North America Needle Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Type (Conventional Needles, Safety Needles), by Product (Hypodermic Needles, Suture Needles, Blood Collection Needles, Pen Needles, Dental Needles, Others), by Material (Stainless Steel, Plastic, Glass, Others), by Delivery Mode (Disposable Needles, Reusable Needles), by End User (Hospitals and Clinics, Diagnostic Centers, Home Healthcare, Ambulatory Surgical Centers, Others)

| Status : Published | Published On : Jul, 2026 | Report Code : VRHC1345 | Industry : Healthcare | Available Format :

|

Page : 132 |

North America Needle Market Overview

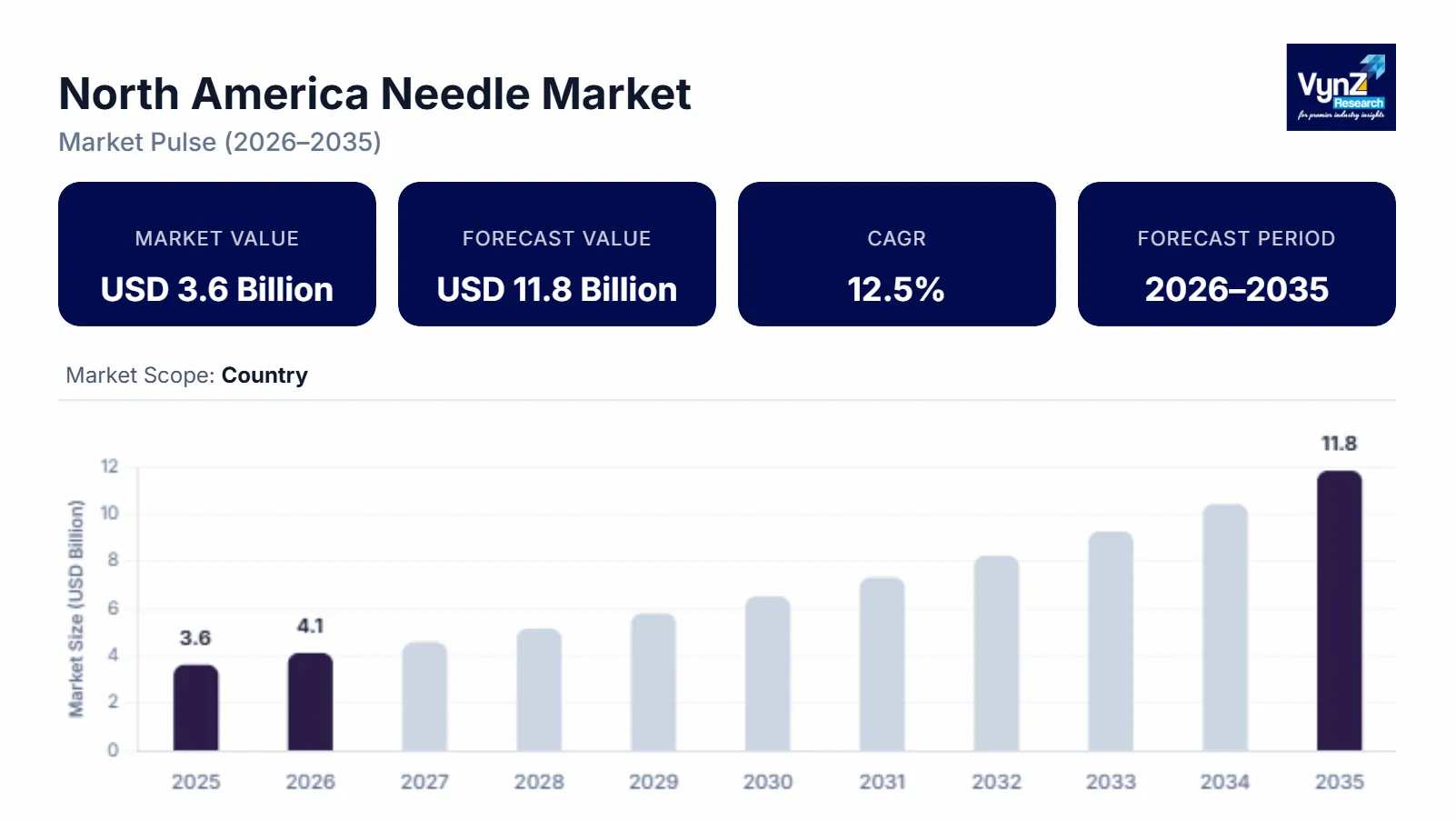

The North America needle market size was estimated at about USD 3.6 billion in 2025 and is expected to reach around USD 4.1 billion in 2026, rising up to roughly USD 11.8 billion by 2035, growing at approximately 12.5% CAGR from 2026 to 2035.

Research Highlights

- Conventional needles held 61.8% market share in 2025 supported by widespread use across healthcare facilities.

- Hypodermic needles captured 38.9% share in 2025 due to increasing vaccination and injectable therapies.

- Disposable needles accounted for 82.6% market share in 2025 owing to stringent infection prevention protocols.

- Home healthcare is projected to expand at 13.8% CAGR during 2026 to 2035 because of growing self-injection therapies.

- The United States represented 62% market share in 2025 supported by advanced healthcare infrastructure and immunization programs.

Market growth is supported by the growing prevalence of chronic diseases, increasing vaccination and immunization programs and growing demand for minimally invasive medical procedures along with increasing adoption of safety engineered needles. Increasing demand from hospitals, diagnostic centers and home healthcare settings along with ongoing investments in healthcare infrastructure and immunization initiatives by the U.S. Centers for Disease Control and Prevention (CDC), the U.S. Food and Drug Administration (FDA) and Health Canada are further supporting market expansion across major regions including California, Texas, and Ontario.

