North America Artificial Intelligence in Healthcare Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by End-User Organisation Size (Large Enterprises, Small & Medium Enterprises (SMEs)), by Application (Diagnostic Imaging & Clinical Decision Support, Remote Patient Monitoring & Virtual Care, Clinical Workflow Automation, Population Health & Risk Analytics, Revenue Cycle & Administrative Intelligence), by Care Delivery Setting (Hospitals & Integrated Health Systems, Pharmaceutical, Biotechnology & Life Sciences Organizations, Specialty Clinics & Ambulatory Care Centers, Payers & Managed Care Organisations, Home Healthcare & Remote Care Providers), by Clinical Focus Area (Oncology & Precision Medicine, Neurology & Cognitive Health, Cardiology & Chronic Disease Management, Radiology & Imaging-Centric Specialties, Primary Care & Preventive Health)

| Status : Published | Published On : Feb, 2026 | Report Code : VRHC1325 | Industry : Healthcare | Available Format :

|

Page : 145 |

North America Artificial Intelligence in Healthcare Market Overview

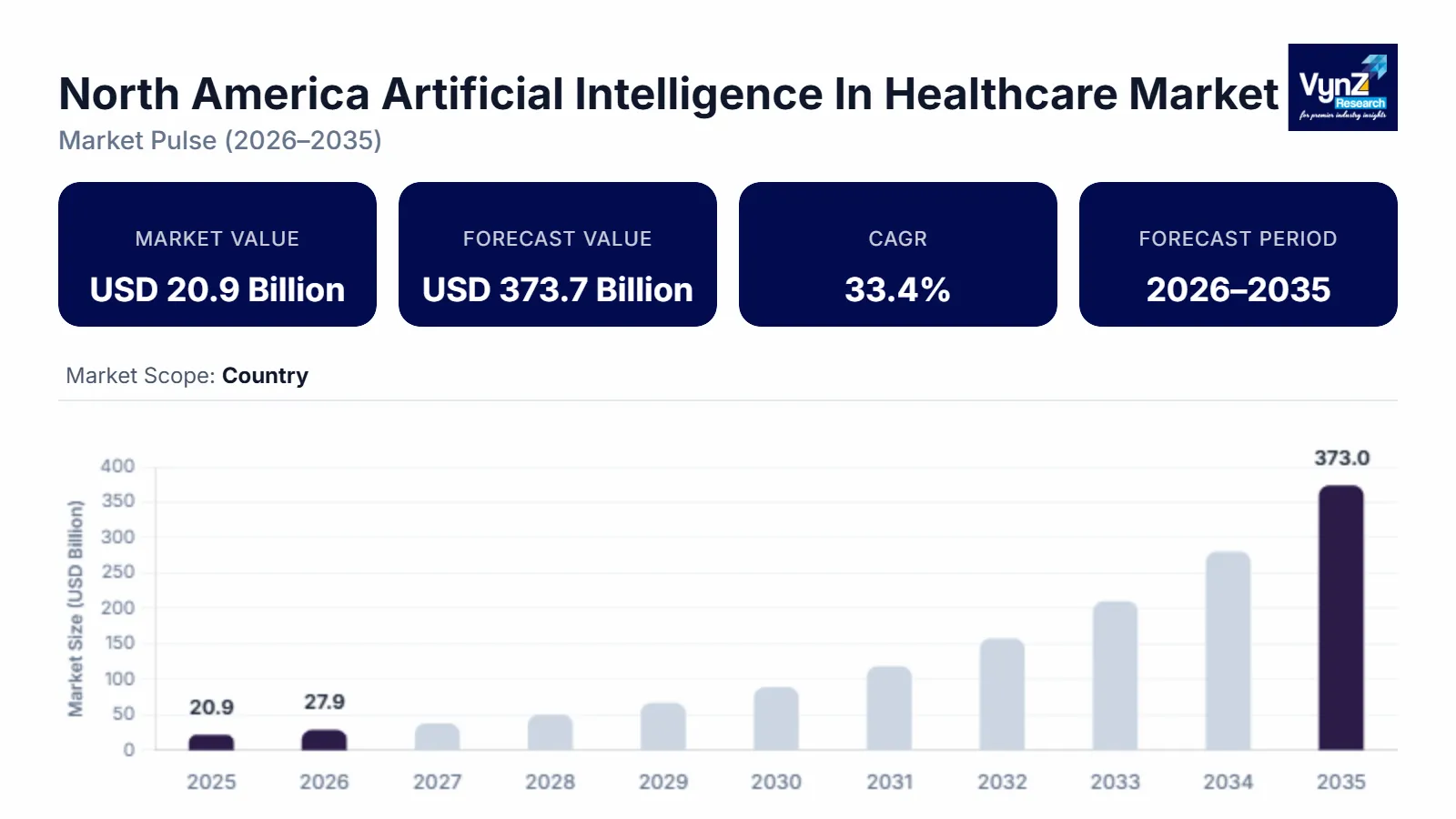

The North America artificial intelligence in healthcare market, which was valued at approximately USD 20.9 billion in 2025 and is estimated to reach around 30.5 billion in 2026, is projected to reach close to USD 373.7 billion by 2035, expanding at a CAGR of about 33.4% during the forecast period from 2026 to 2035.

The healthcare industry is developing at an accelerated rate due to the increasing integration of artificial intelligence (AI) with the healthcare system as a means to provide increased efficiency, personalized, and data-driven care delivery to meet the increasing demands of the population for more efficient, personalized, and data-driven care delivery. Healthcare providers and life science companies have begun to incorporate AI within their organisation through advances in the development of digital health infrastructure, interoperable patient data systems, and sophisticated algorithmic analytics, which enable improved diagnostics, predictive patient management, and better operational performance. The integration of AI will support the earlier detection of diseases, enhance precision medicine initiatives, and streamline clinical workflows, and the increasing demand for value-based care and resilient health systems will drive further innovation and adoption throughout the region, as According to the U.S. Food and Drug Administration, 950 AI-enabled medical devices had received regulatory authorization in 2024.

North America artificial intelligence in healthcare market Dynamics

Market Trends

