Digital Radiology Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Modality (X ray systems, Computed tomography systems, Magnetic resonance imaging systems, Ultrasound imaging systems, Nuclear imaging systems), by Portability (Fixed digital radiology systems, Portable digital radiology systems), by Technology (Computed radiography, Direct radiography, Hybrid digital imaging systems), by End Use (Hospitals, Diagnostic imaging centers, Specialty clinics)

| Status : Published | Published On : Jun, 2026 | Report Code : VRHC1342 | Industry : Healthcare | Available Format :

|

Page : 143 |

Digital Radiology Market Overview

The Digital radiology market size was estimated at USD 8.6 billion in 2025 and is expected to reach around USD 9.2 billion in 2026, rising up to roughly USD 18.5 billion in 2035, growing at approximately 8.2% CAGR from 2026 to 2035.

Research Highlights

- X ray systems led 2025 with 36% share due widespread diagnostic screening across hospitals globally

- Computed tomography systems fastest growth at 9.1% CAGR driven by oncology and trauma imaging demand

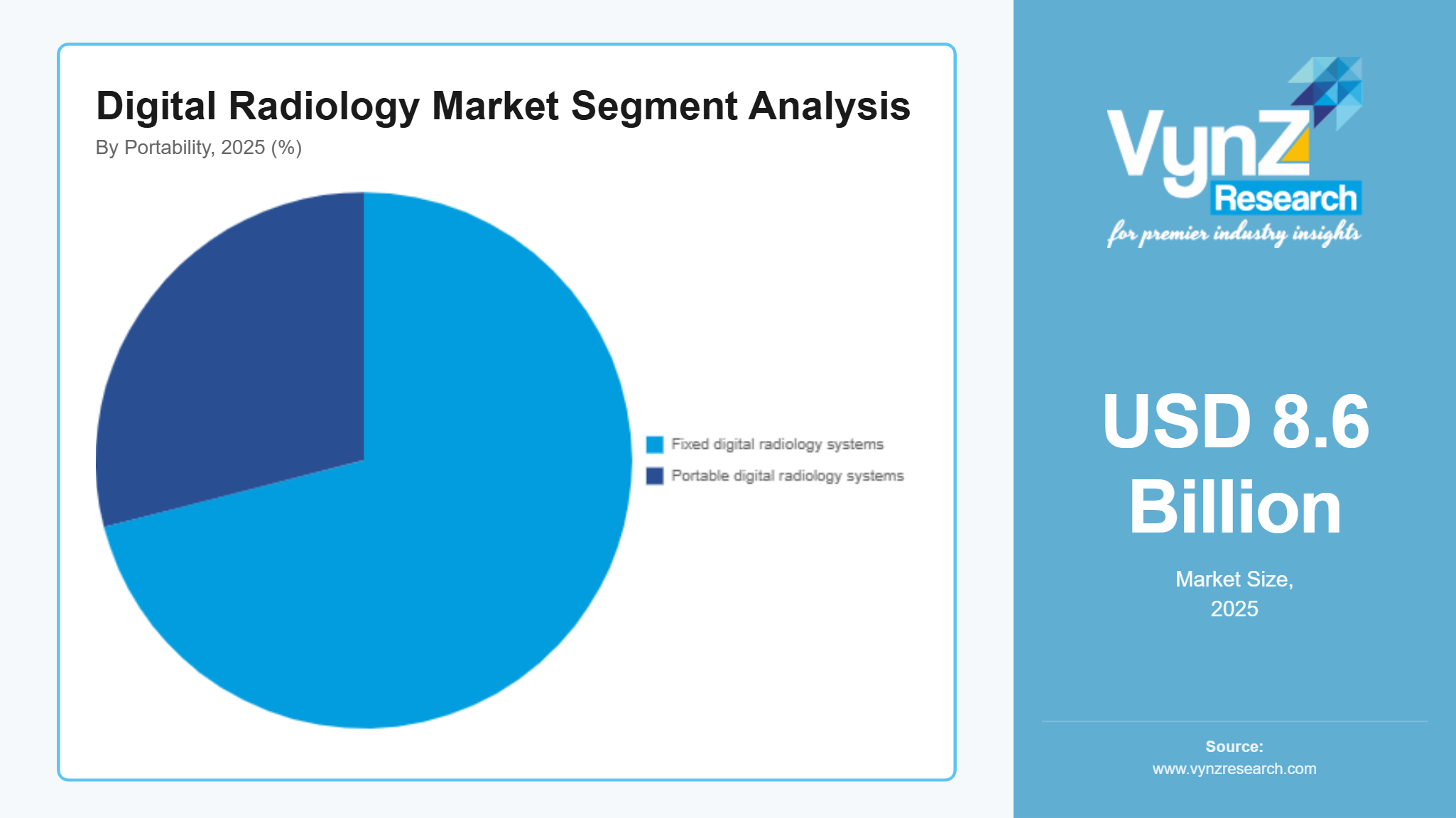

- Fixed digital radiology systems dominated 2025 with 71% share due hospital infrastructure expansion and capacity needs

- Portable digital radiology systems fastest growth at 10.4% CAGR driven by point care and emergency imaging

- Asia Pacific led 2025 with 23% share driven by healthcare digitization and hospital infrastructure expansion globally

The market is expanding due to higher demand and the growing shift in hospitals and diagnostic centers from analog systems to advanced digital systems that improve workflow, accuracy and patient care. Growing prevalence of diseases in underdeveloped countries and need by doctors to find these diseases accurately are also pushing the market forward. Higher adoption of systems using AI and cloud imaging in radiology help doctors make decisions faster and more accurately, pushing the market for diagnostic imaging systems. Governments like the United States Centers for Medicare and Medicaid Services, National Health Mission of India, the United Kingdom National Health Service are spending more money on development of healthcare and digitalization following the guidelines of the World Health Organization for imaging. The International Atomic Energy Agency is observing the safety standards for imaging which is pushing the market growth in North America, Europe and Asia Pacific.

Digital Radiology Market Dynamics

Market Trends

The industry is changing a lot with hospitals going digital and using artificial intelligence in medical imaging. One big trend is the move towards using AI to help doctors interpret images and storing them in the cloud. This improves diagnosis, workflow and accuracy. Another trend is the use of digital imaging platforms that work well with hospital systems and follow certain standards. These changes are influenced by guidelines from the World Health Organization, the US Food and Drug Administration and the International Atomic Energy Agency to make radiology safer, faster and more reliable.

