Europe Hand Sanitizer Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product Type (Gel, Liquid, Foam, Spray), by Composition (Alcohol Based, Non-Alcohol Based), by Distribution Channel (Supermarkets and Hypermarkets, Pharmacies and Drugstores, Convenience Stores, Online Retail, Other Distribution Channels), by End User (Hospitals and Clinics, Household, Corporate Offices, Educational Institutions, Hospitality, Industrial)

| Status : Published | Published On : Mar, 2026 | Report Code : VRHC1330 | Industry : Healthcare | Available Format :

|

Page : 143 |

Europe Hand Sanitizer Market Overview

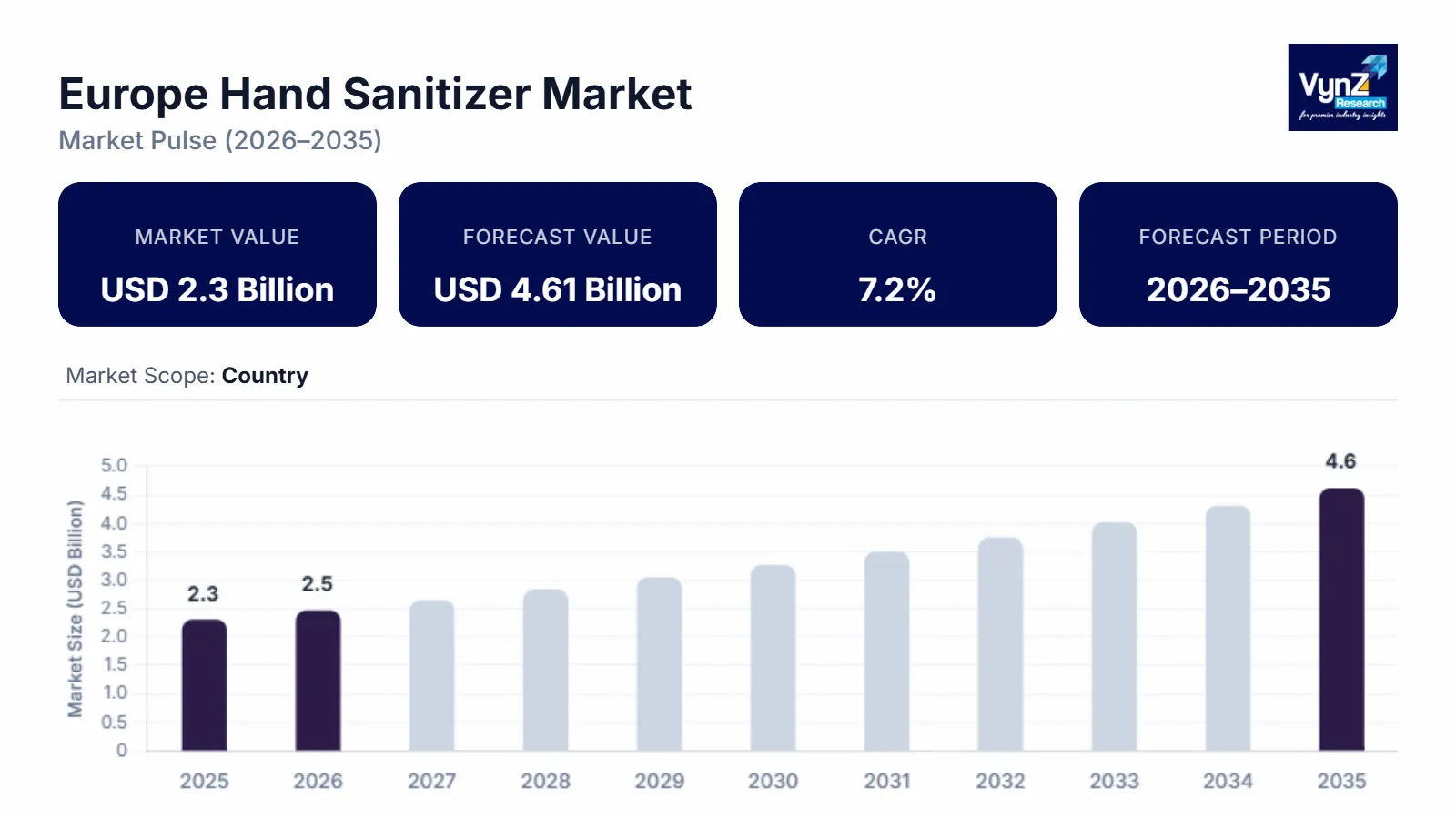

The Europe hand sanitizer market which was valued at approximately USD 2.3 billion in 2025 and is estimated to rise further up to almost USD 2.46 billion by 2026, is projected to reach around USD 4.61 billion in 2035, expanding at a CAGR of about 7.2% during the forecast period 2026 to 2035.

The Europe hand sanitizer market shows stable growth due to institutional procurement and infection prevention standards. Also, product quality regulations create stable market conditions across the entire region. The World Health Organization together with the European Centre for Disease Prevention and Control provided strategic guidance which designated alcohol-based hand rubs as the main method for reducing pathogen transmission in both clinical settings and community environments, thus establishing permanent consumption patterns throughout the entire region.

The market experiences growth because hospitals and long-term care facilities must follow stricter hygiene compliance standards while consumers increasingly adopt preventive healthcare practices. Also, the European Commission continues to enforce biocidal product standard monitoring. National public health systems maintain infection control policies which sustain demand through institutional channels in the United Kingdom National Health Service and German Federal Ministry of Health. Public hygiene awareness programs run by Santé Publique France will lead to ongoing public hygiene awareness programs which will enhance adoption across German healthcare facilities, educational institutions and commercial establishments in France and the United Kingdom.

Europe Hand Sanitizer Market Dynamics

Market Trends

