Europe Dental Implants Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product (Fixtures, Abutments, Crowns, Bridges, Dentures), by Material (Titanium, Zirconium, Ceramic), by Design (Tapered Implants, Parallel Walled Implants), by End User (Dental Hospitals, Dental Clinics, Dental Laboratories, Academic and Research Institutes)

| Status : Published | Published On : May, 2026 | Report Code : VRHC1341 | Industry : Healthcare | Available Format :

|

Page : 122 |

Europe Dental Implants Market Overview

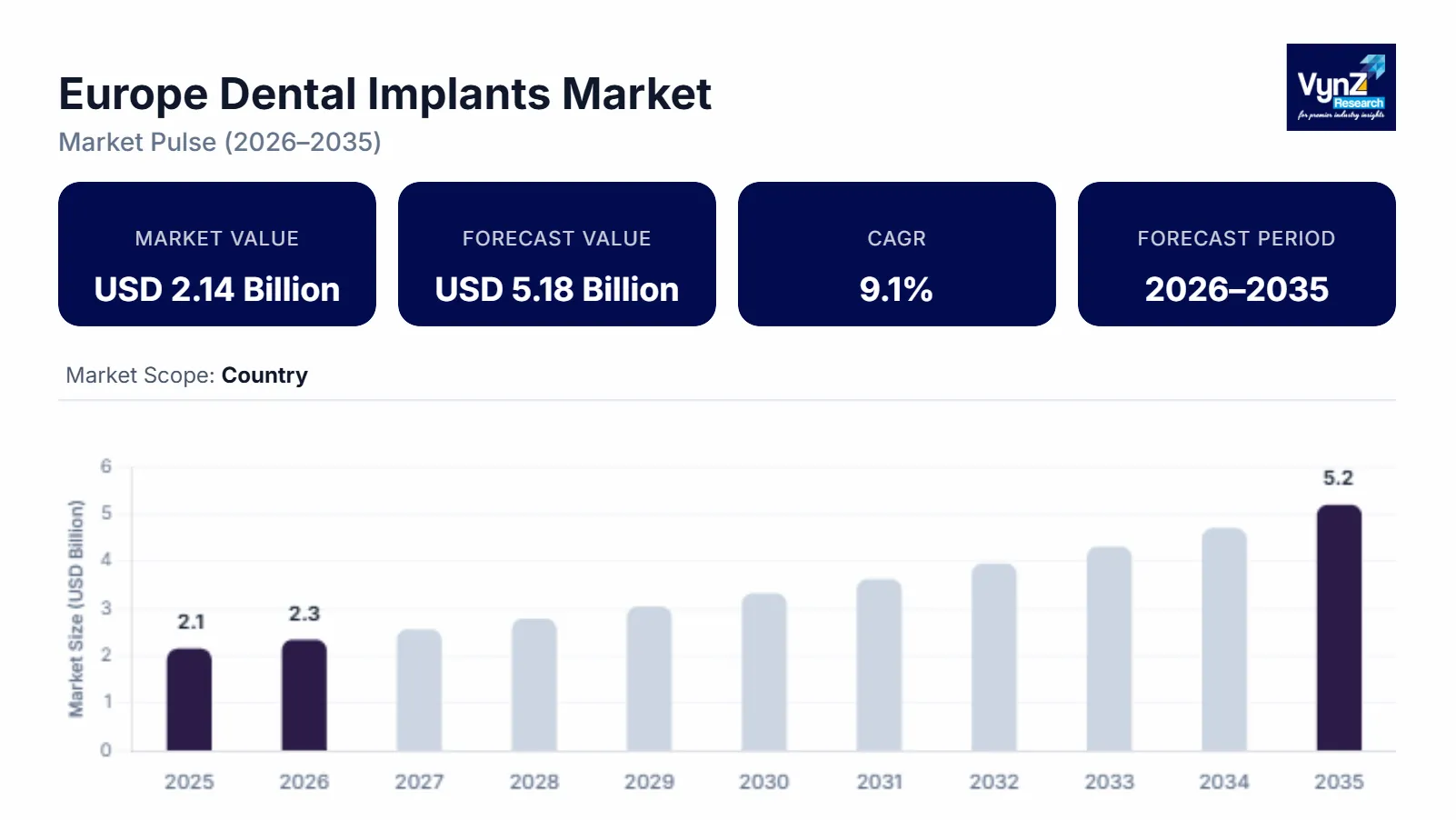

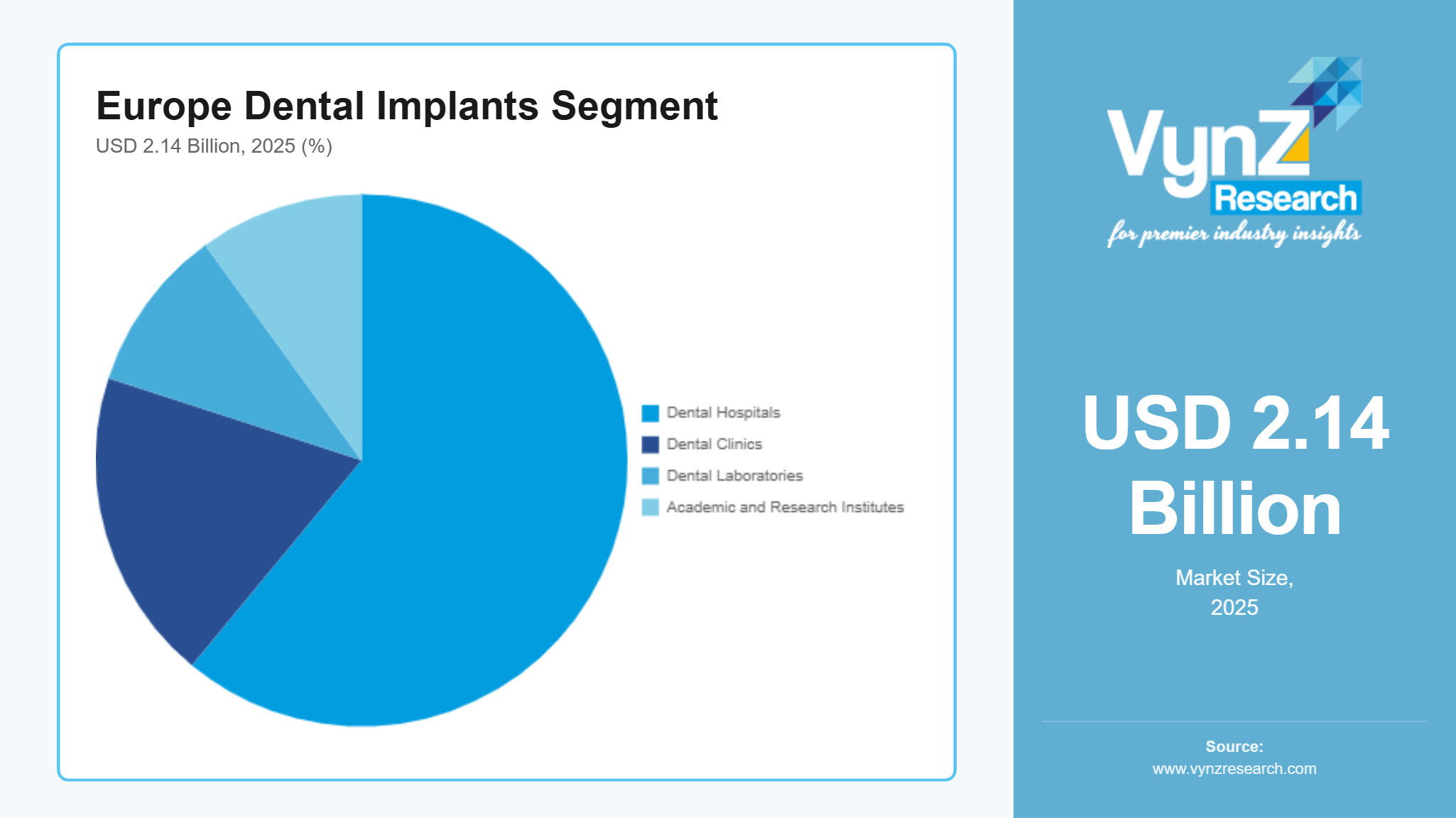

The Europe dental implants market size was estimated at about USD 2.14 billion in 2025 and is expected to reach around USD 2.31 billion in 2026, rising up to roughly USD 5.18 billion by 2035, growing at approximately 9.1% CAGR from 2026 to 2035.

Research Highlights

- Fixtures led 2025 revenue with 51% share due to rising adoption of permanent restorative solutions.

- Titanium implants captured 56% market share in 2025 due to superior biocompatibility and durability benefits.

- Germany dominated 2025 with 24% market share due to advanced dental infrastructure and growing digital dentistry technology adoption.

- Abutments will grow fastest at 8.1% CAGR due to rising demand for customized restorative solutions.

- Zirconium implants will expand at 8.4% CAGR driven by aesthetic preferences and ceramic technology advancements.

Market growth is driven by growing prevalence of tooth loss and periodontal disorders, more people adopting digital dentistry technologies, and higher demand for minimally invasive restorative procedures. Integration of CAD/CAM guided implant systems and advanced surface treatment technologies is creating long-term demand for aesthetically pleasing dental restoration solutions. Growing investments in infrastructure and reimbursement systems are pushing the market in Germany, the U.K., and France.

WHO reports rising cases of edentulism and untreated dental conditions among elders increase demand for advanced restorative treatments across Europe. Public healthcare initiatives and reimbursement support programs are encouraging broader adoption of implant procedures. The National Health Service in the U.K. and various European public oral healthcare programs are making implant procedures more mainstream and increasing investments in digital imaging systems, guided implant surgery, and preventive oral healthcare infrastructure are making commercialization chances stronger across hospitals, specialty clinics, and dental laboratories throughout the region.

Europe Dental Implants Market Dynamics

Market Trends

The industry is moving toward minimally invasive approaches as people demand for restorative solutions with more precision. Oral healthcare modernization efforts, frameworks from the World Health Organization, various European oral healthcare authorities and national dental wellness programs prioritizes prevention, procedural standardization, and results. Lots of clinics are adopting CAD/CAM enabled implant systems, 3D printed surgical guides, and digital imaging tools that support procedural accuracy and better osseointegration results. Hospitals and specialty clinics are increasingly using guided surgery systems, intraoral scanners, and computer assisted treatment planning tools for a better workflow and higher clinical accuracy.

Growth Drivers

The growth in the market is drive by rising tooth loss, periodontal disease, and age-related dental issues. The growing elderly population choose permanent restorative approaches more often. WHO prioritizes the development of implant materials, surface treatments and invasive surgical methods. This helps clinics, specialty centers and dental laboratories get better outcomes. Higher investment in dental healthcare infrastructure, digital dentistry and preventive care programs pushes the growth across Germany, France and the U.K market. Access is easier now because reimbursement support from public healthcare systems has improved, which helps the middle-income patient group in particular. Adoption is higher for advanced dentistry and people are becoming more aware of the long-term benefits of dental rehabilitation which keeps moving the market forward.

Market Restraints / Challenges

Even with encouraging growth, the market still has a few issues. The biggest ones include high procedure costs, complicated regulatory compliance, and not enough accessibility for cost sensitive patient groups. Advanced implant procedures need major investment, like surgical gear, digital imaging systems, CAD/CAM software platforms, and training programs for professionals, increases operating expenses for hospitals and clinics. European public healthcare authority reports also suggest that reimbursement limits and uneven access to specialized dental care are slowing implant adoption in several emerging and rural areas. European medical device regulations and clinical safety approvals create longer commercialization timelines for manufacturers, dependence on imported titanium, zirconium and other advanced dental biomaterials expose suppliers to raw material price swings and supply chain interruptions causing pricing issues and lower procedural accessibility.

Market Opportunities

Opportunities lie in digitally enabled restorative dentistry, premium implant systems, and customized aesthetic rehabilitation solutions that fit the healthcare modernization and meet the rising demand for minimally invasive procedures. Personalized treatment planning is pushing adoption of AI assisted diagnostics, robotic guided implant placement, and more automated digital workflow systems. Firms that can offer high performance implant solutions with stronger osseointegration abilities and restorations that can be customized are positioned well to gain more business from urban specialty clinics and higher income patient groups.

Europe Dental Implants Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.14 Billion |

|

Revenue Forecast in 2035 |

USD 5.18 Billion |

|

Growth Rate |

9.1% |

|

Segments Covered in the Report |

Product, Material, Design, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, U.K., France, Italy, Rest of Europe |

|

Key Companies |

3M Company, BioHorizons Inc., Dentsply Sirona Inc., Institut Straumann AG, MegaGen Implant Co. Ltd., Nobel Biocare Services AG, Osstem Implant Co. Ltd., Southern Implants, Zimmer Biomet Holdings Inc., ZimVie Inc. |

|

Customization |

Available upon request |

Europe Dental Implants Market Segmentation

By Product

In 2025, fixtures accounted for about 51% of total revenue due to higher adoption by clinicians and dependability. Higher demand for permanent restorative solutions and higher compliance requirements of the European Medicines Agency is pushing hospitals and dental clinics toward high-quality implant fixtures for better osseointegration results.

Abutments will be the quickest to grow through 2026 to 2035 with an estimated CAGR of 8.1% because customized prosthetic solutions will be used extensively and CAD/CAM restorative configurations will become the new standard.

By Material

In 2025, titanium implants held the biggest share of the market share with about 56% of the whole revenue mostly because of solid biocompatibility, long term structural steadiness, and consistent clinical success outcomes in restorative dentistry settings. Regulatory direction from European dental organizations and the persistence of public oral healthcare programs keeps reinforcing adoption of titanium implant systems in hospitals, clinics, and academic institutions. Zirconium implants would record the fastest growth from 2026 to 2035 with a projected CAGR of 8.4% due to stronger demand for metal free restorative choices, a noticeable shift in patient preference toward aesthetics, and steady progress in ceramic implant engineering.

By Design

Tapered implants held the largest share of the market in 2025 at roughly 53% of revenue due to procedural familiarity, dependable insertion stability, and good compatibility with direct loading protocols, which are common in advanced restorative workflows. Parallel walled implants are anticipated to grow fastest across the forecast period, reaching an estimated CAGR of 7.9% from 2026 to 2035 due to deeper integration of precision guided treatment planning systems and improvements in implant geometry that helps strengthen osseointegration and supports long run functional stability.

By End User

Dental hospitals and clinics were the largest segment in 2025, accounting for about 61% of total market revenue due to higher patient inflow for restorative procedures, expansion of specialized implantology services and more spending on advanced oral healthcare infrastructure. Public healthcare programs that highlight oral health awareness, preventive dental care, and reimbursement backing are also pushing implant adoption across hospital and clinic networks throughout Europe.

Dental laboratories and academic and research institutes are expected to expand faster over the forecast period with an estimated CAGR of 7.6% from 2026 to 2035 driven by demand for customized prosthetic engineering, faster acceptance of digital workflow technologies and broader dental research initiatives focused on implant innovation.

Regional Insights

Germany

Germany held around 24% of the market in 2025, mostly because of pretty advanced dental healthcare infrastructure, a more frequent use of digital dentistry instruments, and a noticeable uptick incidence of tooth loss among the aging population. Big city hubs like Berlin, Munich and Hamburg have a high demand for implant-based procedures across hospitals, private clinics and specialized restorative centers. Regulatory direction that is backed by the Federal Ministry of Health and European dental safety frameworks is also pushing the use of high precision implant systems and these less invasive restorative routes.

The U.K.

The U.K. represented roughly 18% of the market in 2025, largely due to stronger public awareness regarding oral health, a heavier lean toward cosmetic dentistry, and continued expansion of private dental care setups across cities like London, Birmingham, and Manchester. Guidance from the National Health Service, combined with oral health promotion activities, keeps supporting preventive dental care, as well as restorative treatment uptake across public and private care networks. More routine use of digital treatment planning platforms, intraoral scanning technologies, and guided implant placement is speeding up processes and improving patient experiences.

France

France held about 15% of the market in 2025, driven by stronger investment in modern dental infrastructure, more demand for aesthetic restorative procedures, and wider adoption of minimally invasive implant technologies across urban healthcare hubs. Cities like Paris, Lyon and Marseille are becoming more visible as key anchor points for advanced implant procedures and digital restorative dentistry services. Oral health programs supported by the French Ministry of Health are also raising awareness about preventive and restorative dental options. The market keeps getting another lift from adoption of ceramic implants, CAD/CAM restorative systems, and digitally supported implant planning tools.

Italy

Italy accounted for approximately 11% of the market in 2025, due to rising dental tourism, improved oral health awareness, and more investment into advanced restorative dentistry infrastructure. Major cities such as Milan, Rome and Turin keep showing higher demand for implant supported restorative procedures, especially through specialty clinics and private dental hospitals. Public oral healthcare campaigns, supported by government, together with preventive dental programs, are expanding awareness around long-term tooth replacement solutions and oral rehabilitation treatments. Wider adoption of digital imaging systems, guided surgery approaches, and customized implant prosthetics is enhancing procedure performance, and patient satisfaction across Italy.

Rest of Europe

The rest of Europe, which includes Spain, the Netherlands, Switzerland, Sweden, and several other regional economies, together represented about 18% of the market in 2025 supported by modernization of dental healthcare systems, a rising use of digital restorative technologies, and a growing preference for minimally invasive implant procedures. Efforts in public healthcare, along with oral wellness campaigns from regional health authorities, continue to push preventive dental care, and more advanced restorative treatment adoption in hospitals and specialty clinics. Expansion of private dental chains, a deeper integration of AI assisted treatment planning systems, and increasing investments in premium dental care services are also supporting market growth across the region. The remaining share is held by emerging European economies.

Competitive Landscape / Company Insights

The market is moderately competitive with multinational and regional manufacturers focusing implant innovation, digital dentistry and the expansion of premium restorative offerings across several major European economies. Many companies are investing heavily in R&D, CAD/CAM technologies, guided surgery systems, and creating strategic alliance to hold a stronger position in the market. Regulatory requirements and quality compliance structures of the European Medicines Agency and different regional health authorities are pushing technological progress, procedural standardization, and commercialization of advanced implant systems in hospitals, clinics, and various specialty dental centers.

Mini Profiles

3M Company focuses on restorative dental materials, implant related solutions, and digital dentistry technologies, supported by strong global distribution capabilities, recognized healthcare branding, and extensive research driven product development expertise.

BioHorizons Inc. operates in premium implant dentistry segments, emphasizing precision engineered implant systems, aesthetic restorative performance, and customized treatment solutions supported by advanced clinical integration capabilities.

Dentsply Sirona Inc. leverages digital dentistry technologies, integrated imaging systems, and strategic partnerships to strengthen market presence across implant planning, restorative workflows, and guided surgical treatment platforms.

Institut Straumann AG focuses on premium implant systems, biomaterials, and digital restorative solutions, supported by strong clinical research capabilities, global training networks, and advanced guided surgery technologies across Europe.

MegaGen Implant Co. Ltd. emphasizes innovative implant designs, digitally integrated restorative workflows, and expanding international distribution channels, supported by growing investments in aesthetic dentistry and precision implant manufacturing technologies.

Key Players

- 3M Company

- BioHorizons Inc.

- Dentsply Sirona Inc.

- Institut Straumann AG

- MegaGen Implant Co. Ltd.

- Nobel Biocare Services AG

- Osstem Implant Co. Ltd.

- Southern Implants

- Zimmer Biomet Holdings Inc.

- ZimVie Inc.

Recent Developments

In February 2025, Nobel Biocare Services AG expanded its digital workflow portfolio with advanced guided surgery and restorative planning solutions for implant dentistry applications across Europe. The company also strengthened focus on precision implant integration technologies designed to improve procedural efficiency and long-term restorative outcomes.

In April 2025, Osstem Implant Co. Ltd. increased investments in European dental education and digital implant training programs to support expansion of advanced restorative procedures. The company also introduced enhanced implant surface technologies aimed at improving osseointegration and clinical stability.

In June 2025, Southern Implants launched new premium implant solutions focused on complex restorative and immediate loading procedures across specialty dental clinics. The company continued expanding its digital treatment planning capabilities and customized implant offerings within the European market.

In January 2026, Zimmer Biomet Holdings Inc. strengthened its digital dentistry portfolio through expanded integration of guided surgery systems and implant planning technologies. The company also focused on improving minimally invasive restorative workflows across hospitals and specialty dental centers in Europe.

In March 2026, ZimVie Inc. expanded its implant biomaterial and restorative solutions portfolio to support digitally integrated dental treatment procedures. The company further increased focus on advanced CAD/CAM workflows and precision implant technologies aimed at improving clinical efficiency and patient outcomes.

Europe Dental Implants Market Coverage

Product Insight and Forecast 2026 - 2035

- Fixtures

- Abutments

- Crowns

- Bridges

- Dentures

Material Insight and Forecast 2026 - 2035

- Titanium

- Zirconium

- Ceramic

Design Insight and Forecast 2026 - 2035

- Tapered Implants

- Parallel Walled Implants

End User Insight and Forecast 2026 - 2035

- Dental Hospitals

- Dental Clinics

- Dental Laboratories

- Academic and Research Institutes

Europe Dental Implants Market by Region

- Germany

- By Product

- By Material

- By Design

- By End User

- U.K.

- By Product

- By Material

- By Design

- By End User

- France

- By Product

- By Material

- By Design

- By End User

- Italy

- By Product

- By Material

- By Design

- By End User

- Spain

- By Product

- By Material

- By Design

- By End User

- Russia

- By Product

- By Material

- By Design

- By End User

- Rest of Europe

- By Product

- By Material

- By Design

- By End User

Table of Contents for Europe Dental Implants Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product

1.2.2. By

Material

1.2.3. By

Design

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product

5.1.1. Fixtures

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Abutments

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Crowns

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Bridges

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Dentures

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.2. By Material

5.2.1. Titanium

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Zirconium

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Ceramic

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Design

5.3.1. Tapered Implants

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Parallel Walled Implants

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Dental Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Dental Clinics

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Dental Laboratories

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Academic and Research Institutes

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Product

6.2. By

Material

6.3. By

Design

6.4. By

End User

7. U.K. Market Estimate and Forecast

7.1. By

Product

7.2. By

Material

7.3. By

Design

7.4. By

End User

8. France Market Estimate and Forecast

8.1. By

Product

8.2. By

Material

8.3. By

Design

8.4. By

End User

9. Italy Market Estimate and Forecast

9.1. By

Product

9.2. By

Material

9.3. By

Design

9.4. By

End User

10. Spain Market Estimate and Forecast

10.1. By

Product

10.2. By

Material

10.3. By

Design

10.4. By

End User

11. Russia Market Estimate and Forecast

11.1. By

Product

11.2. By

Material

11.3. By

Design

11.4. By

End User

12. Rest of Europe Market Estimate and Forecast

12.1. By

Product

12.2. By

Material

12.3. By

Design

12.4. By

End User

13. Company Profiles

13.1.

3M Company

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

BioHorizons Inc.

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Dentsply Sirona Inc.

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Institut Straumann AG

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

MegaGen Implant Co. Ltd.

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Nobel Biocare Services AG

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Osstem Implant Co. Ltd.

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Southern Implants

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

Zimmer Biomet Holdings Inc.

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

ZimVie Inc.

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Dental Implants Market