Hydrogen Detection Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Product (Sensors, Detectors, Analyzers, Monitors), by Technology (Electrochemical, Catalytic, Metal Oxide Semiconductor (MOS), Thermal Conductivity, Micro Electro Mechanical Systems (MEMS)), by Implementation (Fixed, Portable), by Detection Range (0–1000 ppm, 0–5000 ppm, 0–20000 ppm, 20000 ppm), by Application (Oil & Gas, Automotive & Transportation, Chemicals, Metal & Mining, Energy & Power, Others)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9206 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 195 |

Hydrogen Detection Market Overview

The hydrogen detection market which was valued at approximately USD 289.3 million in 2025 and is estimated to reach around USD 336.5 million in 2026, is projected to reach close to USD 925.5 million by 2035, expanding at a CAGR of about 11.9% during the forecast period from 2026 to 2035.

The hydrogen detection industry is growing rapidly due to the transformation occurring within the global energy sector to low carbon alternatives. Hydrogen has emerged as an essential component in many countries' decarbonising strategies. However, hydrogen's flammability and invisibility make it necessary for organisations to implement advanced detection methods in order to ensure their facilities operate safely. These two factors have created opportunities and challenges that have driven demand for advanced detection technologies that can provide accurate detections at all times. Governments worldwide are actively developing these opportunities. Public spending on low emission hydrogen was over 38 billion dollars worldwide according to the International Energy Agency, which indicates a large investment by governments in the development of hydrogen infrastructure. Therefore, as investments continue to grow throughout the production, distribution and consumption stages of the hydrogen supply chain, safety technology will be required to support each stage.

At the same time as there is rapid expansion in hydrogen adoption among industries such as oil and gas and chemical, there is also a corresponding increase in the need for continuous monitoring technologies. Additionally, as hydrogen gains traction in mobility and fuel cell applications, the demand for hydrogen detection technologies will expand into new markets and higher growth areas. Technologically, recent advancements in sensor accuracy, miniature design and near real time data analysis capabilities are enhancing detection systems from simple alarm systems to intelligent safety networks.

Hydrogen Detection Market Dynamics

Market Trends

The most significant trend influencing the hydrogen detection industry has been the fast pace of evolution of traditional sensing technology towards intelligent, networked environments. Traditional detection products have evolved beyond detecting gas leaks to be used as platforms for delivering current data on gas leaks in real time, providing predictive intelligence on potential leak locations and remote access to monitoring stations. The fusion of existing sensor technologies such as gas with digital technologies such as IoT and AI allows companies to predict when their equipment will fail or experience a critical failure due to a leak. This trend will be especially important for those working in large scale hydrogen infrastructure projects because there is a need to continuously monitor geographically dispersed hydrogen distribution systems. Increasingly, companies are making decisions based on automation, system integration and data driven decision making versus traditional manual processes. Intelligent detection systems will likely emerge as a key business strategy by increasing operational visibility, decreasing downtime, maintenance costs and overall risk exposure throughout the hydrogen supply chain.

Growth Drivers

The most significant driving force behind the hydrogen detection industry is the growing hydrogen economy. Because many countries and industries have made commitments to reduce greenhouse gases, hydrogen is being considered as a viable alternative to fossil fuels as a sustainable energy source. The increased use of hydrogen has driven investment in the development of hydrogen generation plants, hydrogen storage tanks and hydrogen distribution pipelines. The characteristics of hydrogen that make it dangerous when handled, flammable at very low concentrations, create hazards associated with these areas. Therefore, detectors will be required to protect people, processes and property rather than providing an option. Hydrogen is also being used by industries such as oil and gas, chemicals and electric power. Furthermore, hydrogen powered vehicles are creating opportunities for detecting hydrogen. As hydrogen becomes a mainstay of energy delivery infrastructures globally, the demand for hydrogen detection systems will increase.

Market Restraints / Challenges

Although there is room to grow in demand, the hydrogen detection market has one major problem. The major problem is that it will be hard to ensure hydrogen detection systems consistently work well. Because hydrogen detection systems will most likely be placed in areas where they experience changing temperatures, humidities, pressure changes and possible gas contamination. If you place an accurate sensor in such an environment and do not take care of it properly, calibrate and maintain, you could expect unreliable results. Reliability would require advanced methods of calibration, a high frequency of maintenance and sensors designed to withstand harsh environments. This added level of reliability comes at an increased price of operation and added complexity. For many end users, the consequences of inaccurate readings or delayed detection could result in loss of life. Therefore, the need for hydrogen detection systems to operate reliably under all types of operating conditions is extremely important.

