Asia TIC Market Size & Share - Growth Forecast Report (2026-2035)

Industry Insight by Service Type (Testing, Inspection, Certification), by Sourcing Type (In-house, Outsourced), by Application (Consumer Goods and Retail, Food and Agriculture, Chemicals, Construction and Infrastructure, Energy and Utilities, Oil and Gas, Industrial and Manufacturing, Automotive, Aerospace, Healthcare and Pharmaceuticals), by End Use (Industrial, Commercial, Institutional)

| Status : Published | Published On : Apr, 2026 | Report Code : VRSME9205 | Industry : Semiconductor & Electronics | Available Format :

|

Page : 168 |

Asia TIC Market Overview

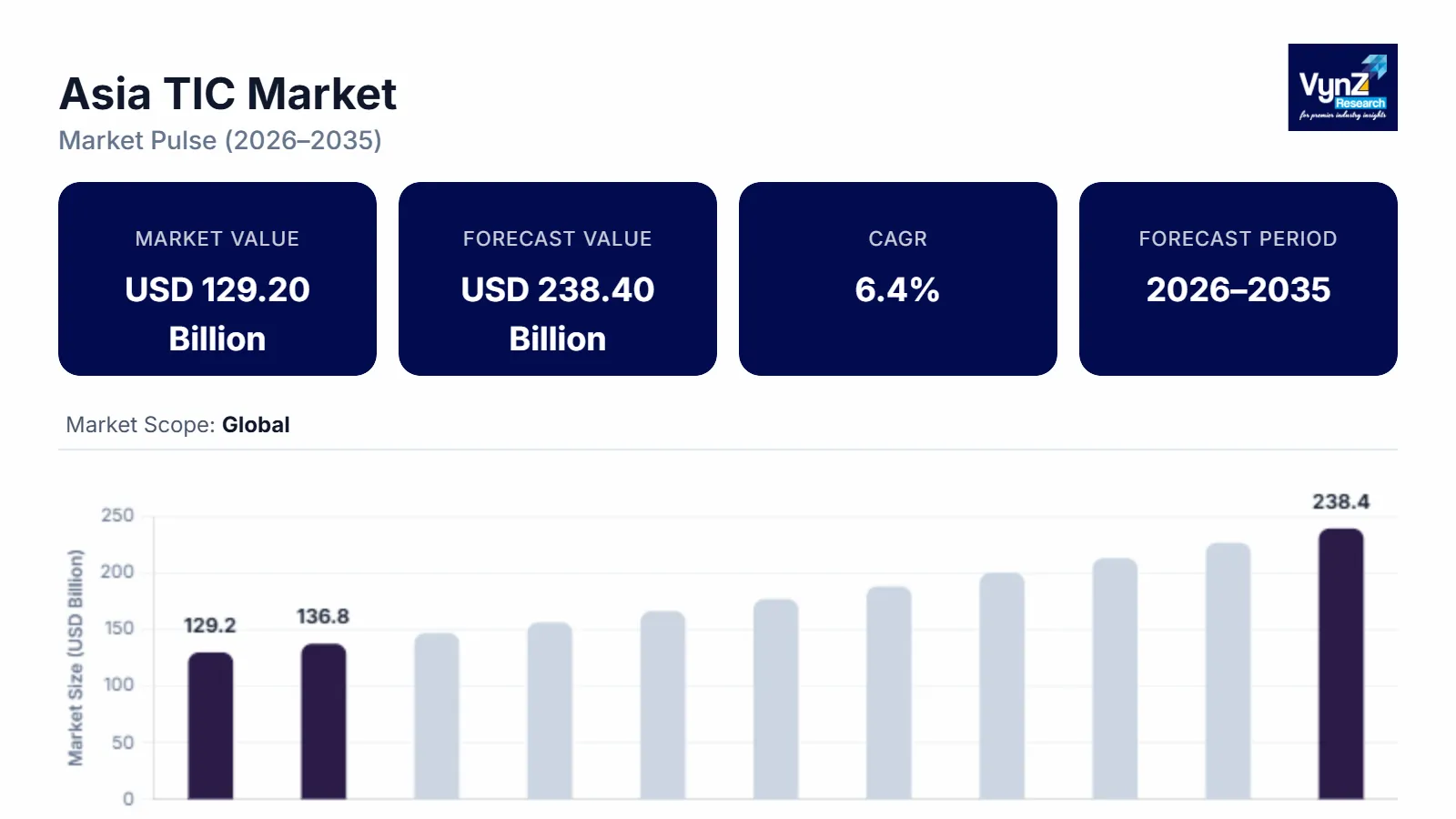

The market for testing and inspection services in Asia which had a value of about USD 129.20 billion in 2025, will reach an estimated value of USD 136.80 billion by 2026, before it expands to approximately USD 238.40 billion in 2035, with a compound annual growth rate (CAGR) of 6.4% between 2026 and 2035.

The market in Asia experiences growth because of three main factors which include industrial expansion, the need for regulatory compliance, and increased international trade, as well as the rising use of digital testing methods and automated inspection technologies. The manufacturing and consumer goods and healthcare sectors all require better quality assurance, which drives investments into standardization and accreditation systems that create economic growth in countries like China, India and Japan.

The development of quality infrastructure through government supported regulatory frameworks establishes essential components that maintain the industrial landscape. Organizations such as the World Health Organization establish strict safety and quality regulations for pharmaceuticals and medical devices and food systems, which create a direct impact on certification requirements in Asian countries. National accreditation bodies together with trade facilitation programs that meet international standards establish a system which promotes testing and inspection services based on compliance requirements. The government has increased its focus on three areas which include improving export product quality, establishing product safety regulations and industrial certification requirements. This government focus receives backing from public funding which supports laboratory infrastructure and conformity assessment systems. This combination leads to ongoing demand throughout essential Asian markets.

Asia TIC Market Dynamics

Market Trends

The industry now shifts toward complete digital systems which enable organizations to verify compliance through unified assessment methods because regulatory requirements have changed and businesses request better efficiency and supply chain tracking capabilities. The market develops through the use of automated testing systems and remote inspection methods which enable organizations to monitor operations in real time while controlling costs and minimizing work interruptions. The standardization initiatives established through government-backed quality infrastructure programs in Asia lead to the development of shared testing standards which help businesses meet international trade obligations.