Growth Drivers

The market is growing because of the increasing number of people with diseases pushing the demand for diagnostic applications in oncology, cardiology and orthopedics. The growth of the market is largely supported by the growing burden of diseases and increasing investments in healthcare infrastructure expansion. The government is investing in healthcare infrastructure for example in the US, India and China and there is a growing focus on precise diagnostics by hospitals and diagnostic centers to be cost-efficient, accurate and fast.

Market Restraints / Challenges

Even though the market is growing there are some challenges. One of them is that advanced imaging systems are very expensive requiring higher capital investment for imaging systems. Data security and interoperability challenges pose barriers for healthcare providers making it difficult for mid-sized healthcare facilities to adopt them especially in regions where price is a concern. Regulatory requirements under US Food and Drug Administration medical device standards and European Medicines Agency imaging safety protocols also increase approval timelines and operational costs.

Market Opportunities

The market has opportunities in AI-driven diagnostic imaging and remote radiology services. Companies offering cloud-enabled, AI-enhanced and portable imaging solutions are well positioned to capture demand. There is a growing demand for diagnostic reporting and a shortage of radiology specialists in some regions. Another key opportunity lies in tele-radiology and mobile imaging systems with increased investments in healthcare infrastructure creating more access and better diagnostic coverage. Advancements supported by World Health Organization health initiatives and United Nations Sustainable Development Goal 3 on good health and wellbeing are expected to enhance adoption and strengthen long term market growth.

Global Digital Radiology Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 8.6 Billion |

|

Revenue Forecast in 2035 |

USD 18.5 Billion |

|

Growth Rate |

8.2% |

|

Segments Covered in the Report |

By Modality, By Portability, By Technology, By End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Agfa-Gevaert, Canon Medical Systems, Carestream Health, Fujifilm Holdings, GE HealthCare, Hitachi, Hologic, Philips Healthcare, Siemens Healthineers, Shimadzu Corporation |

|

Customization |

Available upon request |

Digital Radiology Market Segmentation

By Modality

The X ray systems held 36% of the share of the market in 2025 because they are used a lot in hospitals and diagnostic centers for checking patients and performing tests. They are also affordable and easy to use which is why they are widely accepted and available. The World Health Organization says that diagnostic imaging should be easily accessible and X ray systems should fit the bill.

