Radiation Therapy in Oncology Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Radiation Type (External Beam Radiation Therapy (EBRT), Internal Radiation Therapy (Brachytherapy), Systemic Radiation Therapy), by Therapy (Stereotactic Radiosurgery (SRS) / Stereotactic Body Radiotherapy (SBRT), Intensity-Modulated Radiation Therapy (IMRT), Image-Guided Radiation Therapy (IGRT), Volumetric-Modulated Arc Therapy (VMAT), Proton Beam Therapy (Proton Therapy), Brachytherapy), by Application (Breast Cancer, Prostate Cancer, Lung Cancer, Colorectal Cancer, Others), by End User (Hospitals & Research Institutes, Specialized Radiotherapy / Cancer Centers)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1328 | Industry : Healthcare | Available Format :

|

Page : 178 |

Radiation Therapy in Oncology Market Overview

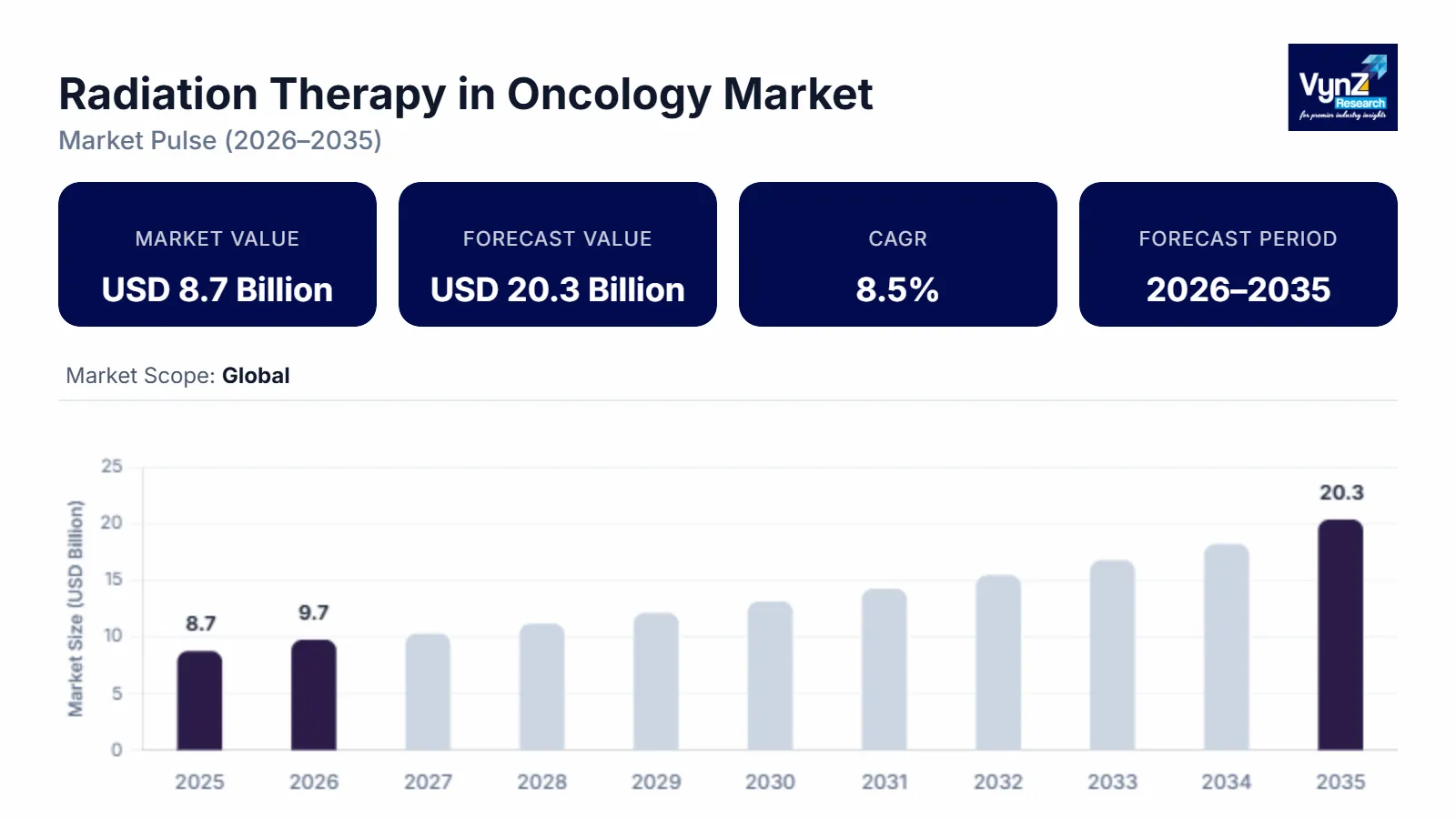

The radiation therapy in oncology market which was valued at approximately USD 8.7 billion in 2025 and is estimated to reach around USD 9.7 billion in 2026, is projected to reach close to USD 20.3 billion by 2035, expanding at a CAGR of about 8.5% during the forecast period from 2026 to 2035.

The market is experiencing sustained growth as cancer care shifts toward precision-driven, technology-enabled treatment models. Rising global cancer incidence, coupled with longer life expectancy, continues to expand the patient pool requiring localized and systemic radiation interventions.

Healthcare providers are prioritizing treatment accuracy, safety, and clinical outcomes, accelerating adoption of advanced modalities such as stereotactic, image-guided, and intensity-modulated radiation therapies. Continuous innovation in treatment planning software, automation, and adaptive therapy is improving workflow efficiency while reducing toxicity to healthy tissue, making radiation therapy an increasingly preferred option across multiple cancer types. Expanding investments in hospital infrastructure, growing establishment of specialized radiotherapy centers, and improved access to oncology services in emerging economies are further strengthening market momentum. Additionally, radiation therapy’s critical role in combination cancer treatment strategies—alongside surgery, chemotherapy, and immunotherapy - positions it as an indispensable pillar of modern oncology, driving long-term, resilient market expansion.

Radiation Therapy in Oncology Market Dynamics

Market Trends