Market Opportunities

There is considerable potential in the hydrogen detection area based on its growing use throughout all stages of the hydrogen value chain as global hydrogen infrastructure expands. Each stage of hydrogen production, storage, transportation and usage has unique safety concerns and therefore requires specialised detection equipment. Thus, there exists a diverse and large market for companies providing detection related products and services. New areas of application in the form of emerging applications including green hydrogen production, decentralised energy systems and hydrogen fuelling stations provide opportunities for growth, especially in regions placing emphasis on cleaner forms of energy. The increased focus on meeting regulatory compliance and mitigating risks is driving industries to replace outdated detection equipment with improved detection technologies. Companies that can deliver high performance detection equipment that meets the changing needs of various operational environments have an opportunity to grow within this developing ecosystem.

Global Hydrogen Detection Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 289.3 Million |

|

Revenue Forecast in 2035 |

USD 925.5 Million |

|

Growth Rate |

11.9% |

|

Segments Covered in the Report |

Product, Technology, Implementation, Detection Range, Application |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

North America, Europe, Asia Pacific, Rest of the World |

|

Key Companies |

Honeywell International Inc., Teledyne Technologies Incorporated, MSA Safety Incorporated, Dragerwerk AG & Co. KGaA, Figaro Engineering Inc., H2scan Corporation, NevadaNano, Membrapor AG, SGX Sensortech, Nissha FIS Inc., Riken Keiki Co., Ltd., and Siemens AG |

|

Customization |

Available upon request |

Hydrogen Detection Market Segmentation

By Product

Detectors account for the largest share of the hydrogen detection market, around 40 % in 2025, since they provide an integrated solution for hydrogen safety in industrial settings. Detectors provide an advantage over separate sensing devices by including both the sensor that detects hydrogen and the processor that interprets signals and sends alerts. The need for ongoing monitoring is a primary reason why detectors are required for high risk applications such as oil refineries, chemical plants and hydrogen storage facilities. In addition to their performance characteristics, detectors are expected to become a major capital expense for companies that place operational safety above all else and comply with regulations. As hydrogen usage expands globally, the need for robust detection infrastructure is intensifying.

Sensors are emerging as the fastest growing category, with a CAGR of 12.2% during the forecast period. The need for precision, portability and ease of deployment of detection technologies is driving this growth. As hydrogen applications expand across multiple industry sectors, there will be a move towards module based designs with sensors integrated into equipment, vehicles and portable devices. This trend is apparent in hydrogen mobility and decentralised energy generation systems, which require continuous monitoring and real time information. Advances in technology continue to reduce costs and improve performance in terms of miniaturising and integrating digital elements into sensors. Government investments in clean hydrogen technologies, billions of dollars, will accelerate the use of hydrogen and increase demand for high performance sensing components.

By Technology

Electrochemical technology holds the largest market share, with around 35% in 2025, as no other sensor can detect such low concentrations of hydrogen as accurately. Therefore, they are required by high risk industrial environments where hydrogen is produced or processed. Their ability to provide reliable, consistent data makes them the first and usually only choice for safety critical applications. As hydrogen infrastructure expands globally, particularly in countries investing large sums into electrolyser capacity, there will be an increasing need for accurate detection technologies. An example includes a recent announcement by the European Union targeting 17.5 GW of total electrolyser manufacturing capacity by 2025. To ensure strict safety standards, electrochemical based hydrocarbon detectors are gaining popularity.

MEMS (Micro Electro Mechanical Systems technology) is emerging as the fastest growing category, growing at a CAGR of 12.5% during the forecast period due to the demand for economical, scalable and flexible hydrogen sensing technologies. These miniature hydrogen detectors have a fast response time and are able to integrate into hydrogen based transportation systems such as pipeline infrastructure, hydrogen fuel cell vehicles and small scale distributed energy applications. Their ability to support mass deployment makes them valuable as hydrogen infrastructure expands geographically. Government backed innovation is further accelerating this growth. For example, the U.S. Department of Energy’s 2026 R&D initiatives are focused on developing low cost, high volume sensor manufacturing technologies to enable widespread deployment across hydrogen pipeline networks.