The market has shifted clearly from pilot projects in experimenting with AI to the implementation of large-scale AI solutions in the clinical and operational processes of healthcare. The adoption is expanding beyond the concept of a proof-of-concept into embedded applications and uses, such as automated diagnostics, clinical documentation, virtual care interfaces, and predictive patient management systems. Integration of AI technology into traditional healthcare IT systems is rapidly increasing, and partnerships among established healthcare providers, tech innovators, and life sciences companies are forming to speed up the delivery of solutions. Real-time decision support and personalised care delivery are being driven by an increasing priority on generative and machine learning-based tools, which represent the next level of maturity in the ecosystem, as According to the U.S. Food and Drug Administration, the cumulative number of authorized AI-enabled medical devices exceeded 1,200 in 2025.

Growth Drivers

The healthcare industry is using the development of digital health (the underlying technology base) and the growth in demand for more personalised, more effective, and more accountable healthcare delivery to grow the use of artificial intelligence (AI). Providers, pharmaceutical companies, medical device manufacturers, and payers are all investing in AI to be able to better identify disease earlier, create more efficient clinical workflows, and develop more precise treatment options for patients. The growing number of value-based payment arrangements, combined with greater access to quality clinical and patient data and increased institutional support for replacing outdated health IT systems, continue to fuel the investment and use of AI technologies, as According to the U.S. Food and Drug Administration, a cumulative total of 1,357 AI-based medical devices had received regulatory clearance in 2025.

Market Restraints / Challenges

There are many barriers to using AI in healthcare, such as poor-quality data, a lack of compatibility between different healthcare systems, a lack of consistency in how data is formatted, and a lack of commonality in how data is standardised. This creates a problem for developing and deploying models with reliable performance. There are also regulatory issues that require extensive validation, auditability, and explainability to ensure that AI-based systems meet the necessary safety and regulatory requirements, creating long and complex cycles to implement AI models. Additionally, there are barriers to widespread use of AI in healthcare due to concerns regarding patient confidentiality and data privacy, potential biases in algorithms, and a need for greater clinician trust to facilitate easier incorporation into clinical routines. Finally, the costs associated with implementing AI in healthcare settings are high, as are the costs of acquiring and retaining the required talent to support these efforts.

