Vital Sign OEM Modules Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Product (Blood Pressure Modules, Pulse Oximetry Modules, ECG Modules, Temperature Modules, Capnography Modules, Others), by Modality (Standalone OEM Modules, Integrated OEM Modules), by End User (Hospitals, Ambulatory Surgical Centers, Home Healthcare, Diagnostic Centers, Others)

| Status : Published | Published On : Jul, 2026 | Report Code : VRHC1344 | Industry : Healthcare | Available Format : | Page : 143 |

Vital Sign OEM Modules Market Overview

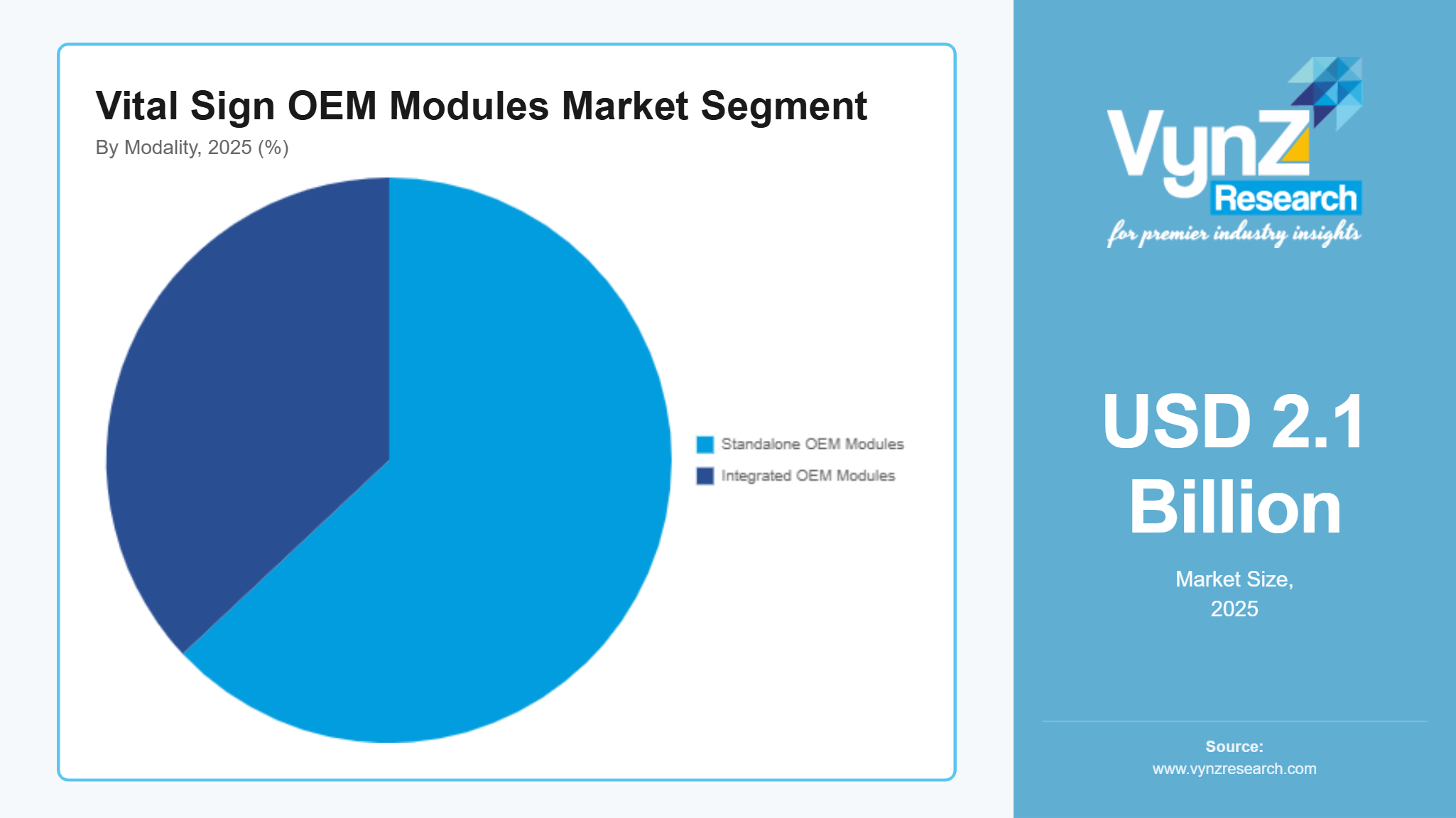

The vital sign OEM modules market size was estimated at about USD 2.1 billion in 2025 and is expected to reach around USD 2.4 billion in 2026, rising to roughly USD 7.1 billion by 2035, growing at approximately 13.2% CAGR from 2026 to 2035.

