India Telemedicine Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Type (Hardware, Software, Telemedicine Consultation Services), by Modality (Real-Time Telemedicine, Remote Patient Monitoring, Store-and-Forward Practice, Consultation Between Specialists and Primary Caregivers, Medical Imaging, Telemedicine Networks), by Application (Teleradiology, Telepathology, Telecardiology, Telepsychiatry, Teledermatology), by End-User (Healthcare Facilities, Homecare)

| Status : Published | Published On : Jun, 2026 | Report Code : VRHC1341 | Industry : Healthcare | Available Format :

|

Page : 125 |

India Telemedicine Market Overview

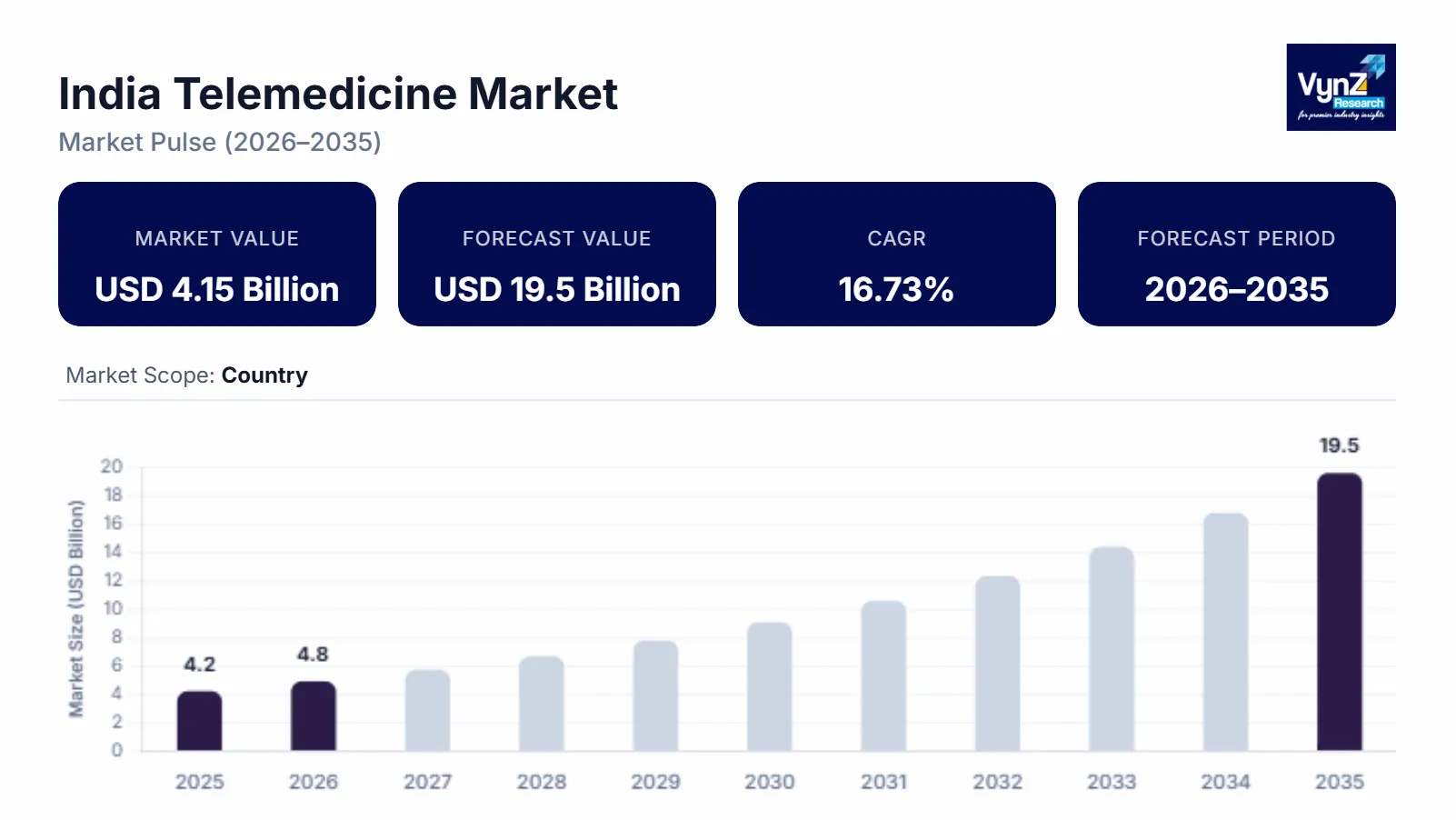

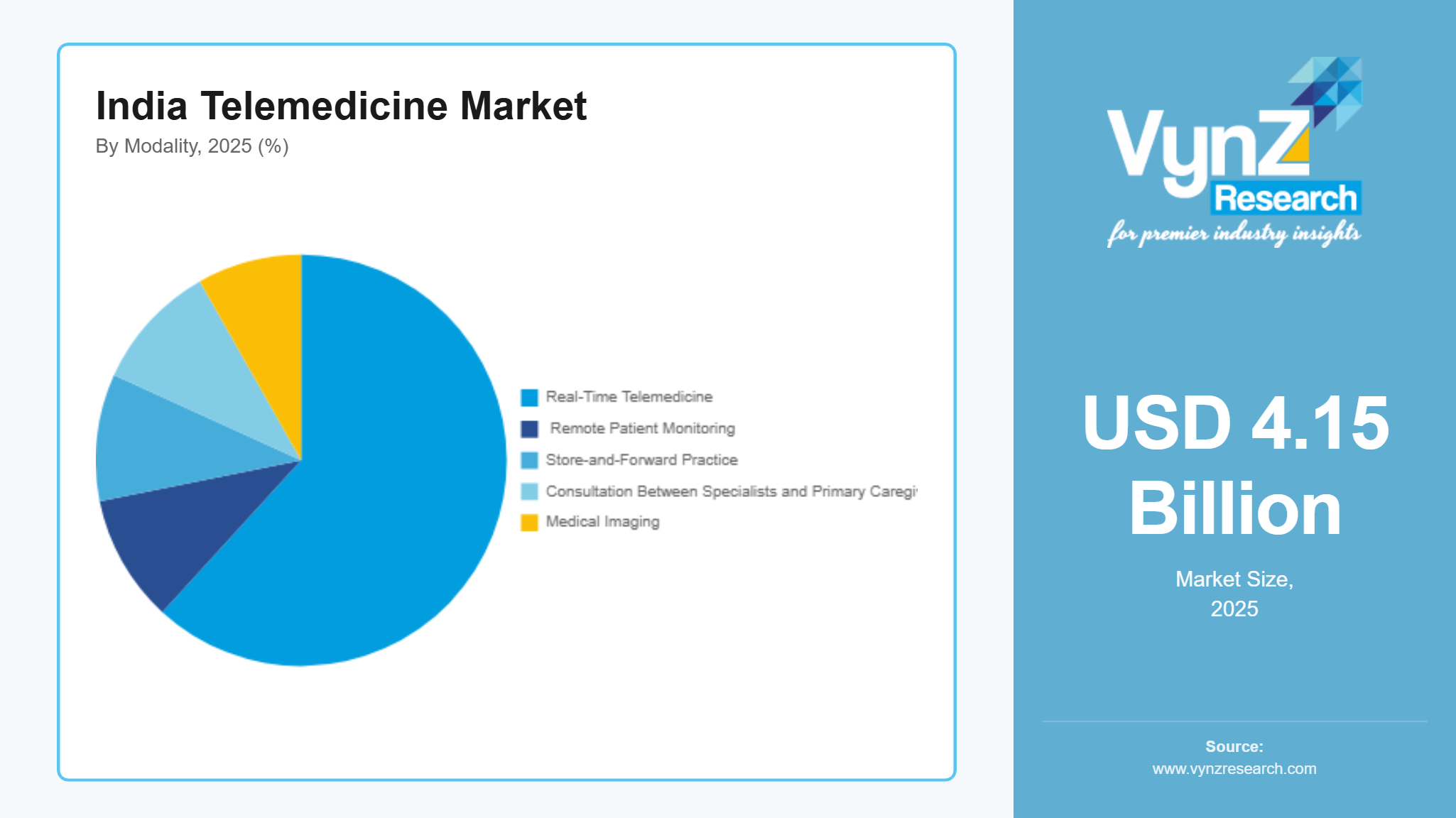

The India telemedicine market size was estimated at about USD 4.15 billion in 2025 and is expected to reach around USD 4.84 billion in 2026, rising to roughly USD 19.5 billion by 2035, growing at approximately 16.73% CAGR from 2026 to 2035.