Market Opportunities

A large number of opportunities exist within the market due to an increase in the use of artificial intelligence (AI) to support both the delivery of healthcare services and conducting research. An expansion of AI tools will likely be used for the early detection of diseases, to provide a path of treatment that is based on the individual's needs, and to predictively manage patients' care to improve the quality of clinical care and operational efficiency. Virtual care, home monitoring, and the development of real-world evidence through the use of AI are all emerging segments in healthcare that create additional revenue streams. Co-creation and co-development between the innovators of technologies, providers, and the life sciences companies provide the opportunity for each organisation to develop solutions that meet their unique needs. The ability to deploy scalable and commercially viable AI throughout the entire healthcare ecosystem continues to grow with the maturation of regulations and the continued growth of the digital health infrastructure.

North America Artificial Intelligence in Healthcare Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 20.9 Billion |

|

Revenue Forecast in 2035 |

USD 373.7 Billion |

|

Growth Rate |

33.4% |

|

Segments Covered in the Report |

Component Type, Organization Size, Application, Care Delivery Setting, Clinical Focus Area |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

U.S. and Canada |

|

Key Companies |

Microsoft Corporation, Google (Alphabet Inc.), IBM Corporation, NVIDIA Corporation, Amazon Web Services (AWS), Intel Corporation, GE HealthCare, Siemens Healthineers, Medtronic, IQVIA Holdings, Inc., Oracle Corporation, Epic Systems Corporation, Veradigm LLC, K Health, Suki / Suki AI |

|

Customization |

Available upon request |

North America Artificial Intelligence In Healthcare Market Segmentation

By Component Type

Solutions is the largest category with a market share of about 45% in 2025, as healthcare institutions rely on the ability to deploy and use them for outcomes, and their ability to enhance the clinical accuracy, diagnostic speed, and quality of care directly. Providers and life science companies prefer mature AI solutions as they can be integrated into existing clinical systems to generate immediate benefits both operationally and medically. Today, these solutions are being used by providers and life science companies as strategic resources to enhance the quality of care delivered, to improve the health outcomes for patients, and to help drive enterprise-wide digital transformation efforts, as According to the U.S. Food and Drug Administration, 1,247 AI-enabled medical devices had received regulatory authorization in 2025.

Services is the fastest-growing category, as an increasing number of organisations are looking to implement and validate complex AI systems within their own regulatory environments and are therefore in need of high-level expert advice and assistance to create customised AI models that perform well clinically and maintain the integrity of the data being used to drive these models. Further, this group of organisations needs assistance to meet the compliance requirements of each organisation (i.e., HIPAA) while meeting the ethical requirements of using AI in healthcare. The need for advisory, integration, and managed services will increase significantly as AI usage moves from being in single use-case applications to enterprise-wide applications, as According to the World Health Organization, 120 countries had established a national digital health strategy or policy in 2024.

By Organization Size

Large enterprises are the largest category with a market share of approx 70% in 2025, because they have existing digital infrastructure, larger resources for investing in new technologies, and large-scale clinical operations where an enterprise-level AI platform could be absorbed. The use of AI by these companies is focused primarily on optimising the volume of patients, large-scale, complicated care paths, and the workflow of multiple sites of operation. As a result, their long-term view toward transforming care with data and planning for future technology roadmaps positions them as the first adopters of enterprise-level healthcare AI solutions, as According to the Office of the National Coordinator for Health Information Technology, 96% of large hospitals in the United States used predictive AI in 2024.

Small and medium enterprises (SMEs) are the fastest-growing category with a CAGR of 33.9% during the forecast period, driven by low-cost entry points for accessible AI platforms and cloud-based delivery models. A larger number of SMEs will utilise AI in order to enhance the ability of clinicians to make accurate diagnoses, automate administrative tasks, and increase patient engagement through the use of technology, without a significant investment in front-end infrastructure. Competitive pressures, increased operational efficiencies, and an increasing need to adopt new models for delivering care are driving AI adoption by smaller healthcare organisations and emerging care providers, as According to the Office of the National Coordinator for Health Information Technology, predictive AI adoption among independent hospitals increased from 31% in 2023 to 37% in 2024.

