AI Data Center Cooling Market Size & Share Growth Forecast Report (2026-2035)

Industry Insight by Cooling Type (Air Cooling, Liquid Cooling, Hybrid Cooling Systems), by Data Center Type (Hyperscale Data Centers, Colocation Data Centers, Enterprise Data Centers, Edge Data Centers), by Cooling Component (Cooling Units, Chillers, Air Handling Units, Pumps, Heat Exchangers), by End User (Cloud Service Providers, Colocation Providers, Enterprises, Government & Defense)

| Status : Published | Published On : May, 2026 | Report Code : VRSME9211 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 143 |

AI Data Center Cooling Market Overview

The AI Data Center Cooling market which was valued at approximately USD 12.6 billion in 2025 and is estimated to rise further up to almost USD 14.4 billion by 2026, is projected to reach around USD 49.6 billion by 2035, expanding at a CAGR of about 14.7% during the forecast period from 2026 to 2035.

Market growth is driven by more hyperscale data center expansion, higher AI and GPU-led workload density and the demand for energy efficient thermal management systems, the shift toward liquid cooling and immersion cooling types. The demand for high performance computing infrastructure keeps rising and so do investments in national digital infrastructure and green data center programs, backing market expansion throughout key regions like the United States, China and Germany. As per the U.S. Department of Energy and the European Commission’s data center energy efficiency guidance, governments are really pushing low carbon cooling solutions to cut down the ICT sector energy consumption.

AI Data Center Cooling Market Dynamics

Market Trends

The market is going through noticeable shifts, especially in how people are choosing cooling tech and their procurement patterns. Users are moving fast toward liquid cooling and immersion cooling setups to ensure better energy efficiency, stronger heat removal and lower operational costs for high density AI computing workloads. AI driven thermal management and predictive cooling optimization is happening due to digital infrastructure automation and hyperscale data center expansion. Guidance from the U.S. Department of Energy and European Commission data center energy efficiency frameworks urges operators to adopt advanced cooling intelligence systems pushing firms toward integrated cooling architectures and energy optimized infrastructure solutions.

Growth Drivers

Market growth is driven by the rapid rise in AI compute workloads, increasing the demand across hyperscale and colocation settings all over the world. More capital is being put into data center infrastructure expansion across North America, Asia Pacific and Europe, pushing the market further. Rising emphasis on energy efficiency and sustainability compliance increases adoption as cloud providers, enterprises and AI developers aim for cost efficiency, better thermal performance, and regulatory compliance. The demand for more advanced cooling systems should stay solid through the forecast period as government backed digital infrastructure and energy efficiency programs are also helping deployments.

Market Restraints / Challenges

The market faces problems in installation and high operating expenses of liquid cooling infrastructure. Retrofitting is difficult which reduces profitability and makes adoption harder in deployments where budgets are tight. Manufacturers and data center operators get hit with supply chain dependency for advanced cooling components and specialized engineering requirements. Relying on skilled thermal engineering expertise and on advanced materials create cost pressure and delay the deployment timeline, especially when large scale AI infrastructure gets rolled out.

Market Opportunities

Openings in AI optimized, energy efficient data center infrastructure however push then market as AI model training demand rises and hyperscale cloud expansion keeps widening. Vendors that can deliver scalable, modular, and high-performance cooling solutions are in a good position to meet the demand from cloud providers, colocation operators, and large enterprises. Another opportunity lies in the next generation liquid cooling ecosystems and smart thermal management platforms. With more investments flowing into AI infrastructure, demand for automated and predictive cooling optimization systems is getting stronger. Developments in digital twins, IoT based monitoring and AI driven energy optimization are expected to raise operational efficiency and increase adoption across data center networks globally.

Global AI Data Center Cooling Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 12.6 Billion |

|

Revenue Forecast in 2035 |

USD 49.6 Billion |

|

Growth Rate |

14.7% |

|

Segments Covered in the Report |

Cooling Type, Data Center Type, Cooling Component, End User |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Asia Pacific, Europe, Rest of the World |

|

Key Companies |

Alphabet Inc. (Google), Amazon Web Services (AWS), Asetek, Carrier Global Corporation, CoolIT Systems, Dell Technologies, Hewlett Packard Enterprise (HPE), Huawei Technologies Co., Ltd., Intel Corporation, Schneider Electric |

|

Customization |

Available upon request |

AI Data Center Cooling Market Segmentation

By Cooling Type

Air cooling took the lead with about 46% share in 2025, basically because of older, legacy setups everywhere, lower upfront installation costs and compatibility with the existing data center infrastructure and offering long term scalability.

