US TIC Market for Sports and Entertainment Industry Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Sourcing Type (Outsourced sourcing, In-house sourcing), by Service Type (Testing, Inspection, Certification), by Industry Vertical (Sports infrastructure, Entertainment venues), by End Use (Stadium operators, Event organizers, Facility management companies, Regulatory authorities)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 131 |

US TIC Market for Sports and Entertainment Industry Overview

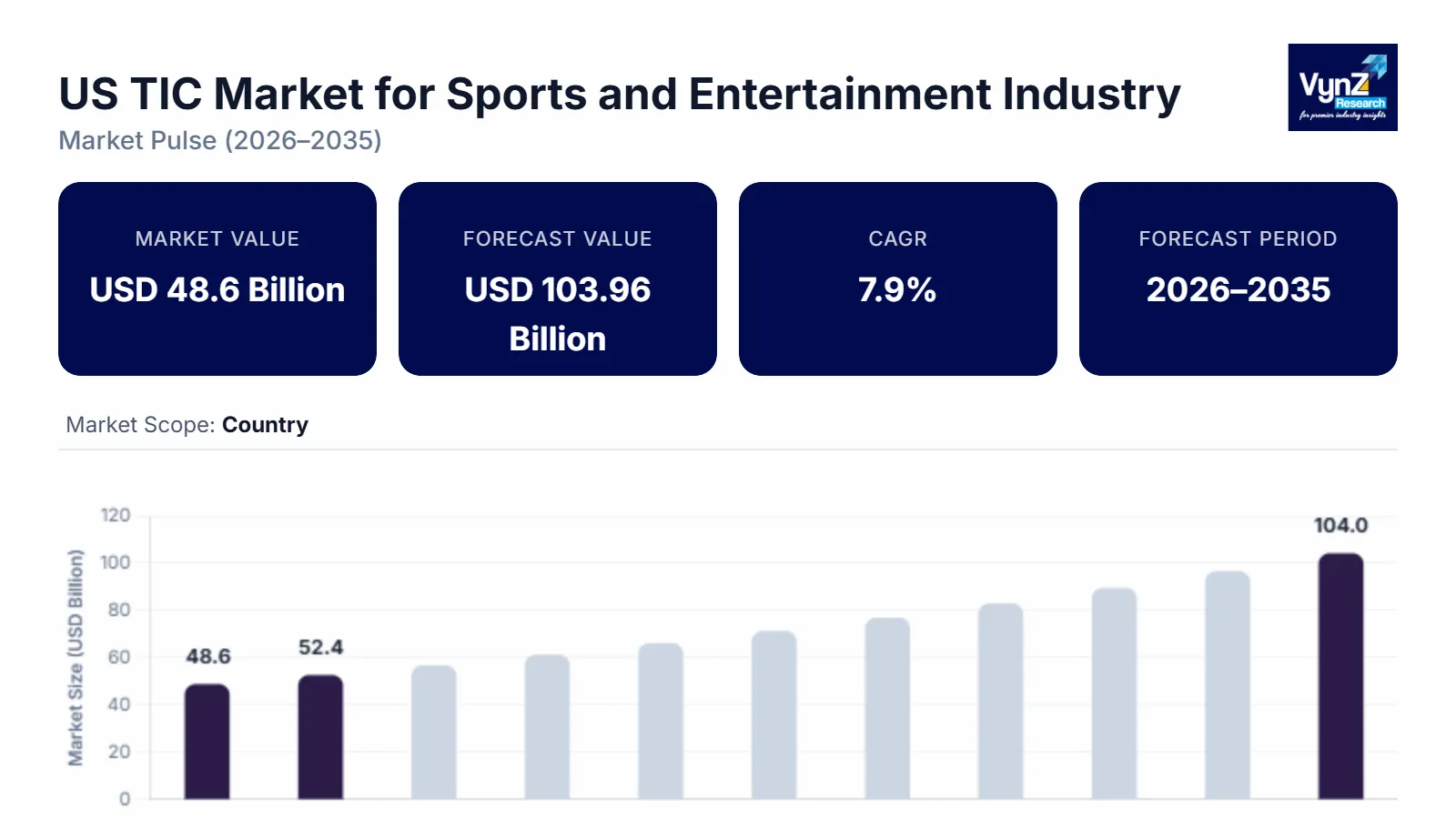

The U.S. TIC market for sports and entertainment industry which was valued at approximately USD 48.6 billion in 2025 and is estimated to rise further up to almost USD 52.44 billion by 2026, is projected to reach around USD 103.96 billion by 2035, expanding at a CAGR of about 7.9% during the forecast period from 2026 to 2035.