North America Needle Market Dynamics

Market Trends

The industry is witnessing notable shifts in safety engineered medical devices advanced injection technologies and infection prevention practices. One of the key trends shaping the market is the increasing adoption of safety needles, reflecting growing emphasis on healthcare worker protection, regulatory compliance, and reduction of needlestick injuries. The U.S. Occupational Safety and Health Administration (OSHA) and the U.S. Centers for Disease Control and Prevention (CDC) continue to recommend safer needle technologies to improve workplace safety across healthcare facilities.

Growth Drivers

The growth of the market is largely supported by the increasing prevalence of chronic diseases which continues to generate consistent demand across hospitals, clinics, ambulatory surgical centers and home healthcare settings. Increasing investments in healthcare infrastructure, immunization programs and injectable therapeutics are further accelerating market expansion. The CDC continues to recommend vaccination across multiple population groups, while the National Institutes of Health (NIH) supports research on injectable therapies for chronic diseases.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit its expansion. Stringent regulatory requirements, increasing raw material costs and product approval complexities continue to affect profitability and market entry particularly for smaller manufacturers. The FDA maintains rigorous quality and manufacturing standards for medical devices, increasing compliance requirements across the industry.

Market Opportunities

The market presents significant opportunities in safety engineered needles particularly driven by expanding healthcare regulations, growing occupational safety awareness and increasing demand for infection prevention. Companies offering advanced, reliable, and high-performance needle technologies are well positioned to capture incremental demand from hospitals, outpatient facilities, and diagnostic centers. The CDC and OSHA continue to encourage the adoption of safer injection devices to reduce occupational exposure.