Liquid cooling should move the quickest, with an estimated CAGR near 18.9% during 2026 to 2035, mainly as hyperscale players and AI training data centers increasingly adopt it to manage heat loads. Hybrid cooling is also picking up, usually through phased infrastructure upgrades and some cost management approaches.

By Data Center Type

Hyperscale data centers held around 39% in 2025 due to vast AI workload processing, ongoing cloud expansion and huge infrastructure spending from major technology firms. Furthermore, capacity additions keep coming and AI model training.

Edge data centers are projected to grow the fastest, with a CAGR around 20.3% during 2026 to 2035, largely because low latency computing demand is rising, IoT is expanding, and distributed AI processing is becoming more common. Colocation data centers are seeing solid momentum as well because enterprises keep outsourcing more to gain cost benefits and scalability.

By Cooling Component

Cooling units accounted for the largest share, about 33% in 2025, because they play a critical role in keeping the thermal balance stable in high density computing environments. Chillers stay important, especially in large scale facilities that need centralized cooling control.

Heat exchangers are forecast to grow at the fastest pace, with a CAGR around 19.7% during 2026 to 2035 due to wider adoption of liquid cooling systems and because more energy recovery mechanisms are being integrated. Pumps and air handling units keep seeing steady demand across both retrofit projects and fresh deployments.

