Human Identification Market Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Consumables, Instruments, Software), by Technology (PCR-based technologies, Next generation sequencing, Capillary electrophoresis), by Application (Forensic applications, Paternity and kinship testing, Clinical and research applications), by End User (Forensic laboratories, Hospitals and research institutions, Government agencies)

| Status : Published | Published On : Apr, 2026 | Report Code : VRHC1335 | Industry : Healthcare | Available Format :

|

Page : 153 |

Human Identification Market Overview

The global human identification market which was valued at approximately USD 0.82 billion in 2025 and is estimated to rise further up to almost USD 0.96 billion by 2026, is projected to reach around USD 2.35 billion in 2035, expanding at a CAGR of about 11.8% during the forecast period from 2026 to 2035.

The market is driven by increasing demand for forensic analysis, growing application of DNA profiling in criminal investigations, and rising focus on disaster victim identification, along with increasing adoption of advanced genomic technologies. The market is growing because law enforcement and healthcare systems are using more biometric and molecular identification methods.

The market expands because forensic and clinical identity verification needs accurate identity verification, which drives national security and public health system investments. The World Health Organization reports show that genomic surveillance and laboratory strengthening have important roles in supporting identification technologies. The government-backed forensic modernization programs together with DNA databank funding across North America, Europe and Asia Pacific, enable more regions to adopt DNA databank technology. The regulatory frameworks which promote standardized forensic practices and cross-border data sharing, create conditions for sustained growth across key regions.

Human Identification Market Dynamics

Market Trends

The market experiences major technological changes together with new forensic data integration methods that law enforcement operations between both law enforcement and healthcare systems use for their identification work. The market experiences an important transformation because next generation sequencing together with advanced DNA analysis platforms gain more popularity as people prefer these technologies which deliver better accuracy and larger sample processing capacity. The World Health Organization and national forensic authorities publish guidelines and technical frameworks which establish standardized laboratory practices and quality assurance systems while promoting automated workflows and digital evidence management system usage in forensic laboratories.

Growth Drivers

The market experiences growth because forensic investigation needs and criminal identification requirements drive ongoing demand from law enforcement agencies and judicial systems. The market expansion gets faster because national security infrastructure and forensic laboratory DNA databank expansion program investments are increasing. The worldwide public health and security organizations demonstrate that molecular identification technologies become essential tools for crime resolution and disaster response. The public security organizations utilize molecular identification technologies to solve crimes and respond to disasters thus supporting permanent adoption.

Market Restraints / Challenges

The market demonstrates positive growth potential but it encounters multiple obstacles which will prevent its expansion. Data privacy regulations and ethical requirements combined with cross-border data sharing rules create complex requirements which restrict market access for organizations that operate in compliance-focused regions. The World Health Organization together with national regulatory bodies create policies which require strict control over genetic data usage thus making it harder for organizations to implement these rules while increasing their operational expenses.

Market Opportunities

The market provides numerous opportunities for growth through the development of forensic identification systems and biometric identification systems which will meet the needs of emerging economies that face increasing urbanization and rising crime rates and their requirement for identity systems. Law enforcement agencies together with public sector institutions will develop a bigger need for identification solutions which organizations deliver at affordable prices and scalable capacities. The United Nations together with national security agencies support government initiatives to establish forensic infrastructure and build digital identity systems which will increase public system usage.

Global Human Identification Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 0.82 Billion |

|

Revenue Forecast in 2035 |

USD 2.35 Billion |

|

Growth Rate |

11.8% |

|

Segments Covered in the Report |

Product Type, Technology, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Agilent Technologies, Danaher Corporation, Eurofins Scientific, GE Healthcare, Illumina Inc., Merck KGaA, NEC Corporation, QIAGEN N.V., Roche Diagnostics, Thermo Fisher Scientific |