By Application

Diagnostic imaging and clinical decision support are the largest categories with a market share of around 30% in 2025, as they drive clinical precision, operational efficiency, and quality of care in high-volume settings. AI-based image interpretation tools and decision support systems are now integral to most routine clinical workflows, enabling physicians to manage diagnostic complexity and reduce variability in clinical outcomes. As such, diagnostic imaging and clinical decision support tools provide real-time clinical benefits and quantifiable process improvement that support long-term enterprise-wide adoption of those applications, as According to the U.S. Food and Drug Administration, radiology software accounted for approximately 81% of all AI-enabled medical device authorizations in 2025.

Remote patient monitoring and virtual care are the fastest-growing categories with a CAGR of 33.9%, largely because of a structural shift in how healthcare is delivered (decentralised) and how patients are engaged (continuously). AI-enabled remote monitoring can be used to create proactive interventions, develop personalised care paths for patients with chronic and post-acute care needs, and also to manage these conditions on a large scale. Therefore, as healthcare organisations move from delivering care at their facility to providing care that continues when patients leave those facilities, the role of virtual care will become an integral part of what it means to deliver care today, as According to the World Health Organization, 129 Member States had established a national digital health strategy or policy in 2024.

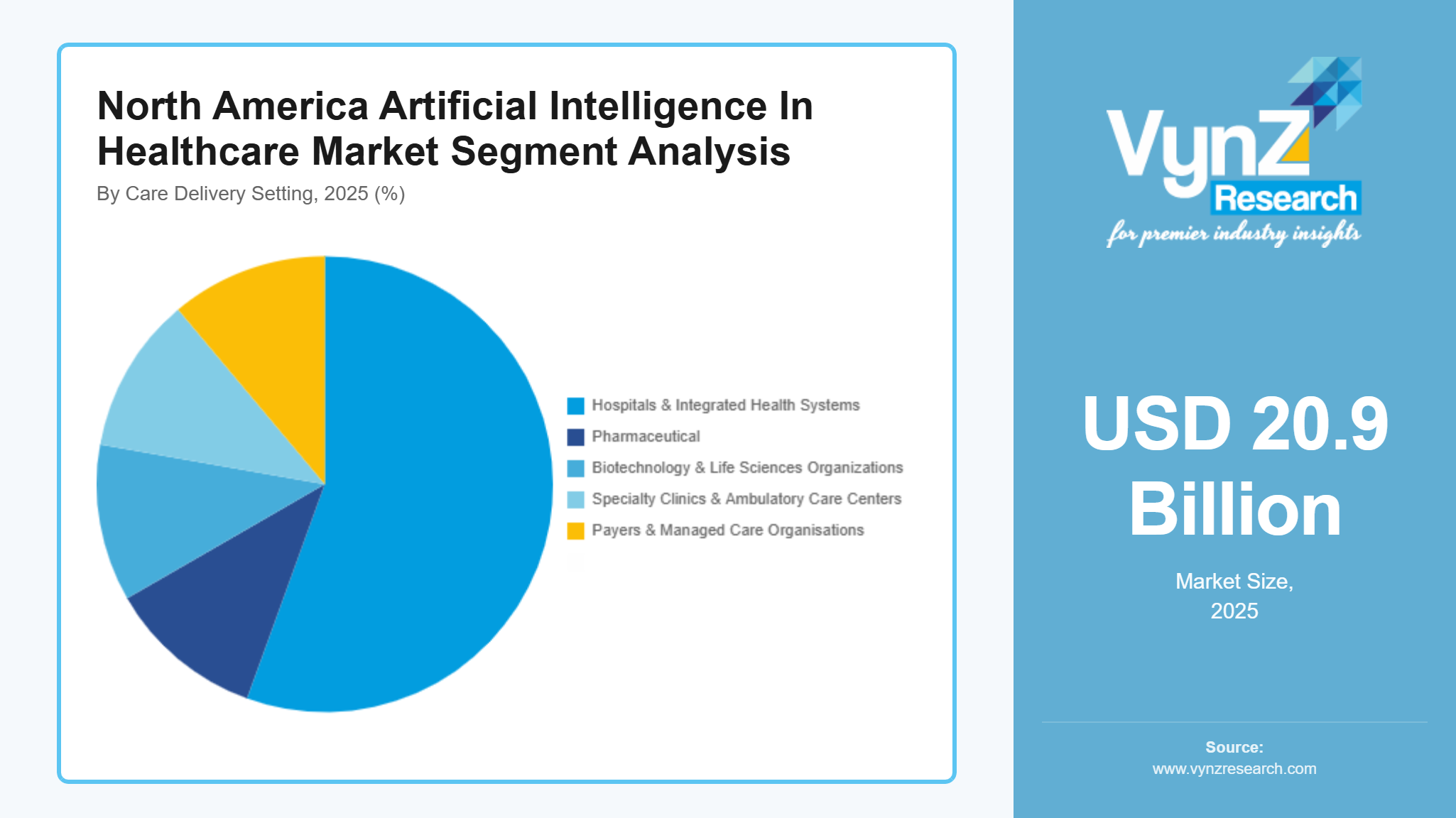

By Care Delivery Setting

Hospitals and integrated health systems are the largest category with a market share of around 50% in 2025, primarily as a result of their critical role in providing acute care services, diagnostic services, and complex clinical decision-making processes. Hospitals use AI in three main areas: clinical operations, patient management, and imaging. As such, hospitals can improve care quality and operational resilience through the deployment of AI. Also, hospitals' large-scale clinical data sets, along with their structured digital environments, provide an excellent platform for hospitals to invest in enterprise-wide AI systems and sustainable technology investments, as According to the Office of the National Coordinator for Health Information Technology, 96% of large hospitals in the United States utilized predictive AI in 2024.