The industry undergoes fundamental changes because it now demands two specific testing methods which need regulatory approval and two alcohol-based products which must prove their effectiveness against infection control measures established by the World Health Organization and European Centre for Disease Prevention and Control. The official hand hygiene guidelines demand hospitals and public institutions to use products which fulfill the alcohol requirements and follow the specified usage instructions because they need standard alcohol content and correct usage methods. The European Commission biocidal product framework encourages manufacturers to develop safe products through safety documentation and transparent product labeling and dermatological testing of their solutions. Healthcare and retail sectors now prefer sustainable packaging options which create skin-friendly products, resulting in new procurement practices.

Growth Drivers

The hand sanitizer market in Europe experiences growth because institutional hygiene requirements and healthcare readiness initiatives continue to operate throughout major economies. The National Health Service and Federal Ministry of Health work to establish infection control standards which hospitals and community healthcare facilities must follow. Rise in campaigns to raise awareness on hygiene among people and surveillance of public health by Santé Publique, France are also promoting consumer adherence to preventive sanitation practices.

Market Restraints / Challenges

The market experiences operational challenges because alcohol and packaging materials create price sensitivity problems which affect demand stability. European Commission biocidal regulations require manufacturers to spend more on documentation and testing processes which satisfy authorization needs. European Medicines Agency and national authorities require strict quality validation of all guidance documents which will increase operational costs for small producers. The healthcare sector may experience increased costs because of our dependence on imported ethanol and supply chain disruptions during peak healthcare periods.

Market Opportunities

The market presents opportunities for premium products which have undergone dermatological testing and eco-friendly formulations because public procurement frameworks now emphasize product safety and environmental sustainability. World Health Organization continues to promote hand hygiene compliance, which enables organizations to maintain their hygiene practices beyond emergency periods. Supermarkets and pharmacies now provide two new volume growth channels through their expanded digital retail platforms and private label products. Automated production processes together with certified manufacturing facilities in German, French and United Kingdom locations will improve supply resilience while meeting demand needs until 2035.

