Brain-Computer Interfaces Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Invasive, Partially invasive, Non invasive), by Component (Hardware, Software, Services), by Application (Healthcare, Communication and control, Entertainment and gaming, Smart home control), by End User (Healthcare institutions, Research and academic organizations, Military and defense, Commercial users), by Technology (Electroencephalography (EEG), Electrocorticography (ECoG), Functional magnetic resonance imaging (fMRI), Near infrared spectroscopy (NIRS))

| Status : Published | Published On : May, 2026 | Report Code : VRHC1336 | Industry : Healthcare | Available Format :

|

Page : 164 |

Brain-Computer Interfaces Market Overview

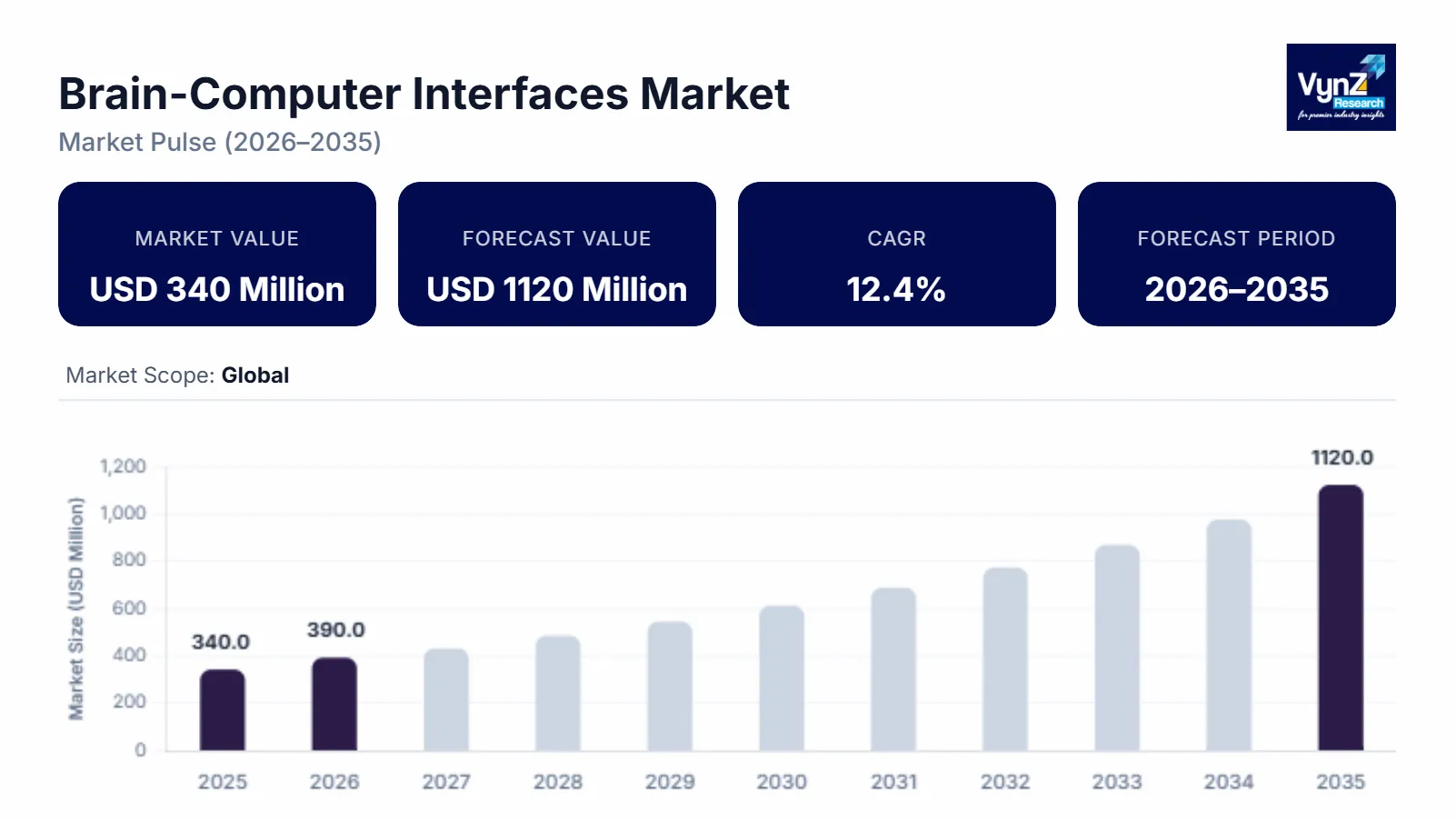

The global brain computer interface market which was valued at approximately USD 340 million in 2025 and is estimated to rise further up to almost USD 390 million by 2026, is projected to reach around USD 1120 million in 2035, expanding at a CAGR of about 12.4% during the forecast period from 2026 to 2035.

