Asia Pacific TIC Market for Building & Construction Industry Size & Share | Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (In-house, Outsourced), by Service Type (Testing, Inspection, Certification), by Industry Vertical (Building Materials, Infrastructure & Capital Equipment, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 145 |

Asia Pacific TIC Market for Building & Construction Industry Overview

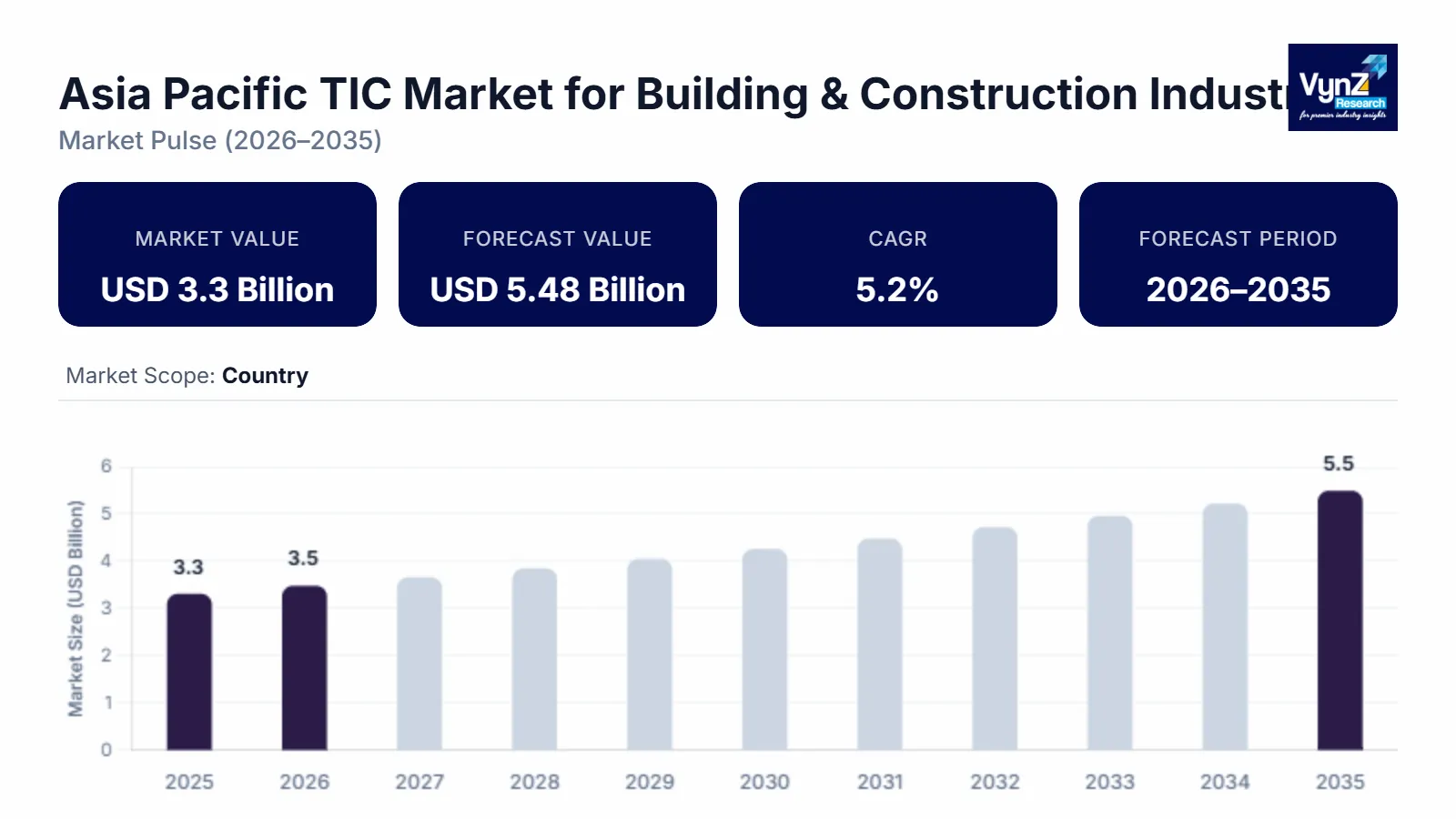

The Asia Pacific TIC market for building and construction industry which had a value of about USD 3.3 billion in 2025, will reach almost USD 3.47 billion by 2026, and will expand to approximately USD 5.48 billion in 2035, which represents a CAGR of about 5.2% during the timeframe of 2026 to 2035.