Europe Hand Sanitizer Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 2.3 Billion |

|

Revenue Forecast in 2035 |

USD 4.61 Billion |

|

Growth Rate |

7.2% |

|

Segments Covered in the Report |

Product Type, Composition, Distribution Channel, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

Germany, United Kingdom, France, Italy, Spain, Netherlands, Rest of Europe |

|

Key Companies |

3M Company, Beiersdorf AG, Colgate-Palmolive Company, Ecolab Inc., Henkel AG & Co. KGaA, Kimberly-Clark Corporation, Procter & Gamble Company, Reckitt Benckiser Group plc, SC Johnson & Son Inc., Unilever PLC |

|

Customization |

Available upon request |

Europe Hand Sanitizer Market Segmentation

By Product Type

The market in 2025 achieved its highest value through gel formulations which generated approximately 48% of total market revenue. The products maintain market leadership because they enable easy application and provide controlled dispensing while most consumers in homes and medical facilities already know how to use them. The World Health Organization has established clinical guidance which endorses the use of alcohol-based hand rubs that meet specific viscosity requirements. The segment maintains stability because pharmacies and supermarkets in Germany, France and the United Kingdom continue to purchase products without interruption.

The period from 2026 to 2035 will see liquid variants achieve the most rapid expansion with a predicted CAGR of 7.6%. The growth of the business sector between hospitals and commercial areas is supported by users who need cost-effective solutions which can absorb materials at a fast rate.

The foam and spray formats are experiencing moderate growth reaching about 6.4% because users find touch-free dispensing systems to be convenient for their offices and transportation stations.