Pharmaceutical, biotechnology, and life sciences organisations are the fastest-growing category, as they continue to apply AI as a tool to drive faster discovery and product development through precision medicine and improved clinical trial development, as well as improved data analysis to make better decisions on their drug development pipeline. The competitive need for pharmaceutical companies to quickly develop new products and to effectively utilise their R&D dollars will be the driver for the large-scale use of AI by these organisations, as According to the U.S. Food and Drug Administration, more than 500 drug and biologic development submissions incorporated AI or machine learning components in 2024.

By Clinical Focus Area

Oncology and precision medicine are the largest categories with a market share of about 35% in 2025, because of the amount of data that will be needed for cancer care, and also how many people want a personalised treatment plan from their doctor. AI helps to develop better treatment plans based on advanced recognition of patterns in the three clinical types of data: imaging, genomic, and clinical data, therefore allowing the physician to make a more accurate and personalised therapy plan. The strategic importance of precision oncology being used in healthcare today continues to create long-term support for AI in this field, as According to the U.S. Food and Drug Administration, radiology and imaging-based tools accounted for approximately 77% of the 1,247 AI-enabled medical devices authorized in 2025.

Neurology and cognitive health are the fastest-growing category, due to the growing importance of AI technology for early identification, monitoring disease progression, and supporting clinically based decisions for complex neurological disorders. Accordingly, the growing focus of clinical practice on cognitive health will be supplemented by new capabilities with imaging analytics and predictive analytics, resulting in higher levels of AI adoption. The integration of AI by healthcare providers will improve the level of diagnostic confidence and the ultimate management of neurological conditions over time, as According to the World Health Organization, 129 Member States had established a national digital health strategy or policy in 2024.

Regional Insights

North America Artificial Intelligence In Healthcare Market

North America is a sophisticated environment for developing artificial intelligence in healthcare due to a highly integrated digital health ecosystem, a robust innovation ecosystem, and a high level of maturity in healthcare IT infrastructure. The area has a collaborative relationship between the tech industry, hospitals, research institutions, and pharmaceutical companies, which allows for quicker conversion of the development of AI technology into a clinical setting. The regulatory environment for the use of clinical-grade AI, the expansion of the use of real-world data, and large-scale investments at the enterprise level to improve healthcare infrastructure are all shaping a structural environment of resilience and innovation across the region.