The new trend appears when organizations combine digital certification platforms with data-based compliance systems, which regulatory requirements and rapid digital industry changes drive forward. The World Health Organization and other authorities require stronger pharmaceutical quality assurance, food safety and medical device quality control through established certification systems. The market developments bring new service offerings which prompt companies to create complete solutions that include digital tracking and compliance services with added value, which then transform their competitive standing throughout the region.

Growth Drivers

The Asia testing inspection and certification market expands because industrial production increases and manufacturing, healthcare and consumer goods industries face stricter regulatory enforcement. The main economies experience growing demand for inspection and certification services because industrial infrastructure investments, export production and quality assurance system development are rising. Government initiatives to promote product safety, environmental compliance and standardized production practices create a stronger demand forecast across different industrial sectors.

International trade standard compliance requires businesses to establish new standards which drive greater market demand. Testing and certification services demand continues to grow because organizations now focus on maintaining operational reliability, product quality and following all regulatory requirements. The World Health Organization and other organizations have developed reports and frameworks which demonstrate how safety validation and quality assurance are critical for essential industries, thereby showing that certified inspection and testing solutions are needed in both public and private sectors.

Market Restraints / Challenges

The market shows strong growth potential because it faces two major obstacles which include complicated regulations and expensive compliance requirements that small and medium enterprises need to adopt. The Asian countries face different regulatory requirements which create operational difficulties because companies need to constantly update their certification processes according to new regulations. Organizations need to spend more time on certification processes while they handle multiple certification requests which require their staff members to work on other tasks.

The two main operational obstacles for service providers arise from their need for technical staff members who possess expert skills and their requirement for advanced testing facilities. Government assessments of quality infrastructure in developing economies indicate gaps in laboratory capacity, accreditation systems, and technical expertise, which can lead to service bottlenecks and increased costs. The economic environment forces businesses to depend on imported technologies and specialized equipment which leads to higher costs and prevents them from expanding their operations.

