APAC Needle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Conventional needles, Safety needles, Bevel needles, Blunt fill needles, Filter needles, Vented needles, Active needles, Passive needles), by Product (Suture needles, Blood collection needles, Ophthalmic needles, Dental needles, Insufflation needles, Pen needles, Others), by Delivery Mode (Hypodermic needles, Intravenous needles, Intramuscular needles, Intraperitoneal needles), by Material (Glass needles, Plastic needles, Stainless steel needles, Polyether ether ketone needles), by End User (Hospitals, Diagnostic centers, Home healthcare, Others)

| Status : Published | Published On : May, 2026 | Report Code : VRHC1335 | Industry : Healthcare | Available Format :

|

Page : 133 |

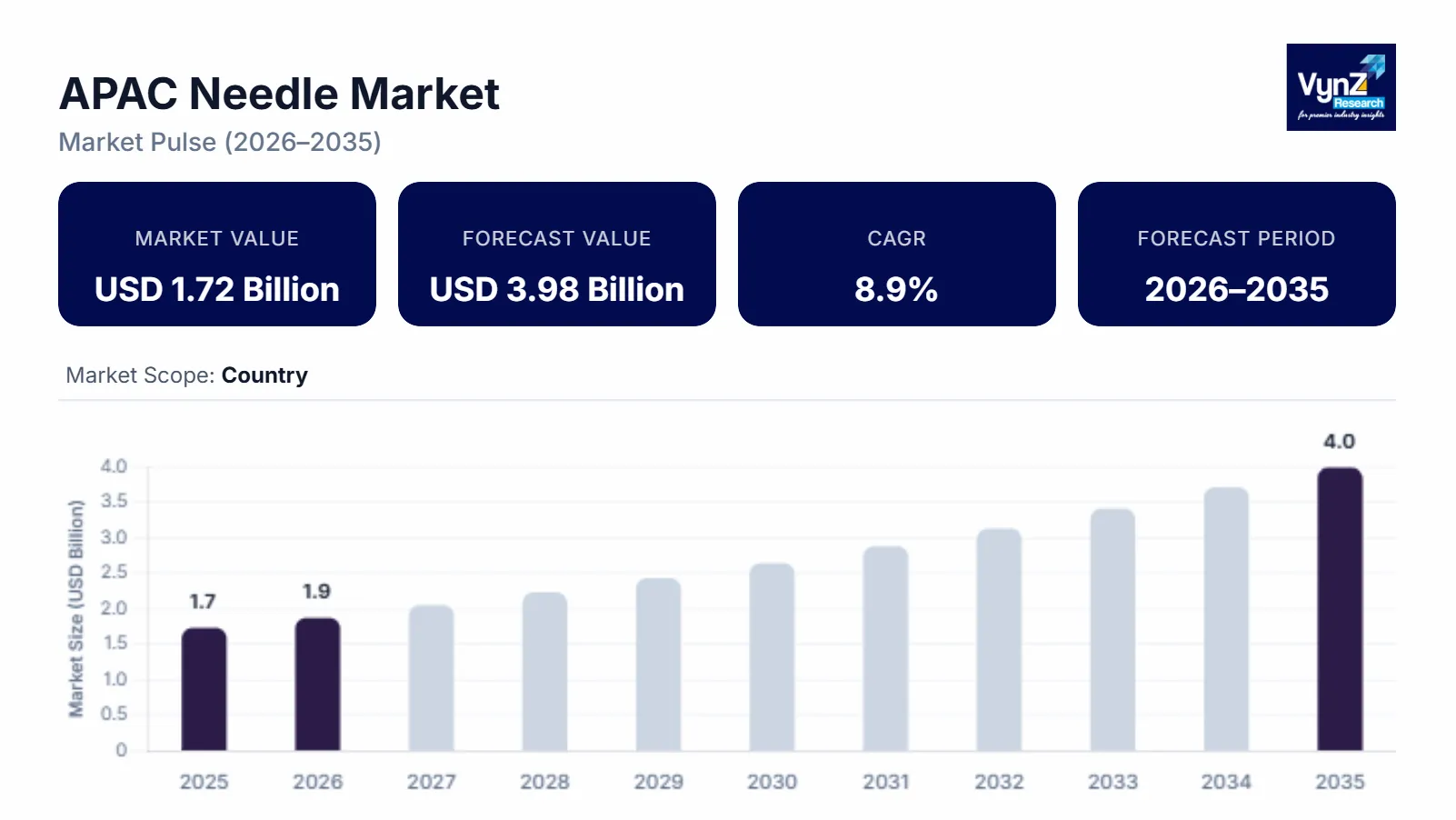

APAC Needle Market Overview

The APAC needle market which was valued at approximately USD 1.72 billion in 2025 and is estimated to rise further up to almost USD 1.86 billion by 2026, is projected to reach around USD 3.98 billion in 2035, expanding at a CAGR of about 8.9% during the forecast period from 2026 to 2035.

The market shows expansion because more people have chronic illnesses that need injectable treatments, while surgical and diagnostic treatments increase and vaccination programs expand, and more people use safety engineered needles. The World Health Organization data shows that vaccination programs in Asia Pacific continue to operate while diabetes and infectious disease cases rise, which leads to ongoing needs for injection devices.

The market growth across China, India, and Japan receives support from rising hospital treatment needs and home healthcare requirements, combined with public health infrastructure investments and immunization program funding. The disease control initiatives and vaccination programs of the government together receive support from WHO and national health departments. This results in higher purchasing of medical supplies, including needles. The regional healthcare facilities are experiencing higher adoption rates because infection prevention and safe injection practices have become more widely known, which regulatory guidelines and training programs support.

APAC Needle Market Dynamics

Market Trends

The industry shows technological changes which impact how healthcare systems acquire needles. The market trend which drives growth shows that safety engineered needle usage has increased because people prefer needles which prevent infections and protect workers. The World Health Organization recommends safer injection devices to decrease needle stick injuries which healthcare providers should implement through better design systems. The market trend shows that prefilled syringes and auto disable mechanisms have started to gain acceptance because companies need to meet regulations for their increasing vaccination activities. The product development process needs to change because these innovations force companies to create better safety solutions while they need to meet compliance requirements which results in new business competition patterns.