Market growth results from three factors which include rising neurological disorder cases, neurotechnology progress, and enhanced artificial intelligence usage for brain signal analysis combined with increased use of noninvasive interface technologies. The World Health Organization highlights a significant global burden of neurological conditions which supports long term need for assistive and therapeutic technologies. The growing need for neurorehabilitation and cognitive monitoring solutions, together with increased brain research program funding and national neuroscience initiative investments, drive market growth across major regions including the United States, and Germany and China.

Brain-Computer Interfaces Market Dynamics

Market Trends

The industry is undergoing significant changes because its technological applications and clinical usage methods are both developing at different rates. The market experiences a fundamental shift because increasing adoption of noninvasive wearable interface systems which exhibit safer, more economical and simpler design characteristics for medical and consumer product usage. The field of neural signal processing is witnessing its first major advance through artificial intelligence and machine learning technologies that make it possible to interpret neural signals which have received fast technology development and digital health system growth in medical fields.

Growth Drivers

Healthcare and rehabilitation services maintain steady demand because neurological disorders create an increasing need for brain computer interface market development. The World Health Organization reports a steady rise in conditions such as epilepsy, Alzheimer disease, and stroke related disabilities, supporting long term adoption of assistive neurotechnology. Healthcare market growth accelerates because both medical facilities and neuroscience research organizations increase their financial investments in healthcare system development. The healthcare industry sees higher adoption rates for neuro-prosthetic systems and communication assistance technologies which provide essential support for their users.

Market Restraints / Challenges

The market should expand according to its growth forecast but the industry faces specific market challenges which will hinder its progress. High device and implementation costs, along with complex regulatory approval processes, continue to affect market penetration, particularly among cost sensitive healthcare systems. Data privacy issues and ethical concerns about neural data handling create operational difficulties for service developers and service providers. Businesses in emerging markets face cost challenges because they need to use advanced technologies which require specialized knowledge to operate.

Market Opportunities

The market presents substantial chances for growth because neurorehabilitation and assistive communication areas require advanced therapy solutions to meet rising demand from disabled people. Healthcare providers who need cost effective interface solutions should choose those businesses that provide budget-friendly interface technologies which can be used in multiple settings. Digital health investments combined with rising consumer demands for cognitive monitoring solutions have created an opportunity for companies to enter the rapidly developing digital health and cognitive monitoring markets. Exponential growth in artificial intelligence systems, cloud-based system analytics and wearable system technologies will make systems easier to use while creating additional applications. Government-supported neuroscience programs and digital health initiatives will drive innovation and product acceptance across essential markets.

Global Brain-Computer Interfaces Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 340 Million |

|

Revenue Forecast in 2035 |

USD 1120 Million |

|

Growth Rate |

12.4% |

|

Segments Covered in the Report |

Type, Component, Application, End User, Technology |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Abbott, Blackrock Neurotech, Brain Products, Emotiv, g.tec medical engineering, Medtronic, Neuralink, NeuroPace, Nihon Kohden, Synchron |

|

Customization |

Available upon request |

Brain-Computer Interfaces Market Segmentation

By Type

The non-invasive interfaces achieved the highest market share in 2025 because they enabled 58% of total revenue through their easy implementation, lower risk during procedures and their ability to function in both medical and consumer markets. The market shows increased adoption of electroencephalography solutions for monitoring neurological conditions and using electroencephalography solutions in rehabilitation procedures. The expansion of digital health programs which receive government funding and the clinical research programs that study non-invasive neurotechnology applications create growth opportunities for hospitals and home care facilities which need to maintain safety and accessibility standards.

The invasive systems will experience the highest market expansion because they will reach a CAGR of 13.1% from 2026 to 2035. The market advances through the development of implantable neuro-prosthetics and the successful results that clinical trials have achieved for treating paralysis and severe neurological disorders. The combination of regulatory agency support and national neuroscience research funding programs helps to drive both innovation and market entry for this industry sector.