Market Opportunities

The market presents significant opportunities in the expansion of digital and automated testing solutions, particularly driven by increasing industrial digitization and demand for efficient compliance management. Manufacturing, healthcare and export-driven companies will demand integrated certification services which provide scalability and technology support because they need to operate more efficiently while meeting international regulations. Government-backed initiatives to enhance national quality infrastructure and laboratory networks create better market expansion opportunities.

The development of specialized certification services for high growth sectors such as renewable energy, advanced manufacturing and pharmaceuticals represents another major market opportunity for businesses. The implementation of sustainability standards, environmental compliance procedures and product safety regulations creates new business opportunities which allow companies to develop premium products and establish enduring partnerships with customers. The upcoming data analytics, remote auditing and smart inspection systems will help organizations deliver better services while achieving higher accuracy rates, which will allow them to serve a wider range of industrial needs.

Global Asia TIC Market Report Coverage

|

Report Metric |

Details |

|

Historical Period |

2020 - 2024 |

|

Base Year Considered |

2025 |

|

Forecast Period |

2026 - 2035 |

|

Market Size in 2025 |

USD 129.20 Billion |

|

Revenue Forecast in 2035 |

USD 238.40 Billion |

|

Growth Rate |

6.4% |

|

Segments Covered in the Report |

By Service Type, By Sourcing Type, By Application, By End Use |

|

Report Scope |

Market Trends, Drivers, and Restraints; Revenue Estimation and Forecast; Segmentation Analysis; Companies’ Strategic Developments; Market Share Analysis of Key Players; Company Profiling |

|

Regions Covered in the Report |

China, India, Japan, South Korea, Rest of Asia |

|

Key Companies |

ALS Limited, Applus+, Bureau Veritas, DEKRA SE, DNV Group, Eurofins Scientific, Intertek Group plc, SGS SA, TÜV Nord Group, TÜV Rheinland, TÜV SÜD |

|

Customization |

Available upon request |

Asia TIC Market Segmentation

By Service Type

The testing sector maintained its position as the market leader in 2025 by generating approximately 62% of total revenue through its extensive use in manufacturing, healthcare, food safety and electronics industries. Testing services remain essential for regulatory compliance because authorities maintain their testing requirements which follow international standards and World Health Organization directives for pharmaceutical and food system testing. The entire Asian region experiences increased demand for product validation and safety verification and compliance testing because export-oriented businesses need these services.

The market for inspection services will experience the highest growth rate through the forecast period which will see an annual compound growth rate of 6.9% from 2026 to 2035. The adoption of real-time monitoring systems along with remote inspection technology and infrastructure development across industrial sectors drives this market growth. The rising need for on-site inspection and compliance verification services emerges from increased investments in construction, energy and transportation systems. Certification services maintain their steady growth trajectory which results from domestic and international trade operations requiring standardized quality assurance frameworks that align with regulatory standards.

By Sourcing Type

The market revenue share of outsourced services reached 57% in 2025 because businesses began to depend on third-party testing and certification services for their specialized testing requirements. The regulatory compliance requirements which require international certification together with certification barriers require companies to choose outsourced solutions. They provide accurate and efficient global certification results. Independent service providers throughout Asia gain operational strength from government-backed accreditation systems and conformity assessment programs.

The market for in-house services will experience the highest growth rate through the upcoming period which will register an annual growth rate of 6.6%. The internal quality control infrastructure improvements that multinational companies and large-scale manufacturers make lead to operational costs and turnaround time reductions within their organizations. The need for supply chain transparency, operational control and data security has driven enterprises to establish internal testing and inspection facilities. Advanced laboratory technologies and digital quality management systems create a new segment expansion opportunity to extend their use across industrial fields.

By Application

The consumer goods and retail market segment delivered the highest revenue contribution of 24% in 2025 because product turnover, safety regulations and international export demand created strong market demand. The Asian testing and certification requirements in this segment continue to grow because governments enforce product safety standards which include product labeling requirements and quality compliance standards. The rising consumer awareness about product safety and quality drives demand for products in both domestic and international markets.