Growth Drivers

The market expands because hospitals, clinics and home healthcare services need more needles to treat rising chronic and infectious diseases. The World Health Organization reports that diabetes cases have been rising which requires patients to receive regular injectable treatments. Market growth in developing countries receives a boost from increasing healthcare infrastructure investments and vaccination program funding. Immunization coverage expansion acts as a key factor which drives vaccine uptake. The forecast period will see strong demand for high quality injection devices because healthcare systems require safe and efficient solutions which government disease prevention programs will support with funding and resources.

Market Restraints / Challenges

The market shows good growth potential yet it has specific obstacles which prevent market growth. The operational efficiency of small healthcare facilities suffers because biomedical waste management and safe disposal regulations create complex systems. Global health authorities require healthcare facilities to follow strict sharps disposal rules which results in higher operational costs. The need for suppliers to use imported raw materials and manufacturing components creates supply chain problems which affect their operational capabilities. The supply chain depends on imported raw materials which creates a risk of price increases and delivery interruptions during global trade disruptions thus hindering market growth and limiting expansion in regions which have price-sensitive markets.

Market Opportunities

The market presents significant opportunities in the expansion of home healthcare and self-administration practices, particularly driven by increasing prevalence of chronic diseases and aging population trends. Companies that provide injection solutions with user-friendly features and safety measures will attract extra patients who need ongoing medical treatment. The market presents another important chance to create advanced safety and smart injection devices which use increasing funding for improved medical consumables to drive better operational results. Safe injection practices will gain wider acceptance through global health organization initiatives which support their implementation while device design improvements and automation enhancements will make devices easier to operate and help patients adhere to treatment plans across the region.