By Application

Healthcare applications captured nearly 49% of total market revenue in 2025 because neurological disorder cases increased and neurorehabilitation and assistive communication technology usage expanded. The World Health Organization reports that neurological diseases have reached epidemic levels worldwide which has created a need for advanced therapeutic options. The growing healthcare system development and neurotechnology adoption in clinical environments create additional strength for this market segment.

The communication and control applications market will achieve the highest growth rate which will result in a CAGR of 12.8% from 2026 to 2035. The increasing use of brain computer interfaces in assistive technologies for physically impaired individuals enables them to control external devices more effectively which drives market growth. The development of advanced signal processing technology and human machine interaction technology leads to better performance outcomes in both medical and non-medical settings.

By Component

The hardware segment achieved market leadership through its 2025 total revenue share of approximately 46% because healthcare professionals required sensors, electrodes and signal collection systems for proper neural data gathering. The industry sees increased hardware usage because of ongoing improvements in device miniaturization and higher precision standards. Government funding for medical device development and neurotechnology infrastructure development creates positive market conditions for this business segment.

The software market will experience the highest growth rate which will result in a 13.4% CAGR from the present time until the complete forecast period. The growing adoption of AI and machine learning technologies for automated data processing and predictive analysis functions drives market expansion. The introduction of cloud platforms and digital health systems enables software development which improves application performance through better user experience and application scalability.