By Implementation

Fixed implementation is the largest category with a market share of about 70% in 2025, due to its function as an essential safety component at all levels of hydrogen production facilities, storage terminals and refineries. The continuous operation of these fixed systems provides a constant level of leak mitigation to satisfy safety requirements. The scale of fixed implementations can be correlated with national efforts toward low carbon energy initiatives. India’s National Green Hydrogen Mission has installed over 8,000 tons per annum TPA of green hydrogen capacity through early 2026, each containing fixed detection networks for safety integration. As countries develop hydrogen clusters and industrial hubs, expansion of infrastructure reinforces fixed systems as the backbone of hydrogen safety deployment.

Portable hydrogen detection devices are witnessing the fastest growth due to increased demand for flexible detection and on site, real time monitoring across changing environments. The ability to inspect, maintain or assess emergencies provides safety beyond fixed stations. With growing transportation and decentralised energy applications using hydrogen, portable detectors remain important. Improvements in sensing technologies are providing better accuracy and reliability with simple operation. This demand for mobility and adaptability in safety solutions is positioning portable detection devices as a key growth driver in the hydrogen ecosystem.

By Detection Range

The 0–1,000 ppm detection range dominates the market, with a market share of about 40% in 2025. This detection range will continue to be important in hydrogen leak detection systems because detecting leaks at low concentrations enables operators to initiate corrective actions prior to dangerous conditions. These ranges are used in industries where safety is paramount such as chemicals, energy and manufacturing, providing assurance to comply with regulations and minimise risks. Government backed investments in hydrogen infrastructure are further emphasising the importance of safety systems, driving demand for sensitive detection solutions across the value chain.

The 0–5,000 ppm detection range is the fastest growing category because it can detect small amounts of hydrogen leakage as well as fluctuations in concentration. This wide range capability enables applications such as transportation, storage and industrial processes. There are emerging uses for hydrogen, creating demand for detection equipment capable of operating over broad ranges of hydrogen concentration. This detection range is likely to be the most adaptable to future changes in the environment in which hydrogen is used.