The market expansion will occur because safety regulations will be enforced more strictly while green building certifications will be adopted more widely and urban areas will grow, plus digital technologies such as AI and IoT will enable automatic inspection and monitoring capabilities. The market growth throughout major regions which include China, India, and Southeast Asia, results from increasing needs for certified building materials and current funding of smart city projects and government infrastructure programs. The market receives additional support from regional government regulations and sustainability programs which governments and organizations implement to encourage construction projects that meet high-quality standards.

Asia Pacific TIC Market for Building & Construction Industry Dynamics

Market Trends

The industry is experiencing substantial technological changes which include new inspection standards that meet the requirements of governmental control systems. The market develops through digital inspection tool implementation and AI-enabled monitoring system adoption, which make construction projects more efficient and improve building quality. The trend of adopting green building certifications emerges as national sustainability programs and urban development policies drive building certification implementation. Companies now focus on value-added TIC solutions because these solutions help them achieve better competitive advantage while maintaining consistent project standards across all major initiatives.

Growth Drivers

The market grows because construction safety regulations and building quality control rules are enforced more stringently which creates permanent demand for residential and commercial construction projects. The market expansion is driven by increased funding for smart city projects and infrastructure development. The market sees growing demand because developers choose certified building products and real-time inspection services to fulfill building code regulations and performance standards which will continue through the entire forecast period. Infrastructure projects which receive government support and construction safety programs at the regional level drive this pattern.

Market Restraints / Challenges

The market has attractive growth potential but it must overcome various obstacles which will hinder its progress. The price fluctuations of testing instruments and the requirement to use foreign inspection equipment cause profitability problems for businesses that operate in budget-sensitive markets. Organizations experience operational challenges because they lack skilled technical staff members and face multiple government regulations about their inspection procedures.

Market Opportunities

The market offers growth potential through modular inspection services and digital inspection services which benefit from increased urbanization and industrial growth throughout the Asia Pacific region. Integrated TIC solution providers who also deliver custom inspection services will meet upcoming demand from major infrastructure developers and government projects. The market expects automated inspection tool development and smart monitoring platform creation to improve operational efficiency while shortening project delivery times and establishing strong bonds with clients for long-lasting business success.

Asia Pacific TIC Market for Building & Construction Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 3.3 Billion |

|

Revenue Forecast in 2035 |

USD 5.48 Billion |

|

Growth Rate |

5.2% |

|

Segments Covered in the Report |

By Sourcing Type, By Service Type, By Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Indonesia, Thailand, Malaysia, Philippines, Vietnam, Rest of Asia |

|

Key Companies |

ALS Limited, Applus+, Bureau Veritas, DEKRA SE, DNV, Element Materials Technology, Eurofins Scientific, Intertek Group plc, Lloyd's Register, SGS Group |

|

Customization |

Available upon request |

Asia Pacific TIC Market for Building & Construction Industry Segmentation

By Sourcing Type

The market for third-party outsourcing services reached its maximum value in 2025 when it generated around 45% of total segment revenue. The method maintains its leading position because it suits both extensive construction work and ongoing requirements for meeting building standards. The inspection and certification processes which receive government support through standardization programs create a situation where third-party sourcing becomes the preferred method for both commercial and residential construction projects.

The forecast period will see stable growth for in-house services which will expand at a rate of 5.6% CAGR between 2026 and 2035. The combination of internal quality control systems with ongoing project oversight and digital inspection tool implementation drives the growth of this industry. The usage of hybrid sourcing models that combine in-house staff with external expert partners drives continuous growth especially within urban infrastructure and smart city initiatives.