North America Needle Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.6 Billion |

|

Revenue Forecast in 2035 |

USD 11.8 Billion |

|

Growth Rate |

12.5% |

|

Segments Covered in the Report |

By Type, By Product, By Material, By Delivery Mode, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

United States, Canada, Mexico, Rest of North America |

|

Key Companies |

B. Braun Medical Inc., Becton, Dickinson and Company (BD), Cardinal Health Inc., Henry Schein Inc., Hologic Inc., ICU Medical Inc., Medtronic plc, MTD Group, Nipro Medical Corporation, Retractable Technologies Inc. |

|

Customization |

Available upon request |

North America Needle Market Segmentation

By Type

Conventional needles accounted for the largest market share of approximately 61.8% in 2025 and are expected to grow at an estimated 11.9% CAGR through 2035 supported by widespread use in hospitals, diagnostic laboratories, vaccination programs and routine clinical procedures where cost effectiveness and broad availability remain important purchasing factors.

Safety needles are projected to register the fastest growth expanding at an estimated 13.6% CAGR during the forecast period due to increasing emphasis on reducing needlestick injuries, improving occupational safety and complying with healthcare regulations continues to accelerate adoption.

By Product

Hypodermic needles held the largest market share of approximately 38.9% in 2025 and are projected to expand at an estimated 12.4% CAGR through 2035 due to their extensive use in injectable drug administration, vaccination programs and diagnostic procedures continues to support market leadership.

Pen needles are expected to witness the fastest growth advancing at an estimated 13.5% CAGR during the forecast period owing to increasing prevalence of diabetes, self-administration of insulin and home healthcare services continue to strengthen adoption.