The market expansion is due to three factors which include the implementation of stricter regulations for sports facilities, the growing need for certified safety verification at major entertainment centers, and the increased use of modern inspection and testing technologies. The industry is expanding because event ecosystems now use digital monitoring systems, automated certification frameworks, and real-time safety analytics to create better safety standards. The rising focus on standardized safety governance in high-capacity public venues is significantly reinforcing demand for structured TIC services.

The international safety and occupational risk management frameworks require mass gathering environments to follow preventive compliance methods which results in stronger inspection and certification standards for the entire sector. The government-led modernization of sports infrastructure through smart stadium initiatives and large-scale public venue upgrades drives the increased adoption of TIC solutions. The strong regulatory enforcement together with infrastructure investments in North America, urban centers continue to push the sports and entertainment TIC market forward.

US TIC Market for Sports and Entertainment Industry Dynamics

Market Trends

The industry is migrating toward digital compliance verification, real-time safety monitoring and federal and occupational safety framework-based integrated certification workflows. Automated inspection systems together with data-driven compliance solutions get more usage because of U.S. workplace safety standards together with large-venue risk management rules. The current transition shows that sports and entertainment venues have increased their focus on transparency and crowd safety and infrastructure security which leads them to use testing and certification technologies for better operational efficiency and regulatory compliance.

The growing adoption of smart stadium technology and AI monitoring systems results from public event infrastructure undergoing digital transformation. The TIC sector service delivery models change because businesses now concentrate on developing predictive risk assessment tools, automated inspection platforms and integrated safety certification ecosystems. The U.S. sports and entertainment TIC industry undergoes competitive changes because federal infrastructure modernization and public safety frameworks require organizations to execute continuous monitoring and standardized compliance.

Growth Drivers

The industry growth depends on increasing regulatory enforcement which creates constant demand for inspection testing and certification services at stadiums arenas and large-scale entertainment venues. The market expansion for sports infrastructure modernization and venue safety system upgrades in major U.S. metropolitan areas occurs at a faster rate because of high-density urban entertainment areas which require more strict compliance standards.

The need to enhance spectator safety, minimize risk and maximize operational efficiency drives the current increase in adoption. Stadium operators, event organizers and facility management authorities require compliance assurance, performance reliability and safety certification standards as their primary needs. TIC services adoption gets structured support through U.S. public safety frameworks and federally funded infrastructure development programs which create ongoing demand for advanced inspection and certification solutions during the forecast period.

Market Restraints / Challenges

The market has strong growth potential but companies struggle with high compliance expenses and complicated safety certification regulations which create multiple levels of approval challenges. Service providers face increased operational expenses from structural integrity requirements, occupational safety standards and venue certification regulations which create difficulties for small TIC companies in price-sensitive markets.

Organizations face operational problems because they depend on advanced inspection technologies, specialized testing equipment and skilled technical personnel. The execution process gets stalled because organizations face two challenges which include a shortage of trained certification professionals and rising costs for digital compliance systems. The U.S. sports and entertainment infrastructure ecosystem short-term profitability and TIC solution deployment get affected by these restrictions and the infrastructure investment cycles and regulatory changes.

Market Opportunities

Digital compliance platforms and AI safety inspection systems need to expand their digital compliance platforms and AI-enabled safety inspection systems because sports infrastructure keeps becoming technology-driven. The demand for automated certification workflows and predictive safety monitoring tools drives service providers to develop integrated data-driven TIC solutions which meet the needs of large venue operations and live events.

The modernization of outdated sports infrastructure together with the growth of smart stadium projects presents a major opportunity for the industry. Government-supported infrastructure upgrades create long-term TIC service contracts through public-private partnerships which focus on enhancing venue safety. The industry expects real-time analytics, remote inspection technologies and cloud-based compliance tracking systems to boost operational efficiency, decision-making capabilities and customer engagement effectiveness.