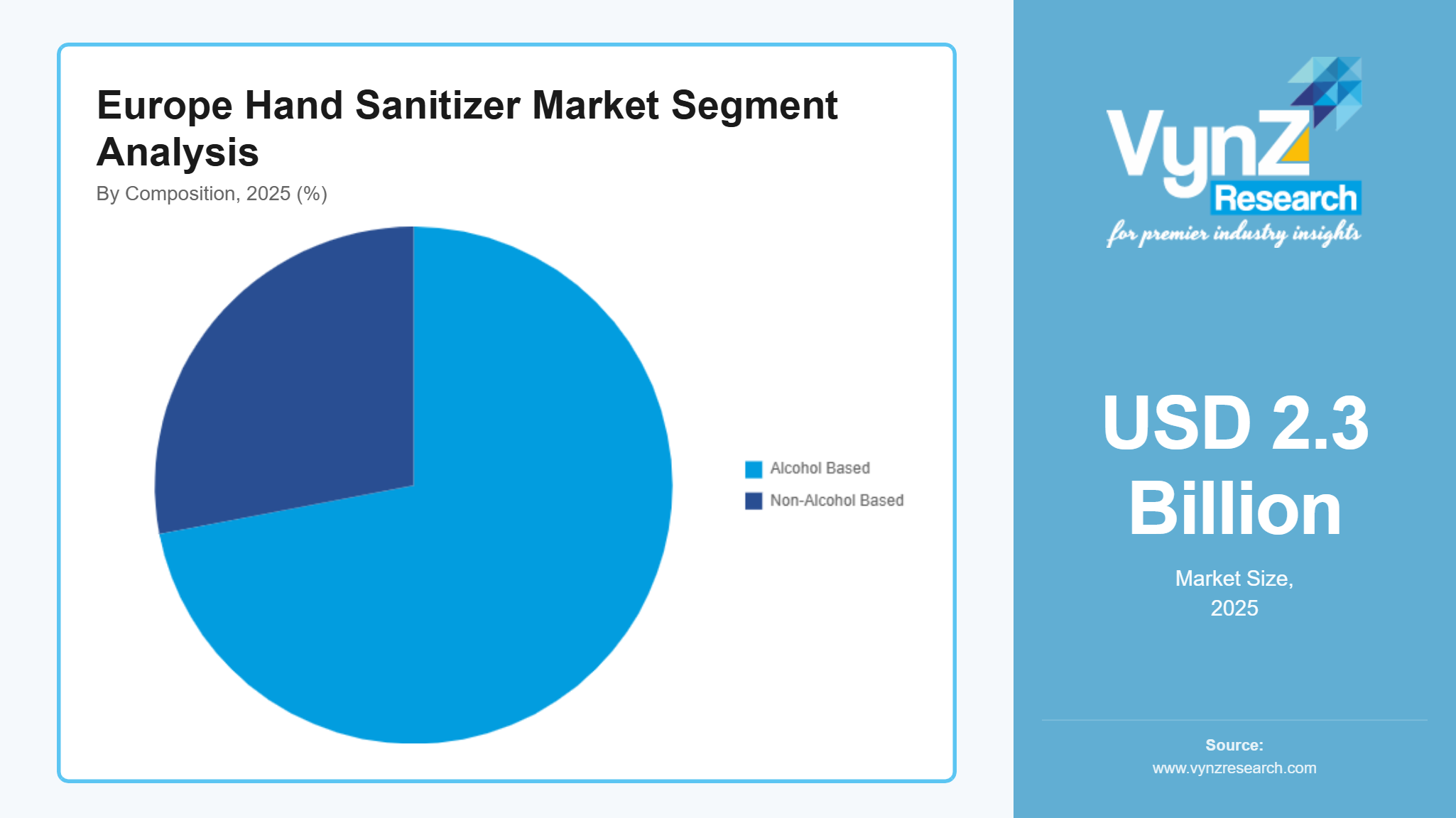

By Composition

The market in 2025 saw alcohol-based formulations achieve greater market share generating almost 72% of total revenue. The products maintain market leadership because the European Centre for Disease Prevention and Control establishes infection control requirements which organizations must follow according to European Commission biocidal regulations. The healthcare sector continues to endorse ethanol and isopropyl alcohol products because the medical community recognizes their effectiveness in clinical applications.

Non-alcohol-based products are expected to experience 6.8% CAGR growth until 2035 because more people desire skin-friendly products which are safe for children. Western European markets are expanding because consumers prefer low irritant solutions which they use in schools and homes.

By Distribution Channel

The distribution of revenue in 2025 showed supermarkets and hypermarkets as the primary distribution channel which generated approximately 41% of total market revenue. The retail sector offers customers high product visibility through its urban distribution network which enables them to make purchases at any time. The pharmacies and drugstores market segment achieves 6.9% growth because people trust medically approved products which pharmacists promote.

Online retail will achieve the most rapid expansion during the forecasting period with its business operations growing at an 8.1% CAGR. The online market expansion is powered by digital commerce platform growth which enables better last mile delivery and allows small companies to buy products in bulk.

The growth of convenience stores and other distribution channels remains consistent at approximately 6.1% because customers make unplanned purchases while traveling.

By End User

The revenue distribution in 2025 showed hospitals and clinics as the primary revenue generators which handled approximately 46% of total revenue. The healthcare system at National Health Service facilities maintains its high standard of infection control through its mandatory health protocols which the Federal Ministry of Health oversees. The healthcare sector uses more institutional cleaning supplies because all medical facilities need to maintain standard hygiene practices and execute continuous patient treatment.

Household consumption is expected to grow at a 7.4% CAGR between now and 2035 because people will maintain their hygiene practices through regular preventive health measures.

The corporate offices, educational institutions, hospitality and industrial facilities in Europe experience a 6.7% growth rate because national health campaigns and workplace safety regulations combine to protect public health.

Regional Insights

Germany

The sanitary product industry in Europe experienced its 2025 market share when Germany held 24% because its healthcare system functioned properly and its infection control procedures were enforced. The Federal Ministry of Health controls institutional demand through its hygienic standards which the EU health authority European Centre for Disease Prevention and Control established. Berlin, Munich, and Hamburg report ongoing hospital and long-term care facility supply activities throughout their major metropolitan areas. The growing pharmacy and retail chain networks improve product distribution to medical and consumer markets.

The United Kingdom

The United Kingdom represents nearly 21% of the regional market in 2025, driven by structured public health policies and centralized healthcare procurement. The National Health Service uses its infection prevention system to match World Health Organization requirements which helps clinics and hospitals maintain their supply needs. Cities like London, Manchester, and Birmingham experience growing hygiene awareness in their commercial offices and educational institutions and transportation networks which supports market growth. The market for household users is experiencing steady growth because more people are shopping through online retail channels.

France

France holds an 18% market share in 2025 because its public hygiene initiatives and Santé Publique France led surveillance programs back its market presence. National infection prevention strategies and compliance with regulatory standards under the European Commission sustain institutional adoption across hospitals and long-term care centers. The Paris, Lyon, and Marseille regions of France particularly value workplace hygiene because their hospitality, retail, and corporate sectors demand more services.