Research Highlights

- Blood Pressure Modules held 29.8% market share in 2025 due to widespread adoption in multiparameter patient monitoring.

- Integrated OEM Modules captured 63.4% share in 2025 supported by increasing demand for connected medical devices.

- Home Healthcare is projected to grow at 14.2% CAGR through 2035 because of expanding remote patient monitoring.

- Hospitals accounted for 58.9% market share in 2025 supported by growing investments in critical care infrastructure.

- North America contributed 36.8% revenue in 2025 supported by advanced healthcare infrastructure and medical technology innovation.

Market growth is supported by increasing demand for patient monitoring systems, growing adoption of connected healthcare technologies and expanding healthcare infrastructure, along with increasing integration of multi parameter monitoring modules, increasing demand for continuous patient monitoring across hospitals, ambulatory care centers, and home healthcare. Ongoing investments by the U.S. Food and Drug Administration (FDA) in digital health innovation, the National Institutes of Health (NIH) in medical technology research and the World Health Organization (WHO) in strengthening essential health services are further supporting market expansion across major regions including North America, Europe and Asia Pacific.

Vital Sign OEM Modules Market Dynamics

Market Trends

The industry is witnessing notable shifts in multiparameter patient monitoring, miniaturization, and connected healthcare technologies. One of the key trends shaping the market is the integration of compact OEM modules with wireless connectivity and real time data transmission, reflecting growing preference for efficient, portable, and continuous patient monitoring. The U.S. Food and Drug Administration (FDA) continues to support innovation in digital health technologies, while the World Health Organization (WHO) promotes wider adoption of digital health solutions to improve healthcare delivery. Another emerging trend is the increasing use of artificial intelligence and cloud enabled monitoring platforms, driven by technological advancements and expanding digital healthcare infrastructure. These developments are encouraging manufacturers to focus on interoperable monitoring modules, remote diagnostics, and integrated patient management solutions.

Growth Drivers

The growth of the market is largely supported by increasing demand for continuous patient monitoring across hospitals, ambulatory surgical centers and home healthcare settings. Rising investments in healthcare infrastructure and digital medical devices are further accelerating market expansion. The World Health Organization (WHO) continues to emphasize strengthening access to essential medical technologies, while the U.S. Department of Health and Human Services (HHS) supports modernization of healthcare delivery systems. Additionally, the growing prevalence of chronic diseases and aging populations is playing a crucial role in boosting market adoption. As healthcare providers prioritize early diagnosis, patient safety, and remote monitoring, demand for advanced vital sign monitoring modules is expected to remain strong throughout the forecast period.

Market Restraints / Challenges

Despite favorable growth prospects, the market faces certain challenges that may limit expansion. Stringent regulatory approval requirements and compliance with medical device standards continue to affect product commercialization, particularly for emerging manufacturers. Furthermore, dependence on specialized electronic components and semiconductor supply chains poses operational challenges for manufacturers. Supply disruptions and increasing component costs can lead to production delays and pricing pressures, affecting overall market performance.

Market Opportunities

The market presents significant opportunities in remote patient monitoring and home healthcare, particularly driven by the growing elderly population and increasing adoption of telehealth services. Companies offering compact, modular, and wireless monitoring solutions are well positioned to address rising demand from healthcare providers and medical device manufacturers. Another key opportunity lies in wearable medical devices and artificial intelligence enabled monitoring systems, where increasing investments in connected healthcare technologies are creating long term growth opportunities. Advancements in cloud computing, predictive analytics, and smart monitoring platforms are expected to improve clinical decision making and patient outcomes.

Global Vital Sign OEM Modules Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.1 Billion |

|

Revenue Forecast in 2035 |

USD 7.1 Billion |

|

Growth Rate |

13.2% |

|

Segments Covered in the Report |

By Product, By Modality, By End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Baxter International Inc., Contec Medical Systems Co., Ltd., GE HealthCare, Honeywell International Inc., Infineon Technologies AG, Medtronic plc, Nihon Kohden Corporation, Philips, Shenzhen Mindray Bio-Medical Electronics Co., Ltd., Smiths Group plc |

|

Customization |

Available upon request |

Vital Sign OEM Modules Market Segmentation

By Product

Blood pressure modules accounted for the largest market share of approximately 29.8% in 2025 and are expected to grow at an estimated 12.8% CAGR through 2035 supported by widespread integration into multiparameter patient monitors, bedside monitoring systems and portable diagnostic devices across hospitals and ambulatory care facilities. Increasing emphasis on continuous cardiovascular monitoring further supports demand.