APAC Needle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 1.72 Billion |

|

Revenue Forecast in 2035 |

USD 3.98 Billion |

|

Growth Rate |

8.9% |

|

Segments Covered in the Report |

By Type, By Product, By Material, By Delivery Mode, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, Thailand, Malaysia, Vietnam |

|

Key Companies |

B. Braun Melsungen AG, Becton Dickinson and Company, Hindustan Syringes and Medical Devices Ltd, Jiangsu Jichun Medical Devices Co Ltd, Kangmei Pharmaceutical Co Ltd, Medtronic plc, Nipro Corporation, Retractable Technologies Inc., Shandong Weigao Group Medical Polymer Company Limited, Terumo Corporation |

|

Customization |

Available upon request |

APAC Needle Market Segmentation

By Type

The market in 2025 saw safety needles achieve their highest market share which resulted in 48% revenue for the entire segment. The healthcare sector experiences rising regulatory demands to prevent infections and protect workers which enables safety needles to maintain their market leadership. The World Health Organization advises healthcare facilities to implement safe injection methods while limiting needle stick injuries which has affected their purchasing decisions especially in hospitals and public health initiatives. The increasing knowledge about blood borne diseases together with established training programs in medical facilities leads to higher usage of safety devices throughout both urban and semi urban territories.

The conventional needle market segment will experience consistent expansion which will reach an estimated CAGR of 8.4% during the period between 2026 and 2035. The market expands because customers find affordable options which they use for their routine clinical and diagnostic testing needs. The development of healthcare access in developing nations together with rising diagnostic center procedure volumes drives the growth of this segment. The continuous public health vaccination programs and basic medical access initiatives lead to consistent device usage in large population areas.

By Product

The largest segment of total market revenue in 2025 was generated by pen needles which accounted for 34% of total market revenue. The rising diabetes rates in Asia Pacific region lead to higher need for insulin which drives our product demand. The global health agencies report that the diabetic population numbers keep increasing in China and India which creates ongoing market demand. The rising preference for home healthcare and self-administration among patients leads to segment growth because patients want to use less painful methods for managing chronic diseases.

The field of blood collection and specialty needles will experience the fastest expansion because the market is projected to grow at a CAGR of 9.1% from 2026 until 2035. The diagnostic testing volume increases together with laboratory infrastructure development in emerging markets which supports market expansion. The government-supported screening programs together with disease surveillance initiatives drive the need for dependable sample collection equipment. The healthcare system diagnostics together with preventive screening programs lead to higher adoption rates by hospitals and diagnostic networks.

By Delivery Mode

Hypodermic delivery modes accounted for the largest market share in 2025, contributing approximately 46% of segment revenue. The delivery method handles all types of medical services which includes vaccination programs and medical procedures. Public health recommendations from the World Health Organization supporting standardized injection practices further strengthen adoption. The healthcare system expansion together with immunization campaigns drive ongoing demand for hypodermic delivery systems.

The intravenous and specialized delivery systems will experience the highest market growth which will reach a CAGR of 9.3% from 2026 to 2035. The growing hospital admissions together with rising demand for advanced therapeutic methods drive market growth. The market segment expands through government healthcare investments which enable more hospitals to build critical care facilities and surgical centers. The tertiary care facilities accelerate drug delivery systems when hospitals implement stricter safety measures for their patients.