Computed tomography systems are expected to grow fast about 9.1% from 2026 to 2035 because doctors need resolution images to diagnose diseases like cancer and heart problems. The United States Food and Drug Administration is also helping to improve imaging which is making these systems more popular.

By Portability

Fixed systems contributed roughly 71% of the market share in 2025 due to higher adoption in hospitals and big diagnostic centers for their ability to handle a lot of patients and produce quality images. The United Kingdom National Health Service and India National Digital Health Mission are also investing in hospital infrastructure which is helping to increase demand.

Portable digital radiology systems are expected to grow fast at about 10.4% from 2026 to 2035 due to their effectiveness in emergency situations and can be used in remote areas. The World Health Organization is also promoting telemedicine which is helping to increase the use of these systems.

By Technology

Direct radiography accounted for about 48% of the market share in 2025 as it produces quality images quickly with less radiation. The International Atomic Energy Agency and United States Food and Drug Administration are also guiding the use of these systems which is helping to increase their adoption.

Hybrid digital imaging systems will grow at about 9.3% from 2026 to 2035 due to their ability to integrate imaging workflows and use artificial intelligence to help diagnose diseases. Hospitals are investing in infrastructure which is helping to increase the use of these systems.

By End Use

Hospitals held about 62% of the market share in 2025 due to large number of patients and growing need diagnostic equipment. The United States Centers for Medicare and Medicaid Services and China Healthy China 2030 strategy are also helping to increase demand.

Diagnostic imaging centers are going to grow fast about 9% from 2026 to 2035 because they are cost effective and can produce quick results along with the growing preference for patients to go to these centers for tests which is helping to increase demand.

Regional Insights

North America

North America accounted for about 38% of the market in 2025 due to a robust healthcare infrastructure, higher use of AI-enabled diagnostic imaging systems and growing digitalization in hospitals. Most of the demand for North America medical imaging systems is in the United States and Canada because these countries have wider hospital networks in cities like New York, Toronto and Chicago. The government is helping with programs like the United States Centers for Medicare and Medicaid Services and working on quality improvement initiatives and the National Institutes of Health is investing money for imaging research.

Europe

Europe made up about 29% of the market in 2025 supported by strict rules, preference by hospitals for using digital systems and growing emphasis on precision diagnostics. The countries with the demand are Germany, France and the United Kingdom due to strong healthcare systems and higher adoption of advanced imaging technologies. The European Medicines Agency and the World Health Organization are helping with rules and guidelines pushing the use of efficient radiology systems. Hospitals are updating their infrastructure and investing in AI based imaging workflows making the market in Europe grow.

Asia Pacific

Asia Pacific contributed roughly 23% of the market share in 2025 due to development in healthcare infrastructure, expanding networks and focusing on digital health transformation. The countries with the demand are China, India, Japan and South Korea with many hospitals and healthcare hubs. The governments of these countries are helping with initiatives like the India National Digital Health Mission, China Healthy China 2030 strategy and Japan healthcare digitalization programs pushing the use of imaging systems. Growing population and number of chronic diseases are also pushing the market in this region.

Rest of the World

The rest of the world held about 10% of the market in 2025 which includes Latin America, the Middle East and Africa. These places are developing their healthcare infrastructure and using advanced diagnostic and imaging systems more and more. Countries like Brazil, Saudi Arabia and South Africa are investing in hospital modernization and diagnostic facility expansion. The government is helping with initiatives aligned with the World Health Organization helping the adoption and expansion of public healthcare services.

Competitive Landscape / Company Insights

The market for imaging is moderately competitive with a lot of companies trying to come up with new products and ideas. These companies, both small and big, are focusing on product innovation, affordability and accessibility. They are spending a lot of money on research to make AI-enabled systems that will help doctors diagnose problems and store medical images on the cloud to stay ahead of the competition. Rules and regulations set by the United States Food and Drug Administration, the World Health Organization and the European Medicines Agency determine what products are allowed and how they are made, increasing competition among them.