The healthcare and pharmaceutical sectors will experience the highest growth potential through the upcoming period which will see an annual growth rate of 7.1%. The market expansion results from two major factors which include rising pharmaceutical production, medical device validation requirements and government regulatory standards that enforce strict industry guidelines. The World Health Organization establishes guidelines and quality standards that healthcare systems must follow to strengthen their compliance mandates. The energy sector, construction industry and automotive sector grow steadily because regional infrastructure development needs industrialization and environmental regulations.

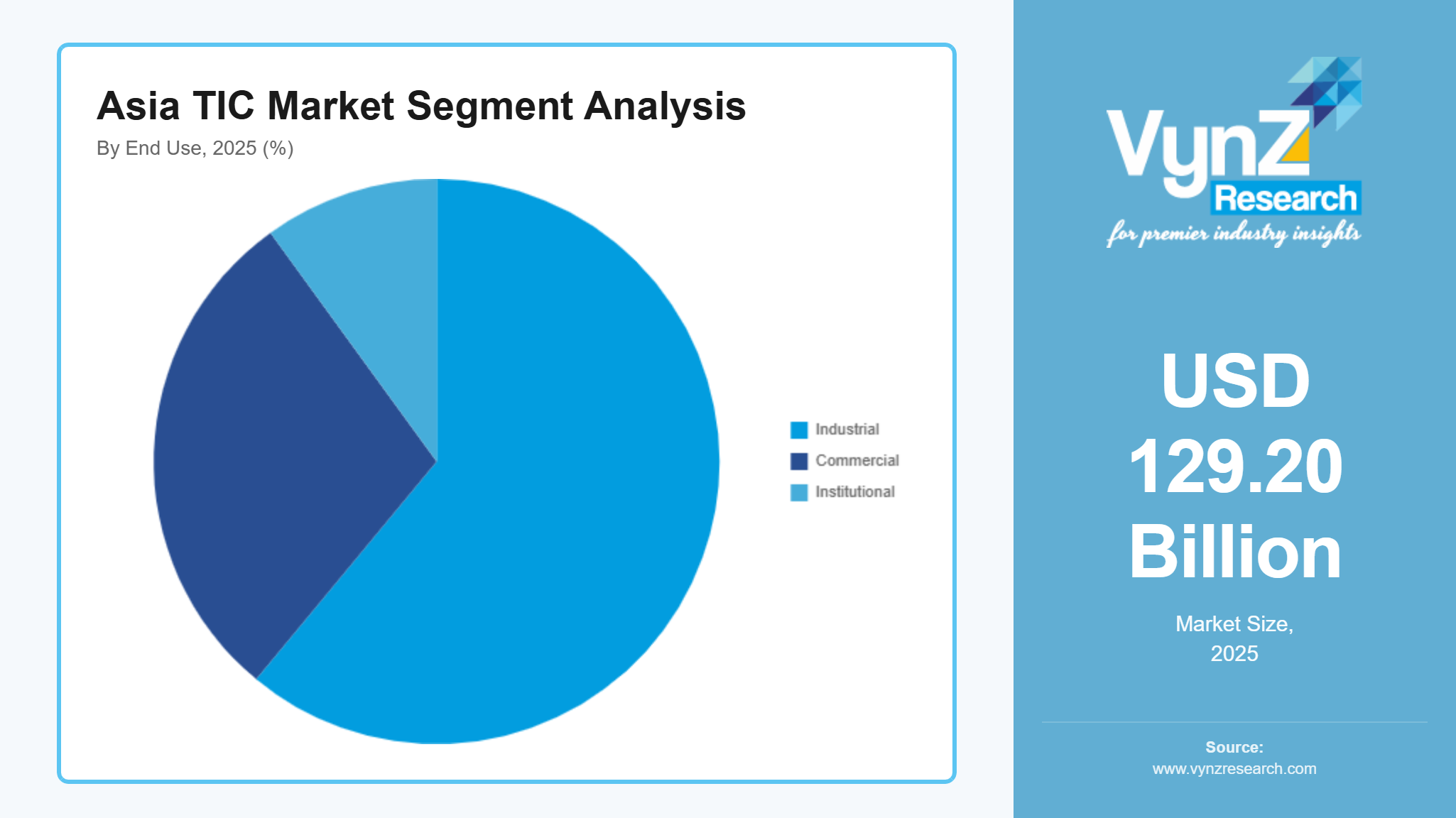

By End Use

The industrial segment generated the largest revenue share of approximately 61% in 2025 because manufacturers expanded their operations through export production and quality assurance system implementation. Asian manufacturing centers experience increased demand because government bodies promote industrial safety standards, environmental regulations and standardization requirements.