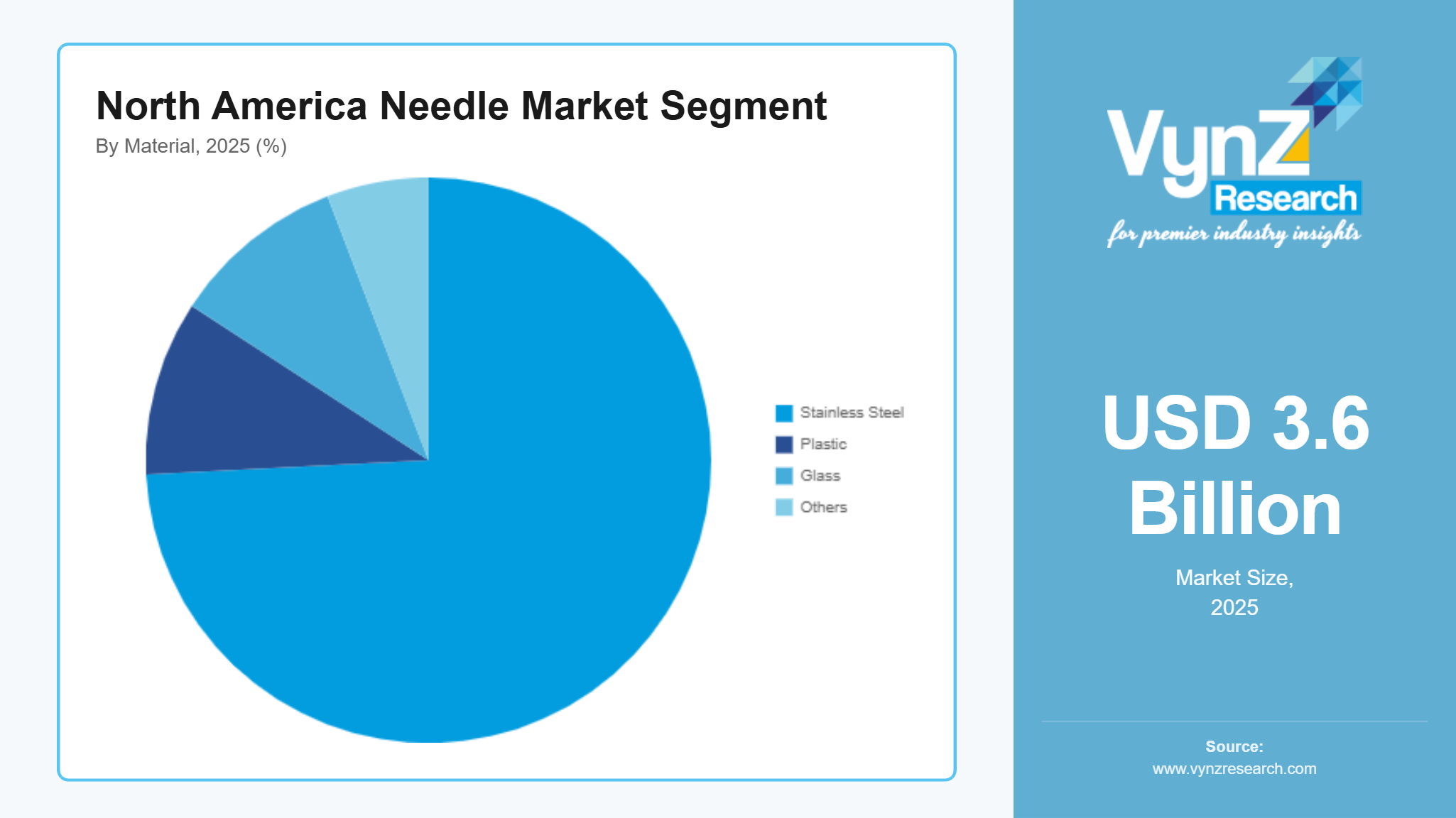

By Material

Stainless steel accounted for the largest market share of approximately 74.2% in 2025 and is anticipated to grow at nearly 12.2% CAGR through 2035 due to its superior strength, corrosion resistance, biocompatibility and precision manufacturing making it the preferred material for medical needles across healthcare applications.

Plastic based needle components are expected to register the fastest growth, recording an estimated 13.1% CAGR during the forecast period for the growing demand for lightweight medical devices, disposable products and improved manufacturing efficiency.

By Delivery Mode

Disposable needles dominated the market with approximately 82.6% share in 2025 and are projected to grow at an estimated 12.6% CAGR during the forecast period because of their widespread adoption. Growth is also supported by infection prevention protocols, single use healthcare practices, and strict regulatory compliance across hospitals and outpatient facilities.

Reusable needles are expected to record steady growth at an estimated 10.8% CAGR through 2035 supported by specialized clinical applications and controlled healthcare environments. Improvements in sterilization procedures and material durability continue to support limited adoption in selected medical settings.

By End User

Hospitals and clinics accounted for the largest market share of approximately 54.6% in 2025 and are expected to expand at an estimated 12.3% CAGR through 2035 owing to high patient volumes, increasing surgical procedures, routine vaccinations and chronic disease management.

Home healthcare is projected to register the fastest growth advancing at an estimated 13.8% CAGR during the forecast period for the growing adoption of self-injectable therapies, increasing elderly populations and expanding treatment of chronic diseases outside hospitals.

Regional Insights

United States

The United States accounted for approximately 62% of the market in 2025, driven by advanced healthcare infrastructure, high surgical volumes and increasing demand for injectable therapies. Strong demand from California, Texas, Florida, and New York continues to support market growth. The Centers for Disease Control and Prevention (CDC) continues to expand adult and childhood immunization programs while the U.S. Food and Drug Administration (FDA) regulates medical needle safety and quality supporting sustained market demand.

Canada

Canada represented nearly 14% of the market in 2025 and is projected to grow at an estimated 12.7% CAGR through 2035 as it is witnessing steady growth due to increasing healthcare expenditure, expanding vaccination programs and growing demand for injectable therapies. Health Canada continues to regulate medical devices and support access to safe healthcare products while the Public Health Agency of Canada (PHAC) promotes national immunization initiatives that sustain needle demand across hospitals and community healthcare settings.

Mexico

Mexico accounted for approximately 5% of the regional market in 2025 and is expected to register an estimated 13.1% CAGR during the forecast period supported by expanding healthcare infrastructure, increasing public immunization coverage and growing treatment of chronic diseases through injectable medications. The Federal Commission for the Protection against Sanitary Risks (COFEPRIS) continues strengthening medical device regulation while the Ministry of Health of Mexico supports nationwide vaccination and healthcare modernization programs.