|

Customization |

Available upon request |

Human Identification Market Segmentation

By Product Type

The market in 2025 reached its highest point through consumables which generated 58% of total revenue for that year. For forensic laboratories, their testing needs for DNA extraction and amplification and analysis processes require ongoing access to their products which establishes their market control. The ongoing demand for forensic laboratory consumables results from government-supported programs and laboratory expansion efforts which national forensic departments and the World Health Organization back. The backlogs of cases which need fast identification during criminal investigations and emergency response operations drive laboratory adoption in both public and private institutions. From 2026 to 2035, instruments will achieve the highest growth rate through their projected compound annual growth rate of 12.6% during that time. The combination of automated sequencing systems and real time PCR platforms with forensic analysis tools results in better throughput and accuracy which drives market expansion. The adoption of forensic infrastructure modernization and laboratory digitization programs accelerates in emerging economies because their governments enhance analytical capabilities through their ongoing investments.

By Technology

PCR-based technologies held the largest market share in 2025, contributing approximately 46% of segment revenue. The high sensitivity of the system, its established protocols, and its ability to work with different forensic and clinical applications make it suitable for widespread adoption. The international health and forensic organizations established standardization guidelines which enable PCR methods to deliver dependable DNA profiling results used in criminal investigations and identity verification processes. The fastest market growth will occur through next generation sequencing which will achieve a 13.2% compound annual growth rate from 2026 to 2035. The technology provides detailed genetic information which helps to analyze complex cases and supports high throughput testing because of its improved accuracy. The adoption of genomic research programs and advanced laboratory infrastructure starts to grow in regions which focus on precision medicine and forensic modernization.

By Application

Forensic applications generated the highest revenue in 2025 through their 51% share of total market earnings. Human identification technologies find extensive application in criminal investigations, law enforcement operations, and disaster victim identification which allows these technologies to dominate the market. The public sector institutions need reliable identification solutions which national security initiatives and forensic capacity building programs deliver through their funding support from global organizations and government agencies. The market for paternity and kinship testing will experience its highest growth during the forecast period through an estimated compound annual growth rate of 12.1%. The segment of genetic testing services expands because people now understand the genetic connections better and identity verification regulations increased and testing services became more available. The adoption of genetic screening and family tracing programs through public health initiatives results in increased usage across all regions of developed and emerging countries.