A defining trend shaping the radiation therapy in oncology market is the sustained rise in global cancer incidence, validated by public health authorities worldwide. According to the World Health Organization (2024), cancer continues to impose a growing clinical and economic burden, driven by aging populations, urban lifestyles, and environmental risk factors. Governments are increasingly prioritizing scalable, evidence-based cancer treatment solutions that can deliver precision while managing long-term care demands. In parallel, national cancer registries are strengthening surveillance and reporting systems, enabling healthcare systems to plan radiotherapy capacity more effectively.

For example, India’s government reported over 1.53 million new cancer cases in 2024, highlighting a sharp rise in demand for structured oncology care. This pattern is echoed in the WHO Eastern Mediterranean Region, where more than 788,000 cancer cases were recorded in 2022 and are projected to reach 1.57 million by 2045, driven by population growth and high prevalence of risk factors such as tobacco use, obesity, physical inactivity, unhealthy diets, and air pollution. As cancer increasingly becomes a chronic condition, radiation therapy is emerging as a cornerstone modality due to its adaptability across disease stages, reinforcing sustained global investment in radiotherapy infrastructure, skilled workforce development, and advanced treatment technologies.

Growth Drivers

The primary driver of growth in the radiation therapy market is the increasing alignment of national cancer control programs with precision-based treatment strategies. Governments and public health agencies are recognizing radiation therapy as an essential pillar of modern oncology due to its clinical effectiveness, scalability, and compatibility with multidisciplinary care. According to the World Health Organization, strengthening access to early diagnosis and effective treatment remains a global priority as cancer incidence continues to rise. In the United States, federal cancer surveillance maintained by the Centers for Disease Control and Prevention consistently informs national treatment guidelines and infrastructure planning, reinforcing the role of radiotherapy across care pathways. Public investment in hospital expansion, digital imaging, and oncology training programs further accelerates adoption of advanced radiation techniques. As policymakers increasingly focus on improving survival outcomes while controlling long-term healthcare costs, radiation therapy is positioned as a cost-effective, outcomes-driven solution—making it a central growth engine for oncology services worldwide.