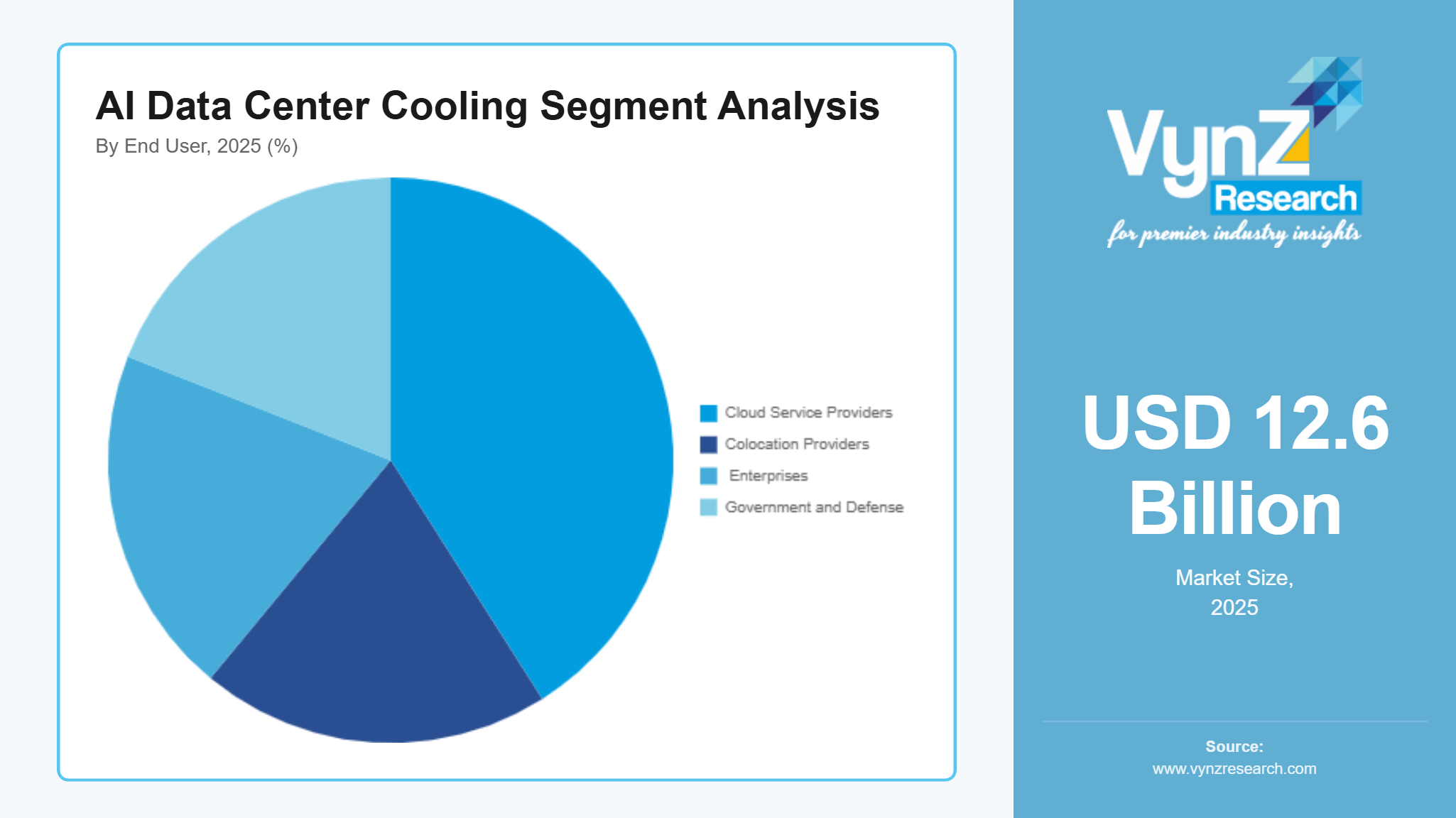

By End User

Cloud service providers led with roughly 41% in 2025, mainly driven by huge hyperscale infrastructure expansion and fast AI workload deployment across worldwide cloud platforms. Colocation providers contribute heavily as well, since enterprises increasingly outsource data center operations to improve cost efficiency and scalability.

Government & defense is projected to show the fastest growth, with a CAGR near 20.8% during 2026 to 2035, driven by rising investments in sovereign cloud infrastructure, national AI programs and secure data center expansion initiatives. Enterprises continue adopting advanced cooling systems to support AI driven digital transformation.

Regional Insights

North America

North America accounted for approximately 42% of the market in 2025, driven by strong hyperscale data center concentration, early AI infrastructure adoption and large-scale cloud computing expansion across the United States and Canada. Key data center hubs such as Virginia, Texas and California continue to dominate demand due to high density AI workloads and continuous expansion of hyperscale facilities. Government backed digital infrastructure and energy efficiency programs, including initiatives referenced by the U.S. Department of Energy, are accelerating deployment of advanced cooling technologies such as liquid cooling and immersion systems. Rising enterprise focus on reducing energy consumption and improving thermal efficiency is further strengthening adoption, while expansion of cloud service providers and colocation operators continues to reinforce regional leadership.

Asia Pacific

Asia Pacific accounted for approximately 28% of the market in 2025, supported by rapid digital transformation, increasing hyperscale data center construction and strong government investment in AI and cloud infrastructure across China, India, Japan and Singapore. The region is witnessing strong demand for high efficiency cooling systems due to rising AI compute workloads and expansion of cloud service ecosystems. Government supported digital economy programs and national data center development policies are significantly accelerating adoption of advanced cooling technologies. Increasing investments by regional hyperscalers and telecom operators are further strengthening infrastructure growth, while energy efficiency mandates and sustainability initiatives are encouraging transition toward liquid and hybrid cooling solutions across new facilities.

Europe

Europe accounted for approximately 19% of the market in 2025, driven by strict environmental regulations, strong focus on energy efficiency and increasing deployment of AI enabled cloud infrastructure across Germany, the United Kingdom, France and the Nordics. Data center operators in the region are prioritizing low carbon and energy optimized cooling systems due to stringent EU climate neutrality targets. Government backed initiatives under the European Commission and national digital infrastructure programs are encouraging adoption of advanced cooling technologies, including liquid and hybrid systems. Rising enterprise demand for sustainable IT infrastructure and compliance with ESG standards is further strengthening market growth, while modernization of existing data centers continues to support steady adoption.

Rest of the World

Rest of the world accounted for approximately 11% of the market in 2025, driven by emerging digital infrastructure development across the Middle East, Latin America and Africa, along with increasing data center investments in GCC countries such as UAE and Saudi Arabia. Growth is supported by rising cloud adoption, telecom expansion and early-stage AI infrastructure deployment. Government led smart city programs and digital transformation initiatives are encouraging establishment of modern data centers with energy efficient cooling systems.

Competitive Landscape / Company Insights

The market is moderately to highly competitive with the presence of global and regional players focusing on product innovation, high efficiency cooling technologies and geographic expansion across hyperscale and colocation data center ecosystems. Companies are increasingly investing in R&D, digital capabilities and AI driven thermal management systems to strengthen their market position. Competition is intensifying as demand rises for liquid cooling, immersion cooling and hybrid systems in AI intensive workloads. Government backed energy efficiency and digital infrastructure programs referenced by agencies such as the U.S. Department of Energy and European Commission are further encouraging adoption of advanced cooling solutions, increasing competitive pressure among vendors globally.

Mini Profiles

Alphabet Inc. (Google) focuses on hyperscale data center infrastructure and AI optimized cooling ecosystems, supported by strong global cloud network, advanced engineering capabilities, and high brand recognition in digital infrastructure markets.

Amazon Web Services (AWS) operates in premium cloud computing segments, emphasizing large scale data center performance, energy efficiency, and customized AI workload optimization across global hyperscale infrastructure environments.