Rest of North America

The Rest of North America accounted for approximately 19% of the market in 2025 and is projected to grow at an estimated 11.8% CAGR through 2035 owing to improving healthcare accessibility, increasing use of disposable medical devices and continued investments in public health infrastructure. Regional health authorities continue promoting infection prevention, safe injection practices and expanded immunization coverage across healthcare systems.

Competitive Landscape / Company Insights

The market is highly competitive with global and regional manufacturers focusing on product innovation, safety engineered needle technologies, manufacturing expansion and strategic partnerships to strengthen their market position. Companies are increasingly investing in research and development, advanced drug delivery solutions and regulatory compliance to enhance competitiveness. The U.S. Food and Drug Administration (FDA), the Centers for Disease Control and Prevention (CDC), and Health Canada continue to support high quality medical devices, safe injection practices and innovation through regulatory oversight and public health initiatives.

Mini Profiles

B. Braun Medical Inc. focuses on injection therapy products, safety needles, and infusion solutions, supported by strong manufacturing capabilities, broad healthcare distribution networks, and continuous product innovation.

Cardinal Health Inc. operates in the mass healthcare supplies segment, emphasizing dependable medical products, supply chain efficiency, and extensive distribution services for hospitals and clinical facilities.

Henry Schein Inc. leverages its extensive distribution network and digital procurement capabilities to expand market presence, supplying needles and medical consumables to healthcare professionals across North America.

ICU Medical Inc. specializes in infusion therapy systems, needle technologies, and vascular access products, supported by advanced engineering expertise and strong relationships with healthcare providers.

Medtronic plc develops innovative medical technologies and specialized injection solutions, supported by global research capabilities, established brand recognition, and continuous investments in healthcare innovation.

Key Players

- B. Braun Medical Inc.

- Becton, Dickinson and Company (BD)

- Cardinal Health Inc.

- Henry Schein Inc.

- Hologic Inc.

- ICU Medical Inc.

- Medtronic plc

- MTD Group

- Nipro

- Medical Corporation

- Retractable Technologies Inc.

Recent Developments

In January 2025, Becton, Dickinson and Company (BD) received expanded regulatory clearance for advanced injection and drug delivery technologies designed to improve patient safety and clinical efficiency. The development strengthened the company's portfolio supporting injectable therapies and hospital care.

In March 2025, Smiths Medical introduced enhancements to its vascular access and infusion product portfolio, focusing on improved clinician safety and workflow efficiency. The expansion reinforced its presence in acute care and specialty healthcare settings.

In May 2025, Nipro Medical Corporation expanded production capacity for injectable medical devices to address growing regional demand for needles and drug delivery products. The investment strengthened supply reliability for hospitals and healthcare providers across North America.

In September 2025, Hologic Inc. expanded manufacturing capabilities for women's health diagnostic products requiring precision sampling and medical device components. The initiative supported increasing demand from healthcare facilities while improving production efficiency.

In February 2026, Retractable Technologies Inc. enhanced its safety needle portfolio with product improvements designed to reduce occupational needlestick injuries and improve regulatory compliance. The development supported growing adoption of safety engineered devices across hospitals and outpatient healthcare facilities.

North America Needle Market Coverage

Type Insight and Forecast 2026 - 2035

- Conventional Needles

- Safety Needles

Product Insight and Forecast 2026 - 2035

- Hypodermic Needles

- Suture Needles

- Blood Collection Needles

- Pen Needles

- Dental Needles

- Others

Material Insight and Forecast 2026 - 2035

- Stainless Steel

- Plastic

- Glass

- Others

Delivery Mode Insight and Forecast 2026 - 2035

- Disposable Needles

- Reusable Needles

End User Insight and Forecast 2026 - 2035

- Hospitals and Clinics

- Diagnostic Centers

- Home Healthcare

- Ambulatory Surgical Centers

- Others

North America Needle Market by Region

- U.S.