Market Restraints / Challenges

Despite strong growth fundamentals, the radiation therapy market faces a critical challenge in the form of unequal access to oncology infrastructure and skilled workforce capacity. While cancer incidence continues to rise globally, the availability of timely, high-quality radiation treatment remains uneven across regions. The World Health Organization highlights that a substantial share of cancer cases could be prevented or more effectively managed, yet gaps in diagnostic coverage, radiotherapy facilities, and trained professionals persist in many healthcare systems. In several emerging economies, rapid growth in cancer prevalence is outpacing investments in oncology infrastructure, placing significant strain on public health resources. Even in developed markets, disparities between urban and rural areas often result in delayed treatment initiation and limited access to advanced radiation technologies. These structural and operational gaps present a major barrier to market scalability, underscoring the need for coordinated government funding, workforce development programs, and long-term infrastructure planning to ensure equitable delivery of radiation therapy worldwide.

Market Opportunities

A significant opportunity in the radiation therapy market is emerging from the growing alignment between national healthcare priorities and long-term oncology infrastructure development. Governments worldwide are moving beyond short-term treatment capacity and focusing on building resilient cancer care systems that emphasize early intervention, precision treatment, and outcome optimization. Public health frameworks increasingly recognize that standardized, technology-enabled radiation therapy can materially reduce mortality while supporting cost-efficient care delivery. At the same time, expanding cancer surveillance and registry programs—such as federally maintained cancer databases in the United States—are providing policymakers with clearer visibility into disease burden, treatment gaps, and future demand. This data-driven approach is accelerating targeted investments in radiotherapy equipment, workforce training, and digital treatment planning platforms. With cancer incidence rising across both developed and emerging markets, scalable radiation solutions are becoming central to national oncology strategies. These conditions create strong opportunities for healthcare providers, technology partners, and advisory firms to support modernization efforts and shape the next phase of sustainable cancer care delivery.

Global Radiation Therapy in Oncology Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 8.7 Billion |

|

Revenue Forecast in 2035 |

USD 20.3 Billion |

|

Growth Rate |

8.5% |

|

Segments Covered in the Report |

Radiation Type, Therapy, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Siemens Healthineers AG, Elekta AB, Accuray Incorporated, Ion Beam Applications SA, Hitachi High-Tech Corporation, Carl Zeiss Meditec AG, Mevion Medical Systems, Inc., Koninklijke Philips N.V., ViewRay Technologies, Inc., Sumitomo Heavy Industries, Ltd., Brainlab AG, Eckert & Ziegler AG |

|

Customization |

Available upon request |

Radiation Therapy in Oncology Market Segmentation

By Radiation Type

External Beam Radiation Therapy (EBRT) is the largest and most widely used radiation type globally, with an estimated market share of 70% in 2025, forming the backbone of modern oncology treatment. EBRT delivers high-energy radiation from outside the body to precisely target tumors, and is the primary modality for common cancers such as breast, lung, prostate, and colorectal cancer. This dominance is reflected in clinical practice guidelines and public health cancer resources, which describe EBRT as the most common form of radiation treatment used across cancer types due to its versatility and ability to integrate with surgery and systemic therapy. EBRT’s broad applicability makes it the first-line choice in multidisciplinary cancer care, driving its widespread adoption and making it the largest contributor to radiation therapy volumes in major healthcare systems worldwide.

Systemic radiation therapy represents the fastest-growing category within oncology radiation, with a CAGR of 8.8% in the coming years, driven by the emergence of radiopharmaceuticals and targeted radionuclide therapies. Unlike localized treatments, systemic therapy involves radioactive agents delivered by infusion or oral ingestion that circulate through the bloodstream to reach cancer cells throughout the body. This approach is especially impactful in advanced or metastatic disease, including thyroid cancer with radioactive iodine and novel targeted agents linked to tumor-seeking molecules. Recent developments in theranostics—combining diagnostic imaging and therapy in a single agent—have expanded systemic radiation’s utility and guided precision dosing. With government cancer agencies increasingly recognizing the clinical value of these treatments, and with ongoing regulatory approvals, systemic radiation is rapidly gaining traction as a complementary modality to both EBRT and brachytherapy in population-based cancer care strategies.