The institutional segment will become the fastest-growing segment through the coming period which will generate an annual growth rate of 6.8%. Public infrastructure development together with healthcare system growth and research center construction requires certified testing and inspection services to support these projects. The commercial application market maintains its ongoing expansion pattern because the retail sector and the logistics sector and the service sector continue to grow. The market maintains its ongoing growth because all end-use sectors show increasing demand for compliance and operational efficiency and standard quality framework implementation.

Regional Insights

China

The market in 2025 assigned China 34% percent of its total share because the country operated extensive manufacturing facilities and export-based businesses while enforcing strict rules for multiple industries which included electronics, automotive and consumer products. The testing and certification market maintains high demand from major industrial locations which include Shanghai, Shenzhen and Guangzhou. The national quality infrastructure receives enhancement through government programs which establish product quality standards, safety compliance measures and industrial standardization protocols. The domestic and international markets receive certification services, which regulatory bodies that comply with international standards and receive WHO guidance for healthcare and food safety use to promote safety.

India

The market share of India in 2025 reaches approximately 21% because the country experiences rapid industrial growth, increasing manufacturing output and rising quality control demands in pharmaceutical, food processing and construction industries. The cities of Mumbai, Delhi and Bengaluru are experiencing increased need for inspection and certification services because of their growing infrastructure and expanding export activities. The national accreditation systems and compliance frameworks which government initiatives establish will support the testing service adoption needed to improve product quality. The market for industrial and institutional sectors experiences growth because organizations have started to align their safety regulations with World Health Organization standards which apply to food and healthcare systems.

Japan

Japan holds a market share of 17% in 2025 because its advanced industrial capabilities, strict regulatory compliance practices and widespread use of precision testing technologies drive the market forward. The cities of Tokyo, Osaka and Nagoya continue to sustain demand for superior inspection and certification services. The government backing of quality assurance systems together with its support for technological development creates an environment which allows automatic digital testing systems to gain market acceptance. The testing and inspection services which key industries rely on become more vital because they handle product safety tests and environmental regulation checks and international certification standard operations.

South Korea

The market share of South Korea represents 8% for 2025 because the country contains major facilities which produce electronics, semiconductors and automotive products. The cities of Seoul and Busan serve as major centers for industrial testing and certification activities. The government initiatives which target innovation, quality control and export competitiveness will help advance inspection and testing technologies. The country experiences steady market expansion because technology-driven industries require businesses to meet international compliance standards and certification obligations.

Rest of Asia

The market share of Rest of Asia in 2025 reaches 10% because the region experiences industrial growth and foreign direct investments which lead to new manufacturing facilities across Indonesia, Thailand and Vietnam. The export markets of electronics, textiles and food processing industries drive companies to establish testing and certification programs because their products need quality assurance. The regulatory framework improvements, product safety standard enhancements and trade competitiveness enhancements which government agencies are working to establish will drive market expansion. The Asia testing inspection and certification market receives its remaining portion from other regions which have not been named, which will lead to a continuing increase in regional market demand and market expansion over time.

Competitive Landscape / Company Insights

The market has a moderate level of competition because established global and regional companies operate in the market while they develop new services, form strategic alliances and expand their operations to new territories. Companies are making greater investments in digital capabilities, laboratory infrastructure and automation technologies to improve their service efficiency and compliance accuracy. The certification processes of companies are being strengthened because organizations like the World Health Organization and national accreditation bodies establish regulatory frameworks and quality standards which they promote. Advanced testing solutions and integrated service offerings continue to be developed through ongoing investment which results in competitive advantages for companies throughout the region.