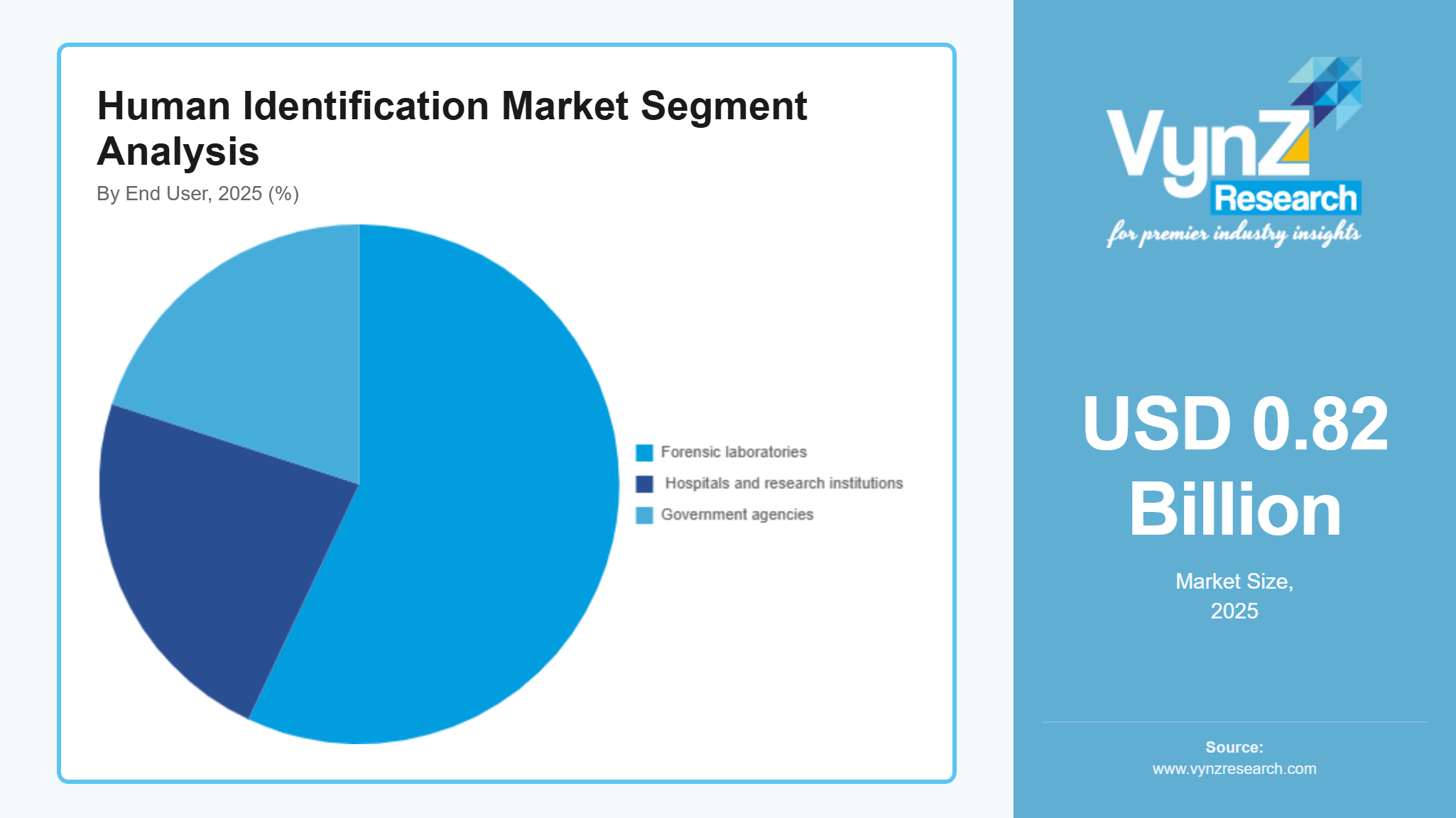

By End User

The market reached its highest point in 2025 through forensic laboratories which brought in 57% of total revenue. The market leader status of the company depends on three factors which include rising case numbers and expanding national DNA databases and the ongoing government support for forensic infrastructure development. The advanced identification technologies which these facilities use become more popular through programs that enhance criminal justice operations and boost investigative precision. The CAGR of hospitals and research institutions will reach 11.4% from 2026 until 2035. The market expands because genetic identification now has wider application in clinical diagnostics and biomedical research and epidemiological studies. Government-sponsored healthcare modernization projects and investments in genomic research facilities boost healthcare adoption while private laboratories and specialized testing centers expand their services to create overall market growth.

Regional Insights

North America

The market received 34% of its total value from North America in 2025 because the region has developed strong forensic systems and spends extensively on public safety while DNA analysis technologies are widely used. The established forensic laboratories of Washington D.C., New York and Los Angeles continuously generate demand through their law enforcement networks. The Federal Bureau of Investigation and other agencies report that national DNA database expansion and enhanced case processing capabilities have improved the analytical resources of the region.

Europe

The European market reached a 25% market share in 2025 because its forensic systems operate under established regulatory frameworks while security partnerships between countries continue to strengthen. The United Kingdom, Germany, France and the Netherlands all utilize DNA profiling and biometric identification as standard procedures in their police forces and governmental departments. The European Network of Forensic Science Institutes supports member states by establishing standardized protocols which enable forensic operations to work together.

Asia Pacific

Asia Pacific captured about 21% of the market in 2025 because urban areas in China, India, and Japan build more forensic systems which help them deal with increasing security threats. The cities of Beijing and Mumbai and Tokyo are expanding their use of identification technologies to enhance public safety and healthcare services. The World Health Organization reports that when laboratory systems and genomic capabilities become stronger, it enables organizations to implement advanced identification solutions.

Rest of the World

The Rest of the World, which includes Latin America, the Middle East and Africa, will generate approximately 20% of the market revenue in 2025. Public safety infrastructure investments and forensic science awareness and biometric identification system implementation create a growth environment in these regions. Brazil, South Africa and the United Arab Emirates are expanding their forensic capabilities while updating their identification systems to enhance law enforcement operations.