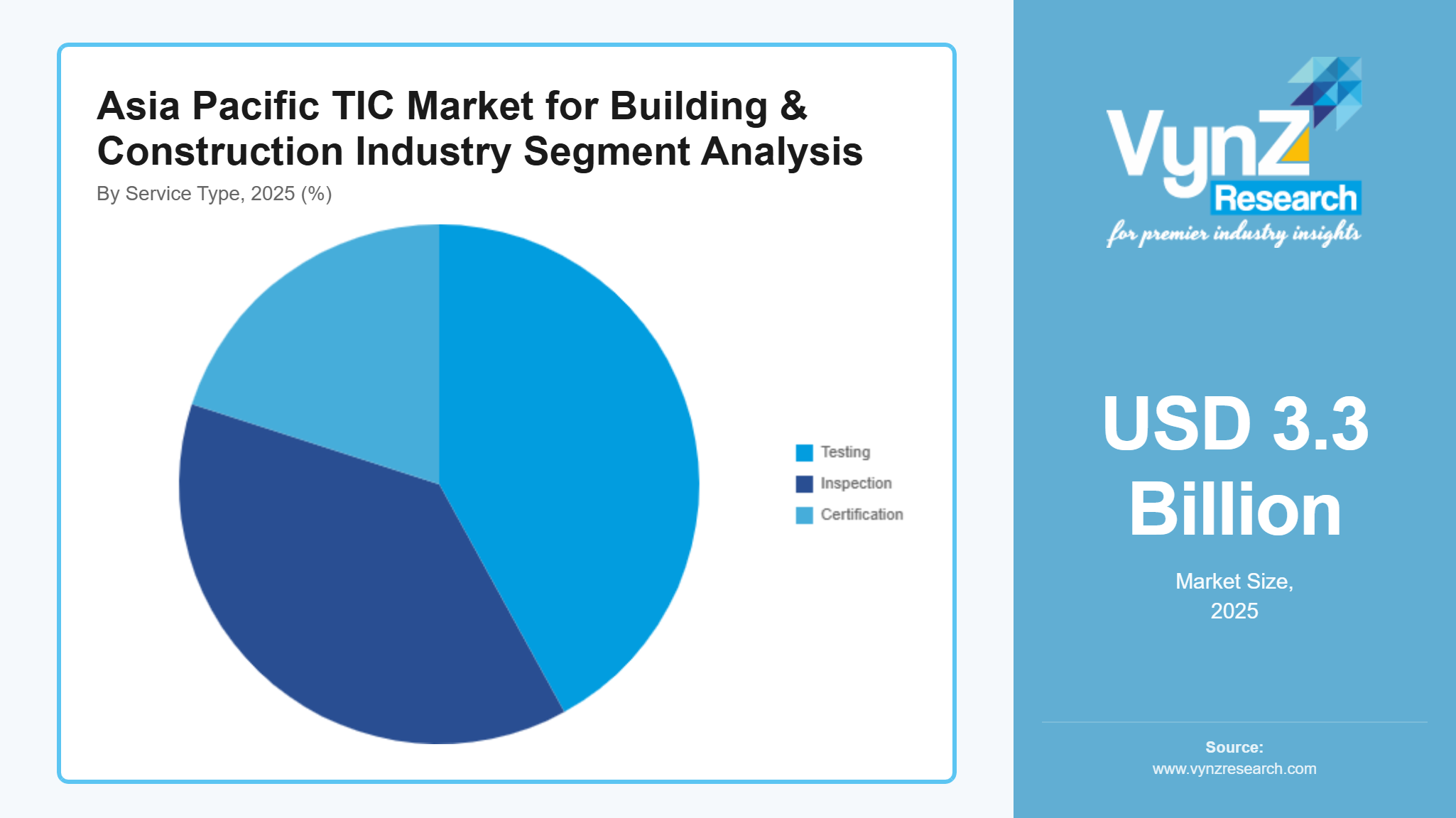

By Service Type

The inspection services industry maintained its dominant market position in 2025 by securing approximately 42% of the total segment revenue. The construction projects require safety verification and regulatory compliance testing along with technical validation procedures which create high demand for these services. The Asia Pacific markets implement national and regional systems which establish standardized inspection methods and quality control processes to support their inspection and monitoring activities.

During the period from 2026 to 2035 testing services will achieve the highest market growth rate when they reach an estimated CAGR of 5.8%. The market expansion success stems from technological progress made in both automated testing and non-destructive testing methods along with material compliance standards and increased regulatory enforcement. Certification services which include both green building certification and sustainability compliance services continue to grow through public-private partnerships and government sustainability initiatives.

By Industry Vertical

The commercial segment held the largest share in 2025, estimated at approximately 40% of total market revenue. The method maintains its leading position because it suits both extensive construction work and ongoing requirements for meeting building standards.

The residential segment will expand at the fastest rate between 2026 and 2035 when it achieves an estimated CAGR of 6.1%. The combination of increased housing requirements and urban renewal projects together with public housing development programs drives market growth. Government smart city initiatives together with educational and healthcare infrastructure investments and construction project quality assessment requirements create additional business potential in industrial and institutional projects.

Regional Insights

China

The market in 2025 showed 32% of its market share coming from China because urban development and major infrastructure development and strict construction safety regulations were being enforced. Market expansion continues because major cities such as Beijing, Shanghai and Guangzhou maintain high demand levels for their products.

