

Material

10.3. By

Facility Type

10.4. By

Design

10.5. By

Region

11. Thailand Market Estimate and Forecast

11.1. By

Type

11.2. By

Material

11.3. By

Facility Type

11.4. By

Design

11.5. By

Region

12. Malaysia Market Estimate and Forecast

12.1. By

Type

12.2. By

Material

12.3. By

Facility Type

12.4. By

Design

12.5. By

Region

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Type

13.2. By

Material

13.3. By

Facility Type

13.4. By

Design

13.5. By

Region

14. Company Profiles

14.1.

Anthogyr SAS

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Bicon LLC

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

BioHorizons IPH Inc.

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

DENTIS

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

DENTIUM Co. Ltd.

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

DENTSPLY Sirona

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Institut Straumann AG

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

KYOCERA Medical Corp.

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Leader Italy

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Nobel Biocare Services AG

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

14.11.

OSSTEM IMPLANT

14.11.1.

Snapshot

14.11.2.

Overview

14.11.3.

Offerings

14.11.4.

Financial

Insight

14.11.5.

Recent

Developments

14.12.

T-Plus Implant Tech. Co.

14.12.1.

Snapshot

14.12.2.

Overview

14.12.3.

Offerings

14.12.4.

Financial

Insight

14.12.5.

Recent

Developments

14.13.

Zimmer Biomet Holdings Inc

14.13.1.

Snapshot

14.13.2.

Overview

14.13.3.

Offerings

14.13.4.

Financial

Insight

14.13.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia Pacific Dental Implants Market