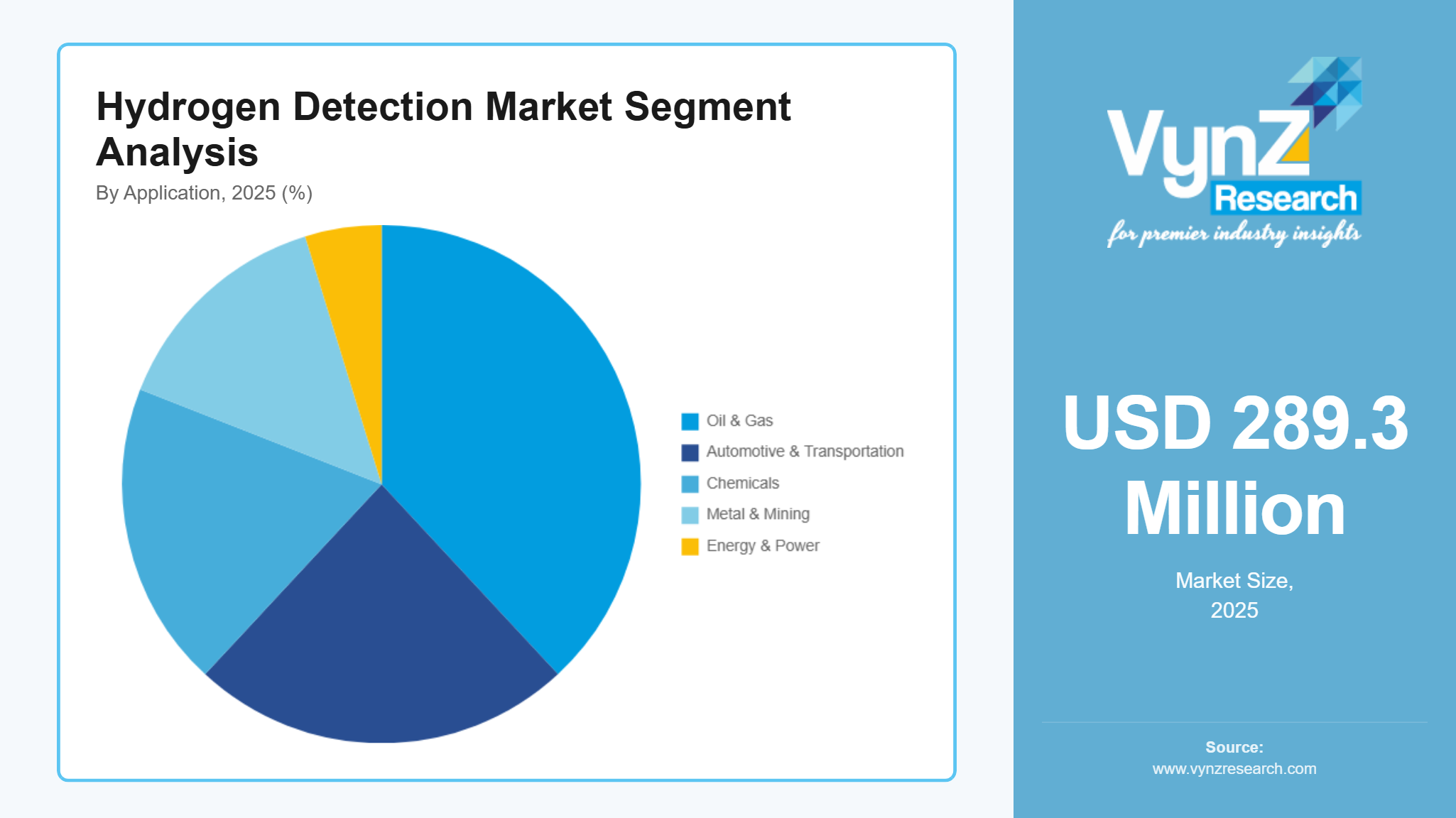

By Application

Oil and gas remain the largest application category in 2025, due to the widespread use of hydrogen in refining and industrial processes. The need for reliable detection systems ensures safe operation when using hydrogen in these processes. In addition, a well established industry base with strict safety guidelines continues to maintain a large market share. Due to the ongoing reliance on hydrogen in industrial applications, there will be high demand for detection systems in the oil and gas sector.

Automotive and transportation is the fastest growing category in the coming years, due to the high acceptance of hydrogen powered cars and hydrogen fuelling station infrastructure. Governments are adopting hydrogen as a vehicle fuel as they work towards decarbonising energy usage. The resulting investment in fuel cell technology has expanded demand for detection systems to provide safe operating conditions in vehicles and fuelling stations. Safety technologies will also play a critical role in facilitating consumer adoption of hydrogen, making this a major growth area within the industry.

Regional Insights

Asia Pacific

Asia Pacific stands as both the largest and fastest growing region in the hydrogen detection market. This can be attributed to its accelerated pace of industrialisation and increased investment in hydrogen related infrastructure. Countries driving this shift include China, Japan, South Korea and India, all having established large scale production, storage and transportation of hydrogen. These countries also have rapidly developing refining, chemicals and energy industries which continue to drive demand for safety equipment. Government backed initiatives such as India’s National Green Hydrogen Mission are accelerating the introduction of new technologies. Therefore, as hydrogen ecosystems transition into larger scale deployments, there is a significant increase in the requirement for high reliability detection equipment, and Asia Pacific will continue to lead in growth.

Europe

Europe holds a strong position in the hydrogen detection market, as the European Union has made aggressive climate goals and has a well structured policy framework that encourages the development and use of hydrogen. The EU has established funding and incentives to support green hydrogen production, along with plans for cross border transport networks and refuelling infrastructure. All of these efforts require advanced safety systems for hydrogen. In addition, strict regulatory guidelines across the EU require high performance detection technologies for industries to meet compliance standards and maintain operational safety. European countries are also focused on developing integrated hydrogen ecosystems, creating consistent demand along the value chain. Therefore, while growth is robust, the market is structured and policy driven, positioning Europe as a mature but steadily expanding region.

North America

North America remains a key market for hydrogen detection because of advancements in technology and growing investment into alternative clean energy. The U.S. and Canada have been actively developing hydrogen use in industries such as manufacturing, energy and transportation. Established research and development capabilities combined with existing industrial infrastructure enable advancement of hydrogen detection technologies. Additionally, there has been emphasis on hydrogen hubs, pipelines and fuel cell transportation which is expected to continue demand growth. While the region expands steadily, its growth is driven by technological advancements and infrastructure upgrades, positioning North America as a stable and innovation driven market within the global hydrogen detection landscape.