The three countries Germany, the United Kingdom, and France will generate about 63% of total regional revenue for 2025 while Italy, Spain, the Netherlands, and other European countries not covered in this section will share the remaining revenue.

Competitive Landscape / Company Insights

The Europe hand sanitizer market operates at a moderate level of competition because international and regional companies concentrate their efforts on developing new product formulas while meeting regulatory standards and expanding their distribution networks. The company invests in three main areas which include developing alcohol-based products that have passed dermatological tests and creating sustainable packaging and building automated production facilities to improve their operational performance. The World Health Organization hygiene compliance frameworks and European Commission regulatory standards both support certified manufacturing practices which help healthcare and retail businesses improve their market position through better competitive advantages.

Mini Profiles

3M Company focuses on healthcare grade disinfectants and alcohol-based sanitization solutions, supported by extensive distribution networks, industrial expertise, and strong brand credibility across European medical and institutional procurement channels.

Beiersdorf AG operates in mass and premium personal care segments, emphasizing dermatological safety, skin compatibility, and consumer trust through established pharmacy presence and strong retail brand positioning.

Colgate-Palmolive Company leverages global supply chain integration and established oral and personal hygiene portfolios to expand sanitization offerings across supermarkets, pharmacies, and digital retail platforms in Europe.

Ecolab Inc. focuses on institutional hygiene and infection prevention systems, supported by service driven solutions, technical compliance expertise, and long-term contracts with hospitals and commercial facilities.

Henkel AG & Co. KGaA operates across consumer and professional hygiene segments, emphasizing formulation innovation, regulatory compliance, and broad retail distribution strength within the European sanitation landscape.

Key Players

- 3M Company

- Beiersdorf AG

- Colgate-Palmolive Company

- Ecolab Inc.

- Henkel AG & Co. KGaA

- Kimberly-Clark Corporation

- Procter & Gamble Company

- Reckitt Benckiser Group plc

- SC Johnson & Son Inc.

- Unilever PLC

Recent Developments

In January 2026, WHO Foundation and Colgate-Palmolive have collaborated to support World Health Organization oral health initiatives. This collaboration will increase public awareness of oral health as a public health priority by promoting its integration into national health systems to provide communities with dental health services and education.

In January 2026, Ecolab and CDP have launched the Water Use Efficiency Index which is a new data-driven tool designed to help businesses measure, benchmark, and improve operational water performance. Announced at the World Economic Forum in Davos 2026, this partnership aims to address accelerating water scarcity by providing sector-specific targets for improved water management.

In November 2025, Kimberly-Clark Corporation and Kenvue Inc. has signed an agreement under which Kimberly-Clark shall acquire all of the outstanding shares of Kenvue common stock in a cash and stock transaction that values Kenvue at an enterprise value of approximately USD 48.7 billion. This transaction brings together two iconic American companies to create a combined portfolio of complementary products. The combined company, with teams of talented people around the globe, will harness a superior commercial engine fueled by strategic customer partnerships, category-defining growth, industry-leading science and innovation, a differentiated digital model, best-in-class marketing and a culture of operating excellence – to unlock the full potential of the combination and better meet the evolving needs of consumers.

Europe Hand Sanitizer Market Coverage

Product Type Insight and Forecast 2026 - 2035

- Gel

- Liquid

- Foam

- Spray

Composition Insight and Forecast 2026 - 2035

- Alcohol Based

- Non-Alcohol Based

Distribution Channel Insight and Forecast 2026 - 2035

- Supermarkets and Hypermarkets

- Pharmacies and Drugstores

- Convenience Stores

- Online Retail

- Other Distribution Channels

End User Insight and Forecast 2026 - 2035

- Hospitals and Clinics

- Household

- Corporate Offices

- Educational Institutions

- Hospitality

- Industrial

Europe Hand Sanitizer Market by Region

- Germany

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- U.K.