Research Highlights

- Services held 58.4% market share in 2025, driven by rising virtual consultations.

- Real time telemedicine captured 61.8% share in 2025 due to convenience.

- Teleconsultation accounted for 42.7% share in 2025, supported by healthcare accessibility.

- Healthcare providers represented 48.9% share in 2025 through digital care integration.

- Maharashtra held 24.8% market share in 2025, supported by advanced healthcare infrastructure.

Wider internet reach and smartphone penetration promotes market expansion, facilitated further by growing need for accessible healthcare services in underserved areas, constant monitoring requirement for the growing number of chronic diseases for long term, and higher acceptance of AI-based teleconsultation and remote patient management platforms. Higher preference over remote digital consultations over one-to-one doctor-patient chats pushes market growth fueled further by steady development of digital healthcare infrastructure. Growing investments in Maharashtra, Karnataka and Delhi NCR, the Ayushman Bharat Digital Mission and the National Digital Health Mission are promoting digital health records and interoperability and eSanjeevani platforms of the government supports over 380 million teleconsultations resulting in its wider acceptance.

India Telemedicine Market Dynamics

Market Trends

The market is witnessing changes in patient preference for digital healthcare delivery and engagement due to greater accessibility. Use of AI in maintaining electronic health records, functional telemedicine platforms, and increased preference for personalized care are also notable moves that are promoting clinical efficiency. Faster and wider acceptance of interoperable digital health ecosystems is also being pushed by the Ayushman Bharat Digital Mission said the National Health Authority. Patients now seem to prefer remote monitoring and they use mobile health applications more than before mainly because internet penetration is higher and connectivity is better.

Growth Drivers

The growth of the market is facilitated by the development in healthcare infrastructure, greater availability of internet in urban and rural regions.

- The Ministry of Electronics and Information Technology reports that virtual healthcare services are becoming more accessible due to broadband expansion and higher digital transformation initiatives.

- The National Health Authority also reports long-term market growth is supported by electronic health records, digital IDs, and connected healthcare platforms, further strengthened by the Ayushman Bharat Digital Mission.

Also, growing chronic diseases, preference for convenience, cost control and continuity of care promotes the need for remote monitoring and teleconsultations. The World Health Organization underlines that digital health technologies support daily monitoring and management of chronic health conditions and offers higher accessibility.

Market Restraints / Challenges

Despite significant growth potential, the market faces challenges due to ununiform digital infrastructural development, uneven internet connectivity in underserved and remote areas. The Telecom Regulatory Authority of India says that poor network quality and weaker broadband reach prevent higher adoption of telemedicine. Data privacy, cybersecurity, and patient information security are other issues that create operational hurdles for technology platforms adding pressure on them to ensure trained staff and secure digital systems are in place. all these increase operational and compliance costs and adds implementation complexities.

Market Opportunities

Significant opportunities for growth are offered by the market in rural healthcare and digital inclusion programs mainly due to growing demand and smartphone adoption.

- The National Health Authority says that progress due to the Ayushman Bharat Digital Mission in digital healthcare infrastructure allows telemedicine providers to reach underserved communities.

- Government programs that promote literacy in digital healthcare and greater healthcare accessibility will create more demand for inexpensive solutions through virtual healthcare in tier II and tier III cities.

Opportunities are also offered due to development in telehealth services, dedicated virtual care, higher investment in digital healthcare, preference to provide value-added services, development in AI and remote diagnostics that promote long term patient engagement.