Rest of the World

The rest of the world, Latin America, the Middle East and Africa, is emerging as a growing market for hydrogen detection technologies. These areas are becoming increasingly interested in hydrogen opportunities, especially in green hydrogen production and exporting projects. The Middle East has invested in large scale hydrogen facilities, whereas Latin America and Africa are using renewable resources to develop a position within the hydrogen supply chain. As these projects advance, there is increasing demand for safe systems such as hydrogen detection. While this market is at an earlier stage, investments and strategic programmes will fuel the development of new hydrogen detection opportunities for suppliers.

Competitive Landscape / Company Insights

The hydrogen detection market is considered moderately fragmented. A significant amount of the market consists of established technology suppliers as well as an increasing number of smaller or regional specialised suppliers. Companies established over many years have an advantage from having a large portfolio of products, access to a wide distribution network and an existing relationship base with end users. At the same time, new entrants are focused on innovation, developing sensors that are smaller, reducing costs and integrating digital systems to create opportunities in niche areas. It is expected that competition will increasingly be based on differences in technology, reliability and the ability to provide complete safety solutions rather than individual components. For this reason, strategic alliances, agreements with suppliers of hydrogen related infrastructure and increased spending on R and D will be key ways companies grow.

Mini Profiles

Honeywell International Inc. is a global technology company delivering solutions in automation, aerospace, and energy. It focuses on improving safety, efficiency, and sustainability across industrial and commercial sectors.

Teledyne Technologies Incorporated provides advanced instrumentation, electronics, and engineered systems. The company serves specialized markets requiring high precision across industrial, aerospace, and environmental applications.

MSA Safety Incorporated develops safety products and solutions that protect workers and infrastructure. Its portfolio includes gas detection systems and protective equipment for industrial environments.

Dragerwerk AG & Co. KGaA offers medical and safety technologies focused on protecting and saving lives. The company provides gas detection and respiratory solutions for industrial and healthcare sectors.

Siemens AG is a global technology company specializing in industrial automation, smart infrastructure, and digitalization. It develops solutions that enhance efficiency and enable advanced industrial operations.

Key Players

- Honeywell International Inc.

- Teledyne Technologies Incorporated

- MSA Safety Incorporated

- Drägerwerk AG & Co. KGaA

- Figaro Engineering Inc.

- H2scan Corporation

- NevadaNano

- Membrapor AG

- SGX Sensortech

- Nissha FIS Inc.

- Riken Keiki Co., Ltd.

- Siemens AG

Recent Developments

March 2026 - Honeywell launched a new infrared gas sensor designed to enhance industrial worker safety by improving detection accuracy in hazardous environments. This innovation strengthens its portfolio in advanced gas detection and industrial automation solutions.

January 2026 - H2scan Corporation announced the launch of its HY-GUARD™ next-generation hydrogen sensor, specifically designed for battery room safety applications. The solution focuses on improving detection accuracy and reliability in high-demand environments such as data centers and energy storage systems, where hydrogen buildup can pose critical risks.

June 2025 - Honeywell announced the acquisition of Sundyne LLC for approximately $2.2 billion, aimed at strengthening its energy and sustainability solutions portfolio. This move expands its capabilities in clean fuels and industrial safety applications.

Global Hydrogen Detection Market Coverage

Product Insight and Forecast 2026 - 2035

- Sensors

- Detectors

- Analyzers

- Monitors

Technology Insight and Forecast 2026 - 2035

- Electrochemical

- Catalytic

- Metal Oxide Semiconductor (MOS)

- Thermal Conductivity

- Micro Electro Mechanical Systems (MEMS)

Implementation Insight and Forecast 2026 - 2035

- Fixed

- Portable

Detection Range Insight and Forecast 2026 - 2035

- 0–1000 ppm

- 0–5000 ppm

- 0–20000 ppm

- 20000 ppm

Application Insight and Forecast 2026 - 2035

- Oil & Gas

- Automotive & Transportation

- Chemicals

- Metal & Mining

- Energy & Power

- Others

Global Hydrogen Detection Market by Region

- North America

- By Product

- By Technology

- By Implementation

- By Detection Range

- By Application

- By Country - U.S., Canada, Mexico

- Europe

- By Product

- By Technology

- By Implementation

- By Detection Range

- By Application

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Product

- By Technology

- By Implementation

- By Detection Range

- By Application

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Product

- By Technology

- By Implementation

- By Detection Range

- By Application

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Hydrogen Detection Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Product