Asetek leverages liquid cooling technology innovation and strategic partnerships with data center operators to expand market presence, supported by advanced thermal management solutions and strong expertise in immersion cooling systems.

Carrier Global Corporation focuses on advanced HVAC and data center cooling systems, supported by global distribution strength, energy efficient product portfolio, and strong industrial brand recognition across infrastructure markets.

CoolIT Systems operates in niche liquid cooling segments, emphasizing high performance direct-to-chip cooling solutions, customization for AI workloads, and strong integration with hyperscale data center architectures.

Key Players

- Alphabet Inc. (Google)

- Amazon Web Services (AWS)

- Asetek

- Carrier Global Corporation

- CoolIT Systems

- Dell Technologies

- Hewlett Packard Enterprise (HPE)

- Huawei Technologies Co., Ltd.

- Intel Corporation

- Schneider Electric

Recent Developments

In May 2026, Microsoft Corporation advanced its AI data center cooling strategy by scaling deployment of microfluidic chip cooling systems designed for high-density AI workloads. The enhancement significantly improves thermal efficiency in GPU-heavy environments and supports next-generation AI infrastructure expansion.

In March 2026, Google Cloud upgraded its AI data center infrastructure with enhanced liquid cooling integration across hyperscale facilities. The development focuses on reducing energy consumption while improving compute density for AI model training and inference workloads.

In March 2026, Amazon Web Services (AWS) expanded its AI data center program “Titus” with advanced liquid cooling and optimized power architectures. The initiative improves rack-level efficiency and supports rapid deployment of high-performance AI servers.

In April 2026, IBM strengthened its hybrid cloud data center infrastructure by integrating AI-optimized thermal management systems. The upgrade enhances workload balancing across enterprise data centers while improving cooling efficiency for large-scale AI operations.

In April 2026, NVIDIA Corporation enhanced its AI infrastructure ecosystem by collaborating with data center partners to deploy advanced direct-to-chip cooling solutions for next-generation GPUs. The initiative improves thermal performance and enables higher AI compute density across global deployments.

Global AI Data Center Cooling Market Coverage

Cooling Type Insight and Forecast 2026 - 2035

- Air Cooling

- Liquid Cooling

- Hybrid Cooling Systems

Data Center Type Insight and Forecast 2026 - 2035

- Hyperscale Data Centers

- Colocation Data Centers

- Enterprise Data Centers

- Edge Data Centers

Cooling Component Insight and Forecast 2026 - 2035

- Cooling Units

- Chillers

- Air Handling Units

- Pumps

- Heat Exchangers

End User Insight and Forecast 2026 - 2035

- Cloud Service Providers

- Colocation Providers

- Enterprises

- Government & Defense

Global AI Data Center Cooling Market by Region

- North America

- By Cooling Type

- By Data Center Type

- By Cooling Component

- By End User

- By Country - U.S., Canada, Mexico

- Europe

- By Cooling Type

- By Data Center Type

- By Cooling Component

- By End User

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Cooling Type

- By Data Center Type

- By Cooling Component

- By End User

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Cooling Type

- By Data Center Type

- By Cooling Component

- By End User

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for AI Data Center Cooling Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Cooling Type

1.2.2. By

Data Center Type

1.2.3. By

Cooling Component

1.2.4. By

End User

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Cooling Type

5.1.1. Air Cooling

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Liquid Cooling

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Hybrid Cooling Systems

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Data Center Type

5.2.1. Hyperscale Data Centers

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Colocation Data Centers

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Enterprise Data Centers

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Edge Data Centers

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.3. By Cooling Component

5.3.1. Cooling Units

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Chillers

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Air Handling Units

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Pumps

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Heat Exchangers

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.4. By End User

5.4.1. Cloud Service Providers

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Colocation Providers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Enterprises

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Government & Defense

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Cooling Type

6.2. By

Data Center Type

6.3. By

Cooling Component

6.4. By

End User

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Cooling Type

7.2. By

Data Center Type

7.3. By

Cooling Component

7.4. By

End User

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Cooling Type

8.2. By

Data Center Type

8.3. By

Cooling Component

8.4. By

End User

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Cooling Type

9.2. By

Data Center Type

9.3. By

Cooling Component

9.4. By

End User

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Alphabet Inc. (Google)

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Amazon Web Services (AWS)

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Asetek

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Carrier Global Corporation

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

CoolIT Systems

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Dell Technologies

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Hewlett Packard Enterprise (HPE)

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Huawei Technologies Co., Ltd.

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

Intel Corporation

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Schneider Electric

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

AI Data Center Cooling Market