India Telemedicine Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.15 Billion |

|

Revenue Forecast in 2035 |

USD 19.5 Billion |

|

Growth Rate |

16.73% |

|

Segments Covered in the Report |

By Type, By Modality, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Maharashtra, Karnataka, Delhi NCR, Tamil Nadu, Rest of India |

|

Key Companies |

1mg, CVS Health, Lybrate, Inc., Meta16labs Healthcare & Analytics Pvt. Ltd., Netmeds Marketplace Ltd., NovaCura Tech Health Services, Practo, Rijuven (India), TeleVital, Zoylo Digihealth Pvt. Ltd. |

|

Customization |

Available upon request |

India Telemedicine Market Segmentation

By Type

Services contributed about 58.4% in 2025 supported by the growth of virtual consultations, better telemonitoring routines, and improved digital health delivery approaches. As per the Ministry of Health and Family Welfare, the continual expansion of the eSanjeevani platform has promoted teleconsultation preference and increased demand for telemedicine services in villages and towns.

Software is expected to grow fast at almost 18.6% during the forecast period because more people are using health records and tools that use artificial intelligence to help with diagnoses and platforms to manage healthcare. The Ayushman Bharat Digital Mission is also helping to create health infrastructure which is making software more important. The National Health Authority says this mission is encouraging people to use software.

By Modality

Real time telemedicine represented nearly 61.8% of the market share in 2025 backed by greater adoption of video consultations, patient preference for easy and time-saving solutions, and better accessibility.

Remote patient monitoring will grow faster with an estimated CAGR of about 18.1% CAGR throughout the forecast period due to higher occurrences of chronic illnesses, greater need for continuous monitoring and increasing aging demographics. The World Health Organization reports that such growing needs will improve healthcare delivery, accessibility and long-term disease management.

By Application

Teleconsultation held the largest market share in 2025 with nearly 42.7% mostly because there is more demand for remote healthcare access, shorter waiting time, and convenience. The Ministry of Health and Family Welfare says that scaling teleconsultation services via eSanjeevani gives comfort to both patients and healthcare providers.

Telecardiology is projected to expand the fastest at a CAGR of roughly 18.4% across the forecast period. This pace is supported by wider acceptance and a rising number of heart patients. The Indian Council of Medical Research stresses the growing number of cardiovascular problems that creates stronger demand for advanced virtual cardiac care solutions.

By End User

Healthcare providers accounted for the largest revenue share of about 48.9% in 2025 because hospitals, specialty centers and clinics integrate telemedicine into daily workflows for greater operational efficiency and patient reach through virtual care frameworks and interoperable healthcare systems, according to the National Health Authority.

Patients segment will register quickest growth rate of about 18.3% through 2035 due to greater smartphone penetration, increased preference for convenient consultations and growing awareness of digital healthcare services. The Ministry of Electronics and Information Technology reports that greater internet availability and digital adoption support patient participation in virtual healthcare ecosystems.

Regional Insights

Maharashtra

Maharashtra represented about 24% of the market in 2025 mainly due to better healthcare systems, growing acceptance, and higher demand from healthcare providers in Mumbai, Pune, and Nagpur, with Maharashtra being the frontrunner, according to the Ministry of Health and Family Welfare due to greater use and deployment. More investment in telemedicine, growing need for accessible and convenient chronic illness management, and implementation of digital health records under Ayushman Bharat Digital Mission run by the National Health Authority is also helping the region perform better.

Karnataka

Karnataka contributed about 18% market share in 2025 due to a strong technology infrastructure, greater healthcare innovation, and favorable policy frameworks. More hospitals, health startups and specialty are increasingly adopting telemedicine keeping the demand consistent. Bengaluru is a major hub for healthcare technology and telehealth platforms. The Ministry of Electronics and Information Technology says that Bengaluru is growing due to better internet, higher spending in technology and more people using remote consultations.

Delhi NCR

Delhi NCR accounted for about 15% of the market share in 2025 due to growing healthcare spends, awareness, virtual services, and acceptance. Long-term growth is further promoted by the large number of hospitals and healthcare establishments. As stated by the National Health Authority and the Ministry of Health and Family Welfare, broader adoption of teleconsultation, a growing liking toward specialist consultations and easier access to digital healthcare services all help push the market forward.