U.S. Artificial Intelligence In Healthcare Market

The United States has a large number of integrated healthcare delivery systems with a high density of AI developers and early institutional deployments of clinical intelligence platforms (CIPs) throughout diagnostics, operations, and precision medicine within the enterprise-scale healthcare environment, which supports the widespread use of AI in the U.S., as According to the Office of the National Coordinator for Health Information Technology, 71% of non-federal acute-care hospitals in the United States used predictive AI integrated into their electronic health records in 2024.

Canada Artificial Intelligence In Healthcare Market

Canada is also expanding its adoption of AI at a very rapid pace due to its extensive public health data infrastructure, system-wide digital health programs, and increasing collaborations between healthcare institutions and technology firms that are supporting AI adoption in diagnostics, virtual care, and population health management, as According to the Government of Canada, the Connected Care for Canadians Act (Bill C-72) was introduced in 2024 to mandate common data standards and interoperability for digital health services.

Competitive Landscape / Company Insights

The market is fragmented due to a variety of global, regional, and niche players offering specialised solutions to numerous clinical and operational use cases. No one company has an overwhelming share of the total market. In many sub-segments, there are multiple providers who compete for market share intensely. This competition is based on application area specialisation, not on consolidated control by a small number of incumbent companies. The fragmentation is also supported by innovative start-ups that address distinct healthcare needs. There are significant differences in AI deployment across the many different clinical domains. While strategic initiatives, such as partnerships and acquisitions, are present, they have not yet materially reduced the competitive base to a highly concentrated structure.

Mini Profiles

Microsoft Corporation is still one of the leading global technology companies delivering cloud-based AI platforms and cognitive services that provide healthcare analytics, clinical insights and seamless data integration with providers, payers, and life sciences innovators.

Google (Alphabet Inc.) is still one of the world's largest technology companies, using AI and machine learning to drive medical imaging, clinical decision support systems, and health data analytics to create scalable healthcare intelligence and research-driven innovation.

IBM Corporation is still an enterprise AI and analytics company providing healthcare-focused platforms that help to increase the effectiveness of clinical decision support, improve care coordination and enhance operational efficiencies of healthcare organisations and research institutions.

NVIDIA Corporation is still one of the leaders in AI computing and GPU technologies, enabling high-performance healthcare analytics, advanced medical imaging, and deep learning infrastructure for hospitals, research laboratories, and life sciences enterprises.

Amazon Web Services (AWS) is still one of the leading cloud and AI service providers delivering scalable machine learning tools, secure data platforms and healthcare-specific solutions to support compliance with analytics regulations and digital transformation initiatives.

Key Players

- Microsoft Corporation

- Google (Alphabet Inc.)

- IBM Corporation

- NVIDIA Corporation

- Amazon Web Services (AWS)

- Intel Corporation

- GE HealthCare

- Siemens Healthineers

- Medtronic

- IQVIA Holdings, Inc.

- Oracle Corporation

- Epic Systems Corporation

- Veradigm LLC

- K Health

- Suki / Suki AI

Recent Developments

January 2026 - OpenAI launched ChatGPT Health, expanding its product portfolio into healthcare with an AI system designed to integrate electronic health records and wellness app data for clinical information access.

November 2025 - Viz.ai launched Viz Assist, introducing autonomous AI agents into its clinical workflow platform to support care coordination and real-time clinical prioritisation across care teams.

July 2025 - Tandem Health rolled out its AI scribing tool across NHS clinical systems, deploying ambient clinical documentation software into routine care environments.

June 2025 - Outcomes4Me completed the acquisition of MIKA Health, extending its AI-based patient engagement and symptom-tracking platform into European digital health markets.