By Therapy

Intensity-Modulated Radiation Therapy (IMRT) represents the largest therapy category within the radiation therapy in oncology market, which held an approx. 30% of share in 2025. This is due to its widespread clinical adoption and versatility across multiple cancer types. IMRT enables highly precise modulation of radiation dose, allowing clinicians to conform treatment to complex tumor geometries while minimizing exposure to surrounding healthy tissue. This balance between precision and safety has positioned IMRT as a foundational therapy in modern radiation oncology. Its compatibility with advanced imaging, treatment planning systems, and combination cancer care strategies further strengthens its role in routine clinical practice. As hospitals and cancer centers continue to standardize advanced external beam therapies, IMRT remains the preferred modality for delivering effective, reproducible, and scalable radiation treatment across diverse patient populations.

Stereotactic Radiosurgery (SRS) and Stereotactic Body Radiotherapy (SBRT) are the fastest-growing therapy categories in radiation oncology, driven by their ability to deliver high-dose radiation with exceptional accuracy in a limited number of treatment sessions. These therapies are increasingly favored for treating small, well-defined tumors where surgical intervention may be high risk or unnecessary. Their non-invasive nature, shorter treatment timelines, and strong clinical outcomes make them highly attractive to both providers and patients. As healthcare systems emphasize efficiency, patient convenience, and precision-based care, SRS and SBRT are rapidly expanding across hospital settings and specialized radiotherapy centers, reinforcing their position as key growth drivers in the evolving oncology treatment landscape.

By Application

Breast cancer remains the largest application category in the radiation therapy market, reflecting its high prevalence and central place in standard oncology care pathways. It holds around 25% of the share in 2025. According to official United States cancer statistics, female breast cancer continues to be one of the most commonly diagnosed cancers, underscoring the critical role of radiotherapy in both curative and adjuvant treatment regimens. Radiation therapy is widely used after breast-conserving surgery and in managing local and regional disease, making it a cornerstone in multidisciplinary care. Its broad clinical applicability, inclusion in national treatment guidelines, and frequent integration with systemic therapies contribute to the high volume of radiation procedures in this category. As cancer care continues to evolve toward precision and personalized medicine, breast cancer’s demand for advanced radiation modalities reinforces its position as the dominant application segment.

Lung cancer is the fastest-growing application category at a CAGR of 8.9% during the forecast period, driven by an expanding role for high-precision radiotherapy in both early-stage and advanced disease. Official lung cancer statistics from federal health authorities highlight that lung cancer causes more deaths than any other cancer type in the United States, reflecting its significant public health impact and unmet treatment need. As radiation technologies such as stereotactic techniques become more refined, clinicians increasingly employ radiotherapy for patients who are not surgical candidates, as well as for oligometastatic disease. Combined with broader adoption of imaging-guided approaches and integration with systemic therapies, this shift is expanding the use of radiation treatments in lung oncology. These dynamics position lung cancer as the fastest expanding application segment for radiation therapy in oncology.