The combination of government initiatives which support smart city development and sustainable building practices together with increasing adoption of certified inspection and testing services leads to greater investment in TIC solutions. The regional market performance improves through the development of digital inspection platforms together with AI-enabled monitoring tool integration.

India

The market share of India reached 22% in 2025. The current building activities for both residential and commercial spaces combined with urban redevelopment projects which the government backs and industrial infrastructure development create the regional growth. The major urban centers of Mumbai, Bangalore and Delhi show an increasing demand pattern.

Advanced TIC services deployment receives support through the Smart Cities Mission which provides investment incentives for sustainable construction practices. The market continues to expand because developers now understand the importance of quality assurance and safety compliance and risk mitigation all three elements for their projects.

Japan

The Japanese market represented 12% of the total market in 2025. The region achieves growth because industrial facilities modernize and urban infrastructure redevelopment occurs and construction safety and quality regulations reach their peak standards. The major cities of Tokyo, Osaka and Yokohama function as the principal centers for TIC adoption.

The government-backed programs which promote earthquake-resilient buildings and smart infrastructure systems together with industrial safety standards create a need for inspection and testing and certification services. The combination of digital monitoring system implementation together with automated testing solution deployment will boost operational efficiency while creating a stable market environment for the long run.

Rest of Asia Pacific

The market share for 2025 showed the Rest of Asia Pacific area which includes Southeast Asian countries and Oceania regions accounted for 12% of total market value. The current industrial development and urbanization along with large commercial and residential project investments are driving the market. The key cities of Jakarta, Bangkok and Sydney show an increasing trend toward adopting TIC services.

The government programs which support sustainable construction and regional safety standards and public-private infrastructure projects create a stronger demand for construction services. The market demand for the remaining products exists outside of China, India and Japan. This market segment represents emerging markets and underserved markets which can achieve rapid growth over the upcoming years.

Competitive Landscape / Company Insights

The market operates with a competitive environment that ranges from moderate to high, as both global and regional companies concentrate their efforts on service innovation, quality assurance and geographic market expansion. Companies are strengthening their market position through increased investment in digital inspection platforms, automated testing solutions and workforce training programs. Government-backed infrastructure programs and regulatory compliance frameworks are encouraging players to enhance technical capabilities, adopt advanced monitoring tools, and implement sustainable TIC solutions across residential, commercial, and industrial projects.

Mini Profiles

ALS Limited focuses on comprehensive inspection, testing, and certification services, supported by strong regional presence, advanced laboratories, and technical expertise, enabling consistent service quality and client trust across the Asia Pacific market.

Applus+ operates in premium TIC segments, emphasizing performance, safety compliance, and integrated solutions. Their extensive technical network and digital platforms enhance service delivery across construction, infrastructure, and industrial projects.

Bureau Veritas leverages global certifications, technical expertise, and strategic partnerships to expand market presence. The company emphasizes quality assurance, safety audits, and regulatory compliance for diverse building and construction projects.

DEKRA SE focuses on inspection, testing, and certification services with strong brand recognition and operational efficiency. They provide customized solutions for building safety, industrial compliance, and environmental standards in APAC.

DNV operates in niche TIC segments, emphasizing risk management, sustainability, and digital solutions. Their technical competence and consulting expertise support regulatory compliance and long-term performance across construction and infrastructure projects.

Key Players

- ALS Limited

- Applus+

- Bureau Veritas

- DEKRA SE

- DNV

- Element Materials Technology

- Eurofins Scientific

- Intertek Group plc

- Lloyd's Register

- SGS Group

Recent Developments

DEKRA SE reported in December 2025 that it celebrated its 100th anniversary with continued mid‑single‑digit revenue growth in its TIC business, emphasizing resilience across volatile economic conditions and a stable core performance. The company also reaffirmed its strategic focus on digital trust services and sustainability offerings as part of its Strategy 2030+ growth priorities.

Eurofins Scientific released its 2025 annual report in February 2026, highlighting strong global network expansion and organic growth across multiple testing services. The report underscored double‑digit growth in APAC environment testing, supported by expanded laboratory capacity and acquisitions in Korea and Japan.

SGS Group completed the acquisition of Applied Technical Services (ATS) in January 2026, enhancing its specialized testing, inspection, calibration, and forensics capacities and reinforcing its global TIC footprint. SGS also advanced climate solutions in November 2025 by acquiring a majority stake in a Paris‑based carbon accounting platform, strengthening its ESG service delivery.