US TIC Market for Sports and Entertainment Industry Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 48.60 Billion |

|

Revenue Forecast in 2035 |

USD 103.96 Billion |

|

Growth Rate |

7.9% |

|

Segments Covered in the Report |

Sourcing Type, Service Type, Industry Vertical |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

West, South, Northeast, Midwest |

|

Key Companies |

Applus+, Bureau Veritas, DNV, Eurofins Scientific, Intertek Group plc, MISTRAS Group, SGS S, TUV Nord Group, TUV Rheinland, TUV SUD |

|

Customization |

Available upon request |

US TIC Market for Sports and Entertainment Industry Segmentation

By Sourcing Type

2025 saw outsourced sourcing reach a market share of 61% because stadium operators and entertainment facility managers depended on accredited third-party inspection and certification providers. The United States sports venues establish their operational certification standards which require organizations to adhere to structural safety and crowd management requirements that exist throughout the country. Public gathering infrastructure in the current business environment makes it necessary to use external TIC service providers who specialize in their services because they provide both quality assurance and efficient compliance verification processes.

The in-house sourcing market will achieve a CAGR of 6.8% during the forecast period because sports franchises and integrated entertainment operators now use internal compliance monitoring systems alongside their digital inspection platforms. The segment experiences growth because customers require organizations to deliver quicker reporting cycles while they maintain operational control over their safety verification processes. Premium stadium networks in the United States make use of their enhanced in-house TIC capabilities to start introducing hybrid compliance management approaches in their operational framework.

By Service Type

The inspection services market reached a 44% market share during 2025 because sports and entertainment venues needed these services to assess their structural integrity and their safety requirements and their regulatory obligations. U.S. safety enforcement frameworks for public venues establish inspection requirements which enable this segment to maintain its lead in the market because these frameworks require venues to undergo regular inspections to ensure they are ready for operations and to reduce risks in areas with large crowds.

Certification services will experience the highest growth rate because their business will expand at a 7.4% CAGR during the upcoming period as more customers require their services to operate standardized compliance systems and receive official safety certifications for their sports arenas and entertainment venues. Digital certification platforms together with automated compliance workflows become more popular among organizations which helps these organizations enhance their regulatory reporting capabilities through better efficiency and transparency. Testing services generated approximately 33% of the market share because their services enable sports and entertainment facilities in the United States to validate their materials and verify equipment safety and assess infrastructure reliability.