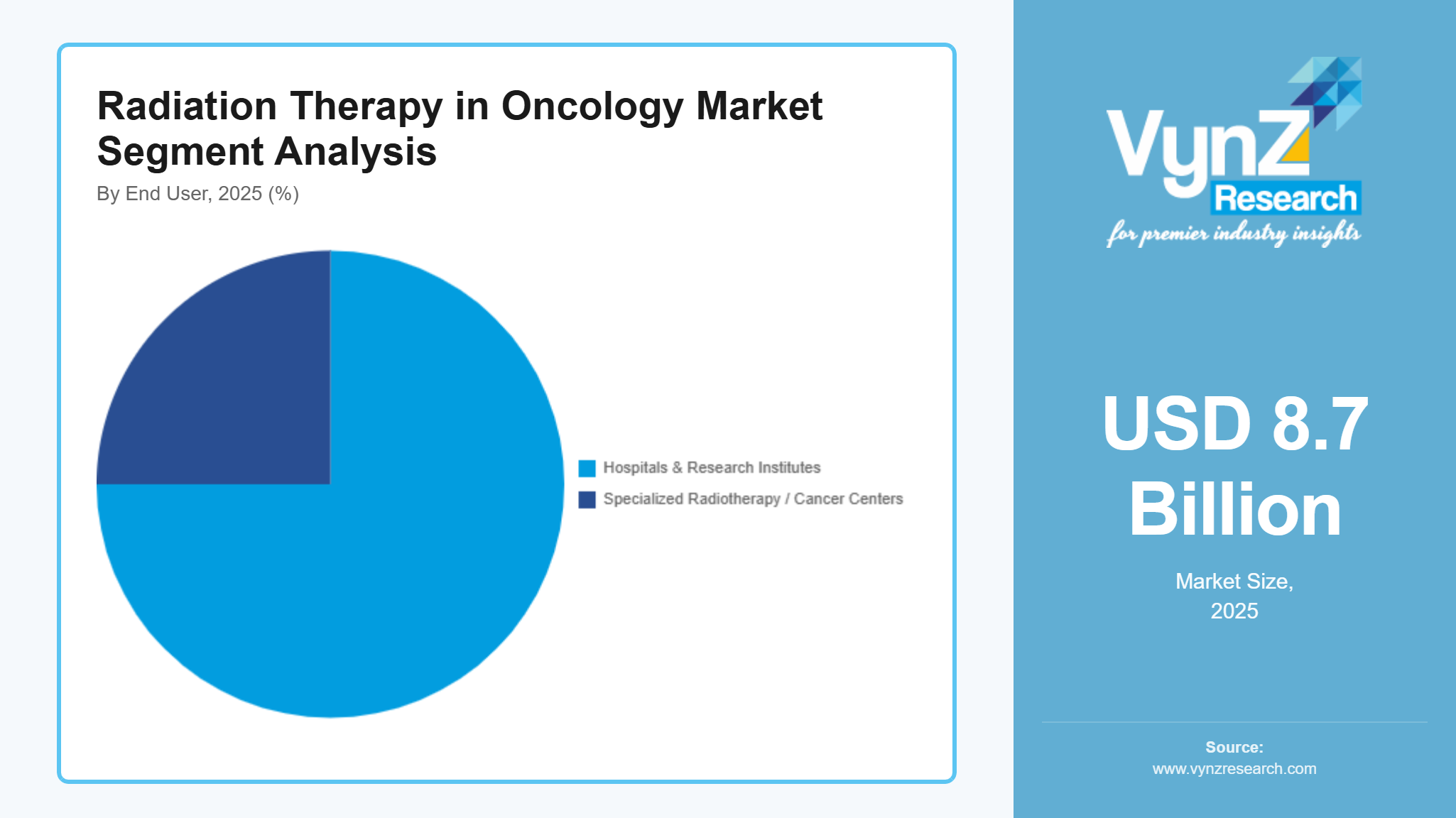

By End User

Hospitals and research institutes constitute the largest end-user category with a market share of about 75% in 2025 due to their integrated care capabilities and established role in cancer management. These institutions offer end-to-end oncology services, combining diagnostics, radiation therapy, medical oncology, and surgical care within a single clinical ecosystem. Their access to advanced treatment infrastructure, multidisciplinary clinical teams, and research-driven protocols enables them to manage complex and high-volume cancer cases efficiently. Hospitals also play a critical role in technology adoption, clinical training, and innovation, making them early adopters of advanced radiation techniques. Their ability to deliver comprehensive, high-acuity care positions hospitals and research institutes as the primary settings for radiation therapy delivery globally.

Specialized radiotherapy and cancer centers represent the fastest-growing end-user category, driven by the shift toward focused, patient-centric oncology care models. These centers are purpose-built for cancer treatment, allowing streamlined operations, reduced treatment timelines, and optimized use of radiation therapy technologies. Their specialized nature enables higher procedural efficiency, personalized care pathways, and improved patient experience compared to general hospital settings. As healthcare systems increasingly prioritize outpatient care and cost-effective service delivery, specialized centers are expanding rapidly across both developed and emerging markets. Their agility, scalability, and exclusive focus on oncology make them a key growth driver in the evolving radiation therapy landscape.

Regional Insights

Asia Pacific

Asia Pacific is the fastest-growing region in the radiation therapy in oncology market, fueled by demographic shifts, increasing cancer awareness, and rapid healthcare system expansion. Governments across the region are scaling oncology infrastructure to address rising patient volumes, particularly in densely populated countries. Improvements in diagnostic reach, hospital capacity, and specialist training are accelerating the adoption of radiation therapy as a core cancer treatment modality. The region’s growth is also supported by modernization initiatives aimed at improving treatment efficiency and accessibility. These dynamics position Asia Pacific as the most significant growth engine for radiation therapy over the coming years.