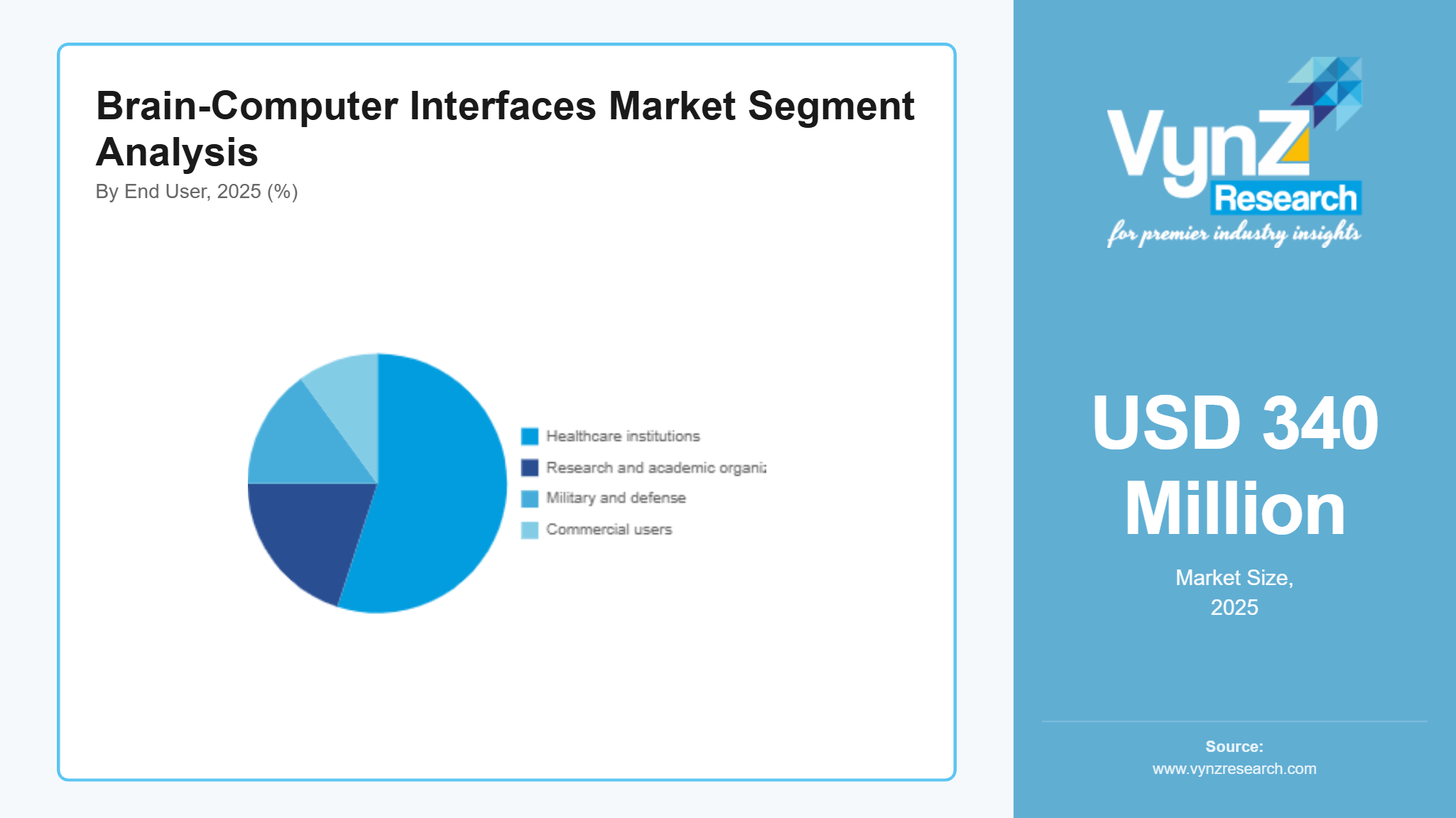

By End User

The healthcare institutions reached revenue leadership in 2025 with around 55% share because they treated more patients, used neurorehabilitation technology and opened new specialized treatment centers for their work. The market for neurological care solutions in hospitals and rehabilitation centers expands through healthcare programs which government programs and funding agencies establish.

The research and academic center market will see the most rapid growth with a projected CAGR of 12.9% between 2026 and 2035. The public funding bodies and the international collaboration networks support clinical trials, neuroscience research and innovation programs which have created market growth. The ongoing development of brain mapping research and cognitive research has increased demand for next generation brain computer interface solutions.

Regional Insights

North America

The market in North America reached 30% market share during 2025 because of advanced healthcare infrastructure, substantial research funding and numerous neurotechnology companies operating in the region. Major urban centers such as New York, Boston, and San Francisco continue to support adoption across hospitals and research institutions. The region benefits from extensive neuroscience programs and regulatory oversight from agencies such as the U.S. Food and Drug Administration, which ensures safety and accelerates clinical approvals. Government backed initiatives including large scale brain research programs and funding support for neurological disorder treatment, aligned with data from public health authorities and global health organizations, continue to strengthen investment in innovative interface technologies and clinical applications.

Europe

The market share of Europe during 2025 stood at 23% because the region has established healthcare systems, academic research networks and their population exhibit rising rates of neurological disorders. Countries such as Germany, the United Kingdom, and France are witnessing steady adoption across hospitals and specialized research centers. The European Medicines Agency and regional health bodies play a crucial role in regulating medical devices and supporting clinical trials. Government funded neuroscience initiatives and digital health strategies are encouraging integration of brain computer interface technologies in rehabilitation and assistive care. Increasing collaboration between academic institutions and healthcare providers further supports consistent regional growth.

Asia Pacific

The market in Asia Pacific region reached 22% during 2025 because of expanding healthcare infrastructure, rising awareness of neurological disorders, and growing investments in medical technology. Countries such as China, Japan, and India are emerging as key contributors, with major cities including Beijing, Tokyo, and Bangalore acting as innovation hubs. The adoption of healthcare modernization programs and national brain research initiatives, which the government supports, is accelerating. Data from global health organizations shows that the region experiences an increasing burden of neurological diseases, which creates a sustained need for advanced neurotechnology solutions. The regional expansion of the market receives support from the increasing emphasis on digital health and affordable medical technologies.

Rest of the World

The global market share for 2025 showed the rest of the world contributed 25% because healthcare access improves and people learn more about neurological care in Latin America, the Middle East and Africa. Urban healthcare centers in Brazil, South Africa and the United Arab Emirates are experiencing early-stage adoption of medical technologies. Government backed healthcare initiatives and international collaborations are encouraging the introduction of advanced medical technologies.

Competitive Landscape / Company Insights

The competitive situation at present shows moderate activity because international technology firms and niche technology companies are currently developing neurotechnology solutions, testing them clinically, and expanding their usage into medical and assistive communication technologies. Companies are increasing their research and development spending while they develop artificial intelligence capabilities and advanced signal processing systems to enhance their products' marketability. The public health and scientific funding organizations show that both government-supported neuroscience research programs and healthcare innovation initiatives drive technological progress while aiding product market entry. The combination of hospital and academic institution partnerships with medical device regulations shapes the competitive landscape and market entry methods that companies use in both developed and emerging markets.

Mini Profiles

Abbott focuses on advanced medical devices and neurotechnology solutions, supported by strong global distribution networks and established healthcare brand recognition across diagnostic and therapeutic applications.