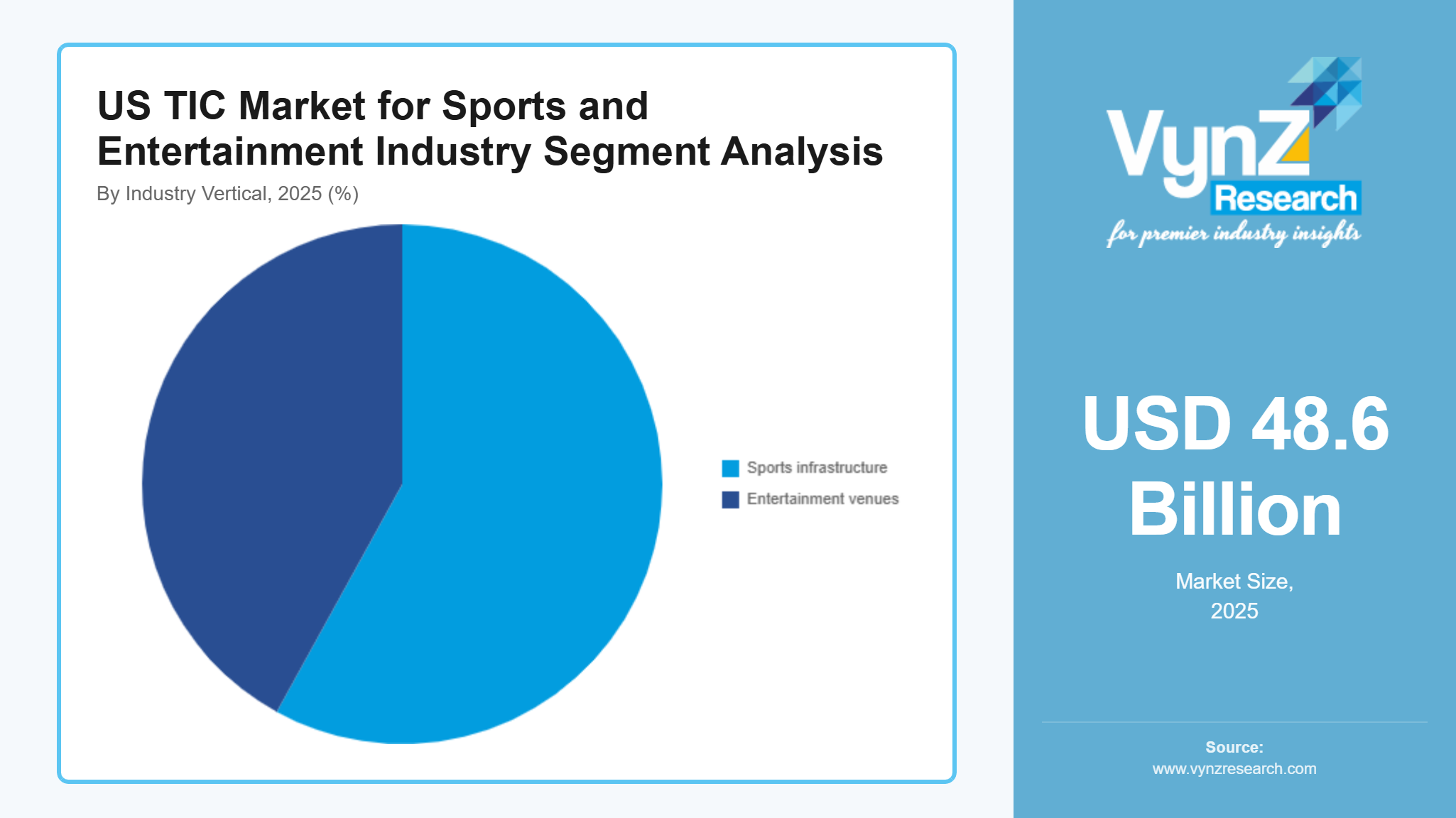

By Industry Vertical

Sports infrastructure accounted for approximately 58% of the total market share in 2025, supported by extensive development of stadiums, arenas, and training complexes across major metropolitan regions of the United States. The segment maintains its strong position in the market because safety regulations require organizations to conduct inspections which verify their compliance with structural safety and crowd control systems and emergency preparedness rules.

Entertainment venues will experience the fastest growth rate of 7.6% because businesses are now investing more money in live event spaces, concert arenas and hybrid entertainment infrastructure. The market segment experiences growth because organizations need TIC services to comply with safety regulations which have become stricter because of the increasing number of large-scale events. The U.S. market for entertainment infrastructure strengthens its regulatory compliance and operational reliability through the use of digital monitoring systems and real-time safety management solutions.

Regional Insights

West

The West United States accounted for approximately 32% of the market in 2025, driven by the presence of major sports and entertainment hubs such as Los Angeles, San Francisco, and Las Vegas. The region experiences growth because it has a high number of large stadiums and entertainment venues which include modern technology and advanced building systems. The increasing development of smart stadiums and digital safety systems in California and Nevada creates more need for inspection testing and certification work. The market keeps expanding because strict crowd safety regulations and structural compliance requirements at high-traffic entertainment sites are being enforced.

South

The South United States held approximately 28% market share in 2025, supported by rapid expansion of sports infrastructure across cities such as Dallas, Houston, Atlanta, and Miami. The region currently needs more space because it already has many stadiums which hold sporting events and people now want to build more entertainment centers. The government-backed infrastructure projects and the public venues already using safety compliance systems help TIC services to expand their market reach. The regional market performance gets stronger because organizations focus more on safety operations and risk management and they modernize their facilities.

Northeast

The Northeast United States accounted for approximately 22% of the market in 2025, driven by dense urban infrastructure, high concentration of historic and modern sports venues across cities such as New York, Boston, and Philadelphia. The region benefits from strict regulatory compliance standards and frequent inspection requirements for aging infrastructure upgrades. The continuous refurbishment of stadiums and entertainment arenas together with strict safety regulation enforcement creates ongoing demand for TIC services. The region experiences consistent market growth because of its high frequency of events and operation of premium venues.

Midwest

The Midwest United States accounted for approximately 18% of the market in 2025, supported by steady demand from cities such as Chicago, Detroit, and Minneapolis. The sports facility growth comes from organizations now modernizing their sports facilities and using safety compliance systems and public entertainment spaces are seeing more investments. The government-led city development projects and infrastructure repair efforts boost the adoption of TIC services. The Midwest area has smaller size than coastal regions but it still experiences stable growth because of ongoing regulatory enforcement and infrastructure system improvements.

Competitive Landscape / Company Insights

The market shows moderate to high competition because both international and national service providers already operate in the market with their advanced inspection technologies, compliance accuracy and digital certification capabilities. Companies are increasingly investing in digital transformation, automated testing systems and real time monitoring solutions to achieve better operational performance and compliance with regulations. The United States maintains demand for trustworthy TIC services through its government-endorsed safety frameworks and its rules for occupational compliance which force companies to improve their service standards and expand their technical skills and establish permanent contracts with sports facilities and entertainment centers.