Europe

Europe maintains a strong and stable position in the radiation therapy in oncology market, driven by publicly funded healthcare systems and coordinated cancer control strategies. The region emphasizes equitable access, standardized treatment protocols, and multidisciplinary oncology care, ensuring consistent demand for radiation therapy services. Long-term investments in healthcare infrastructure and professional training have supported widespread adoption of modern radiotherapy techniques. While market expansion is more measured compared to emerging regions, Europe’s focus on quality, safety, and clinical integration sustains its importance. The region remains a key contributor to innovation, clinical research, and best-practice development in radiation oncology.

North America

North America represents the largest regional market for radiation therapy in oncology, held approx. 35% of market share in 2025, supported by a highly developed healthcare ecosystem and long-standing integration of radiotherapy into standard cancer care. The region benefits from early adoption of advanced treatment technologies, strong clinical expertise, and established care pathways across hospitals and specialized cancer centers. Comprehensive insurance coverage, structured oncology guidelines, and close collaboration between clinical research and care delivery have enabled consistent utilization of radiation therapy across cancer types. As a result, North America continues to set benchmarks in treatment sophistication, operational scale, and clinical outcomes, reinforcing its leadership position in the global radiation therapy landscape.

Rest of the World

The rest of the world, encompassing Latin America, the Middle East, and Africa, represents an emerging and opportunity-driven market for radiation therapy in oncology. Many countries within these regions are strengthening cancer care frameworks as non-communicable diseases gain higher public health priority. Expansion of urban healthcare facilities, targeted oncology investments, and international collaborations are gradually improving access to radiotherapy services. However, adoption levels vary widely due to differences in infrastructure, workforce availability, and funding capacity. Despite these challenges, growing policy focus on cancer treatment and long-term healthcare sustainability is creating momentum for radiation therapy deployment. As systems evolve, these regions offer meaningful opportunities for capacity building, technology integration, and long-term market development.

Competitive Landscape / Company Insights

The radiation therapy in oncology market is moderately consolidated, led by a small group of global technology providers with strong engineering capabilities, extensive installed bases, and deep clinical integration. These players set industry benchmarks through continuous innovation, advanced treatment platforms, and comprehensive service offerings. Surrounding this core group is a diverse network of regional and specialized companies that focus on targeted solutions, software optimization, and cost-efficient systems designed for specific healthcare settings. Competitive differentiation is increasingly driven by treatment precision, workflow efficiency, digital integration, and long-term system performance rather than pricing alone. Partnerships with hospitals, cancer centers, and research institutions are shaping market positioning, particularly in regions expanding oncology infrastructure. As healthcare providers demand scalable, outcome-oriented solutions, companies that align technology innovation with clinical and operational reliability are strengthening their competitive advantage across the global radiation therapy landscape.

Mini Profiles

Siemens Healthineers AG is a global medical technology leader providing advanced imaging, diagnostics, and cancer therapy solutions. The company supports precision radiation therapy across the oncology care continuum through integrated, technology-driven platforms.

Elekta AB specializes in precision radiation therapy and radiosurgery solutions for cancer treatment. Its portfolio enables personalized, high-accuracy treatments across hospitals and specialized cancer centers worldwide.

Accuray Incorporated develops advanced radiotherapy systems designed to deliver highly precise, personalized radiation treatments. The company focuses on improving clinical accuracy, patient outcomes, and treatment efficiency.

Ion Beam Applications SA is a global provider of proton therapy systems and particle accelerator technologies for cancer treatment. The company enables highly targeted radiation delivery while minimizing exposure to healthy tissue.

Mevion Medical Systems, Inc. designs compact proton therapy solutions aimed at expanding access to advanced cancer treatment. Its systems combine precision, efficiency, and reduced infrastructure complexity.

Key Players

- Siemens Healthineers AG

- Elekta AB

- Accuray Incorporated

- Ion Beam Applications SA

- Hitachi High-Tech Corporation

- Carl Zeiss Meditec AG

- Mevion Medical Systems, Inc.