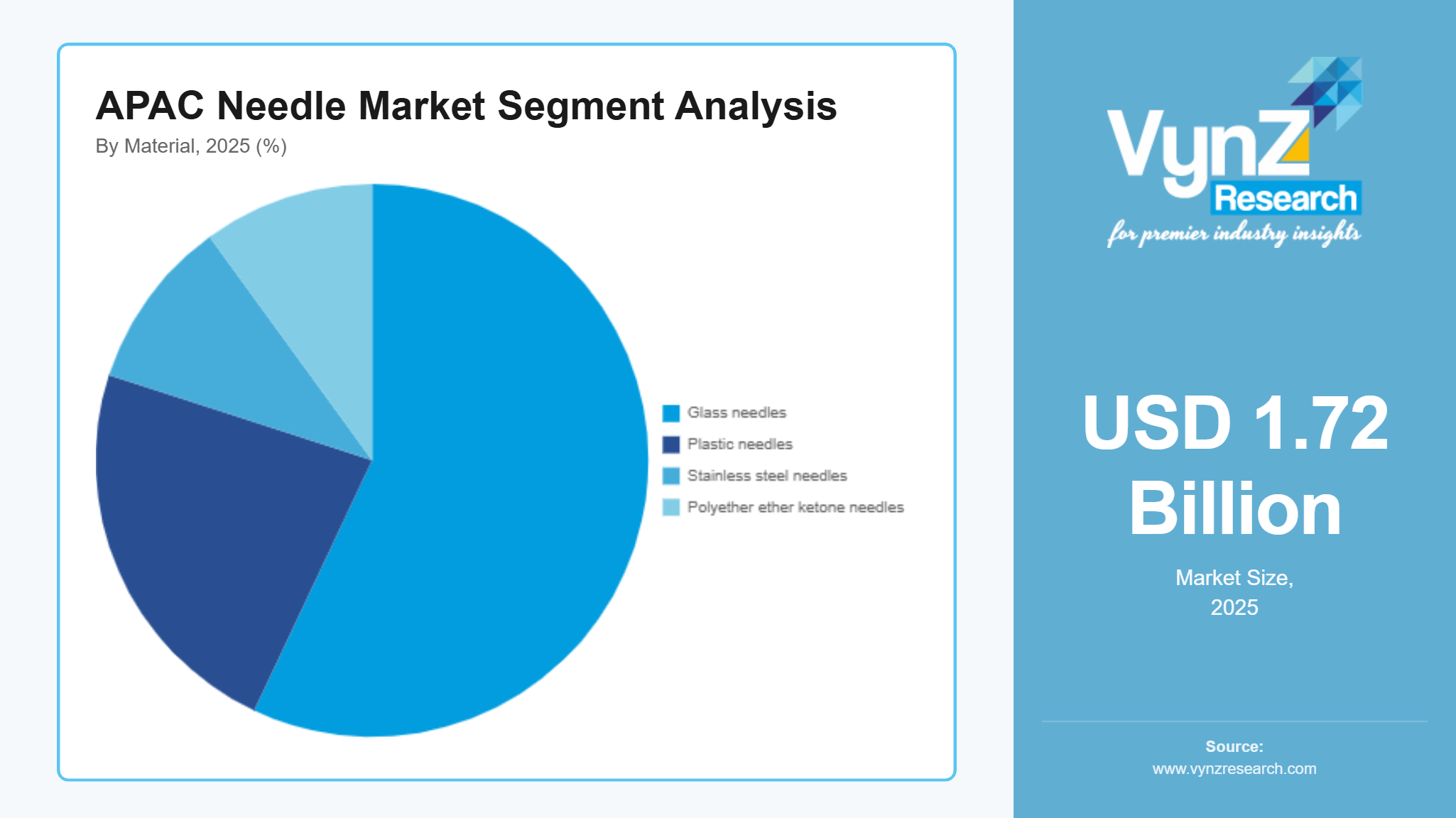

By Material

Stainless steel-based needles accounted for the largest share in 2025, representing approximately 57% of total segment revenue. The medical field widely uses this product because it provides strong performance and cost efficiency while supporting multiple medical applications. The medical industry demands compliance with regulatory standards which mandates safe operations of medical materials throughout all healthcare facilities. The increasing demand for reliable injection devices together with growing procedural volumes supports their continued use in hospitals and clinics.

The market for needle products which use advanced polymer and specialty materials expects to grow the most from 2026 to 2035 with a projected CAGR of 8.7%. The market expands because medical device manufacturers create new lightweight products which can be used safely by users. The market for alternative materials which improve patient comfort and decrease cross contamination risks keeps expanding. The segment growth receives support from research and development investments which focus on advanced medical consumable development.

By End User

The largest market segment in 2025 which generated 52% of total market revenue belongs to hospitals. The organization maintains its market lead because medical facilities experience heavy patient traffic and more surgeries take place together with vaccination programs. The Asia Pacific region experiences increased demand for healthcare services because governments are building new hospitals and healthcare facilities. The institutional sector shows higher adoption rates because global health organizations advocate for safe injection methods and standardized medical treatment procedures.

The home healthcare and diagnostic center market will grow the fastest which will reach a CAGR of 9.2% from 2026 to 2035. Home-based treatment and self-administration become more popular among patients who suffer from diabetes and other chronic illnesses which drives market expansion. The government push for expanded diagnostic networks and preventive healthcare programs leads to higher market demand. The emerging user segments show better product adoption rates because improvements to product accessibility and user experience continue to grow.

