Digital Twin in Healthcare Market Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Component (Software, Hardware, Services), by Technology (AI and Machine Learning, Internet of Things IoT, Big Data Analytics, Blockchain Enabled Systems, Simulation and Modeling Platforms), by Application (Personalized Medicine, Drug Discovery and Development, Medical Device Design and Testing, Surgical Planning and Simulation, Clinical Workflow Optimization), by End User (Healthcare Providers, Pharmaceutical and Biotechnology Companies, Medical Device Manufacturers, Research and Academic Institutes)

| Status : Published | Published On : May, 2026 | Report Code : VRHC1341 | Industry : Healthcare | Available Format :

|

Page : 154 |

Digital Twin in Healthcare Market Overview

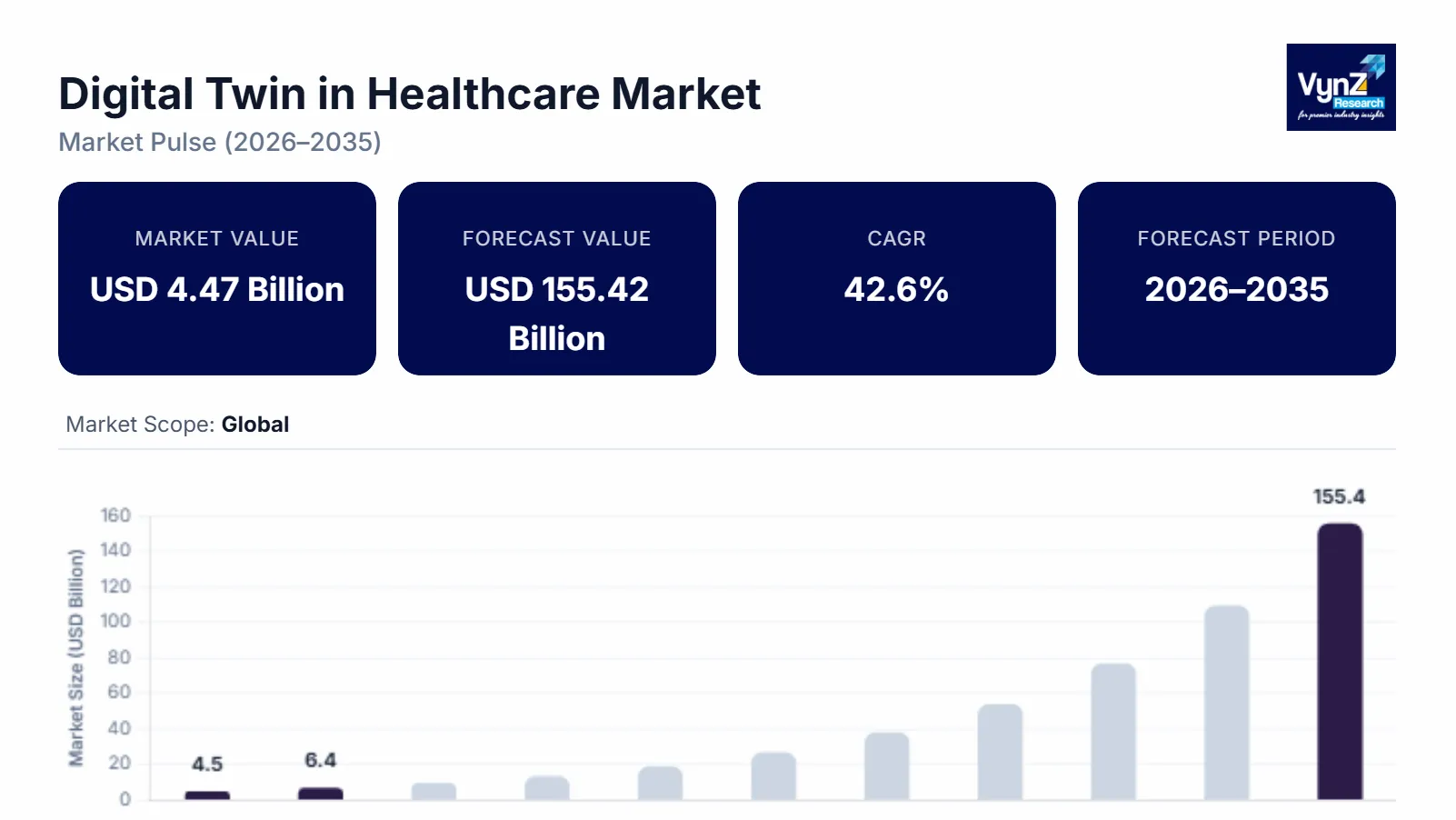

The Digital Twin in Healthcare market which was valued at approximately USD 4.47 billion in 2025 and is estimated to rise further up to almost USD 6.37 billion in 2026, is projected to reach around USD 155.42 billion in 2035, expanding at a CAGR of about 42.6% during the forecast period from 2026 to 2035.