Intertek Group plc announced in May 2025 the acquisition of TESIS, a high‑quality testing and conformity assessment provider, expanding its building products and construction TIC services in Brazil and emerging markets. In September 2025, it further expanded its footprint in Australia with the acquisition of Envirolab, enhancing environmental testing capacities and sustainability solutions.

TUV SUD was listed as a certified body under the Textile Exchange in June 2025, enabling it to issue sustainability certifications (RCS/GRS) across Bangladesh, India, and Vietnam and strengthen its compliance services in textile supply chains. This development expanded TÜV SÜD’s service offerings in the growing sustainability‑driven certification segment of the TIC market across Asia Pacific.

Asia Pacific TIC Market for Building & Construction Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- In-house

- Outsourced

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Industry Vertical Insight and Forecast 2026 - 2035

- Building Materials

- Infrastructure & Capital Equipment

- Others

Asia Pacific TIC Market for Building & Construction Industry by Region

- China

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Japan

- By Sourcing Type

- By Service Type

- By Industry Vertical

- India

- By Sourcing Type

- By Service Type

- By Industry Vertical

- South Korea

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Vietnam

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Thailand

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Malaysia

- By Sourcing Type

- By Service Type

- By Industry Vertical

- Rest of Asia-Pacific

- By Sourcing Type

- By Service Type

- By Industry Vertical

Table of Contents for Asia Pacific TIC Market for Building & Construction Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Asia Market Estimate and Forecast

4.1. Asia Market Overview

4.2. Asia Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. In-house

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Outsourced

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Building Materials

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Infrastructure & Capital Equipment

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Others

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

6. China Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

7. Japan Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

8. India Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

9. South Korea Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

10. Vietnam Market Estimate and Forecast

10.1. By

Sourcing Type

10.2. By

Service Type

10.3. By

Industry Vertical

11. Thailand Market Estimate and Forecast

11.1. By

Sourcing Type

11.2. By

Service Type

11.3. By

Industry Vertical

12. Malaysia Market Estimate and Forecast

12.1. By

Sourcing Type

12.2. By

Service Type

12.3. By

Industry Vertical

13. Rest of Asia-Pacific Market Estimate and Forecast

13.1. By

Sourcing Type

13.2. By

Service Type

13.3. By

Industry Vertical

14. Company Profiles

14.1.

ALS Limited

14.1.1.

Snapshot

14.1.2.

Overview

14.1.3.

Offerings

14.1.4.

Financial

Insight

14.1.5.

Recent

Developments

14.2.

Applus+

14.2.1.

Snapshot

14.2.2.

Overview

14.2.3.

Offerings

14.2.4.

Financial

Insight

14.2.5.

Recent

Developments

14.3.

Bureau Veritas

14.3.1.

Snapshot

14.3.2.

Overview

14.3.3.

Offerings

14.3.4.

Financial

Insight

14.3.5.

Recent

Developments

14.4.

DEKRA SE

14.4.1.

Snapshot

14.4.2.

Overview

14.4.3.

Offerings

14.4.4.

Financial

Insight

14.4.5.

Recent

Developments

14.5.

DNV

14.5.1.

Snapshot

14.5.2.

Overview

14.5.3.

Offerings

14.5.4.

Financial

Insight

14.5.5.

Recent

Developments

14.6.

Element Materials Technology

14.6.1.

Snapshot

14.6.2.

Overview

14.6.3.

Offerings

14.6.4.

Financial

Insight

14.6.5.

Recent

Developments

14.7.

Eurofins Scientific

14.7.1.

Snapshot

14.7.2.

Overview

14.7.3.

Offerings

14.7.4.

Financial

Insight

14.7.5.

Recent

Developments

14.8.

Intertek Group plc

14.8.1.

Snapshot

14.8.2.

Overview

14.8.3.

Offerings

14.8.4.

Financial

Insight

14.8.5.

Recent

Developments

14.9.

Lloyd's Register

14.9.1.

Snapshot

14.9.2.

Overview

14.9.3.

Offerings

14.9.4.

Financial

Insight

14.9.5.

Recent

Developments

14.10.

SGS Group

14.10.1.

Snapshot

14.10.2.

Overview

14.10.3.

Offerings

14.10.4.

Financial

Insight

14.10.5.

Recent

Developments

15. Appendix

15.1. Exchange Rates

15.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia Pacific TIC Market for Building & Construction Industry