North America Artificial Intelligence in Healthcare Market Coverage

End-User Organisation Size Insight and Forecast 2026 - 2035

- Large Enterprises

- Small & Medium Enterprises (SMEs)

Application Insight and Forecast 2026 - 2035

- Diagnostic Imaging & Clinical Decision Support

- Remote Patient Monitoring & Virtual Care

- Clinical Workflow Automation

- Population Health & Risk Analytics

- Revenue Cycle & Administrative Intelligence

Care Delivery Setting Insight and Forecast 2026 - 2035

- Hospitals & Integrated Health Systems

- Pharmaceutical

- Biotechnology & Life Sciences Organizations

- Specialty Clinics & Ambulatory Care Centers

- Payers & Managed Care Organisations

- Home Healthcare & Remote Care Providers

Clinical Focus Area Insight and Forecast 2026 - 2035

- Oncology & Precision Medicine

- Neurology & Cognitive Health

- Cardiology & Chronic Disease Management

- Radiology & Imaging-Centric Specialties

- Primary Care & Preventive Health

North America Artificial Intelligence in Healthcare Market by Region

- North America

- By End-User Organisation Size

- By Application

- By Care Delivery Setting

- By Clinical Focus Area

- Europe

- By End-User Organisation Size

- By Application

- By Care Delivery Setting

- By Clinical Focus Area

- Asia-Pacific (APAC)

- By End-User Organisation Size

- By Application

- By Care Delivery Setting

- By Clinical Focus Area

- Rest of the World (RoW)

- By End-User Organisation Size

- By Application

- By Care Delivery Setting

- By Clinical Focus Area

Table of Contents for North America Artificial Intelligence in Healthcare Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

End-User Organisation Size

1.2.2. By

Application

1.2.3. By

Care Delivery Setting

1.2.4. By

Clinical Focus Area

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. North Market Estimate and Forecast

4.1. North Market Overview

4.2. North Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By End-User Organisation Size

5.1.1. Large Enterprises

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Small & Medium Enterprises (SMEs)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Application

5.2.1. Diagnostic Imaging & Clinical Decision Support

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Remote Patient Monitoring & Virtual Care

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Clinical Workflow Automation

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Population Health & Risk Analytics

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Revenue Cycle & Administrative Intelligence

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Care Delivery Setting

5.3.1. Hospitals & Integrated Health Systems

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Pharmaceutical

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Biotechnology & Life Sciences Organizations

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Specialty Clinics & Ambulatory Care Centers

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Payers & Managed Care Organisations

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Home Healthcare & Remote Care Providers

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.4. By Clinical Focus Area

5.4.1. Oncology & Precision Medicine

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Neurology & Cognitive Health

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Cardiology & Chronic Disease Management

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Radiology & Imaging-Centric Specialties

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Primary Care & Preventive Health

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

End-User Organisation Size

6.2. By

Application

6.3. By

Care Delivery Setting

6.4. By

Clinical Focus Area

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

End-User Organisation Size

7.2. By

Application

7.3. By

Care Delivery Setting

7.4. By

Clinical Focus Area

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

U.K. Market Estimate and Forecast

7.4.3.

France Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

End-User Organisation Size

8.2. By

Application

8.3. By

Care Delivery Setting

8.4. By

Clinical Focus Area

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Vietnam Market Estimate and Forecast

8.4.6.

Thailand Market Estimate and Forecast

8.4.7.

Malaysia Market Estimate and Forecast

8.4.8.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

End-User Organisation Size

9.2. By

Application

9.3. By

Care Delivery Setting

9.4. By

Clinical Focus Area

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Microsoft Corporation

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Google (Alphabet Inc.)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

IBM Corporation

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

NVIDIA Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Amazon Web Services (AWS)

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Intel Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

GE HealthCare

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Siemens Healthineers

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Medtronic

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

IQVIA Holdings, Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Oracle Corporation

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Epic Systems Corporation

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

10.13.

Veradigm LLC

10.13.1.

Snapshot

10.13.2.

Overview

10.13.3.

Offerings

10.13.4.

Financial

Insight

10.13.5.

Recent

Developments

10.14.

K Health

10.14.1.

Snapshot

10.14.2.

Overview

10.14.3.

Offerings

10.14.4.

Financial

Insight

10.14.5.

Recent

Developments

10.15.

Suki / Suki AI

10.15.1.

Snapshot

10.15.2.

Overview

10.15.3.

Offerings

10.15.4.

Financial

Insight

10.15.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

North America Artificial Intelligence in Healthcare Market