Regional Insights

China

The market saw China capture 34% of its market share in 2025 because the country had a vast patient population and developed its healthcare system and conducted numerous vaccination and diagnostic tests. The major cities of Beijing, Shanghai and Guangzhou maintain strong hospital and public health facility needs throughout their hospitals and public health emergencies. The World Health Organization report shows that the country has complete immunization coverage with multiple chronic disease treatment programs which results in continuous demand for injection devices.

India

India is estimated to hold approximately 22% of the market in 2025, supported by increasing healthcare access, rising burden of chronic diseases, and expanding immunization initiatives. The hospitals and clinics and diagnostic centers of Delhi, Mumbai and Bengaluru experience strong demand from key cities in their regions. According to data from global health agencies, the country continues to experience a growing prevalence of diabetes and infectious diseases, driving sustained need for injectable therapies.

Japan

Japan held about 14% of the APAC needle market in 2025 because its advanced healthcare system, aging population and medical technology use drive market growth. The established hospital systems of Tokyo and Osaka drive ongoing medical facility requirements through their hospital networks. Public health authorities report that the medical system needs constant end-user injection device usage due to the growing number of elderly people who require daily medical services.

Rest of Asia Pacific

The market share of the Asia Pacific region which includes countries such as Thailand, Malaysia and Vietnam, reached 30% in 2025. The region experiences growth because its healthcare system advances and people become more aware of preventive health and they establish better vaccination access. International health organizations provide support to public health initiatives by promoting good injection practices and they increase medical supply purchasing.

Competitive Landscape / Company Insights

The market shows moderate competition because both global and regional companies operate in the market by developing new products and entering new markets. Companies are making more research and development and manufacturing investments to enhance their market strength. The World Health Organization guidelines which support safe injection practices create a framework for developing safety engineered products. The government procurement programs and public health initiatives throughout Asia Pacific create competitive challenges for companies who must adjust their products to comply with regulatory requirements and fulfill the needs of major healthcare facilities.

Mini Profiles

B. Braun Melsungen AG focuses on medical consumables and injection solutions, supported by strong global distribution networks, established brand recognition, and continuous investment in safety engineered needle technologies and healthcare partnerships.

Becton, Dickinson and Company operates in premium and mass healthcare segments, emphasizing product innovation, safety compliance, and high-performance injection devices across hospitals, laboratories, and public health programs.

Hindustan Syringes & Medical Devices Ltd leverages large scale local manufacturing and government supply partnerships to expand market presence, ensuring cost efficient production and strong penetration across vaccination and hospital networks.

Jiangsu Jichun Medical Devices Co Ltd focuses on cost competitive medical devices, supported by regional manufacturing strength, expanding export capabilities, and increasing participation in public healthcare procurement programs across Asia Pacific.

Nipro Corporation operates across diversified healthcare segments, emphasizing precision engineering, product reliability, and integrated medical solutions, supported by strong presence in hospital supply chains and growing investments in advanced injection technologies.

Key Players

- B. Braun Melsungen AG

- Becton, Dickinson and Company

- Hindustan Syringes & Medical Devices Ltd

- Jiangsu Jichun Medical Devices Co Ltd

- Kangmei Pharmaceutical Co Ltd

- Medtronic plc

- Nipro Corporation

- Retractable Technologies Inc.

- Shandong Weigao Group Medical Polymer Company Limited

- Terumo Corporation

Recent Developments

In February 2026, Retractable Technologies Inc. expanded its safety needle production capacity to address increasing global demand for injury prevention devices. The initiative supports compliance with international safe injection guidelines and hospital safety protocols.

In May 2025, Shandong Weigao Group Medical Polymer Company Limited enhanced its manufacturing facilities for medical consumables in China. This development strengthens supply capabilities for hospitals and supports growing domestic healthcare demand.

In March 2026, Jiangsu Jichun Medical Devices Co Ltd increased its export activities across Southeast Asia. The company is focusing on cost efficient needle products to expand its presence in emerging healthcare markets.

In July 2025, Kangmei Pharmaceutical Co Ltd expanded its medical supplies distribution network across regional healthcare institutions. The move aims to improve accessibility of essential medical consumables including injection devices.