Blackrock Neurotech operates in the premium neurotechnology segment, emphasizing high performance brain computer interface systems designed for clinical research, neural recording, and advanced implantable communication technologies.

Compumedics leverages strong clinical research partnerships and digital neurodiagnostic capabilities to expand its presence in brain monitoring and sleep disorder related neurotechnology solutions across global healthcare markets.

Emotiv operates in the noninvasive consumer neurotechnology segment, emphasizing portable EEG based brain computer interface devices designed for research, cognitive tracking, and human computer interaction applications.

Medtronic focuses on advanced medical technology and neuromodulation systems, supported by strong global healthcare distribution strength and deep clinical integration across neurological and therapeutic applications.

Key Players

- Abbott

- Blackrock Neurotech

- Brain Products

- Emotiv

- g.tec medical engineering

- Medtronic

- Neuralink

- NeuroPace

- Nihon Kohden

- Synchron

Recent Developments

In December, 2025, Neuralink announced its plan to begin high volume production of brain computer interface devices in 2026 along with a shift toward fully automated surgical implantation systems. The company is scaling human trials, with multiple patients already using implants for communication and device control.

In February, 2025, Medtronic received regulatory approval for its adaptive deep brain stimulation system integrating brain computer interface capabilities for Parkinson’s disease treatment. The development strengthens its neuromodulation portfolio and expands clinical applications in real time brain signal monitoring.

In April, 2025, Precision Neuroscience achieved U.S. FDA clearance for a key component of its brain implant system, enabling safer cortical interface mapping for neurological procedures. The approval supports its expansion into clinical trials for restoring motor and speech functions in paralyzed patients.

In June, 2025, Blackrock Neurotech advanced its neural interface research through expanded clinical collaborations focused on high resolution brain signal decoding technologies. The company strengthened its position in invasive neural recording systems used in paralysis and communication restoration studies.

In May, 2025, Emotiv expanded its neurotechnology platform by upgrading its non invasive EEG based brain computer interface systems for cognitive research and human computer interaction applications. The company continues to enhance accessibility of brain sensing technologies for research and enterprise users.

Global Brain-Computer Interfaces Market Coverage

Type Insight and Forecast 2026 - 2035

- Invasive

- Partially invasive

- Non invasive

Component Insight and Forecast 2026 - 2035

- Hardware

- Software

- Services

Application Insight and Forecast 2026 - 2035

- Healthcare

- Communication and control

- Entertainment and gaming

- Smart home control

End User Insight and Forecast 2026 - 2035

- Healthcare institutions

- Research and academic organizations

- Military and defense

- Commercial users

Technology Insight and Forecast 2026 - 2035

- Electroencephalography (EEG)

- Electrocorticography (ECoG)

- Functional magnetic resonance imaging (fMRI)

- Near infrared spectroscopy (NIRS)

Global Brain-Computer Interfaces Market by Region

- North America

- By Type

- By Component

- By Application

- By End User

- By Technology

- By Country - U.S., Canada, Mexico

- Europe

- By Type

- By Component

- By Application

- By End User

- By Technology

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Type

- By Component

- By Application

- By End User

- By Technology

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Type

- By Component

- By Application

- By End User

- By Technology

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Brain-Computer Interfaces Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Component

1.2.3. By

Application

1.2.4. By

End User

1.2.5. By

Technology

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Invasive

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Partially invasive

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Non invasive

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Component

5.2.1. Hardware

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Software

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Services

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Healthcare

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Communication and control

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Entertainment and gaming

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Smart home control

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Healthcare institutions

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Research and academic organizations

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Military and defense

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Commercial users

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Technology

5.5.1. Electroencephalography (EEG)

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Electrocorticography (ECoG)

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Functional magnetic resonance imaging (fMRI)

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Near infrared spectroscopy (NIRS)

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Type

6.2. By

Component

6.3. By

Application

6.4. By

End User

6.5. By

Technology

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Type

7.2. By

Component

7.3. By

Application

7.4. By

End User

7.5. By

Technology

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Type

8.2. By

Component

8.3. By

Application

8.4. By

End User

8.5. By

Technology

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Type

9.2. By

Component

9.3. By

Application

9.4. By

End User

9.5. By

Technology

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Abbott

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Blackrock Neurotech

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Brain Products

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Emotiv

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

g.tec medical engineering

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Medtronic

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Neuralink

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

NeuroPace

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Nihon Kohden

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Synchron

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Brain-Computer Interfaces Market