Pulse oximetry modules are expected to register the fastest growth, advancing at an estimated 13.9% CAGR during the forecast period due to growing demand for respiratory monitoring, home healthcare devices and portable patient monitoring systems continues to accelerate adoption. Increasing utilization in chronic respiratory disease management and emergency care further strengthens segment expansion.

By Modality

Integrated OEM modules held the largest market share of approximately 63.4% in 2025 and are projected to expand at an estimated 13.1% CAGR through 2035 attributed to increasing incorporation into multiparameter monitoring systems, compact medical equipment and connected healthcare devices that improve clinical workflow and patient management.

Standalone OEM modules are anticipated to witness the fastest adoption rate, recording an estimated 13.7% CAGR throughout the forecast period due to growing demand from portable diagnostic equipment manufacturers and customized medical device applications continues to support market growth. Expanding deployment in remote healthcare and point of care settings further contributes to sustained demand.

By End User

Hospitals accounted for the largest market share of approximately 58.9% in 2025 and are expected to grow at an estimated 12.9% CAGR through 2035 due to increasing investments in critical care infrastructure, patient safety initiatives and advanced monitoring equipment continue to support demand. Rising hospital admissions associated with chronic diseases and an aging population further strengthen segment growth.

Home Healthcare is expected to register the fastest growth, expanding at an estimated 14.2% CAGR during the forecast period because of increasing adoption of remote patient monitoring, telehealth services and portable monitoring devices, growing preference for cost-effective long-term care and continuous monitoring outside traditional hospital settings.

Regional Insights

North America

North America accounted for approximately 40% of the market in 2025 supported by advanced healthcare infrastructure, widespread adoption of patient monitoring technologies, and strong medical device innovation. Demand remains high across the United States and Canada due to increasing deployment of multiparameter monitoring systems in hospitals and outpatient facilities. Government initiatives, combined with increasing adoption of remote patient monitoring and connected healthcare solutions, are encouraging investments in advanced OEM monitoring modules.

Europe

The Europe market accounted for approximately 24% of global revenue in 2025 due to increasing healthcare expenditure, expanding aging populations and growing demand for advanced diagnostic and patient monitoring equipment across hospitals and ambulatory care centers.

Asia Pacific

Asia Pacific represented approximately 18% of the market in 2025 because of expanding healthcare infrastructure, rising chronic disease prevalence and increasing investments in medical device manufacturing across China, India, Japan, and South Korea. The World Health Organization (WHO) continues to encourage improved access to essential medical technologies, while government healthcare modernization programs across the region are accelerating the adoption of advanced patient monitoring systems.

Rest of the World

The Rest of the World accounted for approximately 18% of the global market in 2025 supported by improving healthcare infrastructure, rising investments in medical technology and increasing adoption of patient monitoring systems across Latin America, the Middle East, and Africa.

Competitive Landscape / Company Insights

The market is moderately to highly competitive, with global and regional companies focusing on product innovation, research and development, strategic collaborations and geographic expansion to strengthen their market position. Manufacturers continue to invest in miniaturized monitoring technologies, wireless connectivity and AI enabled patient monitoring solutions to enhance clinical performance. The U.S. Food and Drug Administration (FDA) continues to support innovation in digital medical devices, while the National Institutes of Health (NIH) funds research advancing next generation patient monitoring technologies.

Mini Profiles

Baxter International Inc. focuses on patient monitoring technologies, medical devices, and integrated healthcare solutions, supported by strong global distribution, established hospital relationships, and continuous investment in clinical innovation.

Contec Medical Systems Co., Ltd. operates in the medical monitoring equipment segment, emphasizing affordable vital sign monitoring modules, product reliability, and broad international market accessibility for healthcare providers.

GE HealthCare develops advanced patient monitoring systems and OEM healthcare technologies, leveraging strong research capabilities, digital health expertise, and strategic partnerships to expand its global market presence.

Honeywell International Inc. focuses on sensing technologies, healthcare electronics, and connected medical solutions, supported by technological innovation, engineering expertise, and a diversified global industrial footprint.

Medtronic plc specializes in patient monitoring and medical technology solutions, emphasizing clinical performance, continuous innovation, and integrated healthcare systems to strengthen its position across global healthcare markets.