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- France

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- Italy

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- Spain

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- Russia

- By Product Type

- By Composition

- By Distribution Channel

- By End User

- Rest of Europe

- By Product Type

- By Composition

- By Distribution Channel

- By End User

Table of Contents for Europe Hand Sanitizer Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product Type

1.2.2. By

Composition

1.2.3. By

Distribution Channel

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Europe Market Estimate and Forecast

4.1. Europe Market Overview

4.2. Europe Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product Type

5.1.1. Gel

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Liquid

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Foam

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Spray

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Composition

5.2.1. Alcohol Based

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Non-Alcohol Based

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Distribution Channel

5.3.1. Supermarkets and Hypermarkets

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Pharmacies and Drugstores

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Convenience Stores

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Online Retail

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Other Distribution Channels

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Hospitals and Clinics

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Household

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Corporate Offices

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Educational Institutions

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.4.5. Hospitality

5.4.5.1. Market Definition

5.4.5.2. Market Estimation and Forecast to 2035

5.4.6. Industrial

5.4.6.1. Market Definition

5.4.6.2. Market Estimation and Forecast to 2035

6. Germany Market Estimate and Forecast

6.1. By

Product Type

6.2. By

Composition

6.3. By

Distribution Channel

6.4. By

End User

7. U.K. Market Estimate and Forecast

7.1. By

Product Type

7.2. By

Composition

7.3. By

Distribution Channel

7.4. By

End User

8. France Market Estimate and Forecast

8.1. By

Product Type

8.2. By

Composition

8.3. By

Distribution Channel

8.4. By

End User

9. Italy Market Estimate and Forecast

9.1. By

Product Type

9.2. By

Composition

9.3. By

Distribution Channel

9.4. By

End User

10. Spain Market Estimate and Forecast

10.1. By

Product Type

10.2. By

Composition

10.3. By

Distribution Channel

10.4. By

End User

11. Russia Market Estimate and Forecast

11.1. By

Product Type

11.2. By

Composition

11.3. By

Distribution Channel

11.4. By

End User

12. Rest of Europe Market Estimate and Forecast

12.1. By

Product Type

12.2. By

Composition

12.3. By

Distribution Channel

12.4. By

End User

13. Company Profiles

13.1.

3M Company

13.1.1.

Snapshot

13.1.2.

Overview

13.1.3.

Offerings

13.1.4.

Financial

Insight

13.1.5.

Recent

Developments

13.2.

Beiersdorf AG

13.2.1.

Snapshot

13.2.2.

Overview

13.2.3.

Offerings

13.2.4.

Financial

Insight

13.2.5.

Recent

Developments

13.3.

Colgate-Palmolive Company

13.3.1.

Snapshot

13.3.2.

Overview

13.3.3.

Offerings

13.3.4.

Financial

Insight

13.3.5.

Recent

Developments

13.4.

Ecolab Inc.

13.4.1.

Snapshot

13.4.2.

Overview

13.4.3.

Offerings

13.4.4.

Financial

Insight

13.4.5.

Recent

Developments

13.5.

Henkel AG & Co. KGaA

13.5.1.

Snapshot

13.5.2.

Overview

13.5.3.

Offerings

13.5.4.

Financial

Insight

13.5.5.

Recent

Developments

13.6.

Kimberly-Clark Corporation

13.6.1.

Snapshot

13.6.2.

Overview

13.6.3.

Offerings

13.6.4.

Financial

Insight

13.6.5.

Recent

Developments

13.7.

Procter & Gamble Company

13.7.1.

Snapshot

13.7.2.

Overview

13.7.3.

Offerings

13.7.4.

Financial

Insight

13.7.5.

Recent

Developments

13.8.

Reckitt Benckiser Group plc

13.8.1.

Snapshot

13.8.2.

Overview

13.8.3.

Offerings

13.8.4.

Financial

Insight

13.8.5.

Recent

Developments

13.9.

SC Johnson & Son Inc.

13.9.1.

Snapshot

13.9.2.

Overview

13.9.3.

Offerings

13.9.4.

Financial

Insight

13.9.5.

Recent

Developments

13.10.

Unilever PLC

13.10.1.

Snapshot

13.10.2.

Overview

13.10.3.

Offerings

13.10.4.

Financial

Insight

13.10.5.

Recent

Developments

14. Appendix

14.1. Exchange Rates

14.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Europe Hand Sanitizer Market