Mini Profiles

Agfa-Gevaert focuses on digital radiology imaging solutions including advanced X ray and PACS systems, supported by strong healthcare brand recognition and established global hospital distribution networks across multiple regions.

Canon Medical Systems operates in premium medical imaging segments, emphasizing high performance radiology systems and advanced diagnostic accuracy, supported by strong innovation capabilities and integrated imaging technology platforms globally.

Carestream Health leverages digital imaging technologies and strategic healthcare partnerships to expand market presence, focusing on efficient radiology systems and software solutions for hospitals and diagnostic imaging centers worldwide.

Fujifilm Holdings focuses on medical imaging and digital radiology systems, supported by strong diversification across healthcare technologies and advanced diagnostic solutions enabling improved imaging workflow efficiency and accuracy.

GE HealthCare operates in premium healthcare imaging segments, emphasizing advanced radiology systems, AI integrated diagnostics, and strong global hospital network presence supported by deep clinical innovation capabilities.

Key Players

- Agfa-Gevaert

- Canon Medical Systems

- Carestream Health

- Fujifilm Holdings

- GE HealthCare

- Hitachi

- Hologic

- Philips Healthcare

- Siemens

- Healthineers

- Shimadzu Corporation

Recent Developments

In February 2025, Siemens Healthineers expanded its digital radiology portfolio by introducing upgraded AI enabled imaging software designed to improve diagnostic accuracy and workflow efficiency. The company strengthened its hospital partnerships across Europe and North America to accelerate adoption of integrated imaging systems.

In April 2025, Philips Healthcare launched enhanced cloud based radiology solutions focused on remote diagnostics and real time imaging collaboration. The initiative aimed to improve hospital efficiency and support tele radiology expansion across global healthcare networks.

In June 2025, Hitachi introduced next generation digital X ray and CT imaging systems with improved dose reduction and faster processing capabilities. The development focused on supporting early disease detection and enhancing patient safety in high volume clinical settings.

In September 2025, Shimadzu Corporation announced advancements in digital radiography systems with upgraded detector technologies for improved image clarity. The company emphasized stronger penetration in diagnostic imaging centers across Asia Pacific and North America.

In January 2026, Hologic expanded its imaging solutions portfolio with enhanced radiology systems targeting women’s health diagnostics. The development focused on improving precision imaging performance and strengthening adoption in specialized diagnostic clinics globally.

Global Digital Radiology Market Coverage

Modality Insight and Forecast 2026 - 2035

- X ray systems

- Computed tomography systems

- Magnetic resonance imaging systems

- Ultrasound imaging systems

- Nuclear imaging systems

Portability Insight and Forecast 2026 - 2035

- Fixed digital radiology systems

- Portable digital radiology systems

Technology Insight and Forecast 2026 - 2035

- Computed radiography

- Direct radiography

- Hybrid digital imaging systems

End Use Insight and Forecast 2026 - 2035

- Hospitals

- Diagnostic imaging centers

- Specialty clinics

Global Digital Radiology Market by Region

- North America

- By Modality

- By Portability

- By Technology

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Modality

- By Portability

- By Technology

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Modality

- By Portability

- By Technology

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Modality

- By Portability

- By Technology

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Digital Radiology Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Modality

1.2.2. By

Portability

1.2.3. By

Technology

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Modality

5.1.1. X ray systems

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Computed tomography systems

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Magnetic resonance imaging systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Ultrasound imaging systems

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Nuclear imaging systems

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Portability

5.2.1. Fixed digital radiology systems

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Portable digital radiology systems

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Technology

5.3.1. Computed radiography

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Direct radiography

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Hybrid digital imaging systems

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Diagnostic imaging centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Specialty clinics

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Modality

6.2. By

Portability

6.3. By

Technology

6.4. By

End Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Modality

7.2. By

Portability

7.3. By

Technology

7.4. By

End Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Modality

8.2. By

Portability

8.3. By

Technology

8.4. By

End Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Modality

9.2. By

Portability

9.3. By

Technology

9.4. By

End Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Agfa-Gevaert

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Canon Medical Systems

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Carestream Health

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Fujifilm Holdings

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

GE HealthCare

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Hitachi

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Hologic

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Philips Healthcare

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Siemens Healthineers

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Shimadzu Corporation

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Digital Radiology Market