Mini Profiles

ALS Limited focuses on laboratory testing, inspection, and certification services, supported by strong global laboratory networks, technical expertise, and cost-efficient analytical solutions across environmental, food, and industrial sectors.

Bureau Veritas operates in premium and compliance driven segments, emphasizing quality assurance, risk management, and regulatory certification services tailored for industrial, infrastructure, and consumer product applications across Asia.

DEKRA SE leverages technical inspection expertise and strategic partnerships to expand market presence, offering safety testing, certification, and auditing services across automotive, industrial, and digital assurance sectors.

DNV Group focuses on risk management, certification, and advisory services, supported by strong brand recognition and expertise in energy, maritime, and sustainability assurance across regulated and high-risk industries.

Eurofins Scientific leverages advanced laboratory capabilities and digital integration to expand market presence, offering specialized testing services across pharmaceuticals, food safety, environmental analysis, and industrial applications.

Key Players

- ALS Limited

- Applus+

- Bureau Veritas

- DEKRA SE

- DNV Group

- Eurofins Scientific

- Intertek Group plc

- SGS SA

- TÜV Nord Group

- TÜV Rheinland

- TÜV SÜD

Recent Developments

In December 2025, ALS Limited was highlighted among key players expanding TIC capabilities through advanced laboratory services and sector specific testing solutions, supporting growing compliance demand across industrial and environmental applications. The company continued strengthening its global laboratory network and analytical capabilities in 2026, focusing on high precision testing services for regulated industries.

In Q3 2025, Bureau Veritas reported approximately 7.1% organic growth in its buildings and infrastructure division, driven by increasing demand for safety audits and structural inspection services. In February 2026, the company continued expanding its certification and inspection services aligned with infrastructure and compliance driven projects across global markets.

In 2025, Intertek’s industry services segment recorded steady mid-single digit growth, supported by rising demand for engineering-based inspection and asset integrity services. The company further strengthened its service portfolio in 2026 by focusing on advanced quality assurance and risk-based inspection solutions across industrial sectors.

In December 2025, SGS was recognized among leading TIC providers driving market expansion through diversified testing and certification services across industrial and consumer sectors. In 2026, the company continued to witness strong demand in its industrial division, supported by increasing focus on maintaining safety standards and regulatory compliance.

In June 2025, TÜV SÜD expanded its textile certification services across Bangladesh, India, and Vietnam after receiving approval as a certification body for sustainability standards. This expansion strengthened its position in supply chain certification and sustainable sourcing verification across key manufacturing hubs in Asia.

Global Asia TIC Market Coverage

Service Type Insight and Forecast 2026 - 2035

- Testing

- Inspection

- Certification

Sourcing Type Insight and Forecast 2026 - 2035

- In-house

- Outsourced

Application Insight and Forecast 2026 - 2035

- Consumer Goods and Retail

- Food and Agriculture

- Chemicals

- Construction and Infrastructure

- Energy and Utilities

- Oil and Gas

- Industrial and Manufacturing

- Automotive

- Aerospace

- Healthcare and Pharmaceuticals

- Electronics and Electrical

- IT and Telecommunications

- Marine and Shipping

End Use Insight and Forecast 2026 - 2035

- Industrial

- Commercial

- Institutional

Global Asia TIC Market by Region

- North America

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- By Country - U.S., Canada, Mexico

- Europe

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- By Country - Germany, U.K., France, Italy, Spain, Russia, Rest of Europe

- Asia-Pacific (APAC)

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- By Country - China, Japan, India, South Korea, Vietnam, Thailand, Malaysia, Rest of Asia-Pacific

- Rest of the World (RoW)

- By Service Type

- By Sourcing Type

- By Application

- By End Use

- By Country - Brazil, Saudi Arabia, South Africa, U.A.E., Other Countries

Table of Contents for Asia TIC Market Report

1. Research Overview

1.1. The Report Offers

1.2. Market Coverage

1.2.1. By

Service Type

1.2.2. By

Sourcing Type

1.2.3. By

Application

1.2.4. By

End Use

1.3. Research Phases

1.4. Limitations

1.5. Market Methodology

1.5.1. Data Sources

1.5.1.1.