1.2.2. By

Technology

1.2.3. By

Implementation

1.2.4. By

Detection Range

1.2.5. By

Application

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Product

5.1.1. Sensors

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Detectors

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Analyzers

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.1.4. Monitors

5.1.4.1. Market Definition

5.1.4.2. Market Estimation and Forecast to 2035

5.2. By Technology

5.2.1. Electrochemical

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Catalytic

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.2.3. Metal Oxide Semiconductor (MOS)

5.2.3.1. Market Definition

5.2.3.2. Market Estimation and Forecast to 2035

5.2.4. Thermal Conductivity

5.2.4.1. Market Definition

5.2.4.2. Market Estimation and Forecast to 2035

5.2.5. Micro Electro Mechanical Systems (MEMS)

5.2.5.1. Market Definition

5.2.5.2. Market Estimation and Forecast to 2035

5.3. By Implementation

5.3.1. Fixed

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Portable

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.4. By Detection Range

5.4.1. 0–1000 ppm

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. 0–5000 ppm

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. 0–20000 ppm

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

5.4.4. 20000 ppm

5.4.4.1. Market Definition

5.4.4.2. Market Estimation and Forecast to 2035

5.5. By Application

5.5.1. Oil & Gas

5.5.1.1. Market Definition

5.5.1.2. Market Estimation and Forecast to 2035

5.5.2. Automotive & Transportation

5.5.2.1. Market Definition

5.5.2.2. Market Estimation and Forecast to 2035

5.5.3. Chemicals

5.5.3.1. Market Definition

5.5.3.2. Market Estimation and Forecast to 2035

5.5.4. Metal & Mining

5.5.4.1. Market Definition

5.5.4.2. Market Estimation and Forecast to 2035

5.5.5. Energy & Power

5.5.5.1. Market Definition

5.5.5.2. Market Estimation and Forecast to 2035

5.5.6. Others

5.5.6.1. Market Definition

5.5.6.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Product

6.2. By

Technology

6.3. By

Implementation

6.4. By

Detection Range

6.5. By

Application

6.5.1.

U.S. Market Estimate and Forecast

6.5.2.

Canada Market Estimate and Forecast

6.5.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Product

7.2. By

Technology

7.3. By

Implementation

7.4. By

Detection Range

7.5. By

Application

7.5.1.

Germany Market Estimate and Forecast

7.5.2.

France Market Estimate and Forecast

7.5.3.

U.K. Market Estimate and Forecast

7.5.4.

Italy Market Estimate and Forecast

7.5.5.

Spain Market Estimate and Forecast

7.5.6.

Russia Market Estimate and Forecast

7.5.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Product

8.2. By

Technology

8.3. By

Implementation

8.4. By

Detection Range

8.5. By

Application

8.5.1.

China Market Estimate and Forecast

8.5.2.

Japan Market Estimate and Forecast

8.5.3.

India Market Estimate and Forecast

8.5.4.

South Korea Market Estimate and Forecast

8.5.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Product

9.2. By

Technology

9.3. By

Implementation

9.4. By

Detection Range

9.5. By

Application

9.5.1.

Brazil Market Estimate and Forecast

9.5.2.

Saudi Arabia Market Estimate and Forecast

9.5.3.

South Africa Market Estimate and Forecast

9.5.4.

U.A.E. Market Estimate and Forecast

9.5.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

Honeywell International Inc.

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Teledyne Technologies Incorporated

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

MSA Safety Incorporated

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

Drägerwerk AG & Co. KGaA

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

Figaro Engineering Inc.

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

H2scan Corporation

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

NevadaNano

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

Membrapor AG

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

SGX Sensortech

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

Nissha FIS Inc.

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

10.11.

Riken Keiki Co., Ltd.

10.11.1.

Snapshot

10.11.2.

Overview

10.11.3.

Offerings

10.11.4.

Financial

Insight

10.11.5.

Recent

Developments

10.12.

Siemens AG

10.12.1.

Snapshot

10.12.2.

Overview

10.12.3.

Offerings

10.12.4.

Financial

Insight

10.12.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Hydrogen Detection Market