- By Type

- By Product

- By Material

- By Delivery Mode

- By End User

- Canada

- By Type

- By Product

- By Material

- By Delivery Mode

- By End User

- Mexico

- By Type

- By Product

- By Material

- By Delivery Mode

- By End User

Table of Contents for North America Needle Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Type

1.2.2. By

Product

1.2.3. By

Material

1.2.4. By

Delivery Mode

1.2.5. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. North Market Estimate and Forecast

4.1. North Market Overview

4.2. North Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Type

5.1.1. Conventional Needles

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Safety Needles

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Product

5.2.1. Hypodermic Needles

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Suture Needles

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Blood Collection Needles

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Pen Needles

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Dental Needles

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Others

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Material

5.3.1. Stainless Steel

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Plastic

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Glass

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Others

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By Delivery Mode

5.4.1. Disposable Needles

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Reusable Needles

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.5. By End User

5.5.1. Hospitals and Clinics

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Diagnostic Centers

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Home Healthcare

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Ambulatory Surgical Centers

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Others

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

6. U.S. Market Estimate and Forecast

6.1. By

Type

6.2. By

Product

6.3. By

Material

6.4. By

Delivery Mode

6.5. By

End User

7. Canada Market Estimate and Forecast

7.1. By

Type

7.2. By

Product

7.3. By

Material

7.4. By

Delivery Mode

7.5. By

End User

8. Mexico Market Estimate and Forecast

8.1. By

Type

8.2. By

Product

8.3. By

Material

8.4. By

Delivery Mode

8.5. By

End User

9. Company Profiles

9.1.

B. Braun Medical Inc.

9.1.1.

Snapshot

9.1.2.

Overview

9.1.3.

Offerings

9.1.4.

Financial

Insight

9.1.5.

Recent

Developments

9.2.

Becton, Dickinson and Company (BD)

9.2.1.

Snapshot

9.2.2.

Overview

9.2.3.

Offerings

9.2.4.

Financial

Insight

9.2.5.

Recent

Developments

9.3.

Cardinal Health Inc.

9.3.1.

Snapshot

9.3.2.

Overview

9.3.3.

Offerings

9.3.4.

Financial

Insight

9.3.5.

Recent

Developments

9.4.

Henry Schein Inc.

9.4.1.

Snapshot

9.4.2.

Overview

9.4.3.

Offerings

9.4.4.

Financial

Insight

9.4.5.

Recent

Developments

9.5.

Hologic Inc.

9.5.1.

Snapshot

9.5.2.

Overview

9.5.3.

Offerings

9.5.4.

Financial

Insight

9.5.5.

Recent

Developments

9.6.

ICU Medical Inc.

9.6.1.

Snapshot

9.6.2.

Overview

9.6.3.

Offerings

9.6.4.

Financial

Insight

9.6.5.

Recent

Developments

9.7.

Medtronic plc

9.7.1.

Snapshot

9.7.2.

Overview

9.7.3.

Offerings

9.7.4.

Financial

Insight

9.7.5.

Recent

Developments

9.8.

MTD Group

9.8.1.

Snapshot

9.8.2.

Overview

9.8.3.

Offerings

9.8.4.

Financial

Insight

9.8.5.

Recent

Developments

9.9.

Nipro Medical Corporation

9.9.1.

Snapshot

9.9.2.

Overview

9.9.3.

Offerings

9.9.4.

Financial

Insight

9.9.5.

Recent

Developments

9.10.

Retractable Technologies Inc.

9.10.1.

Snapshot

9.10.2.

Overview

9.10.3.

Offerings

9.10.4.

Financial

Insight

9.10.5.

Recent

Developments

10. Appendix

10.1. Exchange Rates

10.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

North America Needle Market