Tamil Nadu

Tamil Nadu contributed around 14% of the market share in 2025 supported by strong healthcare infrastructure, higher adoption of digital health, and presence of a large number of healthcare centers in Chennai, Coimbatore and Madurai. The Ministry of Health and Family Welfare states that increased involvement of the state to better digital healthcare and teleconsultation services is expediting adoption, investment in healthcare digitization, upgraded internet connectivity, and a preference for professional consultations.

Rest of India

The rest of India collectively contributed about 29% of the market which includes that from Andhra Pradesh, Rajasthan, Gujarat, Telangana, Kerala, Uttar Pradesh and West Bengal due to greater smartphone penetration, continual development of digital health infrastructure and better access. The National Health Authority says that Ayushman Bharat Digital Mission, eSanjeevani telemedicine platform and other programs are increasing acceptance of virtual healthcare in urban and rural areas thereby helping in stronger long-term growth potential.

Competitive Landscape / Company Insights

The market is moderately competitive with hospitals, telehealth platforms and established health care technology providers and startups pushing service innovation and platform development to increase reach. Large number of companies are investing in AI and remote patient monitoring solutions for business growth. The National Health Authority and the Ministry of Health and Family Welfare says that constant rollout of the Ayushman Bharat Digital Mission develops digital health infrastructure, promotes new ideas and increases competitive pressure in the telemedicine ecosystem.

Mini Profiles

1mg focuses on online pharmacy services, teleconsultation, and diagnostic solutions, supported by strong digital reach, extensive healthcare partnerships, and a growing customer base across urban and semi urban markets.

CVS Health operates in integrated healthcare and telehealth services, emphasizing patient engagement, healthcare accessibility, and technology enabled care delivery through its established healthcare ecosystem and service network.

Lybrate Inc. leverages digital healthcare platforms and physician networks to expand market presence, offering teleconsultation, health information services, and virtual care solutions across multiple medical specialties.

Practo focuses on telemedicine, appointment scheduling, and healthcare management solutions, supported by strong brand recognition, a broad provider network, and continuous investments in digital healthcare innovation.

Zoylo Digihealth Pvt. Ltd. specializes in digital healthcare services, teleconsultation, and healthcare aggregation platforms, supported by technology driven solutions, strategic healthcare partnerships, and expanding service accessibility.

Key Players

- 1mg

- CVS Health

- Lybrate, Inc.

- Meta16labs Healthcare & Analytics Pvt. Ltd.

- Netmeds

- Marketplace Ltd.

- NovaCura

- Tech Health Services

- Practo

- Rijuven (India)

- TeleVital

- Zoylo Digihealth Pvt. Ltd.

Recent Developments

In January 2026, Netmeds Marketplace Ltd. continued expanding its digital healthcare ecosystem by strengthening online pharmacy and teleconsultation offerings across multiple Indian cities. The development supported growing demand for integrated virtual healthcare and medicine delivery services.

In March 2026, Meta16labs Healthcare & Analytics Pvt. Ltd. enhanced its healthcare analytics capabilities to support data driven clinical decision making and digital health management. The initiative reflected increasing adoption of artificial intelligence and analytics within the telemedicine landscape.

In April 2026, TeleVital expanded its virtual care service portfolio with a greater focus on remote patient monitoring and digital consultations. The move aimed to improve healthcare accessibility and patient engagement across underserved locations.

In May 2026, Rijuven (India) increased investments in technology enabled healthcare solutions to strengthen its telehealth service capabilities. The expansion supported rising demand for convenient and cost effective digital healthcare services.

In June 2026, NovaCura Tech Health Services focused on enhancing its telemedicine platform through improved digital integration and patient management features. The initiative was intended to improve service efficiency and support long term growth in virtual healthcare delivery.