Primary Research

1.5.1.2.

Secondary Research

1.5.2. Methodology

1.5.2.1.

Data Exploration

1.5.2.2.

Forecast Parameters

1.5.2.3.

Data Validation

1.5.2.4.

Assumptions

1.5.3. Study Period & Data Reporting Unit

2. Executive Summary

3. Industry Overview

3.1. Industry Dynamics

3.1.1. Market Growth Drivers

3.1.2. Market Restraints

3.1.3. Key Market Trends

3.1.4. Major Opportunities

3.2. Industry Ecosystem

3.2.1. Porter’s Five Forces Analysis

3.2.2. Recent Development Analysis

3.2.3. Value Chain Analysis

3.3. Competitive Insight

3.3.1. Competitive Position of Industry

Players

3.3.2. Market Attractive Analysis

3.3.3. Market Share Analysis

4. Global Market Estimate and Forecast

4.1. Global Market Overview

4.2. Global Market Estimate and Forecast to 2035

5. Market Segmentation Estimate and Forecast

5.1. By Service Type

5.1.1. Testing

5.1.1.1. Market Definition

5.1.1.2. Market Estimation and Forecast to 2035

5.1.2. Inspection

5.1.2.1. Market Definition

5.1.2.2. Market Estimation and Forecast to 2035

5.1.3. Certification

5.1.3.1. Market Definition

5.1.3.2. Market Estimation and Forecast to 2035

5.2. By Sourcing Type

5.2.1. In-house

5.2.1.1. Market Definition

5.2.1.2. Market Estimation and Forecast to 2035

5.2.2. Outsourced

5.2.2.1. Market Definition

5.2.2.2. Market Estimation and Forecast to 2035

5.3. By Application

5.3.1. Consumer Goods and Retail

5.3.1.1. Market Definition

5.3.1.2. Market Estimation and Forecast to 2035

5.3.2. Food and Agriculture

5.3.2.1. Market Definition

5.3.2.2. Market Estimation and Forecast to 2035

5.3.3. Chemicals

5.3.3.1. Market Definition

5.3.3.2. Market Estimation and Forecast to 2035

5.3.4. Construction and Infrastructure

5.3.4.1. Market Definition

5.3.4.2. Market Estimation and Forecast to 2035

5.3.5. Energy and Utilities

5.3.5.1. Market Definition

5.3.5.2. Market Estimation and Forecast to 2035

5.3.6. Oil and Gas

5.3.6.1. Market Definition

5.3.6.2. Market Estimation and Forecast to 2035

5.3.7. Industrial and Manufacturing

5.3.7.1. Market Definition

5.3.7.2. Market Estimation and Forecast to 2035

5.3.8. Automotive

5.3.8.1. Market Definition

5.3.8.2. Market Estimation and Forecast to 2035

5.3.9. Aerospace

5.3.9.1. Market Definition

5.3.9.2. Market Estimation and Forecast to 2035

5.3.10. Healthcare and Pharmaceuticals

5.3.10.1. Market Definition

5.3.10.2. Market Estimation and Forecast to 2035

5.3.11. Electronics and Electrical

5.3.11.1. Market Definition

5.3.11.2. Market Estimation and Forecast to 2035

5.3.12. IT and Telecommunications

5.3.12.1. Market Definition

5.3.12.2. Market Estimation and Forecast to 2035

5.3.13. Marine and Shipping

5.3.13.1. Market Definition

5.3.13.2. Market Estimation and Forecast to 2035

5.4. By End Use

5.4.1. Industrial

5.4.1.1. Market Definition

5.4.1.2. Market Estimation and Forecast to 2035

5.4.2. Commercial

5.4.2.1. Market Definition

5.4.2.2. Market Estimation and Forecast to 2035

5.4.3. Institutional

5.4.3.1. Market Definition

5.4.3.2. Market Estimation and Forecast to 2035

6. North America Market Estimate and Forecast

6.1. By

Service Type

6.2. By

Sourcing Type

6.3. By

Application

6.4. By

End Use

6.4.1.

U.S. Market Estimate and Forecast

6.4.2.