- Koninklijke Philips N.V.

- ViewRay Technologies, Inc.

- Sumitomo Heavy Industries, Ltd.

- Brainlab AG

- Eckert & Ziegler AG

Recent Developments

February 2026 - Mevion Medical Systems announced that its MEVION S250-FIT™ Proton Therapy System received CE Marking, enabling clinical use and marketing throughout the European Union. The compact proton therapy system is designed to fit into standard radiotherapy vaults, reducing infrastructure barriers.

January 2026 - Elekta AB announced that its Elekta Evo CT-Linac received U.S. Food and Drug Administration (FDA) 510(k) clearance, making the AI-enhanced imaging linear accelerator available to radiation oncology professionals across the United States. This clearance supports high-precision image-guided cancer treatments, reinforcing Elekta’s leadership in adaptive radiotherapy solutions.

November 2025 - Siemens Healthineers AG announced a strategic reorganization in which its diagnostics business will operate with more autonomy, while its precision therapy segment (including Varian radiotherapy business) will be positioned for focused growth. This structural change is intended to accelerate innovation and market responsiveness in oncology and related care areas.

March 2025 - Ion Beam Applications SA signed a term sheet with Apollo Hospitals for the installation of a Proteus ONE compact proton therapy system in India, with an option for a second system. This agreement will expand access to proton therapy technology in the Indian oncology market.

Global Radiation Therapy in Oncology Market Coverage

Radiation Type Insight and Forecast 2026 - 2035

- External Beam Radiation Therapy (EBRT)

- Internal Radiation Therapy (Brachytherapy)

- Systemic Radiation Therapy

Therapy Insight and Forecast 2026 - 2035

- Stereotactic Radiosurgery (SRS) / Stereotactic Body Radiotherapy (SBRT)

- Intensity-Modulated Radiation Therapy (IMRT)

- Image-Guided Radiation Therapy (IGRT)

- Volumetric-Modulated Arc Therapy (VMAT)

- Proton Beam Therapy (Proton Therapy)

- Brachytherapy

Application Insight and Forecast 2026 - 2035

- Breast Cancer

- Prostate Cancer

- Lung Cancer

- Colorectal Cancer

- Others

End User Insight and Forecast 2026 - 2035

- Hospitals & Research Institutes

- Specialized Radiotherapy / Cancer Centers

Global Radiation Therapy in Oncology Market by Region

- North America

- By Radiation Type

- By Therapy

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Radiation Type

- By Therapy

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Radiation Type

- By Therapy

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Radiation Type

- By Therapy

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Radiation Therapy in Oncology Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Radiation Type

1.2.2. By

Therapy

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Radiation Type

5.1.1. External Beam Radiation Therapy (EBRT)

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Internal Radiation Therapy (Brachytherapy)

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Systemic Radiation Therapy

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Therapy

5.2.1. Stereotactic Radiosurgery (SRS) / Stereotactic Body Radiotherapy (SBRT)

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Intensity-Modulated Radiation Therapy (IMRT)

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Image-Guided Radiation Therapy (IGRT)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Volumetric-Modulated Arc Therapy (VMAT)

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Proton Beam Therapy (Proton Therapy)

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.2.6. Brachytherapy

5.2.6.1. Market Definition

5.2.6.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Breast Cancer

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Prostate Cancer

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Lung Cancer

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Colorectal Cancer

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Others

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals & Research Institutes

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Specialized Radiotherapy / Cancer Centers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Radiation Type

6.2. By

Therapy

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Radiation Type

7.2. By

Therapy

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Radiation Type

8.2. By

Therapy

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Radiation Type

9.2. By

Therapy

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Siemens Healthineers AG

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Elekta AB

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Accuray Incorporated

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Ion Beam Applications SA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Hitachi High-Tech Corporation

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Carl Zeiss Meditec AG

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Mevion Medical Systems, Inc.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Koninklijke Philips N.V.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

ViewRay Technologies, Inc.

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Sumitomo Heavy Industries, Ltd.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Brainlab AG

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Eckert & Ziegler AG

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Radiation Therapy in Oncology Market