In January 2026, Becton, Dickinson and Company expanded its manufacturing capacity for advanced injection devices in Asia to meet rising regional demand. The initiative supports large scale vaccination programs and adoption of safety engineered needles.

APAC Needle Market Coverage

Type Insight and Forecast 2026 - 2035

- Conventional needles

- Safety needles

- Bevel needles

- Blunt fill needles

- Filter needles

- Vented needles

- Active needles

- Passive needles

Product Insight and Forecast 2026 - 2035

- Suture needles

- Blood collection needles

- Ophthalmic needles

- Dental needles

- Insufflation needles

- Pen needles

- Others

Delivery Mode Insight and Forecast 2026 - 2035

- Hypodermic needles

- Intravenous needles

- Intramuscular needles

- Intraperitoneal needles

Material Insight and Forecast 2026 - 2035

- Glass needles

- Plastic needles

- Stainless steel needles

- Polyether ether ketone needles

End User Insight and Forecast 2026 - 2035

- Hospitals

- Diagnostic centers

- Home healthcare

- Others

APAC Needle Market by Region

- China

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- Japan

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- India

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- South Korea

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- Vietnam

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- Thailand

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- Malaysia

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

- Rest of Asia-Pacific

- By Type

- By Product

- By Delivery Mode

- By Material

- By End User

Table of Contents for APAC Needle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Product

1.2.3. By

Delivery Mode

1.2.4. By

Material

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. APAC Market Estimate and Forecast

4.1. APAC Market Overview

4.2. APAC Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Conventional needles

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Safety needles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Bevel needles

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Blunt fill needles

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Filter needles

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Vented needles

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.1.7. Active needles

5.1.7.1. Market Definition

5.1.7.2. Market Estimation and Forecast to 2035

5.1.8. Passive needles

5.1.8.1. Market Definition

5.1.8.2. Market Estimation and Forecast to 2035

5.2. By Product

5.2.1. Suture needles

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Blood collection needles

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Ophthalmic needles

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Dental needles

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Insufflation needles

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Pen needles

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.2.7. Others

5.2.7.1. Market Definition

5.2.7.2. Market Estimation and Forecast to 2035

5.3. By Delivery Mode

5.3.1. Hypodermic needles

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Intravenous needles

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Intramuscular needles

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Intraperitoneal needles

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Material

5.4.1. Glass needles

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Plastic needles

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Stainless steel needles

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Polyether ether ketone needles

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Hospitals

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Diagnostic centers

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Home healthcare

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Others

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Type

6.2. By

Product

6.3. By

Delivery Mode

6.4. By

Material

6.5. By

End User

7. Japan Market Estimate and Forecast

7.1. By

Type

7.2. By

Product

7.3. By

Delivery Mode

7.4. By

Material

7.5. By

End User

8. India Market Estimate and Forecast

8.1. By

Type

8.2. By

Product

8.3. By

Delivery Mode

8.4. By

Material

8.5. By

End User

9. South Korea Market Estimate and Forecast

9.1. By

Type

9.2. By

Product

9.3. By

Delivery Mode

9.4. By

Material

9.5. By

End User

10. Vietnam Market Estimate and Forecast

10.1. By

Type

10.2. By

Product

10.3. By

Delivery Mode

10.4. By

Material

10.5. By

End User

11. Thailand Market Estimate and Forecast

11.1. By

Type

11.2. By

Product

11.3. By

Delivery Mode

11.4. By

Material

11.5. By

End User

12. Malaysia Market Estimate and Forecast

12.1. By

Type

12.2. By

Product

12.3. By

Delivery Mode

12.4. By

Material

12.5. By

End User

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Type

13.2. By

Product

13.3. By

Delivery Mode

13.4. By

Material

13.5. By

End User

14. Company Profiles

14.1.

B. Braun Melsungen AG

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Becton, Dickinson and Company

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Hindustan Syringes & Medical Devices Ltd

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

Jiangsu Jichun Medical Devices Co Ltd

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

Kangmei Pharmaceutical Co Ltd

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Medtronic plc

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Nipro Corporation

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Retractable Technologies Inc.

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Shandong Weigao Group Medical Polymer Company Limited

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

Terumo Corporation

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

APAC Needle Market