Canada Market Estimate and Forecast

6.4.3.

Mexico Market Estimate and Forecast

7. Europe Market Estimate and Forecast

7.1. By

Service Type

7.2. By

Sourcing Type

7.3. By

Application

7.4. By

End Use

7.4.1.

Germany Market Estimate and Forecast

7.4.2.

France Market Estimate and Forecast

7.4.3.

U.K. Market Estimate and Forecast

7.4.4.

Italy Market Estimate and Forecast

7.4.5.

Spain Market Estimate and Forecast

7.4.6.

Russia Market Estimate and Forecast

7.4.7.

Rest of Europe Market Estimate and Forecast

8. Asia-Pacific (APAC) Market Estimate and Forecast

8.1. By

Service Type

8.2. By

Sourcing Type

8.3. By

Application

8.4. By

End Use

8.4.1.

China Market Estimate and Forecast

8.4.2.

Japan Market Estimate and Forecast

8.4.3.

India Market Estimate and Forecast

8.4.4.

South Korea Market Estimate and Forecast

8.4.5.

Rest of Asia-Pacific Market Estimate and Forecast

9. Rest of the World (RoW) Market Estimate and Forecast

9.1. By

Service Type

9.2. By

Sourcing Type

9.3. By

Application

9.4. By

End Use

9.4.1.

Brazil Market Estimate and Forecast

9.4.2.

Saudi Arabia Market Estimate and Forecast

9.4.3.

South Africa Market Estimate and Forecast

9.4.4.

U.A.E. Market Estimate and Forecast

9.4.5.

Other Countries Market Estimate and Forecast

10. Company Profiles

10.1.

ALS Limited

10.1.1.

Snapshot

10.1.2.

Overview

10.1.3.

Offerings

10.1.4.

Financial

Insight

10.1.5.

Recent

Developments

10.2.

Applus+

10.2.1.

Snapshot

10.2.2.

Overview

10.2.3.

Offerings

10.2.4.

Financial

Insight

10.2.5.

Recent

Developments

10.3.

Bureau Veritas

10.3.1.

Snapshot

10.3.2.

Overview

10.3.3.

Offerings

10.3.4.

Financial

Insight

10.3.5.

Recent

Developments

10.4.

DEKRA SE

10.4.1.

Snapshot

10.4.2.

Overview

10.4.3.

Offerings

10.4.4.

Financial

Insight

10.4.5.

Recent

Developments

10.5.

DNV Group

10.5.1.

Snapshot

10.5.2.

Overview

10.5.3.

Offerings

10.5.4.

Financial

Insight

10.5.5.

Recent

Developments

10.6.

Eurofins Scientific

10.6.1.

Snapshot

10.6.2.

Overview

10.6.3.

Offerings

10.6.4.

Financial

Insight

10.6.5.

Recent

Developments

10.7.

Intertek Group plc

10.7.1.

Snapshot

10.7.2.

Overview

10.7.3.

Offerings

10.7.4.

Financial

Insight

10.7.5.

Recent

Developments

10.8.

SGS SA

10.8.1.

Snapshot

10.8.2.

Overview

10.8.3.

Offerings

10.8.4.

Financial

Insight

10.8.5.

Recent

Developments

10.9.

TÜV Nord Group

10.9.1.

Snapshot

10.9.2.

Overview

10.9.3.

Offerings

10.9.4.

Financial

Insight

10.9.5.

Recent

Developments

10.10.

TÜV Rheinland

10.10.1.

Snapshot

10.10.2.

Overview

10.10.3.

Offerings

10.10.4.

Financial

Insight

10.10.5.

Recent

Developments

11. Appendix

11.1. Exchange Rates

11.2. Abbreviations

Note: Financial insight and recent developments of different companies are subject to the availability of information in the secondary domain.

Frequently Asked Questions

Purchase Options

Latest Report

Research Methodology

- Desk Research / Pilot Interviews

- Build Market Size Model

- Research and Analysis

- Final Deliverable

Connect With Our Sales Team

- Toll-Free: +1-888-253-3960

- Phone: +91 9960 288 381

- Email: enquiry@vynzresearch.com

Asia TIC Market