Competitive Landscape / Company Insights

The market shows moderate to extreme competition because international and local companies compete through product development, their pricing methods and international market expansion efforts. Companies are increasing their research and development investments together with their advanced genomic technology development and digital forensic technology research to enhance their market strength. The World Health Organization and national forensic authorities establish regulatory frameworks and quality standards which drive organizations to develop new products and their forensic modernization initiatives create competitive advantages across major regions.

Mini Profiles

Agilent Technologies focuses on genomic analysis instruments and reagents, supported by strong global distribution networks, established brand recognition, and consistent investment in precision diagnostics and laboratory workflow optimization solutions.

Bode Technology operates in the niche forensic services segment, emphasizing high accuracy DNA analysis, casework expertise, and collaboration with law enforcement agencies to support criminal investigations and identification processes.

Danaher Corporation focuses on life sciences and diagnostic solutions, supported by diversified product portfolios, strong operational efficiency, and continuous investment in innovation across molecular testing and analytical technologies.

Eurofins Scientific leverages extensive laboratory networks and strategic partnerships to expand market presence, offering comprehensive testing services across forensic, clinical, and environmental applications with strong geographic penetration.

GE Healthcare focuses on advanced imaging and diagnostic technologies, supported by global healthcare infrastructure, strong brand positioning, and continuous innovation in precision diagnostics and integrated healthcare solutions.

Key Players

- Agilent Technologies

- Danaher Corporation

- Eurofins Scientific

- GE Healthcare

- Illumina Inc.

- Merck KGaA

- NEC Corporation

- QIAGEN N.V.

- Roche Diagnostics

- Thermo

- Fisher Scientific

Recent Developments

In February 2026, Illumina Inc. advanced its sequencing portfolio through new product developments focused on next generation sequencing platforms, enhancing genomic accuracy and throughput for forensic and clinical applications. These innovations reinforce its leadership in genomic technologies and support expanding adoption across identification and research workflows.

In March 2026, QIAGEN N.V. continued expanding its molecular diagnostics capabilities through advancements in digital PCR technologies designed for clinical and forensic applications. The company’s focus on precision testing platforms supports improved analytical performance and broader adoption in identification processes.

In February 2026, Roche Diagnostics strengthened its position in genomic and sequencing solutions through continued development of integrated diagnostic platforms supporting high accuracy molecular analysis. These advancements are aligned with increasing demand for precision identification and clinical genomics applications.

In January 2026, Thermo Fisher Scientific expanded its diagnostic portfolio with regulatory approvals for advanced molecular testing systems, improving clinical identification capabilities and workflow efficiency. The company continues to invest in integrated genomic solutions supporting forensic and healthcare applications.

In April 2026, Merck KGaA increased its focus on genomics and molecular biology research through expanded product offerings supporting sequencing and analytical workflows. These developments strengthen its presence in identification technologies and support growing demand across research and forensic laboratories.

Global Human Identification Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Consumables

- Instruments

- Software

Technology Insight and Forecast 2026 - 2035

- PCR-based technologies

- Next generation sequencing

- Capillary electrophoresis

Application Insight and Forecast 2026 - 2035

- Forensic applications

- Paternity and kinship testing

- Clinical and research applications

End User Insight and Forecast 2026 - 2035

- Forensic laboratories

- Hospitals and research institutions

- Government agencies

Global Human Identification Market by Region

- North America

- By Product Type

- By Technology

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product Type

- By Technology

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product Type

- By Technology

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product Type

- By Technology

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Human Identification Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Consumables

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Instruments

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Software

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. PCR-based technologies

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Next generation sequencing

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Capillary electrophoresis

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Forensic applications

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Paternity and kinship testing

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Clinical and research applications

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Forensic laboratories

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Hospitals and research institutions

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Government agencies

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Technology

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Technology

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Technology

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Technology

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Agilent Technologies

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Danaher Corporation

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Eurofins Scientific

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

GE Healthcare

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Illumina Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Merck KGaA

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

NEC Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

QIAGEN N.V.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Roche Diagnostics

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Thermo Fisher Scientific

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Human Identification Market