Mini Profiles

Applus+ focuses on TIC services including inspection, testing, and certification, supported by strong engineering capabilities and global project execution strength across industrial and infrastructure safety compliance applications.

Bureau Veritas operates in premium TIC segments, emphasizing quality assurance, risk management, and certification services with strong global brand recognition and extensive regulatory compliance expertise across multiple industries.

Eurofins Scientific leverages advanced laboratory testing networks and scientific expertise to expand market presence, focusing on high-precision analytical testing and certification solutions across regulated and industrial sectors.

Intertek Group plc focuses on quality assurance, testing, inspection, and certification services, supported by strong global distribution networks and digital quality solutions enhancing operational efficiency and compliance reliability.

SGS S operates in diversified TIC segments, emphasizing inspection, testing, and certification services with strong technical expertise, global reach, and established trust across industrial safety and regulatory compliance markets.

Key Players

- Applus+

- Bureau Veritas

- DNV

- Eurofins Scientific

- Intertek Group plc

- MISTRAS Group

- SGS S

- TUV Nord Group

- TUV Rheinland

- TUV SUD

Recent Developments

In April 2026, Intertek Group plc announced strategic restructuring discussions aimed at improving efficiency across its testing, inspection, and certification operations. The company is focusing on expanding digital assurance solutions to strengthen compliance services in infrastructure-heavy sectors.

In February 2026, Bureau Veritas reported strong growth in its TIC portfolio driven by increased demand for safety, sustainability, and infrastructure certification services. The company emphasized expansion in digital inspection tools to improve regulatory compliance efficiency.

In March 2026, SGS S expanded its global TIC capabilities through increased investment in laboratory automation and advanced testing infrastructure. The company highlighted rising demand for quality assurance services across regulated industrial and infrastructure markets.

In January 2026, TUV Rheinland strengthened its certification and inspection portfolio by enhancing digital risk assessment systems for industrial safety and public infrastructure projects. The company is focusing on expanding compliance services aligned with evolving regulatory frameworks.

In May 2025, Eurofins Scientific expanded its testing and certification network by increasing laboratory capacity for high-precision analytical services. The company continues to benefit from rising demand for safety and compliance testing across regulated sectors.

US TIC Market for Sports and Entertainment Industry Coverage

Sourcing Type Insight and Forecast 2026 - 2035

- Outsourced sourcing

- In-house sourcing

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Industry Vertical Insight and Forecast 2026 - 2035

- Sports infrastructure

- Entertainment venues

End Use Insight and Forecast 2026 - 2035

- Stadium operators

- Event organizers

- Facility management companies

- Regulatory authorities

US TIC Market for Sports and Entertainment Industry by Region

- West

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By End Use

- South

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By End Use

- Northeast

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By End Use

- Midwest

- By Sourcing Type

- By Service Type

- By Industry Vertical

- By End Use

Table of Contents for US TIC Market for Sports and Entertainment Industry Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Sourcing Type

1.2.2. By

Service Type

1.2.3. By

Industry Vertical

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. US Market Estimate and Forecast

4.1. US Market Overview

4.2. US Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Sourcing Type

5.1.1. Outsourced sourcing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. In-house sourcing

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.2. By Service Type

5.2.1. Testing

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Inspection

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Certification

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.3. By Industry Vertical

5.3.1. Sports infrastructure

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Entertainment venues

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Stadium operators

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Event organizers

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Facility management companies

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. Regulatory authorities

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

6. West Market Estimate and Forecast

6.1. By

Sourcing Type

6.2. By

Service Type

6.3. By

Industry Vertical

6.4. By

End Use

7. South Market Estimate and Forecast

7.1. By

Sourcing Type

7.2. By

Service Type

7.3. By

Industry Vertical

7.4. By

End Use

8. Northeast Market Estimate and Forecast

8.1. By

Sourcing Type

8.2. By

Service Type

8.3. By

Industry Vertical

8.4. By

End Use

9. Midwest Market Estimate and Forecast

9.1. By

Sourcing Type

9.2. By

Service Type

9.3. By

Industry Vertical

9.4. By

End Use

10. Company Profiles

10.1.

Applus+

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Bureau Veritas

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

DNV

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Eurofins Scientific

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Intertek Group plc

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

MISTRAS Group

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

SGS S

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

TUV Nord Group

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TUV Rheinland

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

TUV SUD

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

US TIC Market for Sports and Entertainment Industry