Key Players

- Baxter International Inc.

- Contec

- Medical Systems Co., Ltd.

- GE HealthCare

- Honeywell International Inc.

- Infineon Technologies AG

- Medtronic plc

- Nihon

- Kohden

- Corporation

- Philips

- Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

- Smiths Group plc

Recent Developments

In January 2026, Philips expanded its connected patient monitoring portfolio by introducing enhanced AI enabled clinical decision support capabilities for hospital monitoring systems. The development improves real time patient surveillance and supports broader integration with digital healthcare platforms.

In March 2026, Nihon Kohden Corporation launched an advanced patient monitoring solution featuring enhanced interoperability and remote monitoring capabilities for acute care environments. The new platform is designed to improve clinical workflow and support continuous vital sign monitoring.

In June 2025, Shenzhen Mindray Bio-Medical Electronics Co., Ltd. introduced upgraded multiparameter patient monitoring systems with improved connectivity and intelligent alarm management. The launch strengthens the company's portfolio for hospitals, ambulatory care facilities, and critical care applications.

In September 2025, Smiths Group plc announced enhancements to its medical technology portfolio through expanded investment in connected patient monitoring and critical care solutions. The initiative supports improved clinical efficiency and strengthens the company's healthcare technology business.

In February 2026, Infineon Technologies AG introduced new medical grade sensor and semiconductor solutions designed for next generation patient monitoring devices and wearable healthcare applications. The innovation supports higher measurement accuracy, lower power consumption, and advanced OEM medical device development.

Global Vital Sign OEM Modules Market Coverage

Product Insight and Forecast 2026 - 2035

- Blood Pressure Modules

- Pulse Oximetry Modules

- ECG Modules

- Temperature Modules

- Capnography Modules

- Others

Modality Insight and Forecast 2026 - 2035

- Standalone OEM Modules

- Integrated OEM Modules

End User Insight and Forecast 2026 - 2035

- Hospitals

- Ambulatory Surgical Centers

- Home Healthcare

- Diagnostic Centers

- Others

Global Vital Sign OEM Modules Market by Region

- North America

- By Product

- By Modality

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Product

- By Modality

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product

- By Modality

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product

- By Modality

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Vital Sign OEM Modules Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product

1.2.2. By

Modality

1.2.3. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product

5.1.1. Blood Pressure Modules

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Pulse Oximetry Modules

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. ECG Modules

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Temperature Modules

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.1.5. Capnography Modules

5.1.5.1. Market Definition

5.1.5.2. Market Estimation and Forecast to 2035

5.1.6. Others

5.1.6.1. Market Definition

5.1.6.2. Market Estimation and Forecast to 2035

5.2. By Modality

5.2.1. Standalone OEM Modules

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Integrated OEM Modules

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By End User

5.3.1. Hospitals

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Ambulatory Surgical Centers

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Home Healthcare

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Diagnostic Centers

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product

6.2. By

Modality

6.3. By

End User

6.3.1.

U.S. Market Estimate and Forecast

6.3.2.

Canada Market Estimate and Forecast

6.3.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product

7.2. By

Modality

7.3. By

End User

7.3.1.

Germany Market Estimate and Forecast

7.3.2.

France Market Estimate and Forecast

7.3.3.

U.K. Market Estimate and Forecast

7.3.4.

Italy Market Estimate and Forecast

7.3.5.

Spain Market Estimate and Forecast

7.3.6.

Russia Market Estimate and Forecast

7.3.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product

8.2. By

Modality

8.3. By

End User

8.3.1.

China Market Estimate and Forecast

8.3.2.

Japan Market Estimate and Forecast

8.3.3.

India Market Estimate and Forecast

8.3.4.

South Korea Market Estimate and Forecast

8.3.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product

9.2. By

Modality

9.3. By

End User

9.3.1.

Brazil Market Estimate and Forecast

9.3.2.

Saudi Arabia Market Estimate and Forecast

9.3.3.

South Africa Market Estimate and Forecast

9.3.4.

U.A.E. Market Estimate and Forecast

9.3.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Baxter International Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Contec Medical Systems Co., Ltd.

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

GE HealthCare

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Honeywell International Inc.

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Infineon Technologies AG

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Medtronic plc

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Nihon Kohden Corporation

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Philips

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Shenzhen Mindray Bio-Medical Electronics Co., Ltd.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Smiths Group plc

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Vital Sign OEM Modules Market