India Telemedicine Market Coverage

Type Insight and Forecast 2026 - 2035

- Hardware

- Software

- Telemedicine Consultation Services

Modality Insight and Forecast 2026 - 2035

- Real-Time Telemedicine

- Remote Patient Monitoring

- Store-and-Forward Practice

- Consultation Between Specialists and Primary Caregivers

- Medical Imaging

- Telemedicine Networks

Application Insight and Forecast 2026 - 2035

- Teleradiology

- Telepathology

- Telecardiology

- Telepsychiatry

- Teledermatology

End-User Insight and Forecast 2026 - 2035

- Healthcare Facilities

- Homecare

India Telemedicine Market by Region

- Maharashtra

- By Type

- By Modality

- By Application

- By End-User

- Karnataka

- By Type

- By Modality

- By Application

- By End-User

- Delhi NCR

- By Type

- By Modality

- By Application

- By End-User

- Tamil Nadu

- By Type

- By Modality

- By Application

- By End-User

- Rest of India

- By Type

- By Modality

- By Application

- By End-User

Table of Contents for India Telemedicine Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Modality

1.2.3. By

Application

1.2.4. By

End-User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. India Market Estimate and Forecast

4.1. India Market Overview

4.2. India Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Hardware

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Software

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Telemedicine Consultation Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Modality

5.2.1. Real-Time Telemedicine

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Remote Patient Monitoring

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Store-and-Forward Practice

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Consultation Between Specialists and Primary Caregivers

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Medical Imaging

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Telemedicine Networks

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Teleradiology

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Telepathology

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Telecardiology

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Telepsychiatry

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Teledermatology

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End-User

5.4.1. Healthcare Facilities

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Homecare

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. Maharashtra Market Estimate and Forecast

6.1. By

Type

6.2. By

Modality

6.3. By

Application

6.4. By

End-User

7. Karnataka Market Estimate and Forecast

7.1. By

Type

7.2. By

Modality

7.3. By

Application

7.4. By

End-User

8. Delhi NCR Market Estimate and Forecast

8.1. By

Type

8.2. By

Modality

8.3. By

Application

8.4. By

End-User

9. Tamil Nadu Market Estimate and Forecast

9.1. By

Type

9.2. By

Modality

9.3. By

Application

9.4. By

End-User

10. Rest of India Market Estimate and Forecast

10.1. By

Type

10.2. By

Modality

10.3. By

Application

10.4. By

End-User

11. Company Profiles

11.1.

1mg

11.1.1.

Snapshot

11.1.2.

Overview

11.1.3.

Offerings

11.1.4.

Financial

Insight

11.1.5.

Recent

Developments

11.2.

CVS Health

11.2.1.

Snapshot

11.2.2.

Overview

11.2.3.

Offerings

11.2.4.

Financial

Insight

11.2.5.

Recent

Developments

11.3.

Lybrate, Inc.

11.3.1.

Snapshot

11.3.2.

Overview

11.3.3.

Offerings

11.3.4.

Financial

Insight

11.3.5.

Recent

Developments

11.4.

Meta16labs Healthcare & Analytics Pvt. Ltd.

11.4.1.

Snapshot

11.4.2.

Overview

11.4.3.

Offerings

11.4.4.

Financial

Insight

11.4.5.

Recent

Developments

11.5.

Netmeds Marketplace Ltd.

11.5.1.

Snapshot

11.5.2.

Overview

11.5.3.

Offerings

11.5.4.

Financial

Insight

11.5.5.

Recent

Developments

11.6.

NovaCura Tech Health Services

11.6.1.

Snapshot

11.6.2.

Overview

11.6.3.

Offerings

11.6.4.

Financial

Insight

11.6.5.

Recent

Developments

11.7.

Practo

11.7.1.

Snapshot

11.7.2.

Overview

11.7.3.

Offerings

11.7.4.

Financial

Insight

11.7.5.

Recent

Developments

11.8.

Rijuven (India)

11.8.1.

Snapshot

11.8.2.

Overview

11.8.3.

Offerings

11.8.4.

Financial

Insight

11.8.5.

Recent

Developments

11.9.

TeleVital

11.9.1.

Snapshot

11.9.2.

Overview

11.9.3.

Offerings

11.9.4.

Financial

Insight

11.9.5.

Recent

Developments

11.10.

Zoylo Digihealth Pvt. Ltd.

11.10.1.

Snapshot

11.10.2.

Overview

11.10.3.

Offerings

11.10.4.

Financial

Insight

11.10.5.

Recent

Developments

12. Appendix

12.1. Exchange Rates

12.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

India Telemedicine Market