The market grows due to the rising mix of AI based simulation models in healthcare systems along with the increasing demand for personalized and predictive medicine. Real time patient monitoring and virtual clinical environments are widely used. The World Health Organization notes that the global burden of chronic diseases is growing increasing the need for advanced digital health tools to support earlier diagnosis and treatment precision.

Government backed initiatives for healthcare digitization, the rising investments in smart hospital infrastructure and biomedical innovation promote broader market expansion. Public health agencies and national digital health programs are actively encouraging adoption of simulation-based healthcare technologies to improve clinical efficiency and reduce treatment costs. Collaboration between healthcare providers, pharmaceutical companies and technology firms scale deployment in North America, Europe and Asia Pacific.

Digital Twin in Healthcare Market Dynamics

Market Trends

The industry is moving fast mainly because healthcare simulation usage is shifting and real time patient data integration is getting more attention. This is due to the ongoing digital transformation across clinical systems. One big trend is the rising adoption of AI enabled virtual patient models, treatment personalization and smoother operational efficiency in healthcare services. Another trend is the integration of IoT enabled medical devices with predictive analytics platforms due to rapid digital penetration along with healthcare modernization initiatives. Government supported digital health programs and smart hospital initiatives are strengthening these trends. National healthcare systems are increasingly putting money into interoperable data infrastructure and simulation based clinical planning. Public health authorities are promoting digital innovation to improve care quality and reduce overall system burden. This is especially noticeable in North America, Europe, and Asia Pacific, where healthcare digitization programs are advancing quickly.

Growth Drivers

The market growth is largely supported by the rising demand for personalized medicine and predictive healthcare solutions, producing steady demand across hospitals, pharmaceutical research environments, and clinical decision support applications. Increasing investments in digital healthcare infrastructure and smart hospital development are speeding up overall market expansion. The growing adoption of AI driven healthcare analytics is boosting usage and healthcare providers and research institutions care more about patient outcomes, operational efficiency, and cost reduction, increasing the need for digital twin-based healthcare solutions. Government backed health innovation programs and concerns about rising global disease burden also reinforce this growth momentum.

Market Restraints / Challenges

The market still has hurdles that can slow things down. High implementation costs and complicated integration with existing hospital IT systems continues to limit adoption. This is most noticeable among small and mid-sized healthcare providers. Data privacy concerns, regulatory complexity and patient information management also restrain broader deployment. There are also operational constraints because providers and vendors depend on advanced computing infrastructure and on skilled data science professionals. Also, limited interoperability between older, legacy healthcare systems and newer simulation platforms can cause scalability issues.

Market Opportunities

The market has solid opportunities in personalized healthcare simulation and virtual clinical trial modeling driven by the increasing demand for precision medicine and early disease detection solutions. Companies that offer scalable and interoperable digital twin platforms should be well positioned because they can attract incremental demand from hospitals, research institutions, and pharmaceutical firms. Another opportunity involves AI integrated remote patient monitoring and predictive diagnostics. With rising investments in digital health ecosystems, new pathways are opening for better care delivery and less hospital burden. Advancements in cloud computing, machine learning, and real time analytics are also expected to improve clinical decision support, strengthen patient engagement, and support wider adoption across global healthcare systems.

Global Digital Twin in Healthcare Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 4.47 Billion |

|

Revenue Forecast in 2035 |

USD 155.42 Billion |

|

Growth Rate |

% |

|

Segments Covered in the Report |

Component, Technology, Application, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Ansys Inc, Dassault Systèmes, GE Healthcare, IBM Corporation, Koninklijke Philips N.V., Microsoft Corporation, NVIDIA Corporation, Rescale, Siemens Healthineers AG, Verto Health |

|

Customization |

Available upon request |

Digital Twin in Healthcare Market Segmentation

By Component

Software held the largest market share in 2025 with about 48% of total revenue due to wider deployment of simulation platforms AI enabled healthcare analytics and real time patient modeling tools spread across hospitals and research institutions. Government supported digital health programs and smart hospital initiatives keep pushing software especially in areas that already have advanced healthcare infrastructure and more structured clinical digitization moves.

Services are said to grow the quickest through the forecast window, with a projected CAGR of 44.2%, mainly because demand keeps rising for implementation support, system integration, plus managed digital twin solutions. Healthcare providers and pharmaceutical groups are increasingly deploying specialist service providers to lower day-to-day operational complexity.

By Technology

In 2025, AI and machine learning held roughly 32% market share playing a core role in predictive modeling, patient simulation, and diagnostic optimization inside digital twin ecosystems. Adoption is helped by computational efficiency and by its fit with large scale healthcare datasets. Government sponsored AI in healthcare efforts and public research funding programs are also reinforcing uptake around major innovation hubs.

Simulation and modeling platforms are forecasted to expand the fastest with a CAGR of 45.6%, supported by rising appetite for virtual clinical environments and real time physiological modeling. Internet of things enabled healthcare setups are likewise getting traction due to the growing use of connected medical devices for continuous patient monitoring.

By Application

Personalized medicine held the largest portion of the market in 2025 at around 36% due to the growing need for patient specific treatment planning and precision healthcare approaches. When digital twin models connect with genomic information and clinical records, treatment results get better while healthcare spending drop. Public health organizations keep putting emphasis on personalized care models as a major tactic for handling chronic disease burdens worldwide.

Surgical planning and simulation are expected to grow the fastest, with an estimated CAGR of 46.1%, driven by wider adoption of virtual surgery environments and AI based procedural modeling. Drug discovery and development use cases are also moving forward strongly since digital twin platforms are increasingly used to optimize clinical trials.

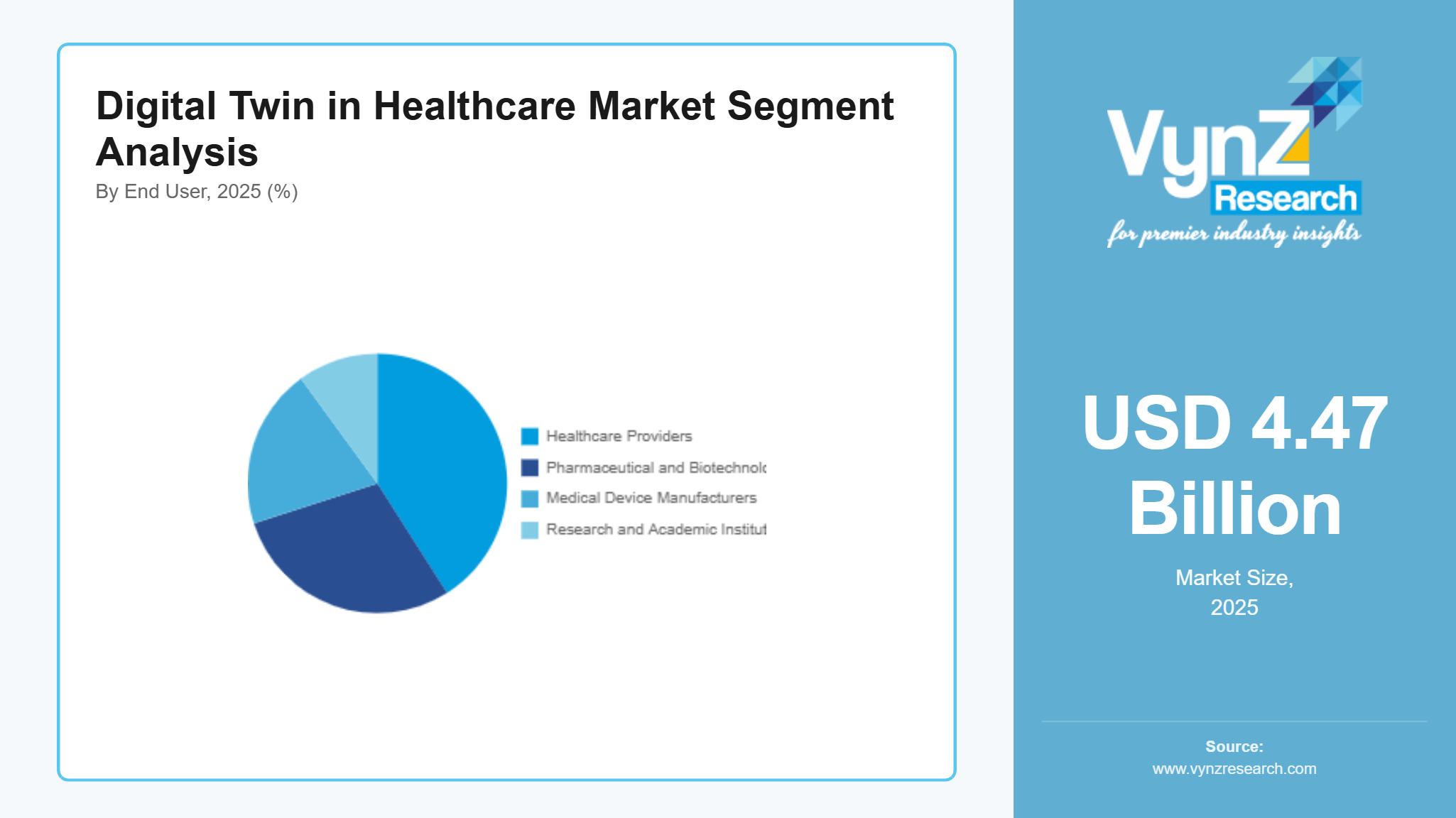

By End User

Healthcare providers accounted for the biggest share in 2025, roughly 41%, supported by broad adoption across hospitals, clinics, and integrated care networks. The push to improve patient outcomes, reduce operational inefficiencies and strengthen real time decision making is pulling deployments forward across healthcare delivery systems. Government supported smart hospital initiatives and digital health transformation programs are also making adoption stickier in advanced healthcare economies.

Pharmaceutical and biotechnology companies are projected to grow at the fastest pace, with a CAGR of 45.8%, driven by increased use of digital twin tech in drug discovery, clinical trial simulation, and precision medicine development. Medical device manufacturers are also adopting digital twin platforms for product testing, design optimization, research and innovation via advanced simulation-based healthcare research and collaborative projects.

Regional Insights

North America

In 2025, North America held 39% of the market due to stronger healthcare infrastructure, wider adoption of AI enabled clinical systems and heavy investment in digital health change. There are many innovation hubs across the United States and Canada promoting broad rollout of virtual patient modeling and simulation-oriented healthcare solutions. Government backed steps for healthcare digitization and precision medicine research promotes expansion and public health agencies and federal funding channels are encouraging predictive healthcare technologies integration.

Europe

Europe represented roughly 26% share in 2025, supported by more structured healthcare setups, solid regulatory frameworks, and steady spending on digital health modernization. Germany, the United Kingdom, and France lead through national level healthcare innovation programs and research funding efforts. Government driven initiatives push interoperability, data security and patient centric care, speeding up deployment of digital twin technologies. Collaboration between public healthcare bodies and technology providers is strengthening clinical simulation and personalized medicine adoption across the region.

Asia Pacific

Asia Pacific was about 22% in 2025 with rapid progress in healthcare infrastructure, growing digital transformation and expanded biomedical research spend. China, India, Japan, and South Korea are major contributors with government programs aimed at digital health ecosystems and smart hospital infrastructure. The national healthcare modernization along with rising adoption of AI integrated medical systems is boosting demand in a very noticeable way. Partnerships between healthcare providers, tech companies and research institutions are making regional adoption easier and helping innovation in digital twin applications.

Rest of the World

Rest of the World made up approximately 13% of the market in 2025 backed by gradual upgrades in healthcare infrastructure and more involvement in global digital health initiatives. The growth is fueled by higher awareness of advanced healthcare simulation tech and greater participation from international healthcare organizations in emerging markets. Government led healthcare modernization programs and early-stage digital transformation are improving adoption.

Competitive Landscape / Company Insights

The market is highly competitive with the presence of global technology providers, healthcare solution vendors and specialized digital health firms focusing on advanced simulation platforms, AI integration, and healthcare data interoperability solutions. Companies are increasingly investing in digital capabilities, cloud-based infrastructure and AI driven R&D to strengthen their market position. Government supported healthcare digitization initiatives and public funding for smart hospital development are encouraging innovation, while regulatory emphasis on patient data security, precision medicine, and interoperable health systems is further intensifying competition across developed and emerging healthcare markets.

Mini Profiles

Ansys Inc focuses on advanced simulation and modeling solutions for healthcare digital twin applications, supported by strong engineering analytics capabilities and wide adoption across medical device design and clinical simulation environments.

Dassault Systèmes operates in premium healthcare simulation and virtual modeling segments, emphasizing high precision 3D experience platforms and integrated lifecycle management solutions for biomedical research and healthcare innovation ecosystems.

GE Healthcare leverages global strategic partnerships and strong healthcare imaging infrastructure to expand market presence, enabling integration of digital twin technologies into diagnostic imaging, patient monitoring, and hospital workflow systems.

IBM Corporation focuses on AI driven healthcare analytics and digital twin platforms, supported by strong cloud computing infrastructure and enterprise level data integration capabilities across clinical and pharmaceutical research applications.

Koninklijke Philips N.V. operates in advanced healthcare technology solutions, emphasizing connected care systems and digital health platforms, supported by strong global distribution networks and hospital integrated patient monitoring ecosystems.

Key Players

- Ansys Inc

- Dassault

- Systèmes

- GE Healthcare

- IBM

- Koninklijke

- Philips N.V.

- Microsoft Corporation

- NVIDIA Corporation

- Rescale

- Siemens

- Healthineers

- AG

- Verto Health

Recent Developments

In February, 2025, Microsoft Corporation expanded its Azure-based healthcare digital twin capabilities by enhancing interoperability with clinical data systems and AI-driven simulation models. This helped healthcare providers improve patient outcome prediction and hospital workflow optimization.

In March, 2025, NVIDIA Corporation advanced its healthcare digital twin ecosystem by improving GPU-accelerated simulation frameworks for medical imaging and surgical planning. The company’s AI computing upgrades enabled more accurate real-time physiological modeling for precision medicine applications.

In January, 2026, Rescale strengthened its cloud-based computational platform by supporting high-fidelity digital twin simulations for healthcare and life sciences research. This development enabled faster biomedical modeling and improved scalability for complex clinical simulations.

In April, 2025, Siemens Healthineers AG enhanced its digital twin solutions for imaging and diagnostics by integrating AI-based predictive modeling into hospital systems. This allowed clinicians to simulate patient-specific scenarios for better diagnosis and treatment planning.

In May, 2025, Verto Health expanded its healthcare digital twin applications by improving real-time patient flow simulation tools for healthcare systems. This helped hospitals optimize capacity planning and reduce operational bottlenecks using predictive analytics.

Global Digital Twin in Healthcare Market Coverage

Component Insight and Forecast 2026 - 2035

- Software

- Hardware

- Services

Technology Insight and Forecast 2026 - 2035

- AI and Machine Learning

- Internet of Things IoT

- Big Data Analytics

- Blockchain Enabled Systems

- Simulation and Modeling Platforms

Application Insight and Forecast 2026 - 2035

- Personalized Medicine

- Drug Discovery and Development

- Medical Device Design and Testing

- Surgical Planning and Simulation

- Clinical Workflow Optimization

End User Insight and Forecast 2026 - 2035

- Healthcare Providers

- Pharmaceutical and Biotechnology Companies

- Medical Device Manufacturers

- Research and Academic Institutes

Global Digital Twin in Healthcare Market by Region

- North America

- By Component

- By Technology

- By Application

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Component

- By Technology

- By Application

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Component

- By Technology

- By Application

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Component

- By Technology

- By Application

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Digital Twin in Healthcare Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Component

1.2.2. By

Technology

1.2.3. By

Application

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Component

5.1.1. Software

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Hardware

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Services

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. AI and Machine Learning

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Internet of Things IoT

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Big Data Analytics

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Blockchain Enabled Systems

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Simulation and Modeling Platforms

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Personalized Medicine

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Drug Discovery and Development

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Medical Device Design and Testing

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Surgical Planning and Simulation

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Clinical Workflow Optimization

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Healthcare Providers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Pharmaceutical and Biotechnology Companies

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Medical Device Manufacturers

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Research and Academic Institutes

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Component

6.2. By

Technology

6.3. By

Application

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Component

7.2. By

Technology

7.3. By

Application

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Component

8.2. By

Technology

8.3. By

Application

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Component

9.2. By

Technology

9.3. By

Application

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Ansys Inc

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Dassault

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Systèmes

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

GE Healthcare

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

IBM

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Koninklijke

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Philips N.V.

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Microsoft Corporation

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

NVIDIA Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Rescale

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Siemens

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Healthineers

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

10.13.

AG

10.13.1.

Snapshot

10.13.2.

Overview

10.13.3.

Offerings

10.13.4.

Financial

Insight

10.13.5.

Recent

Developments

10.14.

Verto Health

10.14.1.

Snapshot

10.14.2.

Overview

10.14.3.

Offerings

10.14.4.

Financial

Insight

10.14.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Digital Twin in Healthcare Market