Flow Cytometry Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Technology (Cell Based Flow Cytometry, Bead Based Flow Cytometry), by Product and Service (Instruments, Reagents and Consumables, Software, Accessories, Services), by Application (Research Applications, Clinical Diagnostics, Industrial Applications, Others), by End User (Hospitals, Clinical Testing Laboratories, Academic and Research Institutes, Pharmaceutical and Biotechnology Companies, Others)

| Status : Published | Published On : Jul, 2026 | Report Code : VRHC1345 | Industry : Healthcare | Available Format :

|

Page : 169 |

Flow Cytometry Market Overview

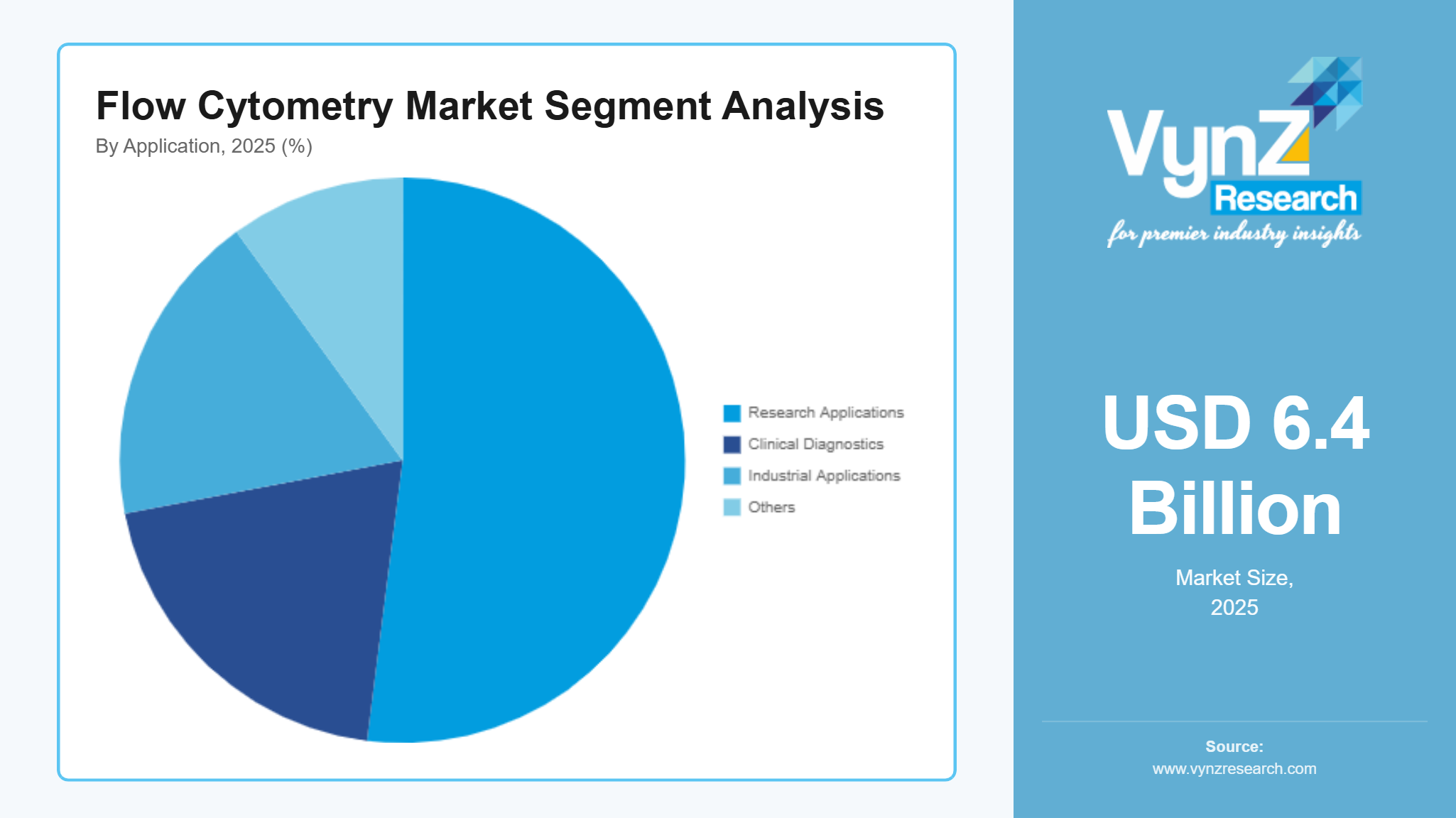

The flow cytometry market size was estimated at about USD 6.4 billion in 2025 and is expected to reach around USD 7.1 billion in 2026, rising up to roughly USD 18.9 billion by 2035, growing at approximately 11.5% CAGR from 2026 to 2035.

Research Highlights

- Cell based flow cytometry accounted for 72.4% market share in 2025 supported by extensive clinical and research applications.

- Reagents and consumables held 46.7% market share in 2025 due to recurring laboratory testing and research activities.

- Research applications captured 52.8% market share in 2025 owing to growing oncology and immunology research investments.

- Academic and research institutes are projected to expand at 12.5% CAGR during 2026 to 2035 because of increasing public research funding.

- North America represented 41.6% market share in 2025 supported by robust biomedical research funding and advanced healthcare infrastructure.

Market growth is fueled by increasing cancer and immunological disease research, expanding use of cell-based diagnostics and growing investments in life sciences research along with increasing adoption of high parameter and automated flow cytometry systems. Increasing demand for clinical diagnostics, drug discovery and biomarker analysis together with ongoing investments in biomedical research by the U.S. National Institutes of Health (NIH), the National Cancer Institute (NCI) and the European Commission's Horizon Europe program are further supporting market expansion across major regions including North America, Europe, and Asia Pacific.

Flow Cytometry Market Dynamics

Market Trends

The industry is witnessing notable shifts in high parameter cell analysis, laboratory automation and multiparametric research applications. One of the key trends shaping the market is the adoption of spectral flow cytometry reflecting increasing demand for higher analytical accuracy, improved workflow efficiency and comprehensive immune profiling. The U.S. National Institutes of Health (NIH) and the National Cancer Institute (NCI) continue supporting advanced cell analysis technologies through funding for biomedical and cancer research. Another emerging trend is the integration of artificial intelligence and automated data analysis into flow cytometry platforms, driven by technological innovation and increasing laboratory digitalization. The U.S. Food and Drug Administration (FDA) and the European Medicines Agency (EMA) continue supporting advanced diagnostic technologies through evolving regulatory frameworks.

Growth Drivers

The growth of the market is largely supported by increasing cancer research and immunology studies which continue to generate consistent demand across pharmaceutical companies, biotechnology firms, hospitals and academic research institutes. Growing investments in biomedical research infrastructure and precision medicine programs are further accelerating market expansion. The National Institutes of Health (NIH) and the National Cancer Institute (NCI) continue funding large scale research programs involving advanced cell analysis technologies. Additionally, expanding applications in clinical diagnostics and drug discovery are playing a crucial role in boosting adoption. As healthcare providers and life science organizations prioritize accurate disease detection and biomarker analysis, demand for advanced flow cytometry instruments and reagents is expected to remain strong throughout the forecast period.

Market Restraints / Challenges

Despite favorable growth prospects the market faces challenges that may limit its expansion. High instrument costs, complex regulatory requirements and expensive reagent procurement continue to affect affordability and market penetration particularly among smaller laboratories and research institutions. The FDA continues to maintain rigorous quality and performance standards for diagnostic devices used in clinical laboratories. Dependence on highly skilled laboratory personnel and specialized analytical software poses operational challenges for manufacturers and end users. Workforce shortages, complex data interpretation, and laboratory validation requirements can increase operational costs and slow technology adoption during periods of resource constraints.

Market Opportunities

The market presents significant opportunities in precision medicine and immunotherapy research particularly motivated by increasing investments in personalized healthcare and biomarker discovery. Companies offering advanced, automated, and high-performance flow cytometry platforms are well positioned to capture incremental demand from pharmaceutical companies, research institutes and clinical laboratories. The National Institutes of Health (NIH) continues expanding funding for precision medicine and translational research initiatives. Another key opportunity lies in cell and gene therapy development, where rising investments in specialized analytical technologies are creating opportunities for premium instrumentation and long term research partnerships. Advancements in automation, artificial intelligence, and high dimensional cell analysis are expected to improve laboratory productivity and research efficiency.

Global Flow Cytometry Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 6.4 Billion |

|

Revenue Forecast in 2035 |

USD 18.9 Billion |

|

Growth Rate |

11.5% |

|

Segments Covered in the Report |

By Technology, By Product and Service, By Application, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Agilent Technologies Inc., Becton, Dickinson and Company (BD), Bio-Rad Laboratories Inc., Cytek Biosciences Inc., Danaher Corporation, Merck KGaA, Miltenyi Biotec, Sony Biotechnology Inc., Sysmex Corporation, Thermo Fisher Scientific Inc. |

|

Customization |

Available upon request |

Flow Cytometry Market Segmentation

By Technology

Cell based flow cytometry accounted for the largest market share of approximately 72.4% in 2025 and is projected to expand at an estimated 11.2% CAGR through 2035 supported by extensive use in immunophenotyping, cancer diagnostics, stem cell research and clinical laboratory testing where high sensitivity and multiparametric analysis remain essential.

Bead based flow cytometry is expected to register the fastest growth advancing at an estimated 12.4% CAGR during the forecast period due to increasing adoption in multiplex assays, cytokine analysis and biomarker detection that is strengthening demand across pharmaceutical and biotechnology research.

By Product and Service

Reagents and consumables held the major market share of approximately 46.7% in 2025 and are expected to grow at an estimated 11.8% CAGR through 2035 due to continuous laboratory testing, recurring research activities and increasing clinical diagnostic procedures sustain consistent demand for antibodies, dyes, buffers, and assay kits.

Instruments are projected to witness the fastest growth recording an estimated 12.1% CAGR during the forecast period owing to increasing adoption of spectral flow cytometers, automated platforms and high throughput analytical systems is encouraging laboratories to modernize existing infrastructure.

By Application

Research applications accounted for the biggest market share of approximately 52.8% in 2025 and are projected to expand at nearly 11.4% CAGR through 2035 because of strong investments and adoption in oncology, immunology, infectious disease research and cell biology across academic and pharmaceutical laboratories.

Clinical diagnostics is expected to register the fastest growth advancing at an estimated 12.3% CAGR during the forecast period supported by the increasing demand for early disease detection, precision diagnostics and hematological testing.

By End User

Pharmaceutical and biotechnology companies accounted for the largest market share of approximately 35.9% in 2025 and are expected to expand at an estimated 11.6% CAGR through 2035 as growing investments in biologics, immunotherapy, vaccine development and drug discovery continue driving demand for advanced flow cytometry platforms.

Academic and research institutes are projected to record the fastest growth at an estimated 12.5% CAGR during the forecast period since growing public funding for life science research, expanding university based clinical studies and increasing translational medicine programs continue strengthening this segment.

Regional Insights

North America

North America accounted for approximately 43% of the market in 2025 due to advanced healthcare infrastructure, strong pharmaceutical research and substantial public funding for life sciences. Strong demand from major biotechnology hubs including Boston, San Diego and San Francisco continues to support market growth. The National Institutes of Health (NIH) and the National Cancer Institute (NCI) continue funding large scale biomedical, oncology, and immunology research programs that extensively utilize flow cytometry technologies.

Europe

Europe held for about 27% of the global market in 2025 and is expected to expand at an estimated 11.4% CAGR through 2035 due to increasing biomedical research, expanding pharmaceutical manufacturing and supportive healthcare policies. The European Commission continues funding life science innovation through Horizon Europe, while the European Medicines Agency (EMA) supports the development of advanced diagnostic and therapeutic technologies across member countries.

Asia Pacific

Asia Pacific accounted for nearly 18% of the market in 2025 and is projected to register an estimated 12.8% CAGR during the forecast period supported by expanding biotechnology industries, increasing clinical research activities, rising healthcare expenditure and growing investments in laboratory modernization across China, Japan, South Korea, and India. Government organizations including the Ministry of Health, Labor and Welfare (Japan) and the National Health Commission of China continue supporting biomedical research and advanced diagnostic infrastructure.

Rest of the World

The Rest of the World contributed almost 12% of the global market in 2025 and is expected to grow at an estimated 10.9% CAGR through 2035 owing to improving healthcare infrastructure, increasing research collaborations and expanding access to advanced diagnostic technologies across Latin America, the Middle East, and Africa. Growing public health investments continue creating opportunities for laboratory modernization and biomedical research.

Competitive Landscape / Company Insights

The market is highly competitive with global and regional companies focusing on product innovation, automation, strategic collaborations and geographic expansion to strengthen their market position. Manufacturers are increasingly investing in research and development, advanced analytical software and high parameter flow cytometry platforms to enhance clinical and research capabilities. The National Institutes of Health (NIH), the National Cancer Institute (NCI), and the U.S. Food and Drug Administration (FDA) continue supporting biomedical research, diagnostic innovation and regulatory standards that drive technological advancements across the market.

Mini Profiles

Agilent Technologies Inc. focuses on analytical instruments, flow cytometry solutions, and laboratory technologies, supported by strong global distribution networks, established brand recognition, and continuous research investments.

Becton, Dickinson and Company (BD) operates in the premium diagnostics and life sciences segment, emphasizing high performance flow cytometry platforms, clinical reliability, and advanced cell analysis capabilities.

Cytek Biosciences Inc. leverages innovative spectral flow cytometry technology, strategic research collaborations, and expanding global distribution channels to strengthen market presence in advanced cell analysis.

Danaher Corporation develops integrated life science and diagnostic solutions, supported by diversified technology portfolios, strong operational capabilities, and extensive customer relationships across research laboratories.

Merck KGaA specializes in reagents, antibodies, and cell analysis products, supported by broad scientific expertise, global manufacturing capabilities, and long-standing relationships with research institutions.

Key Players

- Agilent Technologies Inc.

- Becton, Dickinson and Company (BD)

- Bio-Rad Laboratories Inc.

- Cytek Biosciences Inc.

- Danaher Corporation

- Merck KGaA

- Miltenyi Biotec

- Sony Biotechnology Inc.

- Sysmex Corporation

- Thermo Fisher Scientific Inc.

Recent Developments

In January 2025, Bio-Rad Laboratories Inc. introduced new flow cytometry reagents and quality control solutions to improve consistency in clinical and research laboratories. The launch strengthened its portfolio for advanced cell analysis and immunology applications.

In March 2025, Miltenyi Biotec expanded its automated cell analysis workflow by introducing enhanced flow cytometry capabilities for immunology and cell therapy research. The development improved laboratory efficiency and high throughput sample processing.

In May 2025, Sony Biotechnology Inc. launched an advanced spectral cell analyzer with enhanced multi parameter detection for life science research. The system was designed to improve analytical accuracy and workflow productivity in research laboratories.

In September 2025, Thermo Fisher Scientific Inc. expanded its flow cytometry portfolio by introducing new antibodies and reagents supporting immunophenotyping and translational research. The expansion strengthened solutions for pharmaceutical and academic research customers.

In February 2026, Sysmex Corporation enhanced its clinical flow cytometry offerings through expanded diagnostic capabilities for hematology and oncology applications. The development supported faster and more accurate laboratory testing across healthcare institutions.

Global Flow Cytometry Market Coverage

Technology Insight and Forecast 2026 - 2035

- Cell Based Flow Cytometry

- Bead Based Flow Cytometry

Product and Service Insight and Forecast 2026 - 2035

- Instruments

- Reagents and Consumables

- Software

- Accessories

- Services

Application Insight and Forecast 2026 - 2035

- Research Applications

- Clinical Diagnostics

- Industrial Applications

- Others

End User Insight and Forecast 2026 - 2035

- Hospitals

- Clinical Testing Laboratories

- Academic and Research Institutes

- Pharmaceutical and Biotechnology Companies

- Others

Global Flow Cytometry Market by Region

- North America

- By Technology

- By Product and Service

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Technology

- By Product and Service

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Technology

- By Product and Service

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Technology

- By Product and Service

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Flow Cytometry Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Technology

1.2.2. By

Product and Service

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Technology

5.1.1. Cell Based Flow Cytometry

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Bead Based Flow Cytometry

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Product and Service

5.2.1. Instruments

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Reagents and Consumables

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Software

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Accessories

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Services

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Research Applications

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Clinical Diagnostics

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Industrial Applications

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Others

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Clinical Testing Laboratories

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Academic and Research Institutes

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Pharmaceutical and Biotechnology Companies

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Others

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Technology

6.2. By

Product and Service

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Technology

7.2. By

Product and Service

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Technology

8.2. By

Product and Service

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Technology

9.2. By

Product and Service

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Agilent Technologies Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Becton, Dickinson and Company (BD)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Bio-Rad Laboratories Inc.

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Cytek Biosciences Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Danaher Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Merck KGaA

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Miltenyi Biotec

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Sony Biotechnology Inc.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Sysmex Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Thermo Fisher